|

市場調查報告書

商品編碼

2044052

亞太地區車載內建軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031)Asia-Pacific Vehicle-Embedded Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

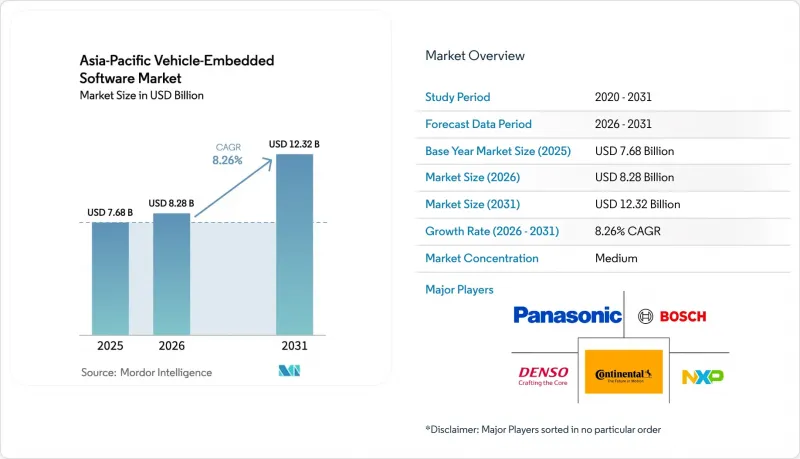

預計亞太地區汽車內建軟體市場規模將從 2025 年的 76.8 億美元成長到 2026 年的 82.8 億美元,然後在 2031 年達到 123.2 億美元,2026 年至 2031 年的複合年成長率為 8.26%。

電氣化的普及、高級駕駛輔助功能的強制實施以及向集中式運算平台的快速轉型,正推動單車軟體支出以遠超硬體成本的速度成長。諸如中國的GB 44495-2024和日本修訂的《道路運輸車輛法》等新的網路安全法規,正在加速從分散式電控系統向依賴可擴展中間件的區域和域架構的過渡。開放原始碼的AUTOSAR Adaptive協定堆疊和基於Linux的作業系統降低了區域供應商的進入門檻,而空中下載(OTA)更新生態系統則為原始設備製造商(OEM)開闢了售後收入來源。隨著中國軟體公司、印度工程服務供應商和全球一級供應商競相交付能夠按時通過ISO 26262審核的檢驗程式碼庫,亞太車載內建軟體市場的競爭日益激烈。

亞太地區車載內建軟體市場趨勢及洞察。

加速乘用車電氣化進程

預計到2025年,電池式電動車(BEV)交車量將超過950萬輛,佔乘用車銷量的38%,將推動軟體管理電池管理系統的需求。印度製造商正在將即時作業系統整合到售價低於1500美元的踏板車中,以實現對磷酸鋰鐵鋰電池組的控制和續航里程預測功能。日本將於2025年4月生效的燃油效率法規將強制要求在型式認證過程中進行基於軟體的動力傳動系統最佳化,一級供應商正與半導體合作夥伴共同參與演算法開發。目前,每款高階電動轎車的代碼量都超過3億行,是以往車型的三倍,這為中間件的商機。

中國和日本強制實施ADAS(先進駕駛輔助系統)

中國將於2026年1月強制實施自動緊急煞車和車道維持輔助系統,預計每年將有約2,500萬輛新車配備該系統。 2025年3月,日本修訂了《道路運輸車輛法》的部分內容,將主動式車距維持定速系統(ACC)納入3.5噸及以上卡車的強制安裝範圍,擴大了ADAS在商用車領域的應用。 2025年,瑞薩電子向豐田交付了超過200萬顆R-Car V4H晶片,協助將ADAS和資訊娛樂系統的處理負載整合到單一運算域中。大陸集團的CAEdge平台透過將神經網路預處理卸載到專用加速器,實現了15毫秒的偵測延遲。符合ASIL-D標準的安全功能檢驗需要額外增加18個月的發布週期,這將進一步加強全部區域OEM廠商和供應商之間的合作。

車輛ECU中的網路安全漏洞

根據聯合國R155合規性審計,23%的傳統架構缺乏硬體加密功能,迫使原始設備製造商(OEM)維修,每輛車的成本超過40美元。香港計劃於2026年12月前遵守R155和R156標準,這將對從灰色市場進口的車輛產生新的維修需求。中國的GB 44495-2024標準要求在整個生命週期內進行網路安全管理,並推動部署基於雲端的安全營運中心,以監控CAN總線流量中的異常情況。半導體短缺正在延緩安全增強型微控制器的部署,從而延長了已知漏洞的暴露時間。

細分市場分析

受印度和東南亞新創企業推動,摩托車市場預計將以9.23%的複合年成長率成長。這些新創公司將Linux儀錶板、藍牙和遠端診斷功能整合到售價低於1500美元的踏板車中。乘用車市場將受惠於中國2,100萬輛的年產量和日本的電子技術傳統,預計到2025年將佔據亞太地區汽車內建軟體市場55.21%的佔有率。輕型商用車正在整合車隊遠端資訊處理系統,以滿足韓國和澳洲強制執行的即時追蹤要求。重型卡車正在採用預測性維護技術,透過分析振動和油質數據,將意外停機時間減少15%。

儘管摩托車銷售成長強勁,但乘用車仍是亞太地區車載內建軟體市場最大的收入來源。然而,在印尼和菲律賓,為了控制成本,價格敏感型轎車通常會省略高級中間件。輕型貨車則受益於強制性的電子記錄設備,從而提高了每輛車的軟體收入。重型商用車則為預測性維護平台支付了更高的平均售價,這些平台僅在感測器檢測到異常時才安排服務預約,這進一步擴大了車載內建軟體的利潤空間。

由於區域控制器需要服務導向的框架來協調異質處理器之間的數據,中間件預計將以9.56%的複合年成長率成長。至2025年,應用軟體在亞太地區車載內建軟體市場規模中佔比將達到38.43%,但目前正轉向容器化部署以加速更新。作業系統正趨向資訊娛樂系統採用Linux,而安全功能則採用QNX及類似的微內核,從而實現通用工具鏈。隨著價值向更高層級轉移,韌體收入相應下降。

一級供應商擴大提供針對特定系統晶片(SoC) 最佳化的專有中間件包,這增加了汽車製造商的切換成本。像 COVESA 這樣的聯盟正在發布開放介面定義以維持互通性。因此,性能最佳化的封閉式協議堆疊和開放的社群程式碼正在並存,迫使亞太地區汽車內建軟體產業的原始設備製造商 (OEM) 在產品上市時間和長期供應商鎖定之間尋求平衡。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加速乘用車電氣化進程

- 中國和日本強制實施ADAS(先進駕駛輔助系統)

- 空中下載 (OTA) 更新生態系統正在各個原始設備製造商 (OEM) 中普及

- 一級廠商採用開放原始碼AUTOSAR

- 新興的軟體定義車輛(SDV)架構

- 面向自動駕駛班車的AI嵌入式平台

- 市場限制因素

- 車輛ECU中的網路安全漏洞

- 功能安全認證開發人員短缺

- 低價摩托車製造商面臨增加物料清單 (BOM) 成本的壓力

- 亞太地區監管格局的碎片化

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 車輛類型

- 搭乘用車

- 輕型商用車

- 大型商用車輛

- 摩托車

- 軟體類型

- 作業系統

- 中介軟體

- 應用軟體

- 韌體

- 透過使用

- ADAS及安全性

- 資訊娛樂

- 動力傳動系統

- 車輛控制和舒適性

- 車載資訊系統

- 依推進類型

- 內燃機

- 電池式電動車

- 油電混合車

- 燃料電池電動車

- 國家

- 中國

- 日本

- 韓國

- 印度

- 澳洲和紐西蘭

- 亞太其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Robert Bosch GmbH

- Denso Corporation

- Continental AG

- Panasonic Holdings Corporation

- NXP Semiconductors NV

- Renesas Electronics Corporation

- BlackBerry Limited

- NVIDIA Corporation

- Qualcomm Incorporated

- Elektrobit Automotive GmbH

- ETAS GmbH

- Tata Elxsi Limited

- KPIT Technologies Limited

- Aptiv PLC

- Huawei Technologies Co. Ltd.

- Baidu Inc.

- Hyundai AutoEver Corporation

- Mahindra Electric Automobile Limited

- Fujitsu Limited

- Hitachi Ltd.

第7章 市場機會與未來展望

The Asia-Pacific vehicle-embedded software market size is expected to grow from USD 7.68 billion in 2025 to USD 8.28 billion in 2026 and is forecast to reach USD 12.32 billion by 2031 at 8.26% CAGR over 2026-2031.

Pervasive electrification, mandatory advanced driver assistance functions, and the rapid pivot toward centralized compute platforms are expanding software spend per vehicle far faster than hardware costs. New cybersecurity mandates such as China's GB 44495-2024 and Japan's revised Road Transport Vehicle Act are accelerating the migration from distributed electronic control units to zonal and domain architectures that rely on scalable middleware. Open-source AUTOSAR Adaptive stacks and Linux-based operating systems are lowering entry barriers for regional suppliers, while over-the-air update ecosystems are unlocking post-sale revenue streams for original equipment manufacturers. Competitive intensity is rising as Chinese software houses, Indian engineering service providers, and global tier-1s race to deliver validated code bases that can pass ISO 26262 audits on compressed timelines within the Asia-Pacific vehicle-embedded software market.

Asia-Pacific Vehicle-Embedded Software Market Trends and Insights

Accelerating Electrification of Passenger Cars

Battery electric vehicle deliveries in China surpassed 9.5 million units in 2025, accounting for 38% of passenger-car sales and driving demand for software-managed battery management systems. Indian manufacturers embed real-time operating systems in sub-USD 1,500 scooters to regulate lithium iron phosphate packs and deliver predictive range functions. Japan's April 2025 efficiency rules require software-validated power-train optimization during type approval, pulling tier-1s into joint algorithm development with semiconductor partners. Each premium electric sedan now ships with more than 300 million lines of code, triple the load of a conventional model, magnifying middleware revenue opportunities.

Mandatory Advanced Driver Assistance Systems in China and Japan

China's automatic emergency braking and lane-keeping mandate effective January 2026 covers roughly 25 million new vehicles a year. Japan amended its Road Transport Vehicle Act in March 2025 to extend adaptive cruise control to trucks over 3.5 tons, widening ADAS reach into commercial fleets. Renesas shipped over 2 million R-Car V4H chips to Toyota in 2025, supporting consolidation of ADAS and infotainment loads on one compute domain. Continental's CAEdge platform reaches 15-millisecond detection latency by offloading neural-net preprocessing to dedicated accelerators. Functional-safety validation at ASIL-D continues to add up to 18 months to release cycles, driving tighter OEM-supplier collaboration across the region.

Cybersecurity Vulnerabilities in Vehicle ECUs

UN R155 compliance audits show 23% of legacy architectures lack hardware cryptography, forcing OEM retrofits costing more than USD 40 per unit. Hong Kong will align with R155 and R156 by December 2026, adding fresh retrofit demand across gray-market imports. China's GB 44495-2024 mandates full-lifecycle cybersecurity management, spurring cloud-based security operation centers that watch CAN-bus traffic for anomalies. Semiconductor shortages slow the rollout of security-enhanced microcontrollers, extending exposure windows for known vulnerabilities.

Other drivers and restraints analyzed in the detailed report include:

- Over-The-Air Update Ecosystems Scaling Across OEMs

- Emerging Software-Defined Vehicle Architectures

- Scarcity of Functional Safety-Certified Developers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Two-wheelers are projected to expand at 9.23% CAGR, propelled by Indian and Southeast Asian start-ups that bundle Linux dashboards, Bluetooth, and remote diagnostics into scooters below USD 1,500. Passenger cars retained 55.21% of Asia-Pacific vehicle-embedded software market share in 2025, buoyed by China's 21 million-unit output and Japan's electronics heritage. Light commercial vehicles integrate fleet telematics to comply with real-time tracking mandates in South Korea and Australia. Heavy trucks adopt predictive maintenance that analyzes vibration and oil quality data, reducing unplanned downtime by 15%.

While two-wheelers drive unit growth, passenger cars remain the largest revenue engine for the Asia-Pacific vehicle-embedded software market size, yet cost-sensitive sedans in Indonesia and the Philippines often strip advanced middleware to hit target price points. Light-duty vans benefit from mandated electronic logging devices, fostering incremental software sales per vehicle. Heavy commercial vehicles pay higher average selling prices for prognostics platforms that schedule service visits only when sensors flag abnormal patterns, further widening embedded software margins.

Middleware is forecast to rise at 9.56% CAGR as zonal controllers need service-oriented frameworks that broker data among heterogeneous processors. Application software held 38.43% of Asia-Pacific vehicle-embedded software market size in 2025, yet is shifting to containerized deployment for faster updates. Operating systems converge around Linux for infotainment and QNX or similar microkernels for safety, enabling common toolchains. Firmware revenue declines proportionally as value migrates upward.

Tier-1s increasingly offer proprietary middleware bundles tuned to specific system-on-chips, raising switching costs for automakers. Consortia such as COVESA publish open interface definitions to preserve interoperability. The resulting blend of closed performance-optimized stacks and open community code forces OEMs to balance time-to-market against long-term vendor lock-in across the Asia-Pacific vehicle-embedded software industry.

The Asia-Pacific Vehicle-Embedded Software Market Report is Segmented by Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Software Type (Operating System, Middleware, Application Software, and Firmware), Application (ADAS and Safety, Infotainment, Powertrain, and More), Propulsion Type (Internal Combustion Engine, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Robert Bosch GmbH

- Denso Corporation

- Continental AG

- Panasonic Holdings Corporation

- NXP Semiconductors N.V.

- Renesas Electronics Corporation

- BlackBerry Limited

- NVIDIA Corporation

- Qualcomm Incorporated

- Elektrobit Automotive GmbH

- ETAS GmbH

- Tata Elxsi Limited

- KPIT Technologies Limited

- Aptiv PLC

- Huawei Technologies Co. Ltd.

- Baidu Inc.

- Hyundai AutoEver Corporation

- Mahindra Electric Automobile Limited

- Fujitsu Limited

- Hitachi Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Electrification of Passenger Cars

- 4.2.2 Mandatory Advanced Driver Assistance Systems in China and Japan

- 4.2.3 Over-the-Air Update Ecosystems Scaling Across OEMs

- 4.2.4 Open-Source AUTOSAR Adoption by Tier-1s

- 4.2.5 Emerging Software-Defined Vehicle Architectures

- 4.2.6 AI-Centric Embedded Platforms for Autonomous Shuttles

- 4.3 Market Restraints

- 4.3.1 Cybersecurity Vulnerabilities in Vehicle ECUs

- 4.3.2 Scarcity of Functional Safety-Certified Developers

- 4.3.3 Rising BOM Cost Pressure on Low-End Two-Wheeler Makers

- 4.3.4 Fragmented Asia Pacific Regulatory Compliance Landscape

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Light Commercial Vehicles

- 5.1.3 Heavy Commercial Vehicles

- 5.1.4 Two-Wheelers

- 5.2 By Software Type

- 5.2.1 Operating System

- 5.2.2 Middleware

- 5.2.3 Application Software

- 5.2.4 Firmware

- 5.3 By Application

- 5.3.1 ADAS and Safety

- 5.3.2 Infotainment

- 5.3.3 Powertrain

- 5.3.4 Body Control and Comfort

- 5.3.5 Telematics

- 5.4 By Propulsion Type

- 5.4.1 Internal Combustion Engine

- 5.4.2 Battery Electric Vehicle

- 5.4.3 Hybrid Electric Vehicle

- 5.4.4 Fuel Cell Electric Vehicle

- 5.5 By Country

- 5.5.1 China

- 5.5.2 Japan

- 5.5.3 South Korea

- 5.5.4 India

- 5.5.5 Australia and New Zealand

- 5.5.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Denso Corporation

- 6.4.3 Continental AG

- 6.4.4 Panasonic Holdings Corporation

- 6.4.5 NXP Semiconductors N.V.

- 6.4.6 Renesas Electronics Corporation

- 6.4.7 BlackBerry Limited

- 6.4.8 NVIDIA Corporation

- 6.4.9 Qualcomm Incorporated

- 6.4.10 Elektrobit Automotive GmbH

- 6.4.11 ETAS GmbH

- 6.4.12 Tata Elxsi Limited

- 6.4.13 KPIT Technologies Limited

- 6.4.14 Aptiv PLC

- 6.4.15 Huawei Technologies Co. Ltd.

- 6.4.16 Baidu Inc.

- 6.4.17 Hyundai AutoEver Corporation

- 6.4.18 Mahindra Electric Automobile Limited

- 6.4.19 Fujitsu Limited

- 6.4.20 Hitachi Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

汽車維修軟體市場規模、佔有率和成長分析:按軟體類型、部署方式、最終用戶、組織規模、通路和地區分類-2026-2033年產業預測

汽車維修軟體市場規模、佔有率和成長分析:按軟體類型、部署方式、最終用戶、組織規模、通路和地區分類-2026-2033年產業預測 汽車軟體市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、功能、解決方案分類

汽車軟體市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、功能、解決方案分類 2026-2034年全球汽車軟體市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球汽車軟體市場規模、佔有率、趨勢和成長分析報告 汽車軟體市場:2026-2032年全球市場預測(依軟體類型、軟體層、動力系統、車輛類型、部署模式和最終用戶分類)

汽車軟體市場:2026-2032年全球市場預測(依軟體類型、軟體層、動力系統、車輛類型、部署模式和最終用戶分類) 汽車軟體市場報告:按產品類型、車輛類型、應用和地區分類(2026-2034 年)

汽車軟體市場報告:按產品類型、車輛類型、應用和地區分類(2026-2034 年) 汽車軟體市場:按車輛類型、軟體層級、電動車應用、產品/服務、應用領域、組織規模和地區分類汽車維修軟體市場:2026年至2032年全球市場預測(依應用程式、部署方式、最終用戶、車輛類型、組織規模及通路分類)

汽車軟體市場:按車輛類型、軟體層級、電動車應用、產品/服務、應用領域、組織規模和地區分類汽車維修軟體市場:2026年至2032年全球市場預測(依應用程式、部署方式、最終用戶、車輛類型、組織規模及通路分類) 汽車軟體市場規模、佔有率和趨勢分析報告:按應用、車輛類型、產品類型、驅動系統、地區和細分市場預測(2026-2033 年)

汽車軟體市場規模、佔有率和趨勢分析報告:按應用、車輛類型、產品類型、驅動系統、地區和細分市場預測(2026-2033 年) 2026年全球汽車維修軟體市場報告

2026年全球汽車維修軟體市場報告 2034年汽車軟體升級市場預測:按組件、車輛類型、部署模式、應用、最終用戶和地區分類的全球分析

2034年汽車軟體升級市場預測:按組件、車輛類型、部署模式、應用、最終用戶和地區分類的全球分析