|

市場調查報告書

商品編碼

2043958

無水氟化氫:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Anhydrous Hydrogen Fluoride - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

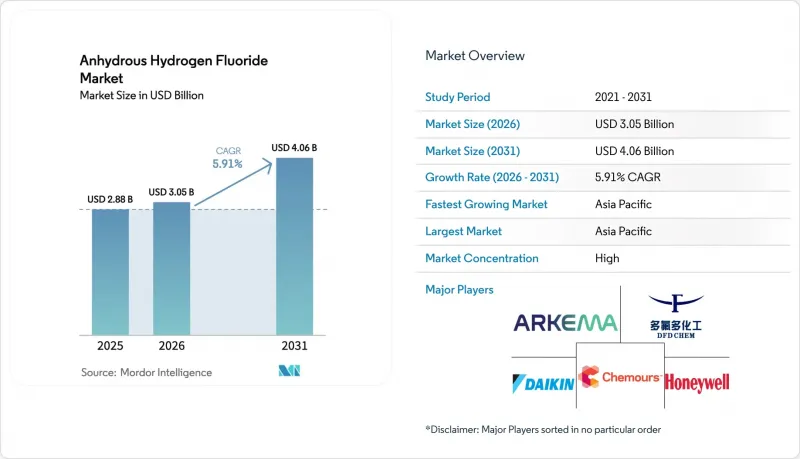

無水氟化氫的市場規模預計將從 2025 年的 28.8 億美元成長到 2026 年的 30.5 億美元,到 2031 年將達到 40.6 億美元,2026 年至 2031 年的複合年成長率為 5.91%。

半導體製造業持續回流美國,北美和歐洲各地建設超級工廠,以及亞太地區從螢石到氟化學品的一體化生態系統,即使傳統消費模式因冷媒的逐步減少而發生重組,也支撐著穩定的需求。未來五年,無水氟化氫市場預計將迎來成長,成長動力來自5奈米以下邏輯節點所需的超高純度等級、磷酸鹽肥料產品中氟化氫的封閉回路型回收,以及用於電動車電池和5G基礎設施的特殊氟聚合物。供應穩定性正成為關鍵的競爭因素,因為全球63%的螢石礦產和超過70%的氟化氫產能仍集中在中國,這使得在墨西哥和印度進行後向整合營運具有戰略吸引力。同時,煉油商收緊汽油含硫量標準,以及石化生產商擴大氟化氫甲醇烷基化製程在丁烯丙烯混合原料中的應用,都在支撐技術級氟化氫的需求,儘管這些需求受到更嚴格的安全和監管控制。

全球無水氟化氫市場趨勢及洞察

半導體產能的擴張將提振對超高純度氟化氫的需求。

根據《晶片與科學法案》,國內製造業激勵措施已促使亞利桑那州、德克薩斯州和俄亥俄州的晶圓製造設施投資超過1,500億美元,但津貼均未提及12N氟化氫的穩定供應。 12N氟化氫是唯一能夠揮發氧化矽而不留下金屬殘留物的蝕刻劑。韓國已授予東洋工程韓國公司一份EPC契約,計劃於2025年建成一座年產5萬噸的氟化氫(HF)工廠。此舉旨在實現供應商多元化,並在2019年出口管制爭端後減少對日本採購的依賴。 Stella Chemifa公司在日本和新加坡已運作年產10.5萬噸的高純度氟化氫產能,該公司正在北美增設生產線,以便將生產基地設在計劃建設的晶圓廠附近,這反映了縮短敏感化學品供應鏈的更廣泛趨勢。 2026 年,半導體產業協會要求美國貿易代表辦公室 (USTR) 在全球範圍內統一純度標準,以便合約價格能夠透明地反映達到亞 ppt 級雜質閾值的成本。

氟聚合物在電動車電池和5G基礎設施的應用前景廣闊

聚二氟亞乙烯(PVDF) 的產量預計將會增加,這主要是由於其被用作鋰離子電池的黏合劑和隔膜,而鋰離子電池需要消耗由氟化氫 (HF) 衍生的偏二氟乙烯單體。阿科瑪公司正在投資 2000 萬美元,計劃在 2026 年年中將其位於肯塔基州卡爾弗特市的 PVDF 產量提高 15%,旨在提高美國電池樹脂的自給率。儘管歐盟和美國的監管機構正在加快對全氟烷基和多氟烷基物質 (PFAS) 的審查,並敦促生產商改用水性 PVDF 分散體(這種分散體可以在不影響性能的前提下減少 90% 的揮發性有機化合物 (VOC)),但由於《基加利修正案》實施後,R142b 原料供應緊張,PV DF 的供不應求嚴重。

螢石供應鏈集中度與價格波動

2026年初的地緣政治緊張局勢導致霍爾木茲海峽航運量下降超過90%,推高布蘭特原油價格至每桶88.87美元,中國聚四氟乙烯現貨價格較上季上漲12%。作為回應,浙江巨化和山東東岳於2026年3月將聚四氟乙烯價格上調15%至16%,這是自2024年以來最大的漲幅。這種情況凸顯了供應鏈簡化如何加速了上游成本飆升並傳導至整個氟產業鏈。

細分市場分析

2025年,純度為99.9 wt%或更高的技術級AHF佔冷媒、本體氟聚合物和甲醇烷基化催化劑總需求的57.12%。然而,純度為99.999 wt%或更高的電子級AHF預計將以6.47%的複合年成長率成長,這主要得益於3nm和2nm半導體節點的需求,在這些節點上,兆分之一級別的金屬污染會顯著降低晶圓良率。雖然兩極化的價格結構使得電子級AHF生產商能夠獲得比普通AHF供應商高出兩倍以上的利潤率,但隨著浙江宏化等中國大型企業開始運作高純度AHF模組,這種溢價差距可能會從2028年開始縮小。

由於晶圓廠傾向將化學品供應基地設在附近以降低運輸風險,無水氟化氫市場正從中受益。目前正在考慮的一個北美計畫預計到2030年每年可新增6萬噸電子級氟化氫。然而,複雜的授權程序和當地社區的嚴格審查正在延長前置作業時間,從而提升了擁有靈活品管系統的現有供應商的價值。

區域分析

到2025年,亞太地區將佔全球無水氟化氫市場規模的60.45%,預計到2031年將以6.22%的複合年成長率成長。中國仍然是核心參與者,佔全球螢石產量的63%,並擁有HF、LiPF6和PVDF的全套生產線。浙江巨化玉門矽氟化物聯合裝置計畫於2026年運作,預計年收入將達數百億元人民幣,進一步提高國內自給率。韓國蔚山的建設、日本對12N純度產品的重視,以及印度Navin Fluorine和古吉拉突邦 Fluorochemicals的擴張,都反映出在2019年日韓出口摩擦之後,亞太地區正轉向重視產能韌性。

在北美,隨著半導體製造廠、電池廠和PVDF擴建項目的運作,市場佔有率預計將會上升。奧爾比亞位於馬塔莫羅斯的工廠幾乎將其每年17.1萬噸的產量全部出口到美國,並且透過使用其位於聖路易斯波托西的自有礦石,避免了北美買家因亞洲運輸延誤而遭受損失。阿科瑪在肯塔基州擴建PVDF生產線以及西恩科在喬治亞的工廠,凸顯了氟化化學中間體本地化的戰略轉變,而這些中間體依賴氫氟酸的供應。

在歐洲,隨著REACH法規下PFAS相關規定的推進,各國面臨最嚴峻的監管阻力。因此,生產商正將投資重點轉向水性分散體和閉迴路HF回收利用,而非新建通用HF生產線。同時,中東、非洲和南美洲仍然是具有重要戰略意義的地區,儘管規模較小。這些地區的煉油商傾向於使用HF甲醇烷基化製程生產富含液化石油氣(LPG)的原料,從而在其他地區環保人士的反對聲中維持了基本需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴大亞洲和美國的半導體產能

- 特種氟樹脂在電動車和5G電纜的應用日益廣泛

- 更嚴格的汽油硫含量標準正在推動對氫氟酸甲醇烷基化催化劑的需求。

- 政府戰略儲備與關鍵礦產政策

- 利用FSA和現場系統進行封閉回路型HF回收

- 市場限制因素

- 螢石供應鏈集中度及價格衝擊

- 對 PFAS 法規的持續審議正在遏制含氟化學品的擴張。

- 電子級精煉設備的高資本投入

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按實體形態和純度等級

- 技術級AHF(純度99.9wt%或更高)

- 高純度/電子級(99.999 wt% 或更高)

- 現場發電的混合解決方案

- 按最終用戶行業分類

- 含氟化學品和冷媒

- 半導體和電子學

- 礦物加工和金屬加工

- 石油甲醇烷基化催化劑

- 玻璃清洗和蝕刻

- 其他工業用途

- 按地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東和非洲

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Arkema

- Buss ChemTech AG

- Daikin Industries, Ltd.

- Do-Fluoride New Materials Co., Ltd.(DFD)

- Fluorsid

- Gujarat Fluorochemicals Ltd.(GFL)

- Honeywell International Inc.

- Jiangsu Meilan Chemical Co., Ltd.

- Merck KGaA

- Morita Chemical Industries Co., Ltd.

- Navin Fluorine International Ltd.

- Orbia Fluor & Energy Materials

- Solvay SA

- Stella Chemifa Corporation

- Taiwan Speciality Chemicals Corp

- Tanfac Industries Ltd.

- The Chemours Company

- Zhejiang Juhua Co., Ltd.

第7章 市場機會與未來展望

第8章:執行長面臨的主要策略挑戰:

The Anhydrous Hydrogen Fluoride Market size is expected to increase from USD 2.88 billion in 2025 to USD 3.05 billion in 2026 and reach USD 4.06 billion by 2031, growing at a CAGR of 5.91% over 2026-2031.

Sustained semiconductor reshoring in the United States, gigafactory build-outs across North America and Europe, and Asia-Pacific's integrated fluorspar-to-fluorochemical ecosystem are reinforcing steady demand even as refrigerant phase-downs reshape legacy consumption patterns. Over the next five years, the anhydrous hydrogen fluoride market will derive incremental volumes from ultra-high-purity grades required for sub-5 nm logic nodes, closed-loop HF recycling from phosphate fertilizer by-products, and specialty fluoropolymers used in electric-vehicle batteries and 5G infrastructure. Supply security is emerging as a decisive competitive factor because 63% of mined fluorspar and more than 70% of global HF capacity remain concentrated in China, amplifying the strategic appeal of backward-integrated operations in Mexico and India. At the same time, refiners upgrading gasoline sulfur specifications and petrochemical producers extending HF alkylation to mixed butylene, propylene feeds are sustaining technical-grade volumes, albeit under tighter safety and regulatory controls.

Global Anhydrous Hydrogen Fluoride Market Trends and Insights

Semiconductor Capacity Build-Out Amplifies Ultra-High-Purity Demand

Domestic-fabrication incentives under the CHIPS and Science Act have triggered more than USD 150 billion of announced wafer-fab spending across Arizona, Texas, and Ohio, yet none of the grants address the secure supply of 12N hydrofluoric acid, the only etchant that volatilizes silicon oxide without metallic residues. South Korea awarded Toyo Engineering Korea an EPC contract in 2025 for a 50,000 tonnes per year HF plant that will diversify sourcing away from Japanese vendors after the 2019 export-control dispute. Stella Chemifa, which already operates 105,000 tonnes of high-purity capacity across Japan and Singapore, is adding North-American production to co-locate near planned fabs, mirroring the broader move to shorten sensitive chemical supply lines. The Semiconductor Industry Association urged USTR in 2026 to harmonize purity standards globally so that contract pricing transparently reflects the cost of achieving sub-ppt impurity thresholds.

Fluoropolymer Expansion for EV Batteries and 5G Infrastructure

Polyvinylidene fluoride volumes are expected to rise, anchored in Li-ion battery binders and separators that consume HF-derived vinylidene fluoride monomer. Arkema allocated USD 20 million to lift PVDF output 15 % at Calvert City, Kentucky, by mid-2026, reinforcing US battery-grade resin self-reliance. Supply tightness is compounded because the Kigali Amendment is squeezing R142b feedstock availability even as the European Union and US regulators accelerate PFAS scrutiny, encouraging producers to shift toward waterborne PVDF dispersions that cut VOCs 90 % without sacrificing performance.

Fluorspar Supply-Chain Concentration and Price Volatility

Geopolitical friction in early 2026 curtailed Strait of Hormuz traffic by more than 90 %, pushing Brent to USD 88.87 per barrel and inflating Chinese HF spot offers by 12 % month-over-month; Zhejiang Juhua and Shandong Dongyue responded with 15-16 % PTFE price hikes in March 2026, the steepest surge since 2024. The episode underscores how single-channel dependence permits rapid pass-through of upstream cost spikes across the fluorine value chain.

Other drivers and restraints analyzed in the detailed report include:

- Alkylation Catalyst Demand Tied to Sulfur Specifications

- Strategic Stockpiling and Critical-Minerals Policies

- Pending PFAS Regulations Dampening Fluorochemical Expansion

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Technical Grade AHF, at more than or equal to 99.9 wt%, dominated 57.12% of 2025 demand across refrigerants, bulk fluoropolymers, and alkylation catalysts. Yet High-Purity Electronic Grade, specified at more than or equal to 99.999 wt%, is forecast to grow at 6.47% CAGR, propelled by the needs of 3 nm and 2 nm semiconductor nodes where single-digit-part-per-trillion metallic contamination can slash wafer yields. A bifurcated pricing structure lets electronic-grade producers command more than double the margin of commodity suppliers; however, Chinese leaders such as Zhejiang Juhua are commissioning deep-purification modules that could compress premium spreads after 2028.

The anhydrous hydrogen fluoride market benefits as fabs co-locate chemical supply to minimize transit risk; North American projects under evaluation could add 60,000 tons per year of electronic-grade HF by 2030. Even so, permitting complexity and local community scrutiny extends lead times, reinforcing the value of established suppliers with transferable quality-management systems.

The Anhydrous Hydrogen Fluoride Market Report is Segmented by Physical Form and Purity Grade (Technical Grade AHF, High-Purity/ Electronic Grade, and Blended On-Site Generation Solutions), End-User Industry (Fluorochemicals and Refrigerants, Semiconductors and Electronics, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific controlled 60.45% of the Anhydrous Hydrogen Fluoride market size in 2025 and is projected to expand at a 6.22 % CAGR to 2031. China remains the backbone, blending 63% of global fluorspar output with end-to-end HF, LiPF6, and PVDF lines; Zhejiang Juhua's Yumen silicon-fluoride complex, slated for 2026 start-up, will add tens of billions of CNY annual revenue and deepen domestic self-sufficiency. South Korea's Ulsan build, Japan's focus on 12N purity, and India's expansion through Navin Fluorine and Gujarat Fluorochemicals reflect a regional pivot toward capacity resilience after the 2019 Japan-Korea export tensions.

North America's share is poised to rise as semiconductor fabs, battery plants, and PVDF expansions come on-stream. Orbia's Matamoros unit exports nearly all of its 171,000 tons per year output to the United States, leveraging captive ore from San Luis Potosi to shield North-American buyers from Asian shipping delays. Arkema's Kentucky PVDF uplift and Syensqo's Georgia plant underscore a strategic shift toward localizing fluorochemical intermediates that hinge on HF availability.

Europe faces the stiffest regulatory headwinds as PFAS proposals advance under REACH. Producers are therefore investing in waterborne dispersions and closed-loop HF recycling rather than green-field commodity HF lines. Meanwhile the Middle East and Africa, along with South America, remain small yet strategically important because refiners there favor HF alkylation for LPG-rich feed slates, sustaining baseline demand despite environmental opposition elsewhere.

- Arkema

- Buss ChemTech AG

- Daikin Industries, Ltd.

- Do-Fluoride New Materials Co., Ltd. (DFD)

- Fluorsid

- Gujarat Fluorochemicals Ltd. (GFL)

- Honeywell International Inc.

- Jiangsu Meilan Chemical Co., Ltd.

- Merck KGaA

- Morita Chemical Industries Co., Ltd.

- Navin Fluorine International Ltd.

- Orbia Fluor & Energy Materials

- Solvay S.A.

- Stella Chemifa Corporation

- Taiwan Speciality Chemicals Corp

- Tanfac Industries Ltd.

- The Chemours Company

- Zhejiang Juhua Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Semiconductor capacity build-out in Asia and United States

- 4.2.2 Expansion of specialty fluoropolymers in Electric Vehicle and 5G cables

- 4.2.3 Stricter gasoline sulfur specs boosting HF alkylation catalysts

- 4.2.4 Government strategic stockpiling and critical-minerals policies

- 4.2.5 Closed-loop HF recycling from FSA and on-site systems

- 4.3 Market Restraints

- 4.3.1 Fluorspar supply-chain concentration and price shocks

- 4.3.2 Pending PFAS regulations dampening fluorochemical expansion

- 4.3.3 High capex for electronic-grade purification units

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Physical Form and Purity Grade

- 5.1.1 Technical Grade AHF (>=99.9 wt %)

- 5.1.2 High-Purity / Electronic Grade (>=99.999 wt %)

- 5.1.3 Blended On-site Generation Solutions

- 5.2 By End-user Industry

- 5.2.1 Fluorochemicals and Refrigerants

- 5.2.2 Semiconductors and Electronics

- 5.2.3 Mineral Processing and Metal Treatment

- 5.2.4 Petroleum Alkylation Catalysts

- 5.2.5 Glass Cleaning and Etching

- 5.2.6 Other Industrial Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 South Korea

- 5.3.1.4 India

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Arkema

- 6.4.2 Buss ChemTech AG

- 6.4.3 Daikin Industries, Ltd.

- 6.4.4 Do-Fluoride New Materials Co., Ltd. (DFD)

- 6.4.5 Fluorsid

- 6.4.6 Gujarat Fluorochemicals Ltd. (GFL)

- 6.4.7 Honeywell International Inc.

- 6.4.8 Jiangsu Meilan Chemical Co., Ltd.

- 6.4.9 Merck KGaA

- 6.4.10 Morita Chemical Industries Co., Ltd.

- 6.4.11 Navin Fluorine International Ltd.

- 6.4.12 Orbia Fluor & Energy Materials

- 6.4.13 Solvay S.A.

- 6.4.14 Stella Chemifa Corporation

- 6.4.15 Taiwan Speciality Chemicals Corp

- 6.4.16 Tanfac Industries Ltd.

- 6.4.17 The Chemours Company

- 6.4.18 Zhejiang Juhua Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

8 Key Strategic Questions for CEOs

無水氟化氫市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測2026-2034年全球無水氟化氫市場規模、佔有率、趨勢和成長分析報告

無水氟化氫市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測2026-2034年全球無水氟化氫市場規模、佔有率、趨勢和成長分析報告 無水氟化氫市場規模、佔有率和成長分析(按應用、最終用途、配方類型、分銷管道和地區分類)—產業預測(2026-2033 年)

無水氟化氫市場規模、佔有率和成長分析(按應用、最終用途、配方類型、分銷管道和地區分類)—產業預測(2026-2033 年) 無水氟化氫市場 - 全球產業規模、佔有率、趨勢、機會及預測(按應用領域(氟聚合物、氟酶、農藥及其他)、地區和競爭格局分類,2020-2030 年預測)

無水氟化氫市場 - 全球產業規模、佔有率、趨勢、機會及預測(按應用領域(氟聚合物、氟酶、農藥及其他)、地區和競爭格局分類,2020-2030 年預測) 無水氟化氫(AHF)-全球市佔率及排名、總收入及需求預測(2025-2031年)

無水氟化氫(AHF)-全球市佔率及排名、總收入及需求預測(2025-2031年) 全球無水氟化氫市場

全球無水氟化氫市場 無水氟化氫市場報告:趨勢、預測和競爭分析(至 2031 年)

無水氟化氫市場報告:趨勢、預測和競爭分析(至 2031 年) 無水氟化氫市場、規模、佔有率、趨勢、行業分析報告:按應用和地區 - 市場預測,2025-2034 年

無水氟化氫市場、規模、佔有率、趨勢、行業分析報告:按應用和地區 - 市場預測,2025-2034 年 無水氟化氫市場規模、佔有率、趨勢分析報告:按應用、地區、細分市場預測,2025-2030 年

無水氟化氫市場規模、佔有率、趨勢分析報告:按應用、地區、細分市場預測,2025-2030 年 無水氟化氫市場機會、成長動力、產業趨勢分析及2025年至2034年預測

無水氟化氫市場機會、成長動力、產業趨勢分析及2025年至2034年預測