|

市場調查報告書

商品編碼

2043963

貨物檢驗:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Cargo Inspection - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

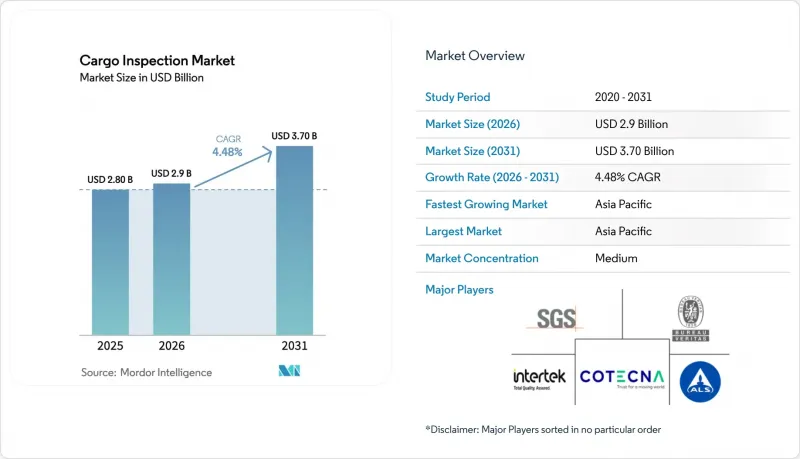

預計到 2025 年,貨物檢驗市場規模將達到 28 億美元,到 2026 年將達到 29 億美元,到 2031 年將達到 37 億美元,2026 年至 2031 年的複合年成長率為 4.48%。

更嚴格的監管顯然正在促進成長。海關計畫將道德行為要求正式化,擴大了小規模貿易業者的AEO(經認證的經營者)計畫範圍,並實現了對供應鏈的早期風險干預。領先的檢驗服務提供者正在對其營運進行現代化改造,透過數位化工作流程和遠端操作,加快了公共部門合約的處理速度,提高了透明度。中東和南亞港口的擴建預計將增加貨物吞吐量,並為品質、數量和安全檢查提供更多環節。隨著跨境電子商務日益分散,海關被迫提高數據質量,篩檢小批量貨物,並實施非侵入式檢驗。然而,在實施過程中仍然存在一些差距,例如資金限制、現場準備不足和人員短缺,因為在掃描目標和數位化里程碑方面仍然存在挑戰,這推動了對第三方檢驗和風險分析服務的需求。

全球貨物檢驗市場趨勢及洞察

嚴格的監管要求和海關合規

世界海關組織(WCO)修訂的2025年安全框架擴大了經認證經營者(AEO)認證的範圍,將微型和小型企業納入其中,並引入了強制性道德準則。此舉圖加強對經認證經營者的管治,並提高對內部威脅的防範。美國政策趨勢表明,陸地邊境的掃描率將大幅提高,但2024會計年度乘用車和商用車的掃描率分別僅為8%和27%,這意味著第三方檢驗支援和技術應用仍有提升空間。美國計劃在2026會計年度部署38套額外的非侵入式檢驗系統,旨在加強西南邊境的檢驗網路,其中期目標為私家車40%和商用卡車70%。這將加重檢驗工作的負擔。歐洲關稅改革取消了150歐元的關稅豁免,並賦予電子商務平台更大的責任。同時,審計發現低價值貨物的少報和不合格率較高,這表明上游工程檢驗和數據品質保證將發揮更關鍵的作用。各地區日益嚴格的法規提升了經認可的檢驗夥伴關係關係、自動化文件和裝貨前檢驗的價值,尤其對於詐騙和安全風險較高的貨物而言更是如此。包括ISO和各國認可機構在內的認證系統正在塑造跨司法管轄區檢驗協議的檢驗和核准方式,並朝著即時資料交換的方向發展。

無損檢測系統的技術進步

在海關現代化專案中,人工智慧、物聯網和機器學習被視為提升影像分析、風險評分和貨物追蹤能力的核心工具。這將提高檢測率,同時不會延誤合規貨物的清關。世界海關組織支援的全球案例研究展示了人工智慧驅動的風險管理和掃描儀間互通性的應用。同時,美國西南邊境的一項類似舉措側重於訓練演算法,以檢測異常情況並將其提交給官員審查。隨著各國政府投資高能量移動貨物檢查系統以及用於港口和邊境檢查站的配套篩檢設備,採購勢頭持續強勁。這增強了移動系統的覆蓋範圍,尤其是在那些因施工限制和場地條件限制而難以安裝固定設備的地區。這些專案需要精心協調和現場整合,以避免干擾其他偵測設備,從而防止在複雜且高流量的環境中出現成本超支和工期延誤。預算限制、建造前置作業時間以及系統工程要求導致各國海關在採用人工智慧輔助檢查服務方面持續存在差異,造成了人工智慧輔助檢查服務與傳統X光設備並存的局面。隨著各國海關協調資料流並規範操作流程,與不斷發展的技術標準(包括國際和區域組織制定的標準)的互通性變得日益重要。

大量資本投資和實施成本

大規模無損檢測 (NTV) 設施的安裝面臨許多挑戰,例如施工、空間和系統整合等,這些都會延長工期並增加成本。因此,掃描率的提升遠未達到法定目標。美國的實施情況清楚地表明了這一點:由於安裝限制和與其他系統的干擾導致進展緩慢,2024 會計年度乘用車和商用車的掃描率分別僅為 8% 和 27%。在港口,碼頭的擴建,包括自動化、電氣化和深水泊位的建設,需要大量資金投入,這給營運商帶來了越來越大的壓力,迫使他們透過提高吞吐能力和營運效率來收回成本。新的海事安全法規增加了對船東的檢驗和認證要求,導致持續的遵循成本。這不僅增加了對檢驗和檢驗的需求,也提高了整個船隊的生命週期成本。在新興市場,為了實現投資多元化,通常採用分階段採購和官民合作關係(PPP) 模式,但這會延緩全面功能的實現,同時也會使供應商管理和績效監控變得更加複雜。提供靈活經營模式和模組化部署的檢測服務提供者能夠很好地適應有限的預算和不斷變化的現場準備。

細分市場分析

到2025年,石油和天然氣產業將佔貨物檢驗市場佔有率的43.13%,這反映出散裝碳氫化合物運輸長期以來對品質和數量認證的依賴。同時,受日益嚴格的純度標準和可追溯性要求的推動,預計到2031年,化學和化肥行業將呈現最高的成長率,達到7.43%。隨著煉油和調配活動的增加,對生質燃料、船用燃料和永續航空燃料的檢測需求也在不斷成長,供應商正在擴展其分析能力,以滿足新型原料和低碳產品的規格要求。國際肥料協會的產品管理框架正在擴大其範圍,涵蓋產品的整個生命週期,深化從生產到儲存和分銷的檢驗覆蓋範圍,第三方審核也繼續根據高績效標準評估設施。金屬和礦物檢測仍然是一個穩定的業務領域,銅和金的交易為實驗室服務和現場測試提供了支持,並且正在進行有針對性的收購,以增強地球化學專業知識和區域影響力。農產品檢驗受惠於糧食品質標準、清晰的程序和收費系統,即使出貨量隨季節波動,檢驗需求仍保持穩定。消費品檢驗則受到新的電子報告要求和更嚴格的資料交換規則的影響,這些要求和規則將合規程序上游工程,並強化了對裝貨前檢驗和文件完整性的需求。

從2019年到2025年,石油和天然氣產業是貨物檢驗市場的主要驅動力,但隨著永續發展期望、管理標準和生命週期文件需求的不斷成長,化學和化肥領域也經歷了快速成長。貨物檢驗行業正積極應對這一趨勢,推出集測試、認證和遠端審核於一體的打包服務,以在控制成本和交付壓力的同時,維持貸款方和買家所期望的保證水準。在金屬和礦產行業的上游服務方面,隨著礦業資本投資週期和探勘活動的進行,市場保持成長勢頭,地球化學分析和現場實驗室的需求也隨之成長。在農業領域,標準化的檢驗費用和一致的品質標準有助於穩定服務需求,因為出口商需要適應運輸路線的調整和氣候變遷。在消費品領域,數位憑證的提交和基於平台的資料交換正在重塑檢驗、檢驗和文件編制流程,從而有助於早期療育,避免邊境延誤。現有公司正努力透過收購主導的業務擴張來維持獲利能力,其目標是引入數位化工作流程工具,擴大成長地區的檢驗能力,並增強其全球網路的韌性。

《貨物檢驗市場報告》按貨物類型(石油和天然氣、金屬和礦產、其他)、服務類型(品質和數量檢驗、重量和吃水檢驗、損壞和污染檢驗、裝運前/裝載前檢驗、其他)以及地區(北美、南美、亞太、歐洲、中東和非洲)進行細分。市場預測以美元計價。

區域分析

預計到2025年,亞太地區將佔據貨物檢驗市場佔有率的30.76%,並在2031年之前維持7.81%的年均成長率,成為該地區成長最快的市場。這主要得益於碼頭升級、海關數位化以及電子商務小包裹的激增。印度的「薩加爾馬拉」(Sagarmala)計畫大規模提升了貨物處理能力,將船舶平均停留時間縮短至49.47小時。同時,正在進行的連接工程也在持續圖,以使陸路交通與新的碼頭吞吐能力相匹配。在阿拉伯半島東部,吉達碼頭的擴建使貨物處理量增加了一倍以上,並新增了一座大型冷藏貨櫃檢驗設施。這不僅改善了生鮮產品的配送,也提高了人們對檢驗和文件處理服務水準的期望。傑貝阿里港電動碼頭車輛和電動貨物裝卸設備的擴建,標誌著該港口正向低排放氣體營運模式轉型,由此帶來的效率提升也為進一步的數位投資創造了空間。這些項目將貨物流集中到大規模樞紐,增加了檢查團隊進行貨量規劃的需求,並進一步提升了在堵塞口岸實施系統性准入協議的價值。在全部區域,海關和港口當局正在擴大技術和培訓的應用,從而促進檢查系統與價值鏈資料平台之間的互通性。

在北美,陸地邊境掃描覆蓋範圍的擴大正在推進,2026會計年度將新增非侵入式偵測設備。隨著系統運作,預計檢查數量及相關服務需求將會增加。監測評估凸顯了高流量邊境檢查站的建設挑戰和空間限制,建議分階段推廣,待各站點準備就緒並控制干擾風險後再進行。在聯邦採購中,例如糧食援助船舶監控,第三方保證機制繼續用於管理專案的品質和完整性。在私營部門,整合和能力建構尤其重要,包括購買專注於專業測試、校準和取證的設備,以補充檢查和檢驗工作。消費品法規新增了電子申報要求,這將影響資料和憑證的工作流程,從而提升將產品合規性與海關申報關聯起來的軟體模組的重要性。總而言之,這些發展趨勢指向一個更自動化、數據驅動的海關環境,並擴大了檢查合作夥伴在規劃和執行中的作用。

歐洲正分階段推動海關改革,旨在取消150歐元的最低閾值,擴大平台責任範圍,上游工程檢驗流程,並強調準確收集數據。歐盟中央海關資料中心將集中管理並規範提交的文件,為檢驗服務提供者提供機會,使其能夠將測試結果、證書和補充記錄整合到標準化格式中。有關卸貨設備和燃油取樣的海事法規已更新,以加強設備認證和取樣要求,從而強化船上檢驗和檢查室支援。在整個歐洲,經認證的經營者(AEO)計畫和國家認證標準持續為檢驗協議的認可和檢驗機構的能力奠定基礎。歐盟改革的成功取決於海關資訊技術系統和電子商務平台的順利整合,這可能會在短期內影響貨物停留時間和檢驗安排。在整個預測期內,結構性改革和技術的穩定應用預計將推動對高價值貨物和合規關鍵物品檢驗的強勁需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 全球貿易量成長與跨境電子商務擴張

- 嚴格的監管要求和海關合規

- 安全威脅日益加劇,走私問題令人擔憂

- 無損檢測(NII)系統的技術進步

- 電子商務的快速發展以及對小包裹檢驗的需求。

- 新興市場的基礎建設

- 市場限制因素

- 大量資本投資和實施成本

- 操作複雜性與技術專長要求

- 隱私問題和資料安全問題

- 維護挑戰和生命週期成本

- 價值/供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

- 移動式和模組化檢測解決方案正在迅速發展。

- 公私合營正在推動市場創新。

第5章 市場規模及成長預測(價值,2020-2031 年)

- 貨物類型

- 石油和天然氣

- 金屬和礦物

- 農產品

- 化學品/肥料

- 消費品

- 其他

- 按服務類型

- 品質和數量驗證

- 重量和吃水調查

- 損壞和污染檢查

- 裝運前/裝載前檢驗

- 船用燃料數量和燃料品質調查

- 貨物裝卸主管

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 秘魯

- 智利

- 阿根廷

- 南美洲其他地區

- 亞太地區

- 印度

- 中國

- 日本

- 澳洲

- 韓國

- 東南亞

- 亞太其他地區

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 比荷盧經濟聯盟(比利時、荷蘭、盧森堡)

- 北歐國家(丹麥、芬蘭、冰島、挪威、瑞典)

- 其他歐洲地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SGS SA

- Bureau Veritas SA

- Intertek Group plc

- Cotecna Inspection SA

- ALS Limited

- Eurofins Scientific

- TUV SUD

- TUV Rheinland

- Dekra SE

- DNV AS

- CCIC(China Certification & Inspection(Group))

- Core Laboratories(Saybolt)

- Peterson & Control Union

- Applus+

- AIM Control Group

- Q&Q Control Services

- Marine Inspection LLC

- Alex Stewart International(ASI)

- OMIC USA

- Camin Cargo Control

第7章 市場機會與未來展望

The Cargo Inspection Market size is projected to be USD 2.80 billion in 2025, USD 2.9 billion in 2026, and reach USD 3.70 billion by 2031, growing at a CAGR of 4.48% from 2026 to 2031.

Regulatory tightening is a clear growth catalyst as customs programs formalize requirements for ethical conduct, AEO coverage for smaller traders, and earlier risk interventions in the supply chain. Operational modernization is underway within major inspection providers, with digital workflows and remote operations allowing faster turnarounds and better transparency for public-sector contracts. Port expansions in the Middle East and South Asia elevate throughput expectations and increase touchpoints for quality, quantity, and safety checks. Rising parcelization from cross-border e-commerce pushes customs to strengthen data quality, small-parcel screening, and non-intrusive inspection deployment. Execution gaps remain as scanning targets and digitalization milestones run into capital constraints, site readiness issues, and staffing shortfalls, which sustain demand for third-party inspection and risk analytics services.

Global Cargo Inspection Market Trends and Insights

Stringent Regulatory Requirements and Customs Compliance

The World Customs Organization's 2025 SAFE Framework update widened AEO eligibility to micro, small, and medium-sized enterprises and introduced mandatory ethics codes, anchoring stronger governance for certified traders and greater vigilance against insider threats. U.S. policy momentum points to much higher scan rates at land borders, although fiscal year 2024 performance lagged with 8% scanning of passenger vehicles and 27% for commercial vehicles, which keeps the door open for expanded third-party inspection support and technology rollouts. The U.S. plan to deploy 38 additional non-intrusive inspection systems in fiscal year 2026 targets stronger coverage on the southwest border, with interim targets of 40% for privately owned vehicles and 70% for commercial trucks that will raise inspection workloads. Europe's customs reform removes the EUR 150 duty exemption and places more responsibility on e-commerce platforms, while audits show a high share of undervaluation and non-compliance within low-value consignments, signaling a larger role for upstream verification and data-quality assurance. Tightening across regions increases the value of certified inspection partnerships, automated documentation, and pre-loading verification, especially for categories with higher fraud or safety risks. Accreditation ecosystems, such as ISO and national accreditation bodies, shape how inspection protocols are validated and recognized across jurisdictions, with a shift toward real-time data exchange.

Technological Advancements in Non-Intrusive Inspection Systems

Customs modernization programs highlight AI, IoT, and machine learning as core tools that improve image analytics, risk scoring, and cargo tracking, which lifts detection rates without slowing clearance of compliant shipments. Country cases supported by the WCO showcase deployments of AI-driven risk management and scanner interoperability, while similar efforts along the U.S. southwest border focus on training algorithms to flag anomalies for officer review. Procurement momentum continues as governments invest in high-energy mobile cargo inspection systems and complementary screening units for ports and border crossings, strengthening mobile coverage where construction or site constraints limit fixed installations. These projects require careful calibration and site integration to avoid interference with other detection assets, which has driven cost overruns and schedule slips in complex, high-traffic environments. Adoption remains uneven across customs administrations due to budget limits, construction lead times, and systems engineering demands, which creates a bifurcated landscape of AI-augmented inspection services and legacy X-ray equipment. Interoperability with evolving technical standards, including those issued by international or regional bodies, increases in importance as authorities coordinate data flows and align operating procedures.

High Capital Investment and Implementation Costs

Large-scale non-intrusive inspection installations face construction, space, and systems-integration hurdles that extend schedules and increase costs, which slow scan-rate improvements against statutory targets. U.S. deployments illustrate these realities, with fiscal year 2024 scan rates reaching only 8% for passenger vehicles and 27% for commercial vehicles as site constraints and interference with other systems delayed progress. At ports, terminal expansions that integrate automation, electrification, and deep-water berths require significant capital, which intensifies pressure on operators to recover costs through higher throughput and operational efficiencies. New maritime safety rules add survey and certification requirements that drive recurring compliance spending for shipowners, expanding demand for inspection and verification but also elevating lifecycle costs across fleets. Emerging markets often turn to phased procurement or PPP structures to spread out investment, which can defer full capability while complicating vendor management and performance oversight. Inspection providers that offer flexible commercial models and modular deployments are better placed to align with constrained budgets and evolving site-readiness conditions.

Other drivers and restraints analyzed in the detailed report include:

- Infrastructure Development in Emerging Markets

- Increasing Global Trade Volumes and Cross-Border Commerce

- Operational Complexity and Technical Expertise Requirements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Oil and gas held 43.13% of the cargo inspection market share in 2025, reflecting a long-standing reliance on quality and quantity certification for bulk hydrocarbon shipments, while chemicals and fertilizers are projected to post the fastest growth at 7.43% through 2031 as purity standards and traceability mandates tighten. Demand for biofuel, marine fuel, and sustainable aviation fuel testing is rising in step with refinery and blending activity, and suppliers are expanding analytical capacity to address new feedstocks and lower-carbon product specifications. The International Fertilizer Association's Product Stewardship framework broadened scope across the product lifecycle, which deepens the inspection footprint from production to storage and distribution, and third-party audits continue to benchmark facilities against high-performance thresholds. Metals and minerals inspection remains a steady line of business as copper and gold activity supports laboratory services and onsite testing, with targeted acquisitions used to add geochemical depth and local reach. Agriculture commodities inspection benefits from grain quality standards, defined procedures, and fee structures that sustain verification demand even when shipment volumes vary by season. Consumer goods inspection is being shaped by new e-filing requirements and stronger data exchange rules, which push more compliance steps upstream and reinforce demand for pre-loading verification and documentation integrity.

From 2019-2025, oil and gas dominated the cargo inspection market, but the chemicals and fertilizers segment accelerated as sustainability expectations, stewardship standards, and lifecycle documentation needs expanded. The cargo inspection industry is responding with bundled offerings that combine testing, certification, and remote audits to manage cost and timing pressures while preserving assurance levels expected by lenders and buyers. Upstream services in metals and minerals maintained momentum through mining capital spending cycles and exploration activity, which reinforced demand for geochemical analysis and onsite labs. In agriculture, standardized inspection rates and consistent quality criteria helped stabilize service demand even as exporters adapted to route adjustments and weather variations. For consumer goods, digital certificate filing and platform-based data exchange are reshaping the points at which inspection, verification, and documentation happen, driving earlier interventions to avoid border delays. Incumbents are defending margins with digital workflow tools and acquisition-led expansions that add laboratory scale in growth corridors and build resilience into global networks.

The Cargo Inspection Market Report is Segmented by Cargo Type (Oil & Gas, Metals & Minerals, and More), by Service Type (Quality & Quantity Verification, Weight & Draft Survey, Damage & Contamination Inspection, Pre-shipment/Pre-loading Inspection, Others), and by Geography (North America, South America, Asia-Pacific, Europe, Middle East and Africa). Market Forecasts are Provided in Value (USD).

Geography Analysis

Asia-Pacific held 30.76% of the 2025 cargo inspection market share and is set to record the fastest regional growth at 7.81% through 2031, supported by terminal upgrades, customs digitization, and e-commerce parcel surges. India's Sagarmala projects added handling capacity at scale and cut average vessel turnaround time to 49.47 hours, while ongoing connectivity works continue to align landside links with new terminal capacity. East of the Arabian Peninsula, the Jeddah terminal expansion more than doubled throughput and added a high-capacity reefer inspection facility, which improves perishable flow while raising service-level expectations for verification and documentation. Jebel Ali's expansion of electric terminal vehicles and electric handlers shows a move toward lower emissions operations, and related efficiencies create scope for further digital investment. These projects concentrate cargo flows in large hubs, which elevates throughput planning needs for inspection teams and reinforces the value of structured access agreements at busy gateways. Region-wide, customs and port authorities are expanding technology use and training, which promotes interoperability between inspection systems and supply-chain data platforms.

North America is moving to lift scan coverage at land borders through additional non-intrusive inspection deployments in fiscal year 2026, which will generate more inspection events and associated service demand as systems come online. Oversight reviews have flagged construction challenges and space constraints at high-traffic crossings, which implies a staggered ramp as sites are readied and interference risks are managed. Federal procurement, such as vessel observation for food aid, shows continued use of third-party assurance to manage program quality and integrity. Within the private sector, consolidation and capability expansions are notable, including acquisitions focused on specialized testing, calibration, and forensics that complement inspection and verification work. Consumer product rules are adding e-filing requirements that will affect data and certificate workflows, raising the importance of software modules that tie together product compliance and customs entry. Together, these actions show a path to a more automated and data-anchored clearance environment that expands the role of inspection partners in planning and execution.

Europe is preparing for a phased customs reform that removes the EUR 150 de minimis threshold and shifts more responsibility to platforms, which will push more verification steps upstream and emphasize clean data capture. The central EU Customs Data Hub is positioned to centralize and harmonize submissions, which creates opportunities for inspection providers that can integrate test results, certificates, and supporting records into standardized formats. Maritime rules on lifting appliances and fuel-oil sampling update equipment certification and sampling requirements, which reinforce shipboard verification and lab support. Across Europe, AEO programs and national accreditation standards continue to set the stage for recognition of inspection protocols and lab competence. The success of EU reforms will depend on smooth integration with customs IT and e-commerce platforms, which could influence dwell time and inspection scheduling in the near term. Over the forecast, structural reforms and steady technology adoption support consistent demand for inspection across high-value goods and compliance-sensitive categories.

- SGS SA

- Bureau Veritas SA

- Intertek Group plc

- Cotecna Inspection SA

- ALS Limited

- Eurofins Scientific

- TUV SUD

- TUV Rheinland

- Dekra SE

- DNV AS

- CCIC (China Certification & Inspection (Group))

- Core Laboratories (Saybolt)

- Peterson & Control Union

- Applus+

- AIM Control Group

- Q&Q Control Services

- Marine Inspection LLC

- Alex Stewart International (ASI)

- OMIC USA

- Camin Cargo Control

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Global Trade Volumes and Cross-Border Commerce

- 4.2.2 Stringent Regulatory Requirements and Customs Compliance

- 4.2.3 Rising Security Threats and Contraband Smuggling Concerns

- 4.2.4 Technological Advancements in Non-Intrusive Inspection (NII) Systems

- 4.2.5 E-commerce Boom and Small Parcel Inspection Demands

- 4.2.6 Infrastructure Development in Emerging Markets

- 4.3 Market Restraints

- 4.3.1 High Capital Investment and Implementation Costs

- 4.3.2 Operational Complexity and Technical Expertise Requirements

- 4.3.3 Privacy Concerns and Data Security Issues

- 4.3.4 Maintenance Challenges and Lifecycle Costs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Mobile and Modular Inspection Solutions Gaining Traction

- 4.9 Public-Private Partnerships Driving Market Innovation

5 Market Size & Growth Forecasts (Value, 2020-2031)

- 5.1 By Cargo Type

- 5.1.1 Oil & Gas

- 5.1.2 Metals & Minerals

- 5.1.3 Agriculture Commodities

- 5.1.4 Chemicals & Fertilizers

- 5.1.5 Consumer Goods

- 5.1.6 Others

- 5.2 By Service Type

- 5.2.1 Quality & Quantity Verification

- 5.2.2 Weight & Draft Survey

- 5.2.3 Damage & Contamination Inspection

- 5.2.4 Pre-shipment/Pre-loading Inspection

- 5.2.5 Bunker Quantity & Fuel Quality Survey

- 5.2.6 Loading/Unloading Supervision

- 5.2.7 Others

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Peru

- 5.3.2.3 Chile

- 5.3.2.4 Argentina

- 5.3.2.5 Rest of South America

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 South East Asia

- 5.3.3.7 Rest of Asia-Pacific

- 5.3.4 Europe

- 5.3.4.1 United Kingdom

- 5.3.4.2 Germany

- 5.3.4.3 France

- 5.3.4.4 Spain

- 5.3.4.5 Italy

- 5.3.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.3.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.3.4.8 Rest of Europe

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab of Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 South Africa

- 5.3.5.4 Nigeria

- 5.3.5.5 Rest of Middle East And Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 SGS SA

- 6.4.2 Bureau Veritas SA

- 6.4.3 Intertek Group plc

- 6.4.4 Cotecna Inspection SA

- 6.4.5 ALS Limited

- 6.4.6 Eurofins Scientific

- 6.4.7 TUV SUD

- 6.4.8 TUV Rheinland

- 6.4.9 Dekra SE

- 6.4.10 DNV AS

- 6.4.11 CCIC (China Certification & Inspection (Group))

- 6.4.12 Core Laboratories (Saybolt)

- 6.4.13 Peterson & Control Union

- 6.4.14 Applus+

- 6.4.15 AIM Control Group

- 6.4.16 Q&Q Control Services

- 6.4.17 Marine Inspection LLC

- 6.4.18 Alex Stewart International (ASI)

- 6.4.19 OMIC USA

- 6.4.20 Camin Cargo Control