|

市場調查報告書

商品編碼

2044032

高密度電信網路:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)Telecom Network Densification - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

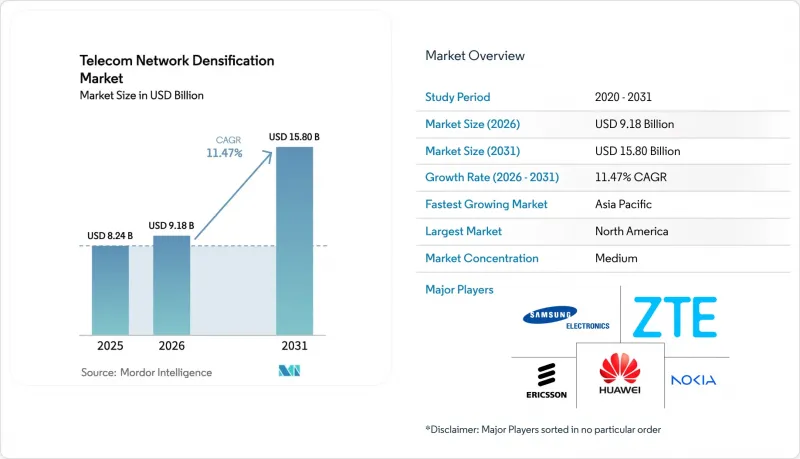

高密度電信網路市場預計將從 2025 年的 82.4 億美元成長到 2026 年的 91.8 億美元,然後從 2026 年到 2031 年以 11.47% 的複合年成長率成長,到 2031 年達到 158 億美元。

預計到2025年,每月行動資料流量將年增25%,而人口密集地區的大型基地台容量將趨於飽和,因此通訊業者正在加速部署小型基地台、分散式天線系統和毫米波節點。由於體育場館、機場和企業園區等場所對可靠覆蓋的需求,室內系統佔據主導地位,但街道層面的簡化核准流程正在推動室外節點迎來第二波成長。隨著通訊業者將廣域覆蓋與多Gigabit熱點整合,結合6GHz以下頻段和毫米波的混合架構正變得越來越普遍,而隨著建築業主將共用基礎設施貨幣化,中立經營模式也在不斷擴展。政府的5G獎勵策略進一步降低了風險,但回程傳輸光纖短缺和各城市間法規的不一致仍然阻礙著部署速度。

全球電信網路密度市場趨勢及洞察

行動數據流量快速成長和5G用戶數量成長

預計到2025年,全球行動數據消費量將達到每月140Exabyte,較2024年成長25%。此外,預計到2029年,5G用戶數將達到56億人。即使採用先進的載波聚合技術,高密度區域的大型基地台吞吐量目前僅約為10Gbps,迫使通訊業者增加基地台數量。影片串流媒體和雲端遊戲已佔總流量的70%,而即將推出的擴增實境(XR)服務預計將進一步增加上行鏈路需求。率先提高網路密度的營運商可以吸引那些追求穩定Gigabit級效能的高階用戶,而落後的營運商則面臨著客戶流失到能夠提供穩定用戶體驗(QoE)的競爭對手的風險。隨著通訊業者採用更高的網路密度和邊緣運算技術,供應商也從中受益,平均售價也隨之上漲。因此,儘管宏觀經濟不確定性,但電信網路密度提升市場仍維持兩位數的成長。

都市區容量短缺正在推動小型基地台和毫米波技術的部署。

在城市熱點地區,即使5G廣域基地台完全覆蓋,由於干擾和用戶密度高,小區邊緣吞吐量在晚高峰時段也常常低於50 Mbps。因此,通訊業者正在路燈、電線杆和建築物外牆上安裝小型基地台,以減少無線設備的面積,同時提高每個用戶的頻寬。例如,EE計劃在2025年中期在倫敦運作超過1500個城市小型基地台,以緩解宏基站的擁塞。然而,毫米波(mmWave)無線電的傳輸損耗比6 GHz以下頻段的無線電高20-30 dB,因此需要5-10倍的安裝點才能覆蓋相同的區域。像聖荷西的「一次挖掘」政策那樣,簡化一站式許可流程的市政當局可以吸引更多通訊業者的投資。相反,繁瑣的核准流程可能會使節點運作延遲一年以上。

在人口稠密的城市中,土地徵用和許可證取得過程十分複雜。

市政法規針對宏基地台塔架制定的規範很少能適用於固定在路燈桿上的背包大小的設備。紐約市的核准通常需要長達24個月,而洛杉磯透過對所有市屬電線杆主許可證,將核准時間縮短至90天。聯邦通訊委員會(FCC)2018年對每個節點每年270美元的聯邦上限仍然帶來法律挑戰,並增加了資本投資計畫的不確定性。部署數千個節點的通訊業者必須與交通部門、公共事業部門和文化遺產保護機構進行談判,而每個部門都有其獨特的工作流程。中立的主機聚合商雖然可以簡化程序,但會增加整體擁有成本,通常會收取30%至40%的利潤。因此,在資本密集型城市中心,許可證核准的延誤仍然是電信網路密度市場擴張面臨的最緊迫障礙。

細分市場分析

到2025年,室內站點將佔總收入的64.56%,成為高密度電信網路單一細分市場中最大的市場佔有率。機場、體育場館和企業園區等場所的同時上線用戶密度將超過每平方公里5萬用戶,遠遠超出室外廣域基地台的容量限制。因此,室內小型基地台和分散式天線系統(DAS)可以將每平方公尺的容量提升10到100倍。地方政府對建築物內安裝的限制很少見,這使得業主可以直接與中立的運營商簽訂契約,從而最大限度地減少獲得許可所需的時間。

預計室外節點將以12.41%的複合年成長率成長,主要得益於交通和零售商店密集區域的路燈桿和電線杆的安裝。美國聯邦通訊委員會(FCC)針對市政收費過高的規定已將合規轄區的平均核准時間從18個月縮短至不到90天。在採用主許可證框架的城市中,電力供應、電線杆接入和光纖連接的申請被整合在一起,從而減輕了通訊業者的負擔。結合室內品質保證和室外移動性需求的均衡建設計畫將有助於通訊業者在電信網路密度不斷增加的市場中提供統一的Gigabit服務並實現收益最大化。

到2025年,6GHz以下頻段的覆蓋將佔總支出的43.91%,因為它可以將站點數量和資本支出(CAPEX)控制在500至1000米半徑的範圍內。然而,通訊業者在廣域覆蓋中增加多Gigabit熱點,結合6GHz以下頻段和毫米波(mmWave)的混合方案預計到2031年將以12.98%的複合年成長率成長。美國810億美元的C頻段頻率競標是一項開創性的舉措,而在日本,NTT Docomo在東京澀谷地區利用28GHz毫米波,在距離基地台100米的範圍內實現了4Gbps的下行速度。

純毫米波的傳輸損耗比6GHz以下頻段高20-30dB,因此其應用僅限於體育場館、機場和人口密集的城市地區。 Release-17的雙頻段連接功能可讓設備同時連接到兩個頻寬,從而最佳化頻譜效率和使用者體驗。透過掌握異質頻寬間的干擾抑制和負載平衡技術,通訊業者能夠確保頻譜投資報酬率(ROI),並擴大高密度電信網路市場。

《通訊網路密度市場報告》按部署位置(室內和室外)、頻段(6 GHz 以下頻段、毫米波(24–71 GHz)以及 6 GHz 以下頻段 + 毫米波混合頻段)、應用(增強型行動寬頻(eMBB)、固定無線接取 (FWA) 等)、最終用戶(通訊業者、企業區和企業通訊網路。市場預測以美元 (USD) 為單位。

區域分析

北美地區在C頻段部署和每年運作5萬個小型基地台的支援下,預計到2025年將貢獻24.56%的收入。加拿大全國範圍內的3.5GHz頻段部署正在將覆蓋範圍擴展到農村地區,而墨西哥的強制性基礎設施共用政策則使得在降低資本支出(CAPEX)的情況下實現網路擴張成為可能。強大的中立主機生態系統和清晰的許可法規保持了高投資勢頭,但歷史上保留下來的區域仍然是部署的瓶頸。

預計亞太地區將以13.04%的複合年成長率(CAGR)領先所有地區,直至2031年,並將很快佔據電信網路密度成長的最大市場佔有率。光是中國移動就營運230萬個5G基地台,印度的Jio和Airtel計畫在2027年部署100萬個小型基地台。日本和韓國在毫米波(mmWave)部署方面處於領先地位,東南亞國協正在加快頻率競標,以實現其數位經濟目標。政府補貼和對產業園區的優惠待遇最大限度地降低了風險,早期網路密度成長主要集中在高GDP地區。

歐洲保持著15%左右的市場佔有率,歐盟的5G行動計畫要求在2030年實現所有交通走廊的5G覆蓋,這將促使路側節點密集部署。海灣合作理事會(GCC)國家正利用智慧城市計畫、杜拜世博會和沙烏地阿拉伯2030願景,快速提升網路密度和用戶均收入。非洲和南美洲雖然發展落後,但基數較低,成長率也較高,奈及利亞和巴西近期分配的頻段加速了試點部署。由於各地監管進展不一,全球供應商需要根據不同地區調整打入市場策略,才能在電信網路密度提升市場中佔有一席之地。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 行動數據流量快速成長和5G用戶數量成長

- 都市區容量短缺正在推動小型基地台和毫米波技術的部署。

- 政府和通訊業者對5G基礎設施的投資

- 企業與私有5G網路對超低延遲連結的需求

- 利用人工智慧最佳化的智慧中繼器降低部署資本支出。

- 透過整合接入回程傳輸(IAB)實現光纖精簡部署

- 市場限制因素

- 人口稠密城市中複雜的土地徵用和授權程序

- 回程傳輸光纖的可用性和成本限制

- 毫米波頻段下行/上行功率不平衡

- 能源消耗增加與永續性目標

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 按部署位置

- 室內的

- 戶外的

- 按頻段

- 低於 6 GHz

- 毫米波(24–71 GHz)

- 混合型 Sub-6 + 毫米波

- 透過使用

- 高級行動寬頻(eMBB)

- 固定無線接入(FWA)

- 工業IoT/工業4.0

- 智慧城市與公共設施

- 關鍵任務和公共安全

- 互聯出行與自動駕駛(V2X)

- 最終用戶

- 通訊業者

- 企業/專用網路主機

- 中立主機提供商

- 政府/公共安全

- 住宅/消費

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- ASEAN

- 亞太其他地區

- 中東和非洲

- GCC

- 南非

- 奈及利亞

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Huawei Technologies Co., Ltd.

- Telefonaktiebolaget LM Ericsson

- Nokia Corporation

- Samsung Electronics Co., Ltd.

- ZTE Corporation

- Qualcomm Technologies, Inc.

- CommScope Holding Company, Inc.

- Airspan Networks Holdings Inc.

- Mavenir Systems, Inc.

- NEC Corporation

- Fujitsu Limited

- Corning Incorporated

- Cisco Systems, Inc.

- Baicells Technologies Co., Ltd.

- ip.access Limited

- Radisys Corporation

- John Mezzalingua Associates, LLC

- Parallel Wireless, Inc.

- Boldyn Networks

第7章 市場機會與未來展望

The Telecom Network Densification Market size is expected to grow from USD 8.24 billion in 2025 to USD 9.18 billion in 2026 and is forecast to reach USD 15.80 billion by 2031 at 11.47% CAGR over 2026-2031.

Operators are accelerating deployments of small cells, distributed antenna systems, and millimeter-wave nodes because monthly mobile data traffic jumped 25% year-on-year through 2025, while macro-cell capacity in dense districts plateaued. Indoor systems dominate because stadiums, airports, and enterprise campuses demand guaranteed coverage, yet streamlined street-level permitting is unlocking a second growth wave for outdoor nodes. Hybrid sub-6 GHz plus mmWave architectures are gaining traction as carriers blend wide-area reach with multi-gigabit hotspots, and neutral-host business models are expanding as building owners monetize shared infrastructure. Government 5G stimulus programs further reduce risk, but backhaul fiber scarcity and fragmented municipal rules continue to temper rollout velocity.

Global Telecom Network Densification Market Trends and Insights

Surging Mobile Data Traffic and 5G Subscription Growth

Global mobile data consumption reached 140 exabytes per month in 2025, a 25% increase from 2024, and 5G subscriptions are on track to reach 5.6 billion by 2029. Macro-cell throughput in high-density corridors now levels off at around 10 Gbps, even with advanced carrier aggregation, compelling operators to increase site counts. Video streaming and cloud gaming already account for 70% of traffic, and forthcoming extended-reality services will further intensify uplink demand. Early movers that densify networks secure premium subscribers seeking stable gigabit performance, whereas laggards risk churn toward rivals with consistent quality of experience. Equipment vendors benefit as operators bundle densification with edge compute, raising average selling prices. Consequently, the Telecom network densification market continues to post double-digit gains despite macroeconomic uncertainty.

Urban Capacity Crunch Spurring Small-Cell and mmWave Rollout

Cell-edge throughput in inner-city hot spots often dips below 50 Mbps during evening peaks, even under full 5G macro coverage, mainly due to interference and high user density. Carriers therefore affix small cells to lamp posts, utility poles, and facades to shrink the radio footprint and lift per-user bandwidth. EE, for instance, activated more than 1,500 urban small cells across London by mid-2025, relieving traffic on congested macro layers. However, mmWave radios experience 20-30 dB higher path loss than sub-6 GHz radios, requiring 5-10 times as many sites to blanket the same geography. Municipalities that streamline single-touch permitting, such as San Jose's "dig-once" policy, attract greater operator capital, whereas fragmented approval chains can delay node activation by over a year.

Complex Site Acquisition and Permitting in Dense Cities

Municipal codes drafted for macro towers seldom accommodate devices the size of a backpack bolted to streetlights. New York City historically required up to 24 months for approvals, whereas Los Angeles cut timelines to 90 days via a master license on all city-owned poles. The federal caps of USD 270 per node annually, imposed by the FCC in 2018, are facing ongoing legal challenges, creating uncertainty for CAPEX planning. Carriers deploying thousands of nodes must negotiate with transportation, public works, and heritage bodies, each with its own workflows. Neutral-host aggregators reduce red tape but often capture 30-40% margins, increasing the total cost of ownership. Hence, slow permitting remains the most immediate drag on the expansion of the Telecom network densification market in capital-intensive urban cores.

Other drivers and restraints analyzed in the detailed report include:

- Government and Operator 5G Infrastructure Investments

- Enterprise/Private-5G Demand for Ultra-Low-Latency Links

- Backhaul-Fiber Availability and Cost Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Indoor sites accounted for 64.56% of 2025 revenue, the largest Telecom network densification market share for any single segment. Airports, arenas, and corporate campuses deliver concurrent user densities above 50,000 per square kilometer, far exceeding outdoor macro limits. Indoor small cells and distributed-antenna systems thus enable 10-to-100-fold capacity gains per square meter. Municipalities rarely govern in-building installations, allowing property owners to contract with neutral hosts directly and minimizing permitting delays.

Outdoor nodes will grow at a 12.41% CAGR, powered by lamp-post and utility-pole deployments along transit and retail corridors. FCC preemption of excessive municipal fees trimmed average approval timelines from 18 months to under 90 days in compliant jurisdictions. Cities adopting master-license frameworks consolidate power supply, pole access, and fiber attachment requests, reducing operator friction. Balanced build plans, indoor for guaranteed quality and outdoor for mobility, help carriers achieve uniform gigabit service and maximize Telecom network densification market size returns.

Sub-6 GHz coverage preserved 43.91% of 2025 spending because a 500-1,000-meter radius keeps site counts and CAPEX manageable. However, hybrid sub-6 GHz + mmWave approaches will post a 12.98% CAGR through 2031 as operators layer wide-area coverage with multi-gigabit hotspots. The United States' USD 81 billion C-band auction set the pace, while Japan's NTT Docomo achieved 4 Gbps downlink in Tokyo's Shibuya district using 28 GHz mmWave within 100 meters of base stations.

Pure mmWave remains specialized for stadiums, airports, and dense downtown blocks, due to 20-30 dB higher path loss than sub-6 GHz. Release-17 dual-connectivity enables devices to connect to both bands simultaneously, optimizing spectral efficiency and user experience. Operators mastering interference mitigation and load balancing across heterogeneous bands protect spectrum ROI and expand the Telecom network densification market.

The Telecom Network Densification Market Report is Segmented by Deployment Location (Indoor and Outdoor), Spectrum Band (Sub-6 GHz, Mmwave (24-71 GHz), and Hybrid Sub-6 + MmWave), Application (Enhanced Mobile Broadband (eMBB), Fixed Wireless Access (FWA), and More), End User (Telecom Operators, Enterprises and Private-Network Hosts, and More), and Geography. The Market Forecasts are in Value (USD).

Geography Analysis

North America retained 24.56% of 2025 turnover, underpinned by C-band deployments and the activation of 50,000 new small cells during the year. Canada's nationwide 3.5 GHz rollout extends coverage to rural communities, while Mexico's infrastructure-sharing mandate unlocks lower-CAPEX expansions. Robust neutral-host ecosystems and clear permitting rules keep investment momentum high, though heritage zones remain deployment bottlenecks.

Asia-Pacific is set to outpace every region, with a 13.04% CAGR through 2031, and will soon command the largest Telecom network densification market share. China Mobile alone operates 2.3 million 5G base stations, while India's Jio and Airtel plan to deploy 1 million small cells by 2027. Japan and South Korea lead mmWave adoption, while ASEAN nations accelerate auctions to fuel digital-economy goals. Governmental subsidies and industrial-park incentives minimize risk and concentrate early densification in high-GDP corridors.

Europe maintains a mid-teens share, and the EU's 5G Action Plan mandates coverage along all transport corridors by 2030, which translates into dense roadside node deployments. GCC nations leverage smart-city visions, the Dubai Expo, and Saudi Vision 2030 to densify networks swiftly, generating high per-user revenue. Africa and South America lag but exhibit high percentage growth from low bases, with Nigeria's and Brazil's recent spectrum awards jump-starting pilot rollouts. Diverse regulatory rhythms mean global vendors must tailor their go-to-market strategies by region to capture their share of the growth in the Telecom network densification market.

- Huawei Technologies Co., Ltd.

- Telefonaktiebolaget LM Ericsson

- Nokia Corporation

- Samsung Electronics Co., Ltd.

- ZTE Corporation

- Qualcomm Technologies, Inc.

- CommScope Holding Company, Inc.

- Airspan Networks Holdings Inc.

- Mavenir Systems, Inc.

- NEC Corporation

- Fujitsu Limited

- Corning Incorporated

- Cisco Systems, Inc.

- Baicells Technologies Co., Ltd.

- ip.access Limited

- Radisys Corporation

- John Mezzalingua Associates, LLC

- Parallel Wireless, Inc.

- Boldyn Networks

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Mobile Data Traffic and 5G Subscription Growth

- 4.2.2 Urban Capacity Crunch Spurring Small-Cell and mmWave Rollout

- 4.2.3 Government and Operator 5G Infrastructure Investments

- 4.2.4 Enterprise/Private-5G Demand for Ultra-Low-Latency Links

- 4.2.5 AI-Optimized Smart Repeaters Lowering Deployment CAPEX

- 4.2.6 Integrated Access and Backhaul (IAB) Enabling Fiber-Lean Roll-Outs

- 4.3 Market Restraints

- 4.3.1 Complex Site Acquisition and Permitting in Dense Cities

- 4.3.2 Backhaul-Fiber Availability and Cost Constraints

- 4.3.3 DL/UL Power Imbalance at mmWave Bands

- 4.3.4 Energy-Use Escalation Vs. Sustainability Targets

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Location

- 5.1.1 Indoor

- 5.1.2 Outdoor

- 5.2 By Spectrum Band

- 5.2.1 Sub-6 GHz

- 5.2.2 mmWave (24-71 GHz)

- 5.2.3 Hybrid Sub-6 + mmWave

- 5.3 By Application

- 5.3.1 Enhanced Mobile Broadband (eMBB)

- 5.3.2 Fixed Wireless Access (FWA)

- 5.3.3 Industrial IoT/Industry 4.0

- 5.3.4 Smart Cities and Public Venues

- 5.3.5 Mission-Critical and Public Safety

- 5.3.6 Connected and Autonomous Mobility (V2X)

- 5.4 By End User

- 5.4.1 Telecom Operators

- 5.4.2 Enterprises and Private-Network Hosts

- 5.4.3 Neutral-Host Providers

- 5.4.4 Government and Public Safety

- 5.4.5 Residential/Consumers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Nigeria

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Huawei Technologies Co., Ltd.

- 6.4.2 Telefonaktiebolaget LM Ericsson

- 6.4.3 Nokia Corporation

- 6.4.4 Samsung Electronics Co., Ltd.

- 6.4.5 ZTE Corporation

- 6.4.6 Qualcomm Technologies, Inc.

- 6.4.7 CommScope Holding Company, Inc.

- 6.4.8 Airspan Networks Holdings Inc.

- 6.4.9 Mavenir Systems, Inc.

- 6.4.10 NEC Corporation

- 6.4.11 Fujitsu Limited

- 6.4.12 Corning Incorporated

- 6.4.13 Cisco Systems, Inc.

- 6.4.14 Baicells Technologies Co., Ltd.

- 6.4.15 ip.access Limited

- 6.4.16 Radisys Corporation

- 6.4.17 John Mezzalingua Associates, LLC

- 6.4.18 Parallel Wireless, Inc.

- 6.4.19 Boldyn Networks

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Analyst Recommendations and Suggestions

小型基地台網路市場機會、成長要素、產業趨勢分析及2026-2035年預測

小型基地台網路市場機會、成長要素、產業趨勢分析及2026-2035年預測 全球小型基地台市場:2025-2031年預測

全球小型基地台市場:2025-2031年預測 2026年全球小型基地台桿市場報告2026年全球小型基地台市場報告

2026年全球小型基地台桿市場報告2026年全球小型基地台市場報告 小型基地台網路市場報告:按蜂窩類型、運行環境、最終用戶行業和地區分類,2026-2034 年

小型基地台網路市場報告:按蜂窩類型、運行環境、最終用戶行業和地區分類,2026-2034 年 小型基地台5G網路市場:按組件、基地台類型、頻段、網路類型、部署模式、應用程式和最終用戶分類-2026-2032年全球市場預測小型基地台網路市場:按類型、部署模式、技術、頻段、回程傳輸鏈路、應用和最終用戶分類——2026-2032年全球市場預測

小型基地台5G網路市場:按組件、基地台類型、頻段、網路類型、部署模式、應用程式和最終用戶分類-2026-2032年全球市場預測小型基地台網路市場:按類型、部署模式、技術、頻段、回程傳輸鏈路、應用和最終用戶分類——2026-2032年全球市場預測 小型基地台5G網路市場分析與預測(至2035年):類型、產品、服務、技術、組件、應用、部署、最終用戶、安裝模式、解決方案2026年全球小型基地台5G網路市場報告2026年全球小型基地台回程傳輸市場報告

小型基地台5G網路市場分析與預測(至2035年):類型、產品、服務、技術、組件、應用、部署、最終用戶、安裝模式、解決方案2026年全球小型基地台5G網路市場報告2026年全球小型基地台回程傳輸市場報告