|

市場調查報告書

商品編碼

2043970

自動駕駛汽車ECU:市場佔有率分析、產業趨勢與統計及成長預測(2025-2030)Autonomous Vehicle ECU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

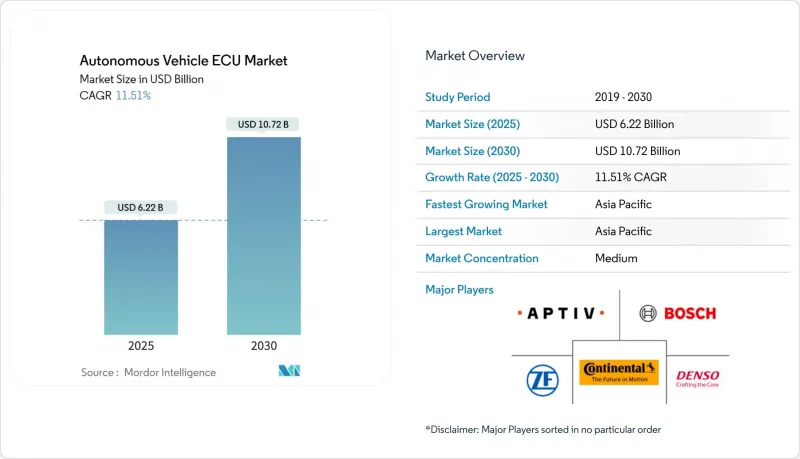

2025年自動駕駛汽車電子控制單元(ECU)市值為62.2億美元,預計2030年將達到107.2億美元。

預計預測期內的複合年成長率為 11.51%。

電控系統(ECU) 快速整合到網域控制器和區域控制器中,加上強制性電氣化和半導體技術的突破,正在推動這項擴張。汽車製造商正用少數高性能平台取代數十個傳統 ECU,這些平台能夠處理感測器融合、故障安全決策和空中下載 (OTA) 更新。隨著安全法規的日益嚴格,集中式架構能夠縮短線束長度、降低組件成本,並創造新的軟體收入來源。半導體技術的進步,特別是 28 奈米製程和寬能隙帶裝置,緩解了散熱限制,並實現了 L3-L4 級功能所需的計算密度。同時,區域分類策略降低了複雜性,並支援模組化車輛升級,從而擴大了對性能最佳化控制器的潛在需求。

全球自動駕駛汽車ECU市場趨勢及洞察

ADAS監理安全要求迅速提高

世界各國政府正強制要求新車配備自動緊急煞車、車道維持和駕駛監控功能,直接催生了對ASIL認證控制器的即時需求。歐盟通用安全法規將於2024年7月生效,美國的豁免政策正在加速國內測試,而聯合國第157號法規則為自動車道維持功能製定了全球標準。加州提出的框架增加了資料報告義務,這將促進集中式日誌記錄架構的發展。每項監管要求都增加了即時收斂、冗餘和安全診斷所需的計算量,從而為專注於安全的ECU供應商帶來了大量的訂單。

半導體計算技術的進步使得集中式ECU成為可能

汽車系統晶片(SoC) 採用 28 奈米製程節點整合 CPU、GPU 和 NPU,與 40 奈米產品相比,每瓦效能提升一倍。恩智浦 (NXP) 的 S32G 系列和瑞薩 (Renesas) 的 RH850/C1M-Ax 系列可在單一封裝內實現硬體加速佈線、感測器融合和雙馬達控制。碳化矽 (SiC) 和氮化鎵 (GaN) 功率元件可實現具有更高開關頻率的緊湊型逆變器 ECU,從而降低發熱量並提高效率。這使得 OEM 廠商能夠在不超出熱設計限制的情況下,省去 10-15 個分立模組,取而代之的是 2-3 個網域控制器,從根本上改變了供應商格局。

高效能ECU中熱管理和電源管理的局限性

具備強大人工智慧功能的汽車晶片會產生高達 100 W/cm² 的晶片熱通量,對 -40 度C至 85 度C的工作溫度範圍提出了嚴峻挑戰。液冷迴路和先進介面材料的使用會使每個控制器的成本增加 200 至 500 美元,從而對注重成本的晶片等級造成壓力。對於純電動車 (BEV) 而言,控制器冷卻與電池維護相互競爭,使得高溫運作週期下的電池組級熱設計更加複雜。

細分市場分析

在2024年的自動駕駛汽車ECU市場中,ADAS控制器佔了61.82%的佔有率。這反映了車道維持、緊急煞車和駕駛員監控功能在大眾市場車型中的標準化。此細分市場受益於強制性安全法規,並利用了成熟的32位元MCU和雷達/攝影機融合演算法,從而實現了成本和性能的良好平衡。供應商正專注於低功耗SoC和軟體工具鏈,以簡化ASIL B/C合規流程。

預計到2030年,自動駕駛系統將以13.21%的複合年成長率成長。這些平台整合了CPU、GPU和NPU,實現端到端的感知、規劃和執行,軟體容量也膨脹至數百GB。集中化設計支援OTA升級和基於雲端的檢驗循環,高性能ECU正成為支援L4級自動駕駛計程車和樞紐間貨運先導計畫的核心要素。

2024年,二級部分自動駕駛在自動駕駛汽車ECU市場中仍將佔據40.38%的市場佔有率,這主要得益於主動車距控制巡航系統和車道居中保持技術的普及。這些系統正在為硬體驅動型自動駕駛汽車奠定基礎,並將隨著法規的放寬,加速向更高級自動駕駛技術的過渡。

同時,L4級自動駕駛系統發展最為迅速,預計2030年將以14.18%的複合年成長率成長。在都市區的固定貨車路線和專用自動駕駛計程車路線上進行的商業試點計畫傾向於採用地理圍欄式運行區域,從而降低檢驗的複雜性。在控制器設計方面,為了符合聯合國歐洲經濟委員會(UN-ECE)ALKS指南,冗餘設計、故障降級模式和即時影像-雷射雷達融合等特性得到了重點關注。

區域分析

到2024年,亞太地區將佔據自動駕駛汽車ECU市場41.28%的佔有率,預計到2030年將以13.28%的複合年成長率成長。中國智慧城市示範計畫、韓國的半導體產業基礎以及日本在高級駕駛輔助系統(ADAS)領域的領先地位,是推動市場需求成長的主要動力。各國都在積極推進符合L3/L4標準的藍圖建設和強制性空中下載(OTA)網路安全更新,這些舉措提高了控制器的規範標準。

北美也正在效仿,這主要受到美國國家公路交通安全管理局 (NHTSA) 豁免政策和加州分階段核准模式的影響,後者要求詳細的資料登錄和故障安全認證。這些框架正在提高控制器記憶體容量和加密標準,並促進國內半導體產業的合作。

歐洲繼續發揮至關重要的作用,透過《通用安全法規》(GSR) 和第155號法規,網路安全和功能安全已納入所有車型。供應商強調符合ISO 21434標準和冗餘車道維持演算法,以滿足NCAP 2026評估標準。拉丁美洲、中東和非洲等新興地區正朝著符合聯合國歐洲經濟委員會(UN-ECE)標準的方向發展,但由於成本敏感度和基礎設施差異,進展較為緩慢。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- ADAS監理安全要求迅速提高

- 半導體計算技術的進步使得集中式ECU成為可能

- 動力傳動系統電氣化正在推動網域控制器的發展。

- OTA(空中下載)技術在聯網汽車領域的發展需要可擴展的運算能力。

- 由於軟體定義車輛 (SDV) 架構的出現,對客製化 ECU 的需求增加。

- 區域控制器的興起有助於降低物料清單成本

- 市場限制因素

- 高效能ECU中熱管理和電源管理的局限性

- 網路安全和功能安全合規成本負擔

- 受地緣政治因素影響,半導體供應鏈出現供不應求。

- 在基於人工智慧的自動駕駛ECU方面進行了大量領先研發投資。

- 價值/供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模及成長預測(價值(美元))

- ECU類型

- ADAS(進階駕駛輔助系統)

- 自動駕駛系統

- 按自動化級別

- 一級(駕駛輔助)

- 二級(部分自動化)

- 3級(有條件自動駕駛)

- 4級(高級自動化)

- 5級(全自動)

- 透過控制架構

- 集中式ECU

- 分散式ECU

- 混合動力ECU

- 車輛類型

- 搭乘用車

- 輕型商用車

- 中型和重型商用車輛

- 依推進類型

- 內燃機

- 電池式電動車(BEV)

- 混合動力電動車(HEV)

- 插電式混合動力汽車(PHEV)

- 燃料電池汽車(FCEV)

- 透過分銷管道

- OEM(Original Equipment Manufacturer)

- 售後市場

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 英國

- 德國

- 西班牙

- 義大利

- 法國

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 印度

- 中國

- 日本

- 韓國

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 埃及

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Robert Bosch GmbH

- Continental AG

- Aptiv PLC

- Denso Corporation

- ZF Friedrichshafen AG

- Valeo SA

- Magna International Inc.

- NVIDIA Corporation

- Mobileye Global Inc.

- Renesas Electronics Corporation

- NXP Semiconductors

- Texas Instruments Inc.

- Infineon Technologies AG

- Veoneer AB

- Hitachi Astemo Ltd.

- Hyundai Mobis Co., Ltd.

- Mitsubishi Electric Corporation

- Panasonic Automotive Systems

- Intel Corporation

- Autoliv Inc.

- Lear Corporation

第7章 市場機會與未來展望

The Autonomous Vehicle ECU market size is valued at USD 6.22 billion in 2025 and is projected to climb to USD 10.72 billion by 2030, registering an 11.51% CAGR during the forecast period.

Rapid consolidation of electronic control units into domain and zonal controllers, combined with electrification mandates and semiconductor breakthroughs, underpins this expansion. Automakers are replacing dozens of legacy ECUs with a handful of high-compute platforms that handle sensor fusion, fail-safe decision-making, and over-the-air (OTA) updates. As safety regulations tighten, centralized architectures shorten wiring harnesses, lower bill-of-materials costs, and create new software revenue streams. Semiconductor advances, especially 28 nm and wide-bandgap devices, ease thermal constraints and unlock the compute density necessary for Level 3-4 functions. Meanwhile, zoning strategies decrease complexity and enable modular vehicle upgrades, expanding addressable demand for performance-optimized controllers.

Global Autonomous Vehicle ECU Market Trends and Insights

Surge in ADAS Regulatory Safety Mandates

Governments now require automated emergency braking, lane keeping, and driver monitoring on new models, prompting immediate demand for ASIL-certified controllers. The EU General Safety Regulation applies from July 2024, while U.S. exemptions accelerate domestic testing, and UN Regulation No. 157 sets global standards for automated lane keeping. California's draft framework adds data-reporting obligations that favor centralized logging architecture. Each mandate increases compute loads for real-time fusion, redundancy, and secure diagnostics, cementing robust order books for safety-focused ECU suppliers.

Advances in Semiconductor Computing Enabling Centralized ECUs

Automotive-grade systems-on-chip integrate CPUs, GPUs, and NPUs on 28 nm nodes, doubling performance per watt over 40 nm parts. NXP's S32G family and Renesas' RH850/C1M-Ax line demonstrate hardware-accelerated routing, sensor fusion, and dual-motor control inside single packages. Silicon-carbide and gallium-nitride power devices allow compact inverter ECUs with higher switching frequencies, mitigating heat and boosting efficiency. OEMs can therefore retire 10-15 discrete modules in favor of two or three domain controllers without breaching thermal envelopes, reshaping the supplier landscape.

Thermal and Power Management Limits for High-Compute ECUs

AI-rich automotive chips push 100 W/cm2 die heat flux, challenging -40 °C to 85 °C reliability envelopes. Liquid loops and advanced interface materials add USD 200-500 per controller, pressuring cost-sensitive trims. For BEVs, controller cooling competes with battery conditioning, complicating pack-level thermal budgeting during hot-weather duty cycles.

Other drivers and restraints analyzed in the detailed report include:

- Electrification of Powertrains Boosting Domain Controllers

- Growth in Connected-Vehicle OTA Requiring Scalable Compute

- Cyber-Security and Functional-Safety Compliance Cost Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

ADAS controllers contributed 61.82% to the autonomous vehicle ECU market size in 2024, reflecting universal fitment of lane-keeping, emergency braking, and driver monitoring on mass-market models. The segment benefits from mandatory safety regulations and leverages mature 32-bit MCUs and radar-camera fusion algorithms that balance cost and performance. Suppliers focus on power-efficient SoCs and software toolchains that simplify ASIL B/C compliance.

Autonomous Driving Systems are projected to grow at a 13.21% CAGR through 2030. These platforms integrate CPUs, GPUs, and NPUs for end-to-end perception, planning, and actuation, swelling software payloads into the hundreds of gigabytes. Centralization enables OTA upgrades and cloud-based validation loops, positioning high-compute ECUs as the core enabler of Level 4 robo-taxis and hub-to-hub freight pilots.

Level 2 partial automation retained 40.38% of the autonomous vehicle ECU market share in 2024, thanks to the mass adoption of adaptive cruise and lane centering. These systems create a base of hardware-ready vehicles, accelerating the migration path to higher autonomy when regulations allow.

Level 4 stacks, however, are scaling fastest at 14.18% CAGR through 2030. Commercial pilots on fixed trucking lanes and urban robo-taxi corridors favor geo-fenced operation domains, reducing validation complexity. Controller designs emphasize redundancy, fail-degraded modes, and real-time image-lidar fusion to fulfill UN-ECE ALKS guidelines.

The Autonomous Vehicle ECU Market Report is Segmented by ECU Type (Advanced Driver Assistance Systems, and More), Level of Automation (Level 1, and More), Control Architecture (Centralized ECU, and More), Vehicle Type (Passenger Vehicles, and More), Propulsion Type (Internal Combustion Engine, and More), Distribution Channel (OEM and Aftermarket), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific captured 41.28 % of the autonomous vehicle ECU market share in 2024 and is advancing at a 13.28% CAGR through 2030. China's smart-city pilots, South Korea's semiconductor footprint, and Japan's ADAS leadership drive bulk demand. National roadmaps fund Level 3/4 highways and mandate OTA cyber-updates, lifting controller specification baselines.

North America follows, shaped by NHTSA exemptions and California's staged permitting model that requires detailed data logging and fail-safe proof points. These frameworks elevate controller memory budgets and encryption standards, stimulating domestic semiconductor collaborations.

Europe remains pivotal as the General Safety Regulation and Regulation No. 155 hard-wire cybersecurity and functional safety into every model. Suppliers emphasize ISO 21434 compliance and redundant lane-keeping algorithms to meet NCAP 2026 scoring. Emerging regions in Latin America, the Middle East, and Africa are aligning with UN-ECE templates yet progressing more slowly due to cost sensitivity and infrastructure gaps.

- Robert Bosch GmbH

- Continental AG

- Aptiv PLC

- Denso Corporation

- ZF Friedrichshafen AG

- Valeo SA

- Magna International Inc.

- NVIDIA Corporation

- Mobileye Global Inc.

- Renesas Electronics Corporation

- NXP Semiconductors

- Texas Instruments Inc.

- Infineon Technologies AG

- Veoneer AB

- Hitachi Astemo Ltd.

- Hyundai Mobis Co., Ltd.

- Mitsubishi Electric Corporation

- Panasonic Automotive Systems

- Intel Corporation

- Autoliv Inc.

- Lear Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in ADAS Regulatory Safety Mandates

- 4.2.2 Advances in Semiconductor Computing Enabling Centralized ECUs

- 4.2.3 Electrification of Powertrains Boosting Domain Controllers

- 4.2.4 Growth in Connected-Vehicle OTA Requiring Scalable Compute

- 4.2.5 Software-Defined Vehicle Architectures Increasing Custom ECU Demand

- 4.2.6 Emergence of Zonal Controllers Reducing BOM Costs

- 4.3 Market Restraints

- 4.3.1 Thermal and Power Management Limits for High-Compute ECUs

- 4.3.2 Cyber-Security and Functional-Safety Compliance Cost Burden

- 4.3.3 Semiconductor Supply-Chain Geopolitics Causing Shortages

- 4.3.4 High Upfront R&D Investment for AI-Based Autonomous ECUs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By ECU Type

- 5.1.1 Advanced Driver Assistance Systems (ADAS)

- 5.1.2 Autonomous Driving Systems

- 5.2 By Level of Automation

- 5.2.1 Level 1 (Driver Assistance)

- 5.2.2 Level 2 (Partial Automation)

- 5.2.3 Level 3 (Conditional Automation)

- 5.2.4 Level 4 (High Automation)

- 5.2.5 Level 5 (Full Automation)

- 5.3 By Control Architecture

- 5.3.1 Centralized ECU

- 5.3.2 Distributed ECU

- 5.3.3 Hybrid ECU

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Light Commercial Vehicles

- 5.4.3 Medium and Heavy Commercial Vehicles

- 5.5 By Propulsion Type

- 5.5.1 Internal Combustion Engine

- 5.5.2 Battery Electric Vehicle (BEV)

- 5.5.3 Hybrid Electric Vehicle (HEV)

- 5.5.4 Plug-In Hybrid Electric Vehicle (PHEV)

- 5.5.5 Fuel Cell Electric Vehicle (FCEV)

- 5.6 By Distribution Channel

- 5.6.1 OEM (Original Equipment Manufacturer)

- 5.6.2 Aftermarket

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 United Kingdom

- 5.7.3.2 Germany

- 5.7.3.3 Spain

- 5.7.3.4 Italy

- 5.7.3.5 France

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 India

- 5.7.4.2 China

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 United Arab Emirates

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 Turkey

- 5.7.5.4 Egypt

- 5.7.5.5 South Africa

- 5.7.5.6 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Continental AG

- 6.4.3 Aptiv PLC

- 6.4.4 Denso Corporation

- 6.4.5 ZF Friedrichshafen AG

- 6.4.6 Valeo SA

- 6.4.7 Magna International Inc.

- 6.4.8 NVIDIA Corporation

- 6.4.9 Mobileye Global Inc.

- 6.4.10 Renesas Electronics Corporation

- 6.4.11 NXP Semiconductors

- 6.4.12 Texas Instruments Inc.

- 6.4.13 Infineon Technologies AG

- 6.4.14 Veoneer AB

- 6.4.15 Hitachi Astemo Ltd.

- 6.4.16 Hyundai Mobis Co., Ltd.

- 6.4.17 Mitsubishi Electric Corporation

- 6.4.18 Panasonic Automotive Systems

- 6.4.19 Intel Corporation

- 6.4.20 Autoliv Inc.

- 6.4.21 Lear Corporation

7 Market Opportunities & Future Outlook

2026-2030年全球港口營運智慧市場

2026-2030年全球港口營運智慧市場 水上運動車輛市場-全球產業規模、佔有率、趨勢、機會與預測:按車輛類型、通路、地點、地區和競爭格局分類,2021-2031年自動駕駛汽車ECU市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、車輛類型、需求類別、地區和競爭格局分類,2021-2031年

水上運動車輛市場-全球產業規模、佔有率、趨勢、機會與預測:按車輛類型、通路、地點、地區和競爭格局分類,2021-2031年自動駕駛汽車ECU市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、車輛類型、需求類別、地區和競爭格局分類,2021-2031年 全球國防機器人與自動駕駛車輛市場:2026-2036 年

全球國防機器人與自動駕駛車輛市場:2026-2036 年 自動駕駛汽車市場規模、佔有率、趨勢和預測:按組件、自動化程度、應用和地區分類,2026-2034年

自動駕駛汽車市場規模、佔有率、趨勢和預測:按組件、自動化程度、應用和地區分類,2026-2034年 人工智慧(AI)在自動駕駛汽車領域的市場:未來預測(至2034年)-按組件、自動駕駛等級、車輛類型、類別、應用、最終用戶和地區進行分析

人工智慧(AI)在自動駕駛汽車領域的市場:未來預測(至2034年)-按組件、自動駕駛等級、車輛類型、類別、應用、最終用戶和地區進行分析 自動駕駛汽車市場:2026-2032年全球市場預測(依自動駕駛等級、動力系統、技術、最終用戶和車輛類型分類)

自動駕駛汽車市場:2026-2032年全球市場預測(依自動駕駛等級、動力系統、技術、最終用戶和車輛類型分類) 2026年全球衛星港口營運監控市場報告2034年全球自動駕駛物流車輛市場預測-按車輛類型、組件、導航技術、自動駕駛等級、應用、最終用戶和地區分類的全球分析2034年自主港口營運市場預測:按自動化程度、設備類型、技術、應用、最終用戶和地區分類的全球分析

2026年全球衛星港口營運監控市場報告2034年全球自動駕駛物流車輛市場預測-按車輛類型、組件、導航技術、自動駕駛等級、應用、最終用戶和地區分類的全球分析2034年自主港口營運市場預測:按自動化程度、設備類型、技術、應用、最終用戶和地區分類的全球分析