|

市場調查報告書

商品編碼

2044029

電信即平台 (TAaP):市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)Telco-as-a-Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

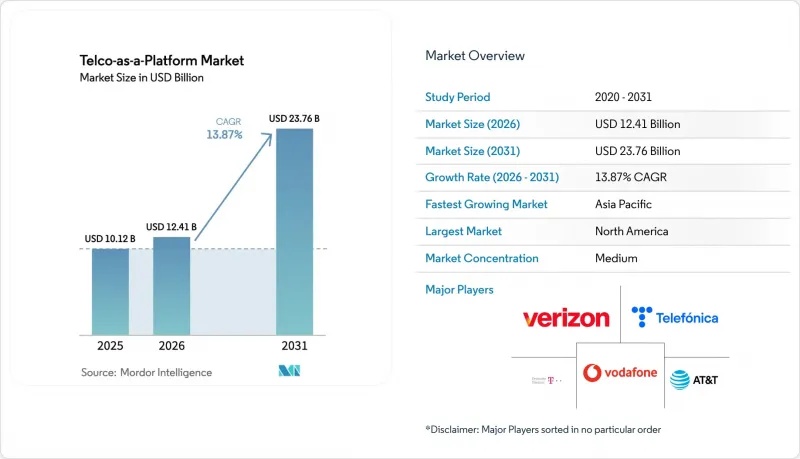

預計電信即平台 (Telco-as-a-Platform) 市場將從 2025 年的 101.2 億美元成長到 2026 年的 124.1 億美元,到 2031 年將達到 237.6 億美元,2026 年至 2031 年的複合成長率為 13.87%。

5Gスタンドアロンコアの導入拡大、多接取邊緣運算(MAEC)の商用化、およびネットワークエクスポージャーインターフェースの標準化により、業界は純粋な接続サービスから可程式設計なプラットフォームへと転換を加速させています。北米、欧州、アジア太平洋地域の通訊業者は現在、統一されたAPIを通じて、オンデマンド品質、デバイス位置情報、SIMスワップ検知機能を提供しており、これにより企業やソフトウェア開発者の統合コストを削減しています。超大規模資料中心業者との提携により、無線基地局内にクラウドコンピューティングが導入され、通訊業者は単なる頻寬の卸売業者ではなく、エッジ,クラウドのオーケストレーターとしての地位を確立しつつあります。同時に、欧州、中国、インド、および湾岸諸国におけるデータ主権に関する規制により、ローカルでの処理が求められており、コンプライアンスとスケーラビリティのバランスをとるハイブリッドプラットフォームアーキテクチャへの需要が生まれています。クラウドプロバイダー、CPaaSの専門企業、および新加入經營者が、依然としてサブスクリプション型のBSSおよびOSSスタックに依存するレガシーキャリアに挑むにつれ、競合の圧力は高まっています。

全球電信即平台 (TAAP) 市場趨勢與洞察

5G獨立核心網路的普及使得網路暴露成為可能。

獨立組網(SA)核心網引入了網路暴露功能,允許第三方軟體透過安全的北向API執行服務品質(QoS)調整、位置保障和會話管理。中國移動的目標是在2025年底前部署超過100萬個5G SA基地台,北美通訊業者也在主要都會區運作SA核心網,使即時網路切片在商業上可行。 3GPP第16版和第17版定義了底層介面,GSMA開放閘道器和Linux基金會的CAMARA專案將其映射到供開發者使用的REST API。這使得軟體團隊只需一次呼叫即可請求跨多個運營商的確認延遲。通訊業者現在不再透過統一的連接服務實現盈利,而是透過差異化的頻寬和延遲分層來實現盈利,隨著全球大部分5G連接在2028年前過渡到SA,這將創造永續的收入來源。

企業對嵌入式連線和 API 存取的需求日益成長

銀行正在採用SIM卡交換和號碼驗證電話來防止帳戶劫持詐騙,而醫院則正在為遠距離診斷部署網路切片,因為超過10毫秒的抖動是不可接受的。製造商正在利用私有5G網路結合邊緣運算來控制機器人,並使用API在換班期間頻寬。 T-Mobile的「T平台」將於2025年推出,它提供了一個自助服務市場,物流公司可以在此自動配置網路切片和物聯網連接,從而省去以往需要數週的採購週期。這種簡化的計量收費模式正在吸引那些缺乏電信專業知識的中小型企業,從而擴大了除財富500強跨國公司之外的收入來源。

傳統IT和BSS/OSS的限制阻礙了API貨幣化。

傳統的每月收費引擎無法以秒為單位計量 API 呼叫次數,也無法支援與延遲等級相關的動態定價。 Oracle 和 Amdocs 已發布了雲端原生收費方案,但遷移數百萬用戶會使通訊業者面臨用戶流失風險和收入保障缺口。 TM Forum 的「開放數位架構」藍圖正在指南重建過程,但到 2025 年,只有少數業者能夠完成試點階段。如果沒有即時策略控制,許多通訊業者將只能提供統一的套餐,從而削弱其與超大規模資料中心業者營運商的差異化優勢。

細分市場分析

預計到2025年,通訊平台即服務(CPaaS)將維持32.45%的市場佔有率,這主要得益於通訊領域的先驅者們將協定抽象化為簡單的REST調用。邊緣雲端平台目前正處於成長最快的階段,複合年成長率(CAGR)高達15.12%,主要得益於企業在無線基地台內部署微服務以避免回程傳輸。 Verizon的5G邊緣運算服務已覆蓋美國50多個大都會圈,用戶回應時間僅需10毫秒,使工廠能夠即時偵測異常情況。 GSMA開放閘道器整合了八個API系列,建構了一個連接通訊和運算的網路開放市場。

這種轉變也正在重塑收入模式。 CPaaS訊息或使用分鐘數收費,而邊緣平台收費CPU 週期、儲存空間和保證頻寬。預計到預測期末,電信即平台 (Telco-as-a-Platform) 在邊緣雲端細分市場中的佔有率將顯著成長,這反映了自動駕駛汽車、電腦視覺和身臨其境型媒體領域對現場分析的需求。 BSS/OSS 即服務解決方案透過吸引那些更傾向於外包收費和編目功能而非自行重建本地系統的區域運營商,降低了准入門檻。

儘管到2025年,公共雲端仍將佔總收入的56.43%,但由於歐盟、中國和中東部分地區嚴格的本地化法規,混合雲架構正以14.03%的複合年成長率快速成長。德國電信和谷歌雲端推出「主權雲端」技術棧,將超大規模創新與監管保障結合。此技術棧僅在德國境內儲存金鑰和元資料。企業透過將對延遲要求較高的資料包路由到邊緣節點,同時將批量分析資料傳輸到中心區域,從而在最佳化成本和合規性的同時,實現了這一目標。

プライベート展開は、規制の厳しいBFSI(銀行,金融,保険)およびヘルスケア分野に限定されたニッチな領域にとどまっています。しかし、こうした垂直市場でさえ、現在ではオンプレミス,叢集と通訊業者のエッジ全体でポリシーを統一するフェデレーテッド,編配,レイヤーに依存しています。「デジタル市場法」は、支配的なクラウドプロバイダーに互通性の支援を義務付けており、通訊業者の交渉力を強化しています。中国やインドでは、サイバーセキュリティ法により個人データの跨境移転が禁止されており、匿名化されたAPIを通じてのみ公共雲端と相互接続する国内のエッジ,グリッドが促進されています。

區域分析

預計到2025年,北美將佔全球收入的28.54%,這主要得益於早期5G SA(獨立組網)部署和雲端邊緣夥伴關係關係。 Verizon的5G Edge與AWS Wavelength合作,已在75個大都會區部署,使電商公司運作建議引擎。同時,AT&T Network Edge在100多個城市整合了Azure運算能力。 T-Mobile的市場正在加速中小企業採用5G技術。儘管美國聯邦通訊委員會(FCC)鼓勵開放式無線存取網(Open RAN)的多樣性,但各州不同的隱私法使得跨州部署變得複雜。

預計亞太地區將維持最高成長率,到2031年複合年成長率將達到14.97%。中國移動覆蓋廣泛的SA網路為工業園區提供全國性的網路服務,而Bharti Airtel的市場平台則使印度的新創企業生態系統能夠獲得號碼認證和物聯網連接。 NTT Docomo已將網路切片商業化應用於自動駕駛汽車測試。 Singatell也正與AWS合作,將新加坡打造為跨國邊緣服務的樞紐。從中國嚴格的在地化政策到新加坡的開放資料走廊,法規環境正在影響平台的設計和定價。

在歐洲,企業正受益於《數位市場法案》和《一般資料居住規範》(GDPR)等統一政策,這些政策要求開放存取和隱私權合規。德國電信、 橘子和西班牙電信正在試行聯合邊緣解決方案,這些方案在滿足資料駐留法規的同時,共享資本投資。沃達豐的 API 市場覆蓋 21 個國家,支援詐欺預防和物聯網套餐的貨幣化。中東通訊業者正利用主權雲端激勵政策,在沙烏地阿拉伯和阿拉伯聯合大公國託管政府工作負載。同時,隨著 4G 覆蓋範圍的擴大,非洲通訊業者正專注於智慧農業領域的物聯網應用。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 5G獨立核心網路的普及將使網路暴露成為可能。

- 企業對嵌入式連線和 API 存取的需求日益成長

- 轉型為連結服務以外的收入來源。

- MEC 的普及正在推動低延遲應用生態系統的發展。

- 監理機關致力於開放網路和公平准入

- 需要運營商級平台的邊緣原生 AI 工作負載

- 市場限制因素

- 傳統IT和BSS/OSS的限制阻礙了API貨幣化。

- 網路暴露API標準化的碎片化

- 企業安全和資料主權問題

- 通訊業者投資平台功能能否獲得投資報酬率存在不確定性。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 買方的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 依平台類型

- CPaaS

- 網路曝光平台(API市場)

- 邊緣雲端平台

- BSS/OSS-as-a-Service

- 其他平台類型(物聯網連接平台)

- 按部署模式

- 公共雲端

- 私有雲端

- 混合雲端

- 網路科技

- 4G/LTE

- 5G 非獨立組網 (NSA)

- 5G獨立組網(SA)

- NB-IoT 和 LPWAN

- 按公司規模

- 小型企業

- 大公司

- 按最終用戶行業分類

- 製造業

- 汽車和交通運輸

- 媒體與娛樂

- 衛生保健

- 能源與公共產業

- BFSI

- 零售與電子商務

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 肯亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Vodafone Group Plc

- Deutsche Telekom AG

- Telefonica, SA

- AT&T Inc.

- Verizon Communications Inc.

- Orange SA

- China Mobile Limited

- China Telecom Corporation Limited

- NTT DOCOMO, Inc.

- Singapore Telecommunications Limited

- Rakuten Symphony, Inc.

- Telstra Group Limited

- T-Mobile US, Inc.

- BT Group plc

- KDDI Corporation

- Swisscom AG

- Dish Network Corporation

- Ericsson AB

- Bharti Airtel Limited

- Rogers Communications Inc.

- Telenor ASA

第7章 市場機會與未來展望

The Telco-as-a-Platform Market size is expected to grow from USD 10.12 billion in 2025 to USD 12.41 billion in 2026 and is forecast to reach USD 23.76 billion by 2031 at 13.87% CAGR over 2026-2031.

The growing deployment of 5G standalone cores, the commercialization of multi-access edge computing, and the standardization of network exposure interfaces are accelerating the industry's pivot from pure connectivity to programmable platforms. Operators in North America, Europe, and Asia-Pacific now expose quality-on-demand, device-location, and SIM-swap detection capabilities through unified APIs, reducing integration costs for enterprises and software developers. Partnerships with hyperscalers place cloud compute inside radio sites, positioning telcos as edge-cloud orchestrators rather than bandwidth wholesalers. At the same time, data-sovereignty regulations in Europe, China, India, and the Gulf states require localized processing, creating demand for hybrid platform architectures that balance compliance with scalability. Competitive pressure intensifies as cloud providers, CPaaS specialists, and greenfield operators challenge legacy carriers that still rely on subscription-oriented BSS and OSS stacks.

Global Telco-as-a-Platform Market Trends and Insights

Proliferation of 5G Standalone Core Enabling Network Exposure

Standalone cores introduce Network Exposure Functions that allow third-party software to invoke quality-of-service tuning, location assurance, and session management through secure northbound APIs. China Mobile surpassed 1 million 5G SA radios by late 2025, and North American operators activated SA cores in major metros, making real-time network slicing commercially viable. 3GPP Releases 16 and 17 defined the underlying interfaces, and the GSMA Open Gateway, along with the Linux Foundation CAMARA project, mapped them to a developer-friendly REST API, giving software teams a single call to request deterministic latency across multiple carriers. Operators now monetize differentiated bandwidth and latency tiers rather than flat connectivity, opening up recurring revenue streams as SA penetration scales toward a majority of global 5G lines before 2028.

Rising Enterprise Demand for Embedded Connectivity and API Access

Banks embed SIM-swap and number-verification calls to stop account-takeover fraud, while hospitals reserve network slices for remote diagnostics that cannot tolerate jitter exceeding 10 milliseconds. Manufacturers orchestrate robotics over private 5G combined with edge compute, using APIs to schedule bandwidth during shift changes. T-Mobile's 2025 launch of T-Platform offered a self-service marketplace where logistics firms automatically provision slices and IoT connections, removing procurement cycles that once took weeks. Simplified pay-as-you-go models attract SMEs that lack telecom expertise, broadening the revenue pool beyond Fortune 500 multinationals.

Legacy IT and BSS/OSS Constraints Hindering API Monetization

Monthly billing engines cannot meter per-second API calls or support dynamic pricing tied to latency classes. Oracle and Amdocs released cloud-native charging stacks, yet migrating millions of subscribers exposes carriers to churn risk and revenue assurance gaps. TM Forum's Open Digital Architecture blueprint guides the rebuild, but only a small subset of operators moved beyond the pilot stage by 2025. Without real-time policy control, many carriers offer only blunt bundles, undermining differentiation from hyperscalers.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Revenue Diversification Beyond Connectivity Services

- MEC Adoption Driving Low-Latency Application Ecosystem

- Fragmented Standards for Network-Exposure APIs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

CPaaS maintained a 32.45% share in 2025, led by messaging pioneers that abstract protocols into simple REST calls. Edge Cloud Platform now records the highest trajectory, with a 15.12% CAGR, as enterprises deploy microservices within radio sites to avoid backhaul. Verizon 5G Edge provides compute within 10 milliseconds of users across more than 50 U.S. metros, enabling factories to detect anomalies in real time. GSMA Open Gateway's alignment of eight API families adds network exposure marketplaces that bond communications with compute.

The shift also reshapes revenue models. While CPaaS charges usage fees per message or per minute, edge platforms charge for CPU cycles, storage, and guaranteed bandwidth. The Telco-as-a-Platform market size for the Edge Cloud subsegment is projected to capture a larger share by the end of the forecast window, reflecting demand for in-situ analytics across autonomous vehicles, computer vision, and immersive media. BSS/OSS-as-a-Service solutions attract regional carriers that prefer to outsource charging and catalog functions rather than rebuild on premises, flattening the cost curve for entry.

Public cloud still accounted for 56.43% of 2025 revenue, but strict localization rules in the EU, China, and parts of the Middle East are driving hybrid architectures at a 14.03% CAGR. Deutsche Telekom and Google Cloud launched a Sovereign Cloud stack that stores keys and metadata only inside German borders, blending hyperscale innovation with regulatory assurance. Enterprises route latency-critical packets to edge locations while forwarding batch analytics to central regions, optimizing cost and compliance simultaneously.

Private deployments remain a niche confined to heavily regulated BFSI and healthcare domains. Yet even these verticals now rely on federated orchestration layers that unify policy across on-premise clusters and telco edges. The Digital Markets Act obliges dominant cloud providers to support interoperability, strengthening carrier bargaining power. In China and India, cybersecurity laws prohibit cross-border transfer of personal data, fueling domestic edge grids that interconnect with public clouds only through anonymized APIs.

The Telco-As-A-Platform Market Report is Segmented by Platform Type (CPaaS, Network Exposure Platform, and More), Deployment Model (Public Cloud, Private Cloud, and More), Network Technology (4G/LTE, NB-IoT and LPWAN, and More), Enterprise Size (Small and Medium Enterprises, and Large Enterprises), End-User Industry (Manufacturing, Automotive, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 28.54% of 2025 revenue, underpinned by early 5G SA launches and cloud-edge partnerships. Verizon 5G Edge, coupled with AWS Wavelength, spans 75 metro zones, allowing e-commerce firms to run recommendation engines within ten milliseconds of customers, while AT&T Network Edge embeds Azure compute in more than 100 cities. T-Mobile's marketplace accelerates SME adoption. Although the Federal Communications Commission encourages Open RAN diversity, divergent state privacy laws complicate multi-state deployments.

Asia-Pacific posts the highest forecast growth at 14.97% CAGR through 2031. China Mobile's extensive SA footprint provides nationwide coverage for industrial parks, while Bharti Airtel's marketplace makes number-verification and IoT connectivity accessible to India's start-up ecosystem. NTT DOCOMO commercialized network slicing for autonomous vehicle trials, and Singtel, with AWS, positions Singapore as a hub for cross-border edge services. Regulatory climates vary, from China's strict localization to Singapore's open data corridors, shaping platform design and pricing.

Europe benefits from unified policies, such as the Digital Markets Act and the GDPR, that mandate open access and privacy compliance. Deutsche Telekom, Orange, and Telefonica pilot federated edges that share capex while meeting data-residency rules. Vodafone's API marketplace spans 21 countries and monetizes fraud-prevention and IoT bundles. Middle East carriers leverage sovereign-cloud incentives to host government workloads in Saudi Arabia and the UAE, while African operators focus on smart-agriculture IoT as 4G coverage widens.

- Vodafone Group Plc

- Deutsche Telekom AG

- Telefonica, S.A.

- AT&T Inc.

- Verizon Communications Inc.

- Orange S.A.

- China Mobile Limited

- China Telecom Corporation Limited

- NTT DOCOMO, Inc.

- Singapore Telecommunications Limited

- Rakuten Symphony, Inc.

- Telstra Group Limited

- T-Mobile US, Inc.

- BT Group plc

- KDDI Corporation

- Swisscom AG

- Dish Network Corporation

- Ericsson AB

- Bharti Airtel Limited

- Rogers Communications Inc.

- Telenor ASA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of 5G Standalone Core Enabling Network Exposure

- 4.2.2 Rising Enterprise Demand for Embedded Connectivity and API Access

- 4.2.3 Shift Toward Revenue Diversification Beyond Connectivity Services

- 4.2.4 MEC Adoption Driving Low-Latency Application Ecosystem

- 4.2.5 Regulatory Push for Open Networks And Fair Access

- 4.2.6 Edge-Native AI Workloads Requiring Telecom-Grade Platforms

- 4.3 Market Restraints

- 4.3.1 Legacy IT and BSS/OSS Constraints Hindering API Monetization

- 4.3.2 Fragmented Standards for Network Exposure APIs

- 4.3.3 Security and Data Sovereignty Concerns Among Enterprises

- 4.3.4 Uncertain ROI for Telcos Investing in Platform Capabilities

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Platform Type

- 5.1.1 CPaaS

- 5.1.2 Network Exposure Platform (API Marketplace)

- 5.1.3 Edge Cloud Platform

- 5.1.4 BSS/OSS-as-a-Service

- 5.1.5 Other Platform Types (IoT Connectivity Platform)

- 5.2 By Deployment Model

- 5.2.1 Public Cloud

- 5.2.2 Private Cloud

- 5.2.3 Hybrid Cloud

- 5.3 By Network Technology

- 5.3.1 4G/LTE

- 5.3.2 5G Non-Standalone (NSA)

- 5.3.3 5G Stand-Alone (SA)

- 5.3.4 NB-IoT and LPWAN

- 5.4 By Enterprise Size

- 5.4.1 Small and Medium Enterprises

- 5.4.2 Large Enterprises

- 5.5 By End-User Industry

- 5.5.1 Manufacturing

- 5.5.2 Automotive and Transportation

- 5.5.3 Media and Entertainment

- 5.5.4 Healthcare

- 5.5.5 Energy and Utilities

- 5.5.6 BFSI

- 5.5.7 Retail and E-Commerce

- 5.5.8 Other End-User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Kenya

- 5.6.5.2.4 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Vodafone Group Plc

- 6.4.2 Deutsche Telekom AG

- 6.4.3 Telefonica, S.A.

- 6.4.4 AT&T Inc.

- 6.4.5 Verizon Communications Inc.

- 6.4.6 Orange S.A.

- 6.4.7 China Mobile Limited

- 6.4.8 China Telecom Corporation Limited

- 6.4.9 NTT DOCOMO, Inc.

- 6.4.10 Singapore Telecommunications Limited

- 6.4.11 Rakuten Symphony, Inc.

- 6.4.12 Telstra Group Limited

- 6.4.13 T-Mobile US, Inc.

- 6.4.14 BT Group plc

- 6.4.15 KDDI Corporation

- 6.4.16 Swisscom AG

- 6.4.17 Dish Network Corporation

- 6.4.18 Ericsson AB

- 6.4.19 Bharti Airtel Limited

- 6.4.20 Rogers Communications Inc.

- 6.4.21 Telenor ASA

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Analyst Recommendations and Suggestions

雲端編配市場:2026-2032年全球市場預測(依服務模式、技術、組織規模、產業及部署模式分類)

雲端編配市場:2026-2032年全球市場預測(依服務模式、技術、組織規模、產業及部署模式分類) MEC(多重存取邊緣)市場預測至2034年-按組件、部署模式、應用、最終用戶和地區分類的全球分析

MEC(多重存取邊緣)市場預測至2034年-按組件、部署模式、應用、最終用戶和地區分類的全球分析 雲端編配市場報告:按解決方案、部署模型、使用者類型、產業和地區分類(2026-2034 年)

雲端編配市場報告:按解決方案、部署模型、使用者類型、產業和地區分類(2026-2034 年) 雲端編配市場:按解決方案、部署類型和區域分類

雲端編配市場:按解決方案、部署類型和區域分類 2026年全球生命週期服務編配市場報告2026年全球門到門任務編配市場報告2026年全球混合雲端編配市場報告2026年全球人工智慧(AI)編配市場報告2026年全球雲端協作市場報告

2026年全球生命週期服務編配市場報告2026年全球門到門任務編配市場報告2026年全球混合雲端編配市場報告2026年全球人工智慧(AI)編配市場報告2026年全球雲端協作市場報告 全球雲端協作市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球雲端協作市場規模、佔有率、趨勢和成長分析報告(2026-2034)