|

市場調查報告書

商品編碼

2044011

5G獨立核心網過渡:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)5G Standalone Core Transformation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

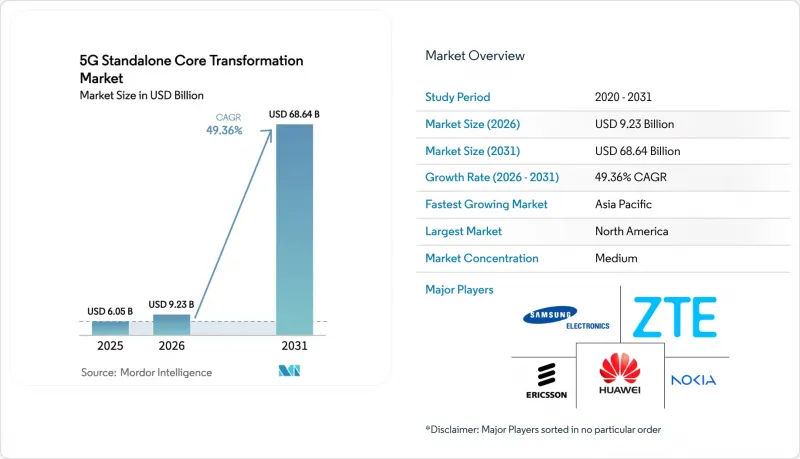

預計 5G 獨立網路核心遷移市場將從 2025 年的 60.5 億美元成長到 2026 年的 92.3 億美元,到 2031 年達到 686.4 億美元,2026 年至 2031 年的複合年成長率為 49.36%。

這項快速成長的驅動力來自於通訊業者從非獨立組網(NSA)架構向雲端原生架構的遷移、工業4.0站點對專用網路投資的增加,以及與超大規模資料中心業者合作以縮短引進週期。雲端原生設計實現了網路切片、超低延遲和邊緣運算的商業化,使通訊業者能夠消除冗餘的演進封包核心網路(EPC)資源並降低訊號開銷。美國、中國、印度和歐盟的公共部門獎勵正在加速農村地區的網路覆蓋擴展。同時,3GPP Release 18規範簡化了多廠商整合,鼓勵二級通訊業者和企業採用API主導的解決方案。此外,容器化網路功能、支援RedCap的大規模物聯網模組以及AI輔助的切片編配正在將目標收入來源擴展到消費者行動寬頻之外,使5G獨立網路核心網路遷移市場走上了持續兩位數成長的道路。

全球5G獨立網路核心網過渡市場趨勢及洞察

通訊業者從NSA到SA的快速過渡

通訊業者正在逐步淘汰雙核心架構,因為並行維護會增加營運成本,並阻礙超可靠低延遲通訊 (URLC) 和專用網路切片等高階功能的採用。 Telia、Three UK、MTN South Africa 和 O2 Telefonica 在 2024 年至 2025 年間的商業轉型證明了這種轉型的經濟效益。 Telia 在逐步淘汰其演進分組核心網 (EPC) 後,訊號開銷降低了 30%。根據全球行動供應商協會 (GMSA) 統計,目前已有 181 家通訊業者投資獨立組網 (SA) 基礎設施,高於前一年的 140 家。這種轉變創造了網路即服務 (NaaS) 的商機,因為企業可以租用有保障的網路切片來運行在非獨立組網 (NSA) 環境限制下無法實現的關鍵任務工作負載。

一級通訊業者正在引進雲端容器化網路功能。

一級營運商正在將其核心網路平台遷移到 Kubernetes,以實現橫向擴展和零停機升級。愛立信在 Google Cloud 上的按需核心網路可在 60 秒內啟動使用者平面功能,使通訊業者能夠在高峰時段將容量擴展十倍。英國 Three 經營一個基於 Red Hat OpenShift編配的9 Tbit/s 核心網,為 3,000 萬用戶提供服務,同時減少了 40% 的實體伺服器。西班牙電信 O2 將其控制平面工作負載託管在法蘭克福的 AWS Outposts 上,從而降低了其汽車和工業客戶的延遲。這些概念驗證案例表明,容器化如何縮短服務引進週期並降低對硬體的依賴。

向雲端原生 5G 核心網路 (5GC) 的遷移涉及高額資本支出 (CAPEX) 和熟練人員短缺。

部署獨立方案需要新的運算叢集、軟體授權和DevOps管線,但目前仍缺乏經過認證的Kubernetes工程師。麥肯錫估計,5G總投資將達到4,000億至5,000億美元,其中核心網路現代化將佔到五分之一。德勤的一項調查顯示,65%的受訪通訊業者認為人才短缺是他們面臨的最大瓶頸。隨著小型通訊業者越來越依賴託管服務,人們開始擔憂利潤率下降和客製化速度變慢的問題。

細分市場分析

預計到2025年,硬體收入將佔總收入的58.40%,這主要反映了x86或ARM運算節點、100Gigabit交換器以及承載容器化功能所需的容器化取網路(RAN)設備的初始採購。儘管5G獨立核心網過渡市場的硬體市場規模預計將穩定成長,但隨著價值向編配智慧轉移,其市場佔有率將會下降。相較之下,受微服務授權、人工智慧驅動的生命週期自動化和持續交付的推動,軟體收入預計將以52.4%的複合年成長率強勁成長。部署愛立信Release 25A和諾基亞MX工業邊緣運算平台的通訊業者正在以每周而非每季發布程式碼的方式交付新功能,這充分展現了雲端原生架構的速度優勢。

除了軟體之外,服務供應商擴大將諮詢、整合和託管營運打包提供。 Oracle 的通訊雲原生核心 (Communications Cloud Native Core) 運作在通用硬體上,使沃達豐和西班牙電信的資本密集度降低了 30%。 VMware 的電信雲端平台 (Oracle Cloud Platform) 提供了一個 Kubernetes 基礎架構,將供應商的軟體和硬體分離,使通訊業者能夠協商更優惠的設備價格。隨著 Release 18 中開放 API 的標準化,差異化因素正從客製化晶片轉向軟體敏捷性,這擴大了快速發展的容器生態系統與靜態設備環境之間的效能差距。

區域分析

預計到2025年,北美將貢獻40.03%的收入,這主要得益於FCC農村地區基金的撥款、NTIA開放式無線接入網(Open RAN)津貼以及為覆蓋2億人口而積極部署的C頻段。 Verizon在芝加哥和達拉斯向獨立網路(SA)系統的過渡將為工業自動化提供優質網路切片,而AT&T計劃在2026年底前逐步淘汰非獨立組網(NSA)節點。在加拿大,3.8 GHz頻段已進行競標,Rogers、Bell和Tellus已在多倫多和溫哥華啟動核心網路的試點營運。同時,墨西哥的Telcel和AT&T Mexico已在墨西哥城和蒙特雷啟動試點營運。強勁的資本市場、早期取得頻段以及接近性超大規模資料中心,正在鞏固該地區作為盈利領先地區的地位。

亞太地區是高速成長的驅動力,預計到2031年將以59.6%的複合年成長率成長。中國擁有360萬個基地台,加之工信部(MIIT)對獨立組網(SAC)的強制性要求,正推動用戶數量爆炸性成長至8.9億。在日本,NTT Docomo、KDDI和Softbank Corporation正在全國部署愛立信、諾基亞和三星的設備,為自動駕駛汽車和智慧工廠領域的客戶提供服務。韓國的SK Telecom、KT和LG U+專注於人工智慧驅動的網路切片,服務於汽車和雲端遊戲領域;而印度的Reliance Jio則憑藉其新建的獨立待開發區架構覆蓋了5000個城市。包括印度6GHz頻段分配和韓國5G+藍圖的區域產業政策,進一步推動了對邊緣運算核心網路的需求。

儘管歐洲在絕對規模上落後於北美和亞太地區,但它正受益於歐盟5G行動計畫下協調一致的頻率政策。德國電信已在法蘭克福、慕尼黑和柏林推出獨立核心網,目標客戶是高速公路沿線的汽車製造商。 Orange已在巴黎和里昂推出服務,而EE和沃達豐英國公司則在倫敦和曼徹斯特部署了核心網。制裁限制了俄羅斯通訊業者獲取西方設備的管道,減緩了部署速度,但瑞士電信、挪威電信和TIM正在證明,即使在小規模的市場,雲端原生設備也能快速遷移。同時,南美、中東和非洲仍處於早期階段,但展現出巨大的潛力。 Claro、TIM和Vivo正在聖保羅和里約熱內盧進行試點運營,而沙烏地阿拉伯的STC、阿拉伯聯合大公國的Etisalat和南非的MTN已開設都市區企業區,併計劃在2027年頻率競標結束後擴大覆蓋範圍。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 通訊業者從NSA到SA的快速過渡

- 政府主導的5G獎勵策略和頻率分配獎勵

- 工業4.0場所中私有5G網路及園區網路的爆炸性成長

- 一級通訊業者正在引進雲端容器化網路功能。

- AI最佳化動態網路切片的商業試點

- RedCap 設備的出現釋放了大規模物聯網安全代理流量的潛力。

- 市場限制因素

- 遷移到雲端原生5GC需要高額資本投入和技能缺口。

- 多廠商核心系統與傳統EPC系統之間的互通性挑戰

- 擴大基於服務的架構中的網路攻擊面

- 頻寬頻譜的碎片化正在減緩 SA 覆蓋範圍的擴大。

- 產業生態系分析

- 監理情勢

- 技術展望

- 波特五力分析

- 新參與企業的威脅

- 供應商議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭關係

第5章:預測市場規模與成長率

- 按組件

- 硬體

- 軟體

- 服務

- 透過部署方法

- 公共雲端

- 私有雲端

- 混合/本地部署

- 最終用戶

- 通訊業者

- 已部署企業/私人 5G 的公司

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 供應商定位分析

- 公司簡介

- Huawei Technologies Co., Ltd.

- Telefonaktiebolaget LM Ericsson

- Nokia Corporation

- ZTE Corporation

- Samsung Electronics Co., Ltd.

- Cisco Systems, Inc.

- Juniper Networks, Inc.

- Mavenir Systems, Inc.

- Affirmed Networks, Inc.(now part of Microsoft)

- NEC Corporation(Nippon Electric Company, Limited)

- Hewlett Packard Enterprise Company

- Oracle Corporation

- Athonet Srl(now part of HPE)

- Casa Systems, Inc.

- Cumucore Oy

- Druid Software Limited

- IPLOOK Networks Co., Ltd.

- Parallel Wireless, Inc.

- Rakuten Symphony, Inc.

- VMware, Inc.(now part of Broadcom)

第7章 市場機會與未來展望

The 5G Standalone Core Transformation Market size is expected to increase from USD 6.05 billion in 2025 to USD 9.23 billion in 2026 and reach USD 68.64 billion by 2031, growing at a CAGR of 49.36% over 2026-2031. Rising operator migration from non-standalone architectures, expanding private network spend across Industry 4.0 sites, and hyperscaler alliances that shorten deployment cycles underpin this sharp trajectory. Cloud-native design unlocks network slicing, ultra-low latency, and edge-computing monetization, allowing carriers to retire duplicated evolved packet core resources and shrink signaling overhead. Public-sector incentives in the United States, China, India, and the European Union accelerate coverage in rural zones, while 3GPP Release 18 specifications simplify multi-vendor integration, encouraging tier-2 operators and enterprises to adopt API-driven solutions. At the same time, containerized network functions, RedCap-enabled mass-IoT modules, and AI-assisted slice orchestration expand the addressable revenue pool far beyond consumer mobile broadband, positioning the 5G standalone core transformation market for sustained double-digit growth.

Global 5G Standalone Core Transformation Market Trends and Insights

Rapid Migration of Operators From NSA to SA Deployments

Operators are abandoning dual-core architectures because parallel maintenance inflates operating costs and blocks advanced features such as ultra-reliable low-latency communication and dedicated network slices. Commercial cutovers by Telia, Three UK, MTN South Africa, and O2 Telefonica during 2024-2025 validated the economic upside, with Telia reporting a 30% reduction in signaling overhead after decommissioning its evolved packet core. The Global Mobile Suppliers Association counted 181 operators investing in standalone infrastructure, up from 140 a year earlier. This migration unlocks network-as-a-service revenue, as enterprises lease guaranteed slices for mission-critical workloads unattainable under non-standalone constraints.

Cloud-Native, Containerized Network-Function Adoption by Tier-1 CSPs

Tier-1 carriers are re-platforming cores on Kubernetes to gain horizontal scaling and zero-downtime upgrades. Ericsson's On-Demand core on Google Cloud spins up user-plane functions in under 60 seconds, helping operators scale capacity tenfold during peak events. Three UK operates a 9 Tbit/s core orchestrated by Red Hat OpenShift, serving 30 million subscribers with 40% fewer physical servers. O2 Telefonica colocated control-plane workloads on AWS Outposts in Frankfurt, trimming latency for automotive and industrial clients. These proofs confirm that containerization compresses service introduction cycles and reduces hardware intensity.

High CAPEX and Skills Gap for Cloud-Native 5GC Transformation

Standalone adoption demands new compute clusters, software licenses, and DevOps pipelines while certified Kubernetes engineers remain scarce. McKinsey pegged the total 5G spend at USD 400-500 billion, with core modernization accounting for up to one-fifth of that. Deloitte found 65% of surveyed operators cited talent shortages as the primary bottleneck. As smaller carriers turn to managed services, margin compression and slower customization follow.

Other drivers and restraints analyzed in the detailed report include:

- Explosion of Private-5G and Campus Networks Across Industry 4.0 Sites

- AI-Optimized Dynamic Network Slicing Commercial Pilots

- Inter-Operability Issues Across Multi-Vendor Cores and Legacy EPC

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware accounted for 58.40% of 2025 revenue, reflecting up-front purchases of x86 or ARM compute nodes, 100-gigabit switches, and RAN gear needed to host containerized functions. The 5G standalone core transformation market size for hardware is projected to grow steadily but cede share as value shifts toward orchestration intelligence. In contrast, software revenue is forecast to climb at a robust 52.4% CAGR, propelled by microservice licensing, AI-powered lifecycle automation, and continuous delivery. Operators deploying Ericsson Release 25A and Nokia MX Industrial Edge report weekly feature drops rather than quarterly code releases, demonstrating the speed premium of cloud-native stacks.

Service providers increasingly bundle consulting, integration, and managed operations alongside software. Oracle's Communications Cloud Native Core lowered capital intensity by 30% for Vodafone and Telefonica by running on commodity gear. VMware's Telco Cloud Platform supplies the Kubernetes substrate that decouples vendor software from hardware, allowing carriers to negotiate favorable appliance pricing. As Release 18 hardwires open APIs, differentiation shifts from custom silicon to software agility, widening the performance gap between fast-moving container ecosystems and static appliance estates.

The 5G Standalone Core Transformation Market Report is Segmented by Component (Hardware, Software, and Services), Deployment Model (Public Cloud, Private Cloud, and Hybrid/On-premises), End-User (Telecom Operators, and Enterprises/Private 5G Owners), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 40.03% of 2025 revenue on the back of FCC rural-fund subsidies, NTIA Open RAN grants, and aggressive C-band rollouts that reached 200 million POPs. Verizon's standalone cutover in Chicago and Dallas opened premium slices for industrial automation, while AT&T plans to decommission non-standalone anchors by late 2026. Canada auctioned 3.8 GHz spectrum and saw Rogers, Bell, and Telus pilot cores in Toronto and Vancouver, whereas Mexico's Telcel and AT&T Mexico began trials in Mexico City and Monterrey. Strong capital markets, early access to spectrum, and proximity to hyperscale data centers position the region as a profitability leader.

Asia-Pacific is the high-growth engine, forecast to expand at a 59.6% CAGR through 2031. China's 3.6 million base-station grid and MIIT mandate for standalone cores underpin explosive scale across 890 million subscribers. Japan's nationwide launch by NTT Docomo, KDDI, and SoftBank leverages Ericsson, Nokia, and Samsung gear to service autonomous-vehicle and smart-factory clients. South Korea's SK Telecom, KT, and LG U+ focus on AI-driven network slicing for automotive and cloud gaming, while India's Reliance Jio covers 5,000 cities on a greenfield standalone architecture. Regional industrial policies, including India's 6 GHz allocation and South Korea's 5G+ roadmap, further lift demand for edge-enabled cores.

Europe trails North America and Asia-Pacific on an absolute scale, but benefits from coordinated spectrum policy under the EU 5G Action Plan. Deutsche Telekom lit standalone cores in Frankfurt, Munich, and Berlin, targeting automotive OEMs along the Autobahn corridors. Orange activated service in Paris and Lyon, and EE and Vodafone UK rolled out cores in London and Manchester. Sanctions limit Russian operator access to Western equipment, slowing adoption, but Swisscom, Telenor, and TIM demonstrate that smaller markets can still transition quickly by adopting cloud-native appliances. Meanwhile, South America and the Middle East, and Africa remain early-stage yet promising. Claro, TIM, and Vivo conducted trials in Sao Paulo and Rio de Janeiro, while STC Saudi Arabia, Etisalat UAE, and MTN South Africa launched urban enterprise zones and plan broader coverage by 2027 as spectrum auctions conclude.

List of Companies Covered in this Report:

- Huawei Technologies Co., Ltd.

- Telefonaktiebolaget LM Ericsson

- Nokia Corporation

- ZTE Corporation

- Samsung Electronics Co., Ltd.

- Cisco Systems, Inc.

- Juniper Networks, Inc.

- Mavenir Systems, Inc.

- Affirmed Networks, Inc. (now part of Microsoft)

- NEC Corporation (Nippon Electric Company, Limited)

- Hewlett Packard Enterprise Company

- Oracle Corporation

- Athonet S.r.l. (now part of HPE)

- Casa Systems, Inc.

- Cumucore Oy

- Druid Software Limited

- IPLOOK Networks Co., Ltd.

- Parallel Wireless, Inc.

- Rakuten Symphony, Inc.

- VMware, Inc. (now part of Broadcom)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Migration of Operators From NSA to SA Deployments

- 4.2.2 Government-Backed 5G Stimulus Packages and Spectrum Incentives

- 4.2.3 Explosion of Private-5G and Campus Networks Across Industry 4.0 Sites

- 4.2.4 Cloud-Native, Containerised Network-Function Adoption by Tier-1 CSPs

- 4.2.5 AI-Optimised Dynamic Network Slicing Commercial Pilots

- 4.2.6 Emergence of RedCap Devices Unlocking Mass-IoT SA Traffic

- 4.3 Market Restraints

- 4.3.1 High CAPEX and Skills Gap for Cloud-Native 5GC Transformation

- 4.3.2 Inter-Operability Issues Across Multi-Vendor Cores and Legacy EPC

- 4.3.3 Elevated Cyber-Attack Surface in Service-Based Architectures

- 4.3.4 Mid-band Spectrum Fragmentation Slowing SA Coverage Expansion

- 4.4 Industry Ecosystem Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Deployment Model

- 5.2.1 Public Cloud

- 5.2.2 Private Cloud

- 5.2.3 Hybrid / On-premises

- 5.3 By End-User

- 5.3.1 Telecom Operators

- 5.3.2 Enterprises / Private 5G Owners

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Russia

- 5.4.3.5 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Rest of the Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Huawei Technologies Co., Ltd.

- 6.4.2 Telefonaktiebolaget LM Ericsson

- 6.4.3 Nokia Corporation

- 6.4.4 ZTE Corporation

- 6.4.5 Samsung Electronics Co., Ltd.

- 6.4.6 Cisco Systems, Inc.

- 6.4.7 Juniper Networks, Inc.

- 6.4.8 Mavenir Systems, Inc.

- 6.4.9 Affirmed Networks, Inc. (now part of Microsoft)

- 6.4.10 NEC Corporation (Nippon Electric Company, Limited)

- 6.4.11 Hewlett Packard Enterprise Company

- 6.4.12 Oracle Corporation

- 6.4.13 Athonet S.r.l. (now part of HPE)

- 6.4.14 Casa Systems, Inc.

- 6.4.15 Cumucore Oy

- 6.4.16 Druid Software Limited

- 6.4.17 IPLOOK Networks Co., Ltd.

- 6.4.18 Parallel Wireless, Inc.

- 6.4.19 Rakuten Symphony, Inc.

- 6.4.20 VMware, Inc. (now part of Broadcom)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

5G高密度和小型基地台部署市場預測—按組件、類型、應用、最終用戶和地區分類的全球分析—2034年

5G高密度和小型基地台部署市場預測—按組件、類型、應用、最終用戶和地區分類的全球分析—2034年 2026年全球高密度5G網路市場報告

2026年全球高密度5G網路市場報告 Frost Radar™ - 5G 網路基礎設施,2026 年全球5G邊緣雲端網路和服務市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球政策控制功能分析市場報告2026年全球政策與收費控制市場報告2026年全球會話管理功能(SMF)策略控制市場報告2026年全球空中下載行車記錄器策略控制市場報告2026年全球衛生署或通訊部政策管理市場報告2026年5G策略控制功能全球市場報告

Frost Radar™ - 5G 網路基礎設施,2026 年全球5G邊緣雲端網路和服務市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球政策控制功能分析市場報告2026年全球政策與收費控制市場報告2026年全球會話管理功能(SMF)策略控制市場報告2026年全球空中下載行車記錄器策略控制市場報告2026年全球衛生署或通訊部政策管理市場報告2026年5G策略控制功能全球市場報告