|

市場調查報告書

商品編碼

2043982

銫:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Cesium - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

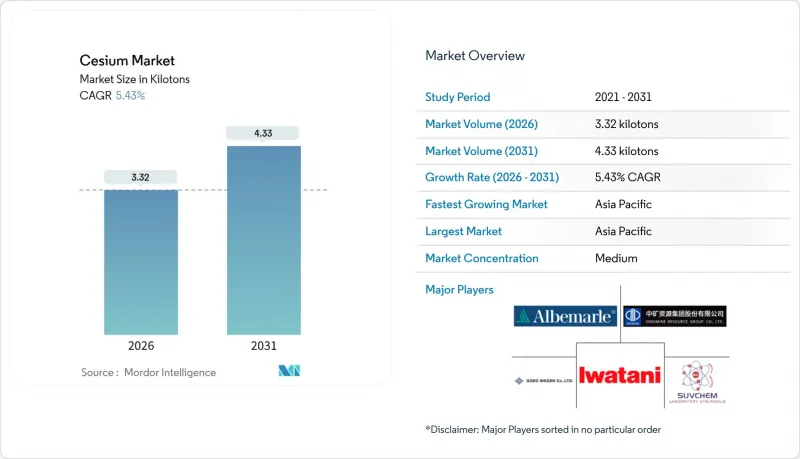

預計到 2026 年銫市場規模為 3.32 千噸,到 2031 年將達到 4.33 千噸,在預測期(2026-2031 年)內複合年成長率為 5.43%。

高壓高溫(HPHT)鑽井活動的增加、5G和未來6G基礎設施的快速發展以及新興的醫療成像應用正在推動需求成長,即便關鍵的鈣礬礦石供應管道仍然稀缺。為此,垂直整合的供應商已與鑽井服務公司簽訂多年契約,以確保這種稀缺原料的供應,並準備在2024年提價。亞太地區在消費和加工方面均處於主導地位,其中中國精煉了全球大部分銫鹽,而日本則在精密電子應用領域佔據主導地位。在北美和歐洲,海上HPHT完井計畫和國防計畫維持著穩定的需求基礎,但買家面臨單一供應商風險,主要來自中礦集團和雅寶集團。

全球銫市場趨勢及洞察

超深高壓高溫井中甲酸銫流體的使用量迅速增加

高密度甲酸銫鹽水因其對地質損害極小,正逐漸成為壓力超過20,000 psi儲存的主要成品油。北海、墨西哥灣和巴西的作業者已證明,由於地質完整性得以保持和油藏壽命採收率的提高,這些成品油的成本可在一年內收回。全球甲酸銫庫存有限,隨著對深井需求的成長,供應日益緊張。為此,中礦集團在阿伯丁和卑爾根建立了專用回收設施,並簽訂了與布蘭特原油期貨價格掛鉤的長期供應合約。這些策略舉措不僅保障了利潤率,也為高溫高壓服務鏈的新進者設置了准入壁壘,鞏固了中礦集團在銫市場的主導地位。

5G/6G 網路的廣泛應用需要超穩定的銫原子鐘。

通訊業者正在加速用銫原子鐘取代銣振盪器,銫原子鐘無需依賴GPS即可長時間保持高精度。這項轉變的主要驅動力是亞微秒同步的需求,這是5G協同多點傳輸的必要條件。沃達豐土耳其公司計劃於2024年推出這項服務,這只是這一趨勢的一個例證,而這一趨勢正在中國、韓國和美國迅速發展。雖然在實驗室環境下,光晶格鐘的精度高於銫原子鐘,但監管計量仍採用基於9.19 GHz銫-133躍遷的國際單位制秒。只要標準化機構維持這個定義,銫原子鐘的主導地位和銫原子鐘市場就將持續穩固。

商業性運作的鎂鋁榴石礦數量有限。

2024年,由於沒有大型聚乙烯礦持續運營,除鑽井液外,對銫鹽的需求只能依賴現有庫存和唐科的間歇性供應。儘管中礦集團主導地位,唐科仍選擇間歇式加工而非連續作業,這表明要么礦石品位較低,要么在當前價格水平下獲利能力難度較大。自2000年代初以來,全球氧化銫(Cs2O)蘊藏量未見重大新發現,航太和國防領域開始囤積高純度碳酸銫和金屬銫。此舉不僅增加了營運資金需求,也降低了銫市場的需求彈性。

細分市場分析

銫化合物市場佔總銷售量的73.45%,預計到2031年將以每年6.02%的速度成長。甲酸鹽溶液在該領域主導,而碳酸鹽則用於生產藥物催化劑和高屈光玻璃。碘化物和溴化物則供應閃爍體和紅外線光學市場。隨著純度的提高,金屬銫的利潤率也隨之提高。儘管每單位氯化銫(CSAC)所使用的金屬量較少,但由於國防相關買家願意支付遠高於通用鹽的價格,因此該細分市場受整體市場波動的影響較小。

在全球基礎設施和醫療保健支出不斷成長的推動下,對銫化合物的需求預計將持續成長,特別是用於高溫高壓鑽孔、特種玻璃和醫學成像的銫化合物。金屬銫的需求將隨著國防採購和通訊網路升級而出現間歇性成長,但這不會改變整體生產平衡。其他銫衍生物,例如氫氧化銫、氟化銫和銻化銫,仍然是蝕刻化學品和光電陰極等小眾產品,僅佔整個市場的一小部分。因此,同時垂直整合銫化合物和金屬銫的生產正成為應對產業需求波動的最可靠策略。

《全球銫市場》報告按產品類型(金屬銫、銫化合物、其他產品類型)、應用領域(石油天然氣、電子、醫療保健、其他應用)和地區(北美、歐洲、亞太、世界其他地區)進行細分。市場預測以噸為單位。

區域分析

預計到2025年,亞太地區將佔43.86%的銫市場佔有率,並在2031年實現6.56%的最高成長速度。中國擁有全球最大的精煉叢集,能夠熟練地將來自加拿大和辛巴威的聚銫礦轉化為碳酸鹽、碘化物和超乾甲酸鹽。同時,以五藤重根株式會社和巖谷株式會社為首的日本專業製造商,不僅向國內電子業供應原子鐘級銫鹽,還將剩餘產品出口到北美和歐洲。韓國全國5G網路的快速發展,正在提升該地區對銫振盪器的需求。同時,中國在南海的海洋探勘也推動了對甲酸鹽的需求。然而,目前尚不明確的出口許可框架令人擔憂,這可能導致高純度銫被挪用,優先滿足國內航太和電信業的需求。

北美和歐洲是成熟的市場,但它們構成了具有重要戰略意義的市場叢集。北美和歐洲的銫金屬及其特殊化合物的精煉以德國雅寶公司位於朗格斯海姆的工廠為中心。墨西哥灣的三次高壓高溫(HPHT)井和北海的老舊高壓儲存確保了甲酸鹽的穩定供應。然而,這兩個地區目前都嚴重依賴中礦公司(Sinomine)提供的上游礦石。在美國,國防部門為CSAC項目儲備銫金屬,即使這需要更長的前置作業時間和更高的成本來保證高純度,這一立場也沒有改變。在大西洋彼岸的歐洲,進口商面臨歐盟《關鍵原料法》規定的可追溯性要求。雖然這些要求延長了採購週期,但如果價格超過臨界水平,也可能導致北美銫礬石開採活動的復甦。

儘管其他地區(ROW)目前發揮的作用有限,但其戰略潛力毋庸置疑。在巴西的鹽層下下層,巴西石油公司(Petrobras)及其合作夥伴正在從7000公尺以上的深度開採甲酸鹽水,這表明市場需求可能會持續到2030年。西非的深海開發雖然會受到原油價格波動的影響,但隨著基礎建設的推進,其長期前景十分可觀。然而,非洲作為銫供應國的潛力與鋰價格的復甦密切相關。奈米比亞、津巴布韋和剛果民主共和國(DRC)等富含鋰雲母的地區的項目寄希望於鋰價格上漲,從而使銫的共加工有利可圖。如果鋰價格沒有回升,這些國家作為潛在供應國的地位將仍然處於邊緣,全球銫市場將繼續集中在少數生產地區。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 超深高壓高溫井中甲酸銫流體的使用量迅速增加

- 5G/6G 網路的廣泛應用需要超穩定的銫原子鐘。

- 先進醫學影像診斷領域對銫基閃爍體的需求不斷成長。

- 微型銫原子鐘在自主和國防無人機機隊的興起

- 在非洲從鋰雲母尾礦中試規模提取銫

- 市場限制因素

- 商業性運作的磷礦數量稀少。

- 對策略性鹼金屬實施嚴格的出口管制

- 由於該副產品的價格依賴鋰的供應,因此其價格容易波動。

- 價值鏈分析

- 供應鏈分析

- 監理政策分析

- 出口管制和貿易限制

- 環境法規

- 價格分析

- 過去的價格趨勢

- 影響價格的因素

- 貿易分析

- 生產成本分析

- 波特五力分析

- 新參與企業的威脅

- 供應商議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭關係

- 銫礦列表:按公司

- 供應分析

- 監理政策分析

- 貿易分析

- 價格趨勢分析

- 生產成本分析

第5章:預測市場規模與成長率

- 依產品類型

- 銫金屬

- 銫化合物

- 其他產品類型

- 透過使用

- 石油和天然氣

- 電子設備

- 醫療保健

- 其他用途

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 其他地區(ROW)

第6章 競爭情勢

- 市場集中度分析

- 策略趨勢

- 市佔率/排名分析

- 公司簡介

- Albemarle Corporation

- GODO SHIGEN Co., Ltd.

- Iwatani Corporation

- Sinomine Resource Group Co., Ltd.

- Suvchem

第7章 市場機會與未來展望

The Cesium Market size is estimated at 3.32 kilotons in 2026, and is expected to reach 4.33 kilotons by 2031, at a CAGR of 5.43% during the forecast period (2026-2031).

Rising high-pressure high-temperature (HPHT) drilling activity, fast-growing 5G and future 6G infrastructure, and new medical-imaging uses are expanding demand even as the pipeline of primary pollucite ore remains thin. Vertically integrated suppliers have reacted by raising prices in 2024 while locking in multiyear contracts with drilling-service companies to secure scarce feedstock. Asia-Pacific leads both consumption and processing because China refines the bulk of global cesium salts, and Japan dominates precision-electronics applications. In North America and Europe, offshore HPHT completions and defense programs sustain a stable demand base but expose buyers to a single-supplier risk centered on Sinomine and Albemarle.

Global Cesium Market Trends and Insights

Surging Use of Cesium-Formate Fluids in Ultra-Deep HPHT Wells

Cesium-formate brines, with high densities and minimal formation damage, have emerged as the go-to completion fluid for reservoirs exceeding 20,000 psi. Operators in the North Sea, Gulf of Mexico, and Brazil have demonstrated that they can recover the cost of these fluids within a year, thanks to preserved formation integrity and enhanced lifetime recovery. The global inventory of cesium-formate is limited, and the supply is tightening as the demand for deeper wells grows. In response, Sinomine has established dedicated recovery bases in Aberdeen and Bergen, and has tied long-term supply contracts to Brent oil futures. These strategic moves not only safeguard profit margins but also create barriers for new competitors in the HPHT service chain, solidifying Sinomine's dominance in the cesium market.

Proliferation of 5G/6G Networks Requiring Ultra-Stable Cesium Clocks

Telecom operators are increasingly replacing rubidium oscillators with cesium atomic clocks, which can maintain GPS-free accuracy for an extended period. This shift is largely driven by the need for sub-microsecond synchronization, a requirement for 5G coordinated multipoint transmission. Vodafone Turkey's 2024 deployment is just one example of a trend that's rapidly gaining momentum in China, South Korea, and the United States. While optical lattice clocks have achieved greater accuracy than cesium in laboratory settings, the regulatory metrology still recognizes the SI second based on the 9.19 GHz cesium-133 transition. As long as standards bodies uphold this definition, cesium's dominant position-and the market for cesium-remains firmly established.

Limited Number of Commercially Active Pollucite Mines

In 2024, the absence of a continuously operating primary pollucite mine compelled the demand for cesium salts-used outside of drilling fluids-to depend on existing inventories and sporadic outputs from Tanco. Despite Sinomine's leadership, Tanco has opted for batch processing over continuous operations, hinting at either subpar ore grades or challenging processing economics given the current price levels. With global reserves of cesium oxide (Cs2O) showing no significant discoveries since the early 2000s, aerospace and defense sectors have begun stockpiling high-purity cesium carbonate and metal. This move has not only heightened their working-capital demands but also dampened the demand's elasticity in the cesium market.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand for Cs-Based Scintillators in Advanced Medical Imaging

- Rise of Mini-Cs Atomic Clocks for Autonomous and Defense UAV Fleets

- Tight Export Controls on Strategic Alkali Metals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The cesium market size for compounds stood equals to 73.45% of total volume, and is forecast to grow at 6.02% through 2031. Formate brines lead this segment, while carbonate supports pharmaceutical catalysis and high-refractive-index glass. Iodide and bromide cater to scintillator and infrared-optics markets. The metal segment commands premium margins as purity levels increase. Although each CSAC unit requires only small amounts of metal, defense buyers are willing to pay significantly higher prices compared to commodity salts, insulating this sub-segment from broader market fluctuations.

As global infrastructure and healthcare spending rise, the demand for cesium compounds-driven by HPHT drilling, specialty glass, and medical imaging-is set to continue. While metal demand will see episodic growth aligned with defense procurement and telecom upgrades, it won't alter the overall tonnage balance. Other cesium derivatives like hydroxide, fluoride, and antimonide will remain niche players, catering to etching chemistry and photocathodes, collectively making up a minor portion of the market. Thus, vertical integration into both cesium compounds and metal emerges as the most reliable strategy against demand fluctuations in the industry.

The Cesium Market Report is Segmented by Product Type (Cesium Metal, Cesium Compounds, and Other Product Types), Application (Oil and Gas, Electronics, Medical and Healthcare, and Other Applications), and Geography (North America, Europe, Asia-Pacific, and Rest of the World). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific accounted for 43.86% of the cesium market share in 2025 and is anticipated to log the fastest 6.56% CAGR to 2031. China, boasting the world's largest refinery cluster, adeptly transforms pollucite sourced from Canada and Zimbabwe into carbonate, iodide, and ultra-dry formate. Meanwhile, Japan's specialized producers, spearheaded by GODO SHIGEN and Iwatani, not only cater to domestic electronics with atomic-clock-grade salts but also export their surplus to North America and Europe. South Korea's nationwide 5G Advanced upgrade amplifies the regional demand for cesium oscillators. Concurrently, Chinese offshore explorations in the South China Sea bolster the demand for formate. However, a looming concern is the pending export-license frameworks, which may redirect high-purity cesium to prioritize domestic aerospace and telecom needs.

North America and Europe, while mature, represent a market cluster of strategic significance. Western refining of cesium metal and its specialty compounds finds a cornerstone in Albemarle's Langelsheim plant in Germany. The Lower Tertiary HPHT wells in the Gulf of Mexico and the aging high-pressure reservoirs of the North Sea guarantee a steady offtake of formate. Yet, both regions find themselves heavily reliant on upstream ore supplied by Sinomine. In the U.S., defense sectors are stockpiling cesium metal for CSAC programs, even if it means accepting longer lead times and incurring higher purity-assurance costs. Across the Atlantic, European importers face challenges with the traceability mandates of the EU Critical Raw Materials Act. While these mandates extend procurement cycles, they might also set the stage for a revival of North American pollucite operations, especially if prices surpass a critical threshold.

While the Rest of the World currently plays a modest role, its potential is undeniably strategic. In Brazil's pre-salt fields, Petrobras and its partners are tapping into formate brines for depths surpassing 7,000 m, signaling a demand that could stretch through 2030. West Africa's deepwater activities, though swayed by oil-price fluctuations, hint at a promising long-term trajectory as infrastructure continues to develop. However, Africa's potential as a cesium supplier is closely tied to a rebound in lithium prices. Projects in lepidolite-rich regions of Namibia, Zimbabwe, and the DRC are banking on higher lithium values to make cesium co-processing viable. Without this price recovery, these nations remain on the periphery as prospective suppliers, leaving the global cesium market heavily concentrated in a select few producing locales.

- Albemarle Corporation

- GODO SHIGEN Co., Ltd.

- Iwatani Corporation

- Sinomine Resource Group Co., Ltd.

- Suvchem

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging use of cesium-formate fluids in ultra-deep HPHT wells

- 4.2.2 Proliferation of 5G/6G networks requiring ultra-stable cesium clocks

- 4.2.3 Growing demand for Cs-based scintillators in advanced medical imaging

- 4.2.4 Rise of mini-Cs atomic clocks for autonomous and defense UAV fleets

- 4.2.5 Pilot-scale extraction of cesium from lepidolite tailings in Africa

- 4.3 Market Restraints

- 4.3.1 Limited number of commercially active pollucite mines

- 4.3.2 Tight export controls on strategic alkali metals

- 4.3.3 Volatile pricing due to by-product dependence on Li supply

- 4.4 Value Chain Analysis

- 4.5 Supply Chain Analysis

- 4.6 Regulatory Policy Analysis

- 4.6.1 Export Controls and Trade Restrictions

- 4.6.2 Environmental Regulations

- 4.7 Pricing Analysis

- 4.7.1 Historical Price Trend

- 4.7.2 Price Influencing Factors

- 4.8 Trade Analysis

- 4.9 Production Cost Analysis

- 4.10 Porter's Five Forces

- 4.10.1 Threat of New Entrants

- 4.10.2 Bargaining Power of Suppliers

- 4.10.3 Bargaining Power of Buyers

- 4.10.4 Threat of Substitutes

- 4.10.5 Competitive Rivalry

- 4.11 List of Cesium Mines, By Company

- 4.12 Supply Analysis

- 4.13 Regulatory Policy Analysis

- 4.14 Trade Analysis

- 4.15 Price Trend Analysis

- 4.16 Production Cost Analysis

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Cesium Metal

- 5.1.2 Cesium Compounds

- 5.1.3 Other Product Types

- 5.2 By Application

- 5.2.1 Oil and Gas

- 5.2.2 Electronics

- 5.2.3 Medical and Healthcare

- 5.2.4 Other Applications

- 5.3 By Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 Rest of the World

6 Competitive Landscape

- 6.1 Market Concentration Analysis

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Albemarle Corporation

- 6.4.2 GODO SHIGEN Co., Ltd.

- 6.4.3 Iwatani Corporation

- 6.4.4 Sinomine Resource Group Co., Ltd.

- 6.4.5 Suvchem

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

四氯鉑酸鉀市場-全球產業規模、佔有率、趨勢、機會、預測:銷售管道、最終用途、地區和競爭格局分類,2021-2031年

四氯鉑酸鉀市場-全球產業規模、佔有率、趨勢、機會、預測:銷售管道、最終用途、地區和競爭格局分類,2021-2031年 高鐵酸鉀市場規模、佔有率和成長分析:按產品形式、生產通路、應用、最終用途和地區分類-2026-2033年產業預測

高鐵酸鉀市場規模、佔有率和成長分析:按產品形式、生產通路、應用、最終用途和地區分類-2026-2033年產業預測 銫市場:按組件、部署模式、資料類型、應用程式和最終用戶分類-2026-2032年全球市場預測碘乙烷市場:依純度、包裝、應用及分銷管道分類的全球市場預測,2026-2032年

銫市場:按組件、部署模式、資料類型、應用程式和最終用戶分類-2026-2032年全球市場預測碘乙烷市場:依純度、包裝、應用及分銷管道分類的全球市場預測,2026-2032年 全球醋酸鉀市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球醋酸鉀市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026-2030年全球銫市場

2026-2030年全球銫市場 山梨酸鉀市場規模、佔有率和成長分析(按應用、形態、等級、通路和地區分類)-2026-2033年產業預測

山梨酸鉀市場規模、佔有率和成長分析(按應用、形態、等級、通路和地區分類)-2026-2033年產業預測 氫氧化銫市場規模、佔有率和成長分析(按產品類型、純度等級、應用、終端用戶產業和地區分類)-2026-2033年產業預測

氫氧化銫市場規模、佔有率和成長分析(按產品類型、純度等級、應用、終端用戶產業和地區分類)-2026-2033年產業預測 亞磷酸鉀:全球市佔率及排名、總收入及需求預測(2025-2031年)焦亞硫酸鉀:全球市佔率及排名、總收入及需求預測(2025-2031年)

亞磷酸鉀:全球市佔率及排名、總收入及需求預測(2025-2031年)焦亞硫酸鉀:全球市佔率及排名、總收入及需求預測(2025-2031年)