|

市場調查報告書

商品編碼

2044034

直接到設備 (D2D) 衛星連接:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)Direct-to-Device Satellite Connectivity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

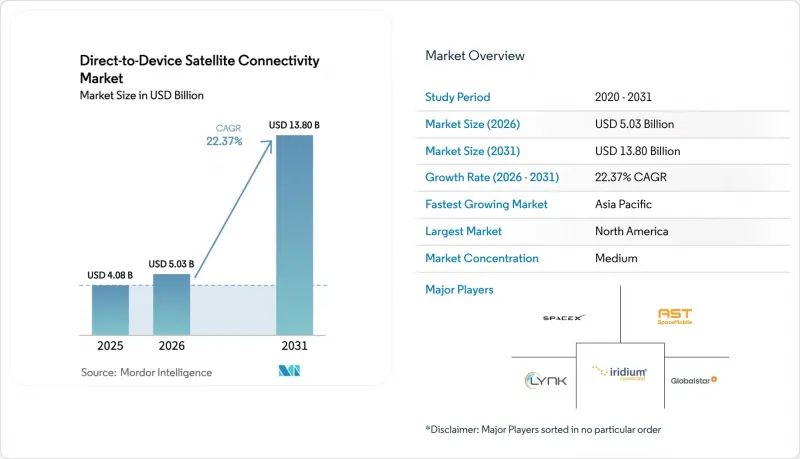

2025 年 D2D(直接到設備)衛星連接市場價值 40.8 億美元,預計到 2031 年將達到 138 億美元,而 2026 年為 50.3 億美元,預測期(2026-2031 年)複合年成長率為 22.37%。

智慧型手機和穿戴式裝置製造商迅速採用符合3GPP標準的非地面電波網路(NTN)晶片組,小型衛星發射成本不斷降低,以及主要經濟體農村地區基礎設施建設的明確要求,共同推動衛星通訊從一項小眾安全功能發展成為消費設備的主流通訊層。北美、亞太和歐洲的行動通訊業者目前正將衛星簡訊和語音通訊與高級套餐捆綁銷售,這迅速提高了消費者的認知度,並縮短了低地球軌道(LEO)衛星星系的投資回收期。每月15至20美元的價格遠低於傳統衛星電話的費用,消費者越來越願意為始終線上連線付費。同時,企業將衛星物聯網視為因應物流中斷的保障。隨著垂直整合的LEO業者利用規模經濟進行發射,以及晶片組供應商尋求橫向合作以分攤NTN整合成本,市場競爭日益激烈。

全球D2D(直接到設備)衛星連接市場趨勢與洞察

NTN相容智慧型手機的快速普及

到2025年,將有超過1.5億台具備Release-17 NTN無線功能的設備出貨,衛星連接將成為旗艦機型和高階中階機型的標配。蘋果、三星、華為以及多家安卓OEM廠商都利用橫向晶片組平台來規避專有的地面基礎設施。同時,美國聯邦通訊委員會(FCC)的「太空補充覆蓋」規則解決了美國監管方面的模糊之處。這種規模效應將使整合成本分攤到更廣泛的用戶群體,從而降低零售價格的加價,用戶在離開地面覆蓋區域時也能獲得無縫的備用連接。

透過共乘發射和可重複使用火箭降低發射成本。

SpaceX 的獵鷹 9 號共乘發射服務,通常能以低於 100 萬美元的價格將 200 公斤的有效載荷送入軌道,與 2020 年典型的單次發射火箭相比,價格降低了 60%。發射成本的降低使得像 Satelliot 和 Lynk Global 這樣的新創公司能夠透過先將少量衛星送入軌道、進行現場測試並進行改進,從而縮短衛星星系的建造時間。預計於 2026 年投入營運的藍色起源公司的新格倫火箭將擴展發射能力,並進一步強化加速部署和降低額外運力成本的良性循環。

與地面行動通訊業者(MNO)的頻段共存

行動通訊業者認為,衛星下行鏈路會干擾國際行動通訊(IMT)頻寬,降低都市區的上行鏈路品質。美國法規將有害輻射限制在-20 dBW/MHz,但歐洲尚未制定統一的閾值,且要求各國單獨核准,延緩了部署進程。缺乏先進波束成形技術的中小型衛星營運商被迫進行成本高昂的設計變更,而現有地面營運商的遊說活動則要求實施更嚴格的限制,這造成了短期部署風險。

細分市場分析

預計到2025年, L波段將佔直接到設備(D2D)衛星連接市場收入的41.53%。這主要得益於銥星和環球星數十年的資產積累,這些資產可與現有晶片組互操作,並能穿透樹木和輕型建築物。這些特性滿足了公共安全需求以及企業遠端辦公設備的需求,從而維持了龐大的部署基礎。然而,資料密集型應用場景正促使人們更加關注Ku波段和Ka波段。這些頻寬提供更寬的頻道頻寬,支援行動裝置上的視訊會議和雲端存取。 3GPP Release-18標準規範了Ka波段NTN信令,消除了先前阻礙供應商整合針對27-40 GHz鏈路最佳化的天線的監管障礙。

預計Ka波段的出貨量將以25.61%的複合年成長率成長,多家通訊業者將租賃現有的地球靜止軌道容量,在專用低地球軌道(LEO)衛星發射之前提供服務。這種混合模式既能加快產品上市速度,又能節省金錢。在預測期間內,隨著BlueBird、OneWeb-Eutelsat和Viasat等公司在未經改裝的行動電話上演示Mbps以上的通訊, Ka波段在D2D(直接到設備)衛星連接市場的佔有率預計將縮小與L波段的差距。競爭優勢將取決於先進的波束成形技術,以確保功率預算在終端限制範圍內,以及獲得調諧頻段的使用權,以避免對都市區造成干擾。這些因素可能會導致供應集中在少數幾家技術先進的廠商手中。

區域分析

預計到2025年,北美將佔全球收入的39.22%,這得益於美國聯邦通訊委員會(FCC)明確了相關法規,以及一項204億美元的農村數位機遇基金,該基金旨在津貼服務欠缺地區的衛星服務。 SpaceX和T-Mobile預計到2026年初將獲得超過300萬直接行動電話的用戶,這將支撐消費者需求,並產生網路效應,促使終端供應商推出相容NTN標準的設備。加拿大正在利用Telesat的Lightspeed LEO網路為北極和大平原地區的社區提供服務,而墨西哥正在考慮在其聯邦網路連接計劃中使用Starlink回程傳輸。創業投資的高度集中、在可重複使用火箭領域的領先地位以及對軍民兩用應用的濃厚興趣等因素,都促成了該地區的領先地位。

亞太地區預計將實現26.62%的複合年成長率,這主要得益於中國將北斗通訊技術整合到華為和小米設備中,印度行政部門決定為OneWeb-Eutelsat和Jio-SES分配頻率,從而解決了競標摩擦,以及日本KDDI-Starlink和樂天-AST SpaceMobile的合作。澳洲區域電信評估建議將衛星通訊作為內陸地區的預設選擇,Telstra目前已將Starlink回程傳輸捆綁到偏遠基地台。在韓國等人口稠密的城市市場,衛星通訊主要用於海上區域覆蓋和災害復原,但自動駕駛汽車的長期需求可能會擴大其在都市區的室內應用場景。

剩餘市佔率分佈在歐洲、南美洲以及中東和非洲。歐洲的部署尚待CEPT制定和諧共存規則,儘管已與沃達豐和橘子開展試點項目,但全面商業服務的推出仍被推遲。在巴西,Anatel強制要求在亞馬遜河流域進行網路覆蓋,並將衛星通訊定位為學校和診所唯一可擴展的解決方案。在中東和非洲,Yahsat和Thuraya為政府、能源和非政府組織使用者提供服務。成長取決於更低的設備價格和符合當地購買力的預付物聯網套餐。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- NTN相容智慧型手機的迅速普及

- 透過共乘和可重複使用火箭降低發射成本

- NTN標準化採納情形(3GPP Release-17)

- 關於農村地區醫療保險覆蓋率的國家義務(美國、印度、澳洲、巴西)

- 來自無人系統(無人機和無人地面車輛)的需求

- 新興的計量收費聯網微數據資料方案

- 市場限制因素

- 與地面電波網路營運商共存的頻段

- 行動電話設備中用戶終端功率預算的限制

- 跨境服務提供權方面的監理不確定性

- 除了 SOS 和通訊之外,其他產生收入用途有限。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 按頻段

- L波段

- S波段

- Ku波段

- Ka波段

- 其他頻段(UHF、 X波段)

- 依設備類型

- 智慧型手機

- 物聯網模組和感測器

- 穿戴式裝置

- 筆記型電腦和平板電腦

- 聯網汽車

- 按最終用戶行業分類

- 消費性電子產品

- 海上

- 航空

- 物流/運輸

- 農業

- 能源與公共產業

- 政府/國防

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Space Exploration Technologies Corp.

- AST SpaceMobile, Inc.

- Lynk Global, Inc.

- Iridium Communications Inc.

- Globalstar, Inc.

- Viasat, Inc.

- Eutelsat SA

- Omnispace LLC

- Sateliot, SL

- Skylo Technologies, Inc.

- Kepler Communications Inc.

- Al Yah Satellite Communications Company PJSC

- Hiber Global BV

- Qualcomm Incorporated

- MediaTek Inc.

- Apple Inc.

- Bullitt Group Ltd.

- Samsung Electronics Co., Ltd.

- Huawei Technologies Co., Ltd.

- T-Mobile US, Inc.

第7章 市場機會與未來展望

The Direct-to-Device Satellite Connectivity Market size was valued at USD 4.08 billion in 2025 and is estimated to grow from USD 5.03 billion in 2026 to reach USD 13.80 billion by 2031, at a CAGR of 22.37% during the forecast period (2026-2031). Rapid adoption of 3GPP-compliant non-terrestrial network (NTN) chipsets by smartphone and wearable makers, falling small-satellite launch costs, and explicit rural-coverage mandates in major economies have moved satellite links from a niche safety feature to a mainstream layer in consumer devices. Mobile network operators in North America, Asia-Pacific, and Europe now bundle satellite text and voice in premium plans, accelerating mass-market awareness and compressing payback periods for low-Earth-orbit (LEO) constellations. Consumer willingness to pay for ubiquitous coverage is helped by monthly price points of USD 15-20, well below legacy satellite-phone tariffs, while enterprises view satellite IoT as an insurance policy against logistics disruptions. Competitive intensity is rising as vertically integrated LEO players leverage launch economies of scale and chipset vendors pursue horizontal partnerships that spread NTN integration costs across many handset brands.

Global Direct-to-Device Satellite Connectivity Market Trends and Insights

Rapid Expansion of NTN-Compatible Smartphones

More than 150 million handsets shipped in 2025 with Release-17 NTN radios, making satellite connectivity a default feature in flagship and upper-midrange tiers. Apple, Samsung, Huawei, and multiple Android OEMs leveraged horizontal chipset platforms to avoid proprietary ground infrastructure, while the Federal Communications Commission's Supplemental Coverage from Space rules removed regulatory ambiguity in the United States. This scale effect spreads integration cost across a broader base, reduces retail price premiums, and primes users to expect seamless fallback when leaving terrestrial coverage.

Falling Launch Costs Due to Rideshare and Reusable Rockets

SpaceX regularly posts launch prices below USD 1 million for 200 kg payloads on Falcon 9 rideshare missions, a 60% reduction compared to typical expendable rockets in 2020. Lower launch capex lets emerging operators such as Sateliot and Lynk Global orbit small batches, test in situ, then iterate, compressing constellation build-out timelines. Blue Origin's New Glenn vehicle, expected to be online in 2026, will expand launch capacity, reinforcing a virtuous cycle of faster deployment and cheaper incremental capacity.

Spectrum Coexistence with Terrestrial MNOs

Mobile operators argue that satellite downlinks spill into International Mobile Telecommunications bands, degrading urban uplinks. While U.S. rules cap unwanted emissions at -20 dBW/MHz, Europe has yet to harmonize thresholds, forcing country-by-country approvals that slow rollouts. Smaller satellite players lacking advanced beam-forming face costly redesigns, and lobbying by terrestrial incumbents seeks even stricter limits, injecting short-term deployment risk.

Other drivers and restraints analyzed in the detailed report include:

- 3GPP Release-17 NTN Standardization Uptake

- National Rural-Coverage Mandates

- Limited Revenue-Generating Use-Cases Beyond SOS/Messaging

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

L-band captured 41.53% of 2025 revenue within the direct-to-device satellite connectivity market, benefiting from decades-old Iridium and Globalstar assets that interoperate with existing chipsets and penetrate foliage and light structures. These characteristics underpin public-safety mandates and enterprise remote-worker kits, sustaining a sizable installed base. However, data-hungry use cases are drawing attention to Ku- and Ka-bands, where wider channels enable video conferencing and cloud access on handheld devices. 3GPP Release-18 standardized Ka-band NTN signaling, clearing a regulatory hurdle that had discouraged handset vendors from integrating antennas optimised for 27-40 GHz links.

Ka-band shipments are forecast to grow at a 25.61% CAGR, and several operators are leasing existing geostationary capacity to seed service before the launch of dedicated LEO craft. This hybrid model accelerates go-to-market while preserving capital. Over the forecast, Ka-band's share of the direct-to-device satellite connectivity market size is projected to close the gap with L-band as BlueBird, OneWeb-Eutelsat, and Viasat demonstrate multi-Mbps links on unmodified phones. Competitive advantage will hinge on beam-forming sophistication that keeps power budgets within handset limits and on coordinated spectrum rights that avoid urban interference, factors likely to consolidate supply around a handful of technically advanced players.

The Direct-To-Device Satellite Connectivity Market Report is Segmented by Frequency Band (L-Band, S-Band, Ku-Band, Ka-Band, More), Device Type (Smartphones, Iot Modules and Sensors, Wearables, Laptops and Tablets, and Connected Vehicles), End-User Industry (Consumer Electronics, Maritime, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 39.22% of 2025 revenue, anchored by FCC rule clarity and the USD 20.4 billion Rural Digital Opportunity Fund, which subsidizes satellite service in unserved areas. SpaceX and T-Mobile added over 3 million direct-to-cell subscribers by early 2026, validating consumer appetite and creating network effects that encourage handset vendors to ship NTN-ready devices. Canada leverages Telesat's Lightspeed LEO network for Arctic and prairie communities, while Mexico eyes Starlink backhaul for federal connectivity programs. Venture capital density, reusable-rocket leadership, and dual-use military interest collectively sustain the region's lead.

Asia-Pacific is forecast to post a 26.62% CAGR, propelled by China's integration of Beidou messaging in Huawei and Xiaomi handsets, India's administrative spectrum allocation that removes auction friction for OneWeb-Eutelsat and Jio-SES, and Japan's KDDI-Starlink and Rakuten-AST SpaceMobile partnerships. Australia's Regional Telecommunications Review endorsed satellite as the default option for its outback, and Telstra now bundles Starlink backhaul for remote towers. Dense urban markets such as South Korea use satellite mainly for maritime coverage and disaster resilience, but long-term demand from autonomous vehicles could expand indoor urban use cases.

Europe, South America, and Middle East, and Africa split the remainder. European rollouts await harmonized coexistence rules from CEPT, delaying broad commercial service despite Eutelsat OneWeb pilots with Vodafone and Orange. Brazil's Anatel mandates coverage of the Amazon basin, positioning satellite as the only scalable solution for schools and clinics. In the Middle East and Africa, Yahsat and Thuraya serve government, energy, and NGO users; growth hinges on handset price declines and prepaid IoT plans that match local spending power.

List of Companies Covered in this Report:

- Space Exploration Technologies Corp.

- AST SpaceMobile, Inc.

- Lynk Global, Inc.

- Iridium Communications Inc.

- Globalstar, Inc.

- Viasat, Inc.

- Eutelsat S.A.

- Omnispace LLC

- Sateliot, S.L.

- Skylo Technologies, Inc.

- Kepler Communications Inc.

- Al Yah Satellite Communications Company PJSC

- Hiber Global B.V.

- Qualcomm Incorporated

- MediaTek Inc.

- Apple Inc.

- Bullitt Group Ltd.

- Samsung Electronics Co., Ltd.

- Huawei Technologies Co., Ltd.

- T-Mobile US, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Expansion of NTN-Compatible Smartphones

- 4.2.2 Falling Launch Costs Due to Rideshare and Reusable Rockets

- 4.2.3 3GPP Release-17 NTN Standardization Uptake

- 4.2.4 National Rural-Coverage Mandates (US, India, AU, BR)

- 4.2.5 Demand from Unmanned Systems (UAVs and UGVs)

- 4.2.6 Emerging Pay-As-You-Go IoT Micro-Data Plans

- 4.3 Market Restraints

- 4.3.1 Spectrum Coexistence With Terrestrial MNOs

- 4.3.2 User-Terminal Power-Budget Constraints Inside Handsets

- 4.3.3 Regulatory Uncertainty on Cross-Border Service Rights

- 4.3.4 Limited Revenue-Generating Use-Cases Beyond SOS/ Messaging

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Frequency Band

- 5.1.1 L-Band

- 5.1.2 S-Band

- 5.1.3 Ku-Band

- 5.1.4 Ka-Band

- 5.1.5 Other Frequency Bands (UHF, X-Band)

- 5.2 By Device Type

- 5.2.1 Smartphones

- 5.2.2 IoT Modules and Sensors

- 5.2.3 Wearables

- 5.2.4 Laptops and Tablets

- 5.2.5 Connected Vehicles

- 5.3 By End-User Industry

- 5.3.1 Consumer Electronics

- 5.3.2 Maritime

- 5.3.3 Aviation

- 5.3.4 Logistics and Transportation

- 5.3.5 Agriculture

- 5.3.6 Energy and Utilities

- 5.3.7 Government and Defense

- 5.3.8 Other End-user Industries

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Russia

- 5.4.3.5 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Rest of the Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Space Exploration Technologies Corp.

- 6.4.2 AST SpaceMobile, Inc.

- 6.4.3 Lynk Global, Inc.

- 6.4.4 Iridium Communications Inc.

- 6.4.5 Globalstar, Inc.

- 6.4.6 Viasat, Inc.

- 6.4.7 Eutelsat S.A.

- 6.4.8 Omnispace LLC

- 6.4.9 Sateliot, S.L.

- 6.4.10 Skylo Technologies, Inc.

- 6.4.11 Kepler Communications Inc.

- 6.4.12 Al Yah Satellite Communications Company PJSC

- 6.4.13 Hiber Global B.V.

- 6.4.14 Qualcomm Incorporated

- 6.4.15 MediaTek Inc.

- 6.4.16 Apple Inc.

- 6.4.17 Bullitt Group Ltd.

- 6.4.18 Samsung Electronics Co., Ltd.

- 6.4.19 Huawei Technologies Co., Ltd.

- 6.4.20 T-Mobile US, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

醫療保健衛星連接市場規模、佔有率和成長分析:按組件、應用、通訊方式、最終用戶和地區分類-2026-2033年產業預測

醫療保健衛星連接市場規模、佔有率和成長分析:按組件、應用、通訊方式、最終用戶和地區分類-2026-2033年產業預測 2026年全球衛星連結市場報告2026年全球企業衛星通訊服務市場報告

2026年全球衛星連結市場報告2026年全球企業衛星通訊服務市場報告 醫療保健衛星連結市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、設備、部署模式、最終用戶和解決方案分類

醫療保健衛星連結市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、設備、部署模式、最終用戶和解決方案分類 全球醫療衛星連線市場規模、佔有率、趨勢和成長分析報告(2026-2034)2025年全球醫療保健衛星連結市場報告

全球醫療衛星連線市場規模、佔有率、趨勢和成長分析報告(2026-2034)2025年全球醫療保健衛星連結市場報告 醫療保健衛星連接市場規模、佔有率、趨勢分析報告:按組件、按應用、按連接性別、按最終用途、按地區、按細分市場、預測,2024-2030 年

醫療保健衛星連接市場規模、佔有率、趨勢分析報告:按組件、按應用、按連接性別、按最終用途、按地區、按細分市場、預測,2024-2030 年