|

市場調查報告書

商品編碼

2043962

六水硝酸鎂:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Magnesium Nitrate Hexahydrate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

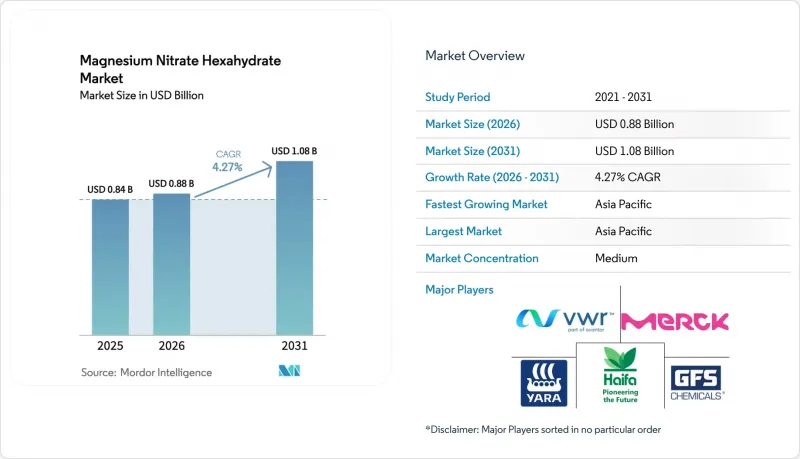

預計六水硝酸鎂的市場規模將從 2025 年的 8.4 億美元擴大到 2026 年的 8.8 億美元,到 2031 年將達到 10.8 億美元,2026 年至 2031 年的複合年成長率為 4.27%。

需求成長主要受兩個協同因素驅動。首先,溫室和滴灌農場正從使用硝酸銨鈣轉向使用水溶性硝酸鎂,以便在不提高土壤pH值的情況下同時糾正氮和鎂的缺乏,從而直接提升了肥料產品的需求。其次,工業用戶高度重視該化合物在硝酸鹽濃度方面的吸濕性、在採礦炸藥中的氧化平衡作用以及在相變儲熱中的潛熱特性。這些因素共同作用,形成了持續且多樣化的需求,從而緩解了農業週期的波動。競爭程度仍然適中。這是因為肥料級、工業級和試劑級產品在品質規格上有顯著差異,從而自然形成客戶鎖定,並允許專業生產商根據純度定價。雖然上游鎂價格的波動會帶來利潤風險,但隨著阿肯色州和巴西的專案即將交付首批產品,供應鏈正逐步走向在地化。預計這項發展將緩解原物料價格突變對預測期後半段下游複合生產商的影響。

全球六水硝酸鎂市場趨勢及洞察

對特種肥料和水溶性肥料的需求不斷成長

精準施肥系統使種植者能夠根據蒸騰速率調整養分,其中硝酸鎂溶液以中性形式提供16%的氮和9.4%的鎂。 2026年的田間試驗證實,0.5%的種子處理劑即使在乾旱脅迫下也能將玉米發芽率提高12%,這支持了其增強作物抗逆性的作用。 2025年,一座年產6000噸的生產廠在巴西運作,使當地經銷商能夠以兩週的前置作業時間(而非之前的六週)供應水溶性產品,從而消除了咖啡和柑橘種植者長期以來面臨的物流障礙。 2025年的葉面噴布試驗表明,2%的噴施溶液可使甜玉米穗重增加9%,花腐病減少22%,證明了該化合物在保護商品產量方面的作用。隨著滴灌系統在農場的普及,需求逐漸增加,這種促進劑的全部效果將在中期內顯現。

催化劑原料在精細化工領域的應用日益廣泛。

硝酸鎂經煅燒可轉化為高比表面積的氧化鎂。這項特性使其成為極具價值的路易斯酸催化劑。 2025年的一項研究表明,由此鹽製得的氧化鎂在120 度C下可將酮轉化為醇,轉化率高達94%,且單位轉化成本優於鈀。石油化工許可公司指定使用2N至5N級氧化鎂作為重整和分解催化劑的載體,因為該等級氧化鎂不會釋放硫,而硫在分解過程中會使活性金屬中毒。由於其具有脫水性能,在生產純度為95wt%的硝酸時,氧化鎂可取代硫酸,而95wt%的硝酸是製造炸藥和某些藥物活性成分所必需的。鑑於製藥領域的檢驗週期通常需要4-6年,因此應從長遠觀點看待氧化鎂的發展前景。

硝酸鹽排放的健康和環境監測

在美國,飲用水中硝酸鹽氮的含量限制為10毫克/公升;在歐盟,地下水中硝酸鹽氮的含量限制為50毫克/公升。這些規定要求受影響地區的農民減少水溶性硝酸鹽的使用或種植覆蓋作物。考慮引入硝酸鎂凝聚劑的市政污水處理廠必須證明殘留硝酸鹽的含量在排放許可證規定的限值範圍內。目前,許多排放許可證對磷和硝酸鹽的含量都有雙重限制,這使得產業計畫變得複雜。美國環保署(EPA)2024年的報告指出,農業徑流與墨西哥灣的低氧區域有關,這加速了各州強制使用緩釋肥料的法規訂定,並在短期內抑制了市場需求。監管機構已經開始執行這些限制措施,因此短期內市場需求的抑制顯而易見。

細分市場分析

預計到2025年,肥料級六水硝酸鎂將佔據51.28%的市場佔有率,並以5.03%的複合年成長率成長,這主要得益於保護性農業面積的增加以及可溶性混合物取代了散裝白雲石石灰。工業級六水硝酸鎂的成長速度放緩,主要是由於硝酸濃縮液、催化劑和石油化工催化劑的需求趨於成熟,但多年期合約確保了即使在肥料市場低迷時期也能獲得穩定的收入。試劑級六水硝酸鎂的純度為98%至99.5%,主要供應給分析實驗室和藥物合成等細分市場,由於需要批次追溯,其價格比通用級高出50%至80%。

隨著製藥業驗證週期的結束和水質檢測套組需求的成長,試劑級六水硝酸鎂的市場規模預計將顯著擴大。雖然化肥級價格仍與全球氮肥價格指數掛鉤,但巴西新廠降低的運輸成本可能會使供應成本價差擴大8-10%,使交付在上游鎂價波動的情況下也能維持在較高水準。能夠靈活調整不同等級產量的供應商可以透過套利從暫時的價格上漲中獲利,但由於大多數工廠都是為特定用途而建,預計市場集中度將保持在中等水平。

預計到2025年,脫水劑的應用將佔銷售額的35.22%,年複合成長率為4.78%。這是因為製藥和炸藥製造商依賴這種鹽來生產高達95%的無硫酸鹽污染的硝酸。對氧化劑的需求與礦業炸藥調查計畫密切相關,其中許多項目正處於高級試點階段,因此短期成長將較為溫和。然而,如果法規進一步限制純硝酸銨的使用,則可能成為成長的轉捩點。

隨著滴灌種植面積的擴大,六水硝酸鎂作為肥料和灌溉增溶劑的市場規模預計將達到更高水準。儘管催化劑促進劑的需求量佔總需求量的不到10%,但由於氧化物叢集作為低成本載體在精細化學品過渡加氫製程的應用,預計其利潤率成長將最為顯著。按功能分類,市場呈現典型的「雙引擎」結構,由大規模農業應用和小規模、高附加價值的化工細分市場組成。

區域分析

2025年,亞太地區佔全球銷售額的25.12%,成為六水硝酸鎂市場的主要驅動力。預計該地區也將維持最高的成長率,到2031年複合年成長率將達到4.96%。中國在原鎂上游的主導地位確保了國內硝酸鎂生產商穩定的原料供應,使得其工廠價格在大多數月份比進口價格低12-18%。印度政府透過「總理農業灌溉計畫」(Pradhan Mantri Krishi Sinchayee Yojana)對微灌進行補貼,促進了番茄和辣椒種植者採用化肥灌溉,從而加速了對可溶性硝酸鎂的需求。儘管產量較低,但日本和韓國採購高純度試劑級硝酸鎂,支撐了其較高的單位利潤率。

北美是硝酸鹽銷售的第二大市場,主要來源包括美國的工業和實驗室消費以及墨西哥保護主義農業的快速成長。 2025年12月,根據《國防生產法》,在阿肯色州建造一座鹽水製金屬轉化工廠獲得核准。運作後,預計將使該地區的硝酸鹽生產成本降低5-7%,並提高對中國電力限制的供應韌性。加拿大在硝酸鹽市場中的地位仍然較為特殊,主要集中在為硬岩礦山提供炸藥預分散劑,以及向安大略省和魁北克省的製藥廠銷售試劑。

歐洲市場雖然出口量不大,但卻是一個高價值市場,因為買家需要符合EN標準和REACH(化學品註冊、評估、授權和限制)規定的試劑和凝聚劑。對硝酸鹽和磷的更嚴格監管正將需求從農業轉向都市污水處理,即使化肥出口量保持平穩,也能支撐利潤。南美洲是以色列和挪威生產商成長最快的出口市場,這得益於巴西一家特種肥料廠將交貨時間縮短了一個月。中東和非洲的出口量落後於其他地區,但在石化產品以及南非金礦和煤礦酸性礦山廢水處理方面仍有成長空間。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對特種肥料和水溶性肥料的需求不斷成長

- 催化劑原料在精細化工領域的應用日益廣泛。

- 採礦炸藥和雷管的使用量增加

- 相變材料在熱能儲存方面的新應用

- 3D列印混凝土外加劑簡介

- 市場限制因素

- 硝酸鹽排放的健康和環境審查

- 易揮發鎂礦石和滷水供應鏈定價

- 在施肥和灌溉中用硝酸鈣/硝酸銨混合物替代其他肥料

- 價值鏈分析

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按年級

- 肥料等級

- 工業級

- 試劑級

- 其他等級(醫藥等級、電子/超高純度等級)

- 透過主要功能

- 增溶劑

- 脫水劑

- 氧化劑

- 催化劑/加速器

- 透過使用

- 肥料和葉面噴布

- 化學合成與催化劑

- 炸藥和推進劑

- 用水和污水處理

- 混凝土和建築添加劑

- 其他用途(熱能儲存、藥品和營養補充劑等)

- 按最終用戶行業分類

- 農業

- 化工/石油化工

- 採礦和冶金

- 建築/施工

- 水/污水管理

- 其他終端用戶產業(醫療保健/生命科學、紡織等)

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- American Elements

- Avantor Inc.

- GFS Chemicals Inc.

- Haifa Negev Technologies LTD

- Merck KGaA

- Noah Chemicals

- Sure Chemical Co., Ltd. Shijiazhuang

- Spectrum Chemical

- Thermo Fisher Scientific Inc.

- Valudor Products, LLC

- Yara

第7章 市場機會與未來展望

第8章:執行長面臨的主要策略挑戰:

The Magnesium Nitrate Hexahydrate Market size is expected to increase from USD 0.84 billion in 2025 to USD 0.88 billion in 2026 and reach USD 1.08 billion by 2031, growing at a CAGR of 4.27% over 2026-2031.

Demand growth pivots on two reinforcing factors. First, greenhouse and drip-irrigated farms are replacing calcium-ammonium nitrate with water-soluble magnesium nitrate to correct simultaneous nitrogen and magnesium deficiencies without raising soil pH, a shift that directly lifts fertilizer-grade volumes. Second, industrial users value the compound's hygroscopicity in nitric-acid concentration, its oxidizing balance in mining explosives, and its latent-heat profile in phase-change thermal storage, which together create a recurring, diversified pull that moderates cyclical swings in the agriculture cycle. Competitive intensity remains moderate because quality specifications differ sharply between fertilizer, industrial, and reagent grades, creating natural customer lock-in and room for specialty producers to price for purity. Upstream magnesium price volatility injects margin risk, yet the supply chain is slowly regionalizing as projects in Arkansas and Brazil move closer to first metal, a development that should smooth raw-material shocks for downstream formulators by the late forecast period.

Global Magnesium Nitrate Hexahydrate Market Trends and Insights

Rising Demand for Specialty and Water-Soluble Fertilizers

Precision fertigation systems allow growers to meter nutrients in line with evapotranspiration, and magnesium nitrate delivers 16% nitrogen with 9.4% magnesium in a form that stays neutral in solution. Field trials in 2026 found that 0.5% seed priming lifted maize germination by 12% under drought stress, underscoring its resilience benefit. A 6,000-ton plant opened in Brazil in 2025, enabling regional distributors to supply soluble grades with a two-week lead time instead of six, removing a historic logistics hurdle for coffee and citrus growers. Foliar studies in 2025 showed that 2% sprays boosted sweet-corn ear weight by 9% and cut blossom-end rot by 22%, proving the compound's role in protecting marketable yield. Demand lifts in a stepwise fashion as farms install drip systems, meaning the driver's full effect lands over a medium horizon.

Growing Adoption as Catalytic Feedstock in Fine Chemicals

Magnesium nitrate converts to high-surface-area magnesium oxide on calcination, an attribute prized for Lewis-acid catalysis. A 2025 study achieved 94% ketone-to-alcohol conversion at 120°C using oxide derived from the salt, beating palladium on cost per mole converted. Petrochemical licensors specify 2N-5N grades as supports in reforming and cracking catalysts because decomposition releases no sulfur that would poison active metals. Dehydrating qualities make it an alternative to sulfuric acid for pushing nitric acid to 95 wt%, a purity demanded in explosives and certain active pharmaceutical ingredients. Validation cycles in pharmaceuticals run four to six years, placing growth in the long-term bucket.

Health and Environmental Scrutiny of Nitrate Discharge

The United States caps nitrate-nitrogen in drinking water at 10 mg/L, and the European Union limits groundwater nitrate to 50 mg/L, rules that force growers in vulnerable zones to trim soluble nitrate inputs or add cover crops. Municipal plants considering magnesium-nitrate coagulants must show that residual nitrate stays inside discharge permits that now often include dual phosphorus and nitrate ceilings, complicating business cases. An Environmental Protection Agency (EPA) paper in 2024 linked farm runoff to the Gulf of Mexico hypoxic zone, fast-tracking state mandates for controlled-release fertilizers that depress immediate demand. Because regulators already enforce these limits, the restraint bites in the short term.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Use in Mining Explosives and Detonators

- Emerging Use in Thermal-Energy-Storage Phase-Change Materials

- Volatile Magnesium Ore and Brine Supply Pricing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fertilizer Grade captured 51.28% of the magnesium nitrate hexahydrate market share in 2025 and is projected to expand at a 5.03% CAGR as protected-agriculture acreage grows and soluble blends displace bulk dolomitic lime. Industrial Grade posted slower growth because demand in nitric-acid concentration, detonators, and petrochemical catalysts is mature, yet its multi-year contracts buffer revenue during fertilizer downturns. Reagent Grade, manufactured at 98-99.5% purity, serves analytical laboratories and pharmaceutical synthesis niches where batch traceability commands premiums of 50-80% over commodity grades.

The magnesium nitrate hexahydrate market size for Reagent Grade is forecast to grow substantially as pharmaceutical validation cycles clear and demand for water-quality testing kits expands. Fertilizer Grade pricing remains tethered to global nitrogen benchmarks, but freight savings from the new Brazilian plant could widen delivered-cost spreads by 8-10%, defending margins despite volatile upstream magnesium prices. Suppliers that can swing output between grades stand to arbitrage transient price spikes, yet most facilities are purpose-built, reinforcing moderate market concentration.

Dehydrating-agent use held 35.22% of revenue in 2025 and will grow at 4.78% CAGR because pharmaceutical and explosives producers rely on up-to-95% nitric acid that the salt delivers without sulfate contamination. Oxidizing-agent volumes track mining explosives research programs, many of which sit in advanced pilots, so near-term growth is slower but could inflect if regulatory shifts keep tightening pure ammonium nitrate.

The magnesium nitrate hexahydrate market size for Solubilizing Agent roles in fertigation is set to touch a higher value, mirroring drip-irrigation acreage expansion. Catalytic-promoter demand, though under 10% of volume, is projected to post the highest margin growth as oxide nanoclusters emerge as low-cost supports in transfer-hydrogenation routes for fine chemicals. Function splits underscore a classic dual-engine profile: large agricultural tonnage plus small, high-value chemical niches.

The Magnesium Nitrate Hexahydrate Market Report is Segmented by Grade (Fertilizer Grade, and More), Primary Function (Solubilizing Agent, and More), Application (Fertilizers and Foliar Sprays, Chemical Synthesis and Catalysts, and More), End-User Industry (Agriculture, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led the magnesium nitrate hexahydrate market in 2025 with 25.12% revenue and is positioned for the fastest 4.96% CAGR through 2031. China's upstream dominance in primary magnesium secures captive feedstock for domestic nitrate producers, keeping ex-works prices 12-18% lower than imports in most months. India's government subsidies for micro-irrigation under the Pradhan Mantri Krishi Sinchayee Yojana are catalyzing fertigation adoption among tomato and capsicum growers, accelerating soluble-grade demand. Japan and South Korea, while small in tonnage, buy high-purity reagent grades, supporting premium unit margins.

North America ranks second in revenue, split between the United States' industrial and laboratory consumption and Mexico's protected-agriculture boom. The December 2025 Defense Production Act award to build a brine-to-metal plant in Arkansas could shave 5-7% off regional nitrate production costs once operational, improving supply resilience against Chinese power curtailments. Canada's role remains niche, focused on explosives predispersions for hard-rock mines and reagent sales to pharmaceutical plants in Ontario and Quebec.

Europe posts moderate tonnage but commands high value because buyers seek reagent and coagulant grades certified to EN and REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) standards. Stricter nitrate and phosphorus directives are rotating demand from agriculture into municipal water treatment, cushioning revenue even as fertilizer tonnage flattens. South America is the fastest-expanding export destination for Israeli and Norwegian producers, following the Brazilian specialty-fertilizer plant that cut delivery lead times by a month. The Middle East and Africa lag in volume yet show upside in petrochemicals and acid-mine-drainage remediation in South African gold and coal fields.

- American Elements

- Avantor Inc.

- GFS Chemicals Inc.

- Haifa Negev Technologies LTD

- Merck KGaA

- Noah Chemicals

- Sure Chemical Co., Ltd. Shijiazhuang

- Spectrum Chemical

- Thermo Fisher Scientific Inc.

- Valudor Products, LLC

- Yara

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for specialty and water-soluble fertilizers

- 4.2.2 Growing adoption as catalytic feedstock in fine-chemicals

- 4.2.3 Increasing use in mining explosives and detonators

- 4.2.4 Emerging use in thermal-energy-storage phase-change materials

- 4.2.5 Deployment in 3-D-printed concrete admixtures

- 4.3 Market Restraints

- 4.3.1 Health and environmental scrutiny of nitrate discharge

- 4.3.2 Volatile magnesium ore and brine supply chain pricing

- 4.3.3 Substitution by calcium-/ammonium-nitrate blends in fertigation

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Grade

- 5.1.1 Fertilizer Grade

- 5.1.2 Industrial Grade

- 5.1.3 Reagent Grade

- 5.1.4 Other Grades (Pharmaceutical Grade, Electronic/Ultra-high-purity Grade)

- 5.2 By Primary Function

- 5.2.1 Solubilizing Agent

- 5.2.2 Dehydrating Agent

- 5.2.3 Oxidizing Agent

- 5.2.4 Catalyzing/Promoter Agent

- 5.3 By Application

- 5.3.1 Fertilizers and Foliar Sprays

- 5.3.2 Chemical Synthesis and Catalysts

- 5.3.3 Explosives and Propellants

- 5.3.4 Water and Waste-water Treatment

- 5.3.5 Concrete and Construction Additives

- 5.3.6 Other Applications (Thermal Energy Storage (TES), Pharmaceuticals and Nutraceuticals, etc.)

- 5.4 By End-user Industry

- 5.4.1 Agriculture

- 5.4.2 Chemical and Petrochemical

- 5.4.3 Mining and Metallurgy

- 5.4.4 Building and Construction

- 5.4.5 Water and Waste-water Management

- 5.4.6 Other End-user Industries (Healthcare and Life-Sciences, Textile, etc.)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 American Elements

- 6.4.2 Avantor Inc.

- 6.4.3 GFS Chemicals Inc.

- 6.4.4 Haifa Negev Technologies LTD

- 6.4.5 Merck KGaA

- 6.4.6 Noah Chemicals

- 6.4.7 Sure Chemical Co., Ltd. Shijiazhuang

- 6.4.8 Spectrum Chemical

- 6.4.9 Thermo Fisher Scientific Inc.

- 6.4.10 Valudor Products, LLC

- 6.4.11 Yara

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment