|

市場調查報告書

商品編碼

2043907

泰國汽車租賃市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Thailand Car Rental - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

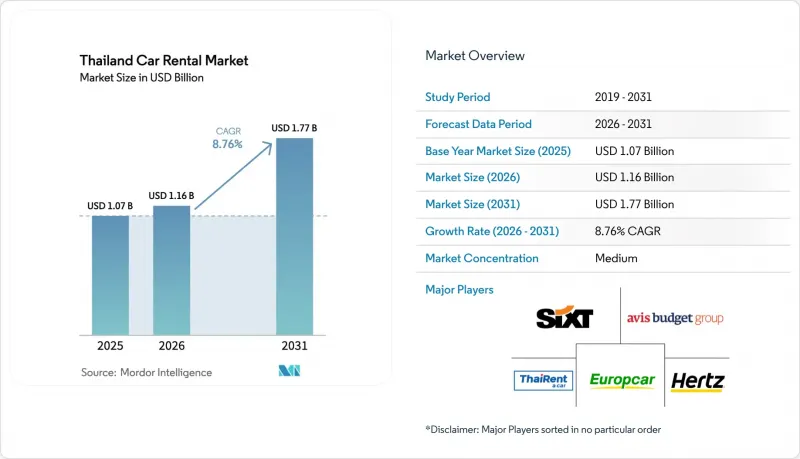

2025年泰國汽車租賃市場價值10.7億美元,預計到2031年將從2026年的11.6億美元成長到17.7億美元,預測期(2026-2031年)複合年成長率為8.76%。

對主要客戶市場持續的免簽政策、廉價航空公司快速進入區域機場以及車輛電氣化進程的加速,都推動了泰國汽車租賃市場的長期成長。然而,由於中國團體遊客數量銳減、車輛融資監管收緊以及車輛購置成本上升,該行業正面臨短期衝擊。因此,營運商正在調整其商業模式,更加重視國內遊客和長期企業契約,引入數位化預訂平台以滿足價格敏感型需求,並部署電池式電動車(BEV)以響應政府的永續發展激勵政策。此外,隨著P2P平台和叫車整合型汽車租賃服務的興起,傳統業者的利潤空間受到擠壓,迫使其投資於差異化服務模式,市場競爭也日益激烈。

泰國汽車租賃市場的趨勢與洞察

旅遊業復甦與簽證豁免制度

泰國於2025年推出的對中國、印度和俄羅斯的永久免簽政策,掃除了長期以來阻礙短期旅行者的障礙。預計到2025年,來自中國的自由行旅客數量將恢復到疫情前水準的75%以上,這將提振對不依賴巴士旅行團的多日租車需求。預計到2025年,來自印度和俄羅斯的遊客將達到約440萬人次,他們傾向於選擇多目的地自駕遊,遊覽海灘和文化景點。這種轉向即興、臨時預訂的趨勢,對於能夠提供車輛即時可用性資訊和靈活取車方式的營運商來說,無疑是一大利好。

數位預訂和價格比較平台的興起

預計到2025年,Drivemate和Houpcar等數位預訂應用程式,以及整合到Grab和Traveloka等超級應用程式中的聚合平台,將佔據泰國汽車租賃市場交易量的63.16%,並在2031年之前以9.28%的複合年成長率成長。雖然透明定價給利潤率帶來了壓力,但現有營運商正在整合應用程式介面(API),以便在多個入口網站上提供即時定價信息,從而顯著擴大其覆蓋範圍。營運商正透過送車上門、捆綁保險和會員計畫來凸顯自身差異化優勢,但精簡成本結構對於在與資產規模較小的數位平台競爭中保持競爭力至關重要。

車輛維修成本不斷上漲

2026年的消費稅改革將電池式電動車(BEV)的稅率降至2%,同時將大型內燃機汽車(ICE)的課稅提高至50%。這推高了傳統汽車的初始購買成本,迫使汽車租賃公司在資金限制和加速電氣化之間尋求平衡。半導體短缺導致交貨週期延長,延長了車輛的平均使用壽命,並增加了維護成本。 2025年12月推出的新的央行汽車租賃監理措施收緊了信貸標準,提高了中小企業的借貸成本。對於中型企業而言,如何在財務獎勵和流動性需求之間取得平衡變得至關重要。

細分市場分析

到2025年,線上預訂將佔泰國租車市場63.16%的佔有率,預計到2031年將以9.28%的複合年成長率成長,這主要得益於整合式搜尋引擎和P2P(點對點)列表服務的普及,這些服務能夠即時顯示數十家運營商的價格。應用程式整合了便利的電子錢包支付、一鍵保險和用戶評價功能,提高了用戶對透明度和便利性的期望。在主要機場,線下櫃檯仍然能夠吸引一些臨時到店的顧客,但隨著行動優先的旅客更傾向於使用智慧型手機進行即時預訂,其成長速度正在放緩。面對聚合平台的激烈價格競爭,營運商正努力透過實施動態定價和建立忠誠度夥伴關係來維持直接管道的流量。

Tyrang集團收購Drivemate並即時部署其純電動車(BEV)車隊,證實了其向精簡資產型供應鏈和數位搜尋策略轉型的正確性。超級應用正將其影響力擴展到食品配送和金融科技生態系統,透過交叉促銷將普通用戶轉化為租車客戶。老年旅客和首次到訪者在處理複雜的保險問題時仍然傾向於面對面服務,因此人工櫃檯仍將發揮重要作用。儘管如此,數位化共享的擴展似乎仍在持續,自助結帳亭和非接觸式車輛交付服務正在人流密集的場所普及。

2025年,受曼谷、普吉島和清邁機場休閒旅遊需求的推動,短期租賃將佔泰國汽車租賃市場佔有率的71.26%。日租金仍然是主要收入來源,但季節性波動使得現金流更容易受到影響。相較之下,長期租賃和包含維護及道路救援系統的月度訂閱預計到2031年將以9.41%的複合年成長率成長。跨國公司正在採用計量型的車隊模式,以對沖擁有成本並透過用電池式電動車(BEV)取代內燃機(ICE)汽車來滿足永續發展要求。

企業客戶優先考慮預算可預測性和覆蓋全國的服務網路,這迫使營運商提供車隊管理門戶,使其具備使用情況分析和集中計費功能。此外,遠距辦公人員也傾向於靈活使用車輛而非擁有車輛,這方面的需求日益成長。訂閱服務供應商透過將使用率低的公務車輛重新部署到週末休閒用車池,最佳化資產利用率並平衡季節性收入波動。對於傳統的日租業者而言,進入長期合約市場需要重組維護營運和信用風險評估架構。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 旅遊業復甦與簽證豁免制度

- 數位預訂和價格比較平台的興起

- 廉價航空公司正在向區域機場擴張

- 中國自駕遊的激增

- 政府計劃鼓勵購買電動車租賃車輛

- 基於區塊鏈的存款和損失追蹤系統

- 市場限制因素

- 車輛維修成本不斷上漲

- 來自叫車和超級應用的競爭

- 加強對車輛採購和消費貸款的監管

- 電動車租賃車輛充電基礎設施不足

- 價值/供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模及成長預測(價值(美元))

- 按預訂類型

- 線上

- 離線

- 租賃期

- 短期

- 長期

- 透過使用

- 休閒與旅遊

- 通勤/商務

- 按車輛類型

- 經濟型和迷你型

- 緊湊型和中型

- SUV/MPV

- 奢華與高階

- 透過推進力

- 內燃機(ICE)

- 混合動力電動車(HEV)

- 電池式電動車(BEV)

- 租賃頻道

- 飛機場

- 市中心/機場外

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- The Hertz Corporation

- Thai Rent A Car

- Chic Car Rent

- Enterprise Holdings

- Sixt SE

- Drive Car Rental

- QC Leasing(Thrifty)

- Siam Rent A Car

- Europcar Mobility Group

- Sunny Cars

- Bizcar Rental

- Avis Budget Group

- Budget Thailand

- National Car Rental

- Yesaway Car Rental

- ASAP Car Rental(KB Auto)

- Zuzuche

- Rent Connected

- EcoCar Rent

- ADA Car Rental

第7章 市場機會與未來展望

The Thailand car rental market size was valued at USD 1.07 billion in 2025 and is estimated to grow from USD 1.16 billion in 2026 to reach USD 1.77 billion by 2031, at a CAGR of 8.76% during the forecast period (2026-2031).

Sustained visa-free entry for major source markets, rapid expansion of low-cost carriers into secondary airports, and accelerated fleet electrification together underpin the long-run growth profile of the Thailand car rental market. At the same time, the sector faces near-term turbulence from a sharp fall in Chinese group tourism, tightening fleet-financing rules, and rising vehicle acquisition costs. Operators are therefore rebalancing toward domestic travelers and long-term corporate subscriptions, deploying digital booking platforms to capture price-sensitive demand, and adding battery electric vehicles (BEVs) to meet government sustainability incentives. Competitive intensity is rising as peer-to-peer platforms and ride-hailing-linked rental schemes squeeze traditional operators' margins and force them to invest in differentiated service models.

Thailand Car Rental Market Trends and Insights

Tourism Rebound & Visa-Free Schemes

Thailand's permanent visa-waiver for China, India, and Russia, introduced in 2025, removed a long-standing friction that deterred short-stay travelers. Chinese independent visitors recovered to over 75% of pre-pandemic levels in 2025, boosting multi-day car-hire demand beyond coach-based itineraries. Indian and Russian tourists accounted for around 4.4 million arrivals in 2025 and gravitated toward multi-destination road trips across beach and cultural circuits. The shift toward spontaneous, last-minute digital reservations rewards operators with real-time fleet visibility and flexible pick-up options.

Rise of Digital Booking & Price-Comparison Platforms

Digital booking apps such as Drivemate and Houpcar, along with aggregators embedded in super-apps like Grab and Traveloka, captured 63.16% of the Thailand car rental market transactions in 2025 and are growing at a 9.28% CAGR through 2031. Transparent price discovery pressures margins but vastly enlarges reach, prompting incumbents to integrate application programming interfaces (APIs) that feed real-time rates to multiple portals. Operators differentiate via doorstep delivery, bundled insurance, and loyalty perks, yet must streamline cost structures to remain competitive against asset-light digital platforms.

Rising Fleet Acquisition & Maintenance Costs

The 2026 excise-tax overhaul slashed BEV rates to 2% while lifting taxes on large ICE engines to 50%, inflating upfront prices for conventional cars and forcing rental firms to weigh accelerated electrification against capital constraints. Semiconductor shortages extend delivery lead times, prolonging fleet age and raising maintenance bills. New central-bank supervision of auto leasing since December 2025 has tightened credit standards, lifting borrowing costs for smaller operators. Balancing fiscal incentives with liquidity needs becomes critical for mid-tier companies.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Low-Cost Carriers to Secondary Airports

- Surge in Chinese Self-Drive Tourism

- Competition from Ride-Hailing and Super-Apps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Online reservations accounted for 63.16% of the Thailand car rental market size in 2025 and are projected to grow at a 9.28% CAGR through 2031, driven by metasearch engines and peer-to-peer listings that expose live prices across dozens of operators. Apps embed seamless e-wallet payments, one-click insurance, and user ratings, raising expectations for transparency and convenience. Offline desks still capture last-minute walk-ins at major airports, but their growth lags as mobile-first travelers favor the immediacy of smartphone bookings. Operators experiment with dynamic pricing and loyalty partnerships to retain direct-channel traffic amid aggressive aggregator discounting.

Thairung Group's acquisition of Drivemate and the immediate infusion of a BEV fleet validated the strategic pivot toward asset-light supply and digital discovery. Super-apps extend reach into food delivery and fintech ecosystems, converting everyday users into rental customers through cross-promotion. Elderly travelers and first-time visitors still value face-to-face service for complex insurance questions, sustaining a residual role for staffed counters. Nonetheless, digital share gains appear durable, underpinning automated check-out kiosks and contactless vehicle handovers in high-volume locations.

Short-term hires accounted for 71.26% of Thailand's car rental market share in 2025, driven by leisure-centric traffic at Bangkok, Phuket, and Chiang Mai airports. Daily rates remain the yield driver, yet seasonal volatility exposes cash flow to swings. In contrast, long-term rentals and monthly subscriptions bundled with maintenance and roadside support are set to grow at a 9.41% CAGR through 2031. Multinationals adopt pay-as-you-use fleets to hedge against ownership costs and align with sustainability mandates by swapping ICE units for BEVs.

Corporate accounts prize predictable budgeting and nationwide service coverage, pushing operators to offer fleet portals with usage analytics and centralized billing. Demand also stems from remote-work professionals choosing flexible car access over ownership. Subscription providers optimize asset utilization by redeploying idle corporate cars into weekend leisure pools, smoothing revenue seasonality. For traditional daily-rental players, entering long-term contracts requires re-engineering maintenance operations and credit-risk assessment frameworks.

The Thailand Car Rental Market Report is Segmented by Booking Type (Online and Offline), Rental Duration (Short-Term and Long-Term), Application (Leisure/Tourism and Commuting/Business), Vehicle Class (Economy and Mini, and More), Propulsion (Internal Combustion Engine and More), and Rental Channel (Airport and Downtown/Off-airport). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- The Hertz Corporation

- Thai Rent A Car

- Chic Car Rent

- Enterprise Holdings

- Sixt SE

- Drive Car Rental

- Q.C. Leasing (Thrifty)

- Siam Rent A Car

- Europcar Mobility Group

- Sunny Cars

- Bizcar Rental

- Avis Budget Group

- Budget Thailand

- National Car Rental

- Yesaway Car Rental

- ASAP Car Rental (K.B. Auto)

- Zuzuche

- Rent Connected

- EcoCar Rent

- ADA Car Rental

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tourism Rebound & Visa-Free Schemes

- 4.2.2 Rise of Digital Booking & Price-Comparison Platforms

- 4.2.3 Expansion of Low-Cost Carriers to Secondary Airports

- 4.2.4 Surge in Chinese Self-Drive Tourism

- 4.2.5 Government EV-Rental Purchase Incentive Programme

- 4.2.6 Blockchain-Based Deposit & Damage-Tracking Systems

- 4.3 Market Restraints

- 4.3.1 Rising Fleet Acquisition & Maintenance Costs

- 4.3.2 Competition From Ride-Hailing & Super-Apps

- 4.3.3 Stricter Fleet-Financing & Consumer-Loan Rules

- 4.3.4 Sparse Charging Infrastructure for EV Rentals

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Booking Type

- 5.1.1 Online

- 5.1.2 Offline

- 5.2 By Rental Duration

- 5.2.1 Short-term

- 5.2.2 Long-term

- 5.3 By Application

- 5.3.1 Leisure / Tourism

- 5.3.2 Commuting / Business

- 5.4 By Vehicle Class

- 5.4.1 Economy & Mini

- 5.4.2 Compact & Mid-size

- 5.4.3 SUV & MPV

- 5.4.4 Luxury & Premium

- 5.5 By Propulsion

- 5.5.1 Internal-Combustion Engine (ICE)

- 5.5.2 Hybrid Electric Vehicle (HEV)

- 5.5.3 Battery Electric Vehicle (BEV)

- 5.6 By Rental Channel

- 5.6.1 Airport

- 5.6.2 Downtown / Off-airport

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 The Hertz Corporation

- 6.4.2 Thai Rent A Car

- 6.4.3 Chic Car Rent

- 6.4.4 Enterprise Holdings

- 6.4.5 Sixt SE

- 6.4.6 Drive Car Rental

- 6.4.7 Q.C. Leasing (Thrifty)

- 6.4.8 Siam Rent A Car

- 6.4.9 Europcar Mobility Group

- 6.4.10 Sunny Cars

- 6.4.11 Bizcar Rental

- 6.4.12 Avis Budget Group

- 6.4.13 Budget Thailand

- 6.4.14 National Car Rental

- 6.4.15 Yesaway Car Rental

- 6.4.16 ASAP Car Rental (K.B. Auto)

- 6.4.17 Zuzuche

- 6.4.18 Rent Connected

- 6.4.19 EcoCar Rent

- 6.4.20 ADA Car Rental

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

汽車麥克風市場規模、佔有率和成長分析:按麥克風類型、應用、連接方式、車輛類型和地區分類-2026-2033年產業預測

汽車麥克風市場規模、佔有率和成長分析:按麥克風類型、應用、連接方式、車輛類型和地區分類-2026-2033年產業預測 租車市場機會、成長要素、產業趨勢分析及2026-2035年預測。

租車市場機會、成長要素、產業趨勢分析及2026-2035年預測。 租車市場:2026年至2032年全球市場預測(依租賃期限、燃料類型、服務功能、用戶層、車輛類型及預訂方式分類)汽車租賃市場:2026-2032年全球市場預測(依租賃期限、驅動方式、車輛等級、車輛類型、銷售管道及客戶類型分類)

租車市場:2026年至2032年全球市場預測(依租賃期限、燃料類型、服務功能、用戶層、車輛類型及預訂方式分類)汽車租賃市場:2026-2032年全球市場預測(依租賃期限、驅動方式、車輛等級、車輛類型、銷售管道及客戶類型分類) 2026年全球自駕汽車租賃市場報告2026年全球乘用車租賃市場報告2026年全球汽車租賃市場報告

2026年全球自駕汽車租賃市場報告2026年全球乘用車租賃市場報告2026年全球汽車租賃市場報告 2026-2034年全球汽車麥克風市場規模、佔有率、趨勢和成長分析報告租車及租賃市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測租車及租賃市場:2026年至2032年全球預測(依車輛類型、型號、租賃時長、動力系統、應用領域、最終用戶及預訂模式分類)

2026-2034年全球汽車麥克風市場規模、佔有率、趨勢和成長分析報告租車及租賃市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測租車及租賃市場:2026年至2032年全球預測(依車輛類型、型號、租賃時長、動力系統、應用領域、最終用戶及預訂模式分類)