|

市場調查報告書

商品編碼

2043892

塔式起重機:市佔率分析、產業趨勢與統計、成長預測(2026-2031)Tower Cranes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

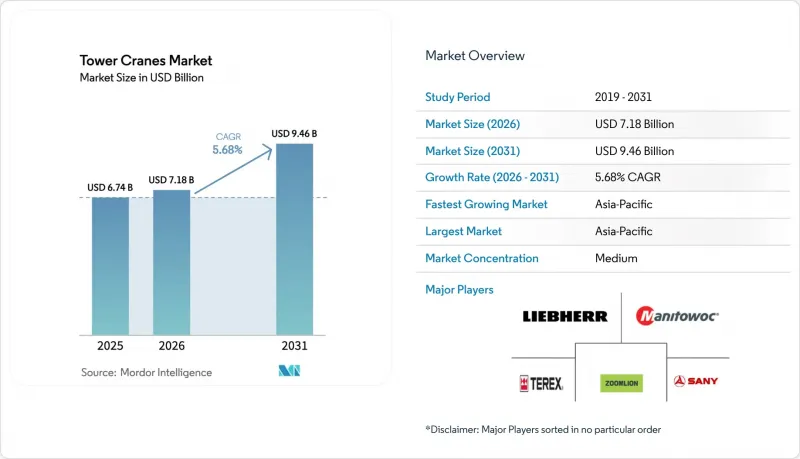

2025年塔式起重機市值為67.4億美元,預計到2031年將達到94.6億美元,高於2026年的71.8億美元,預測期(2026-2031年)複合年成長率為5.68%。

亞太地區城市軌道交通網路的蓬勃發展、沿岸地區雄心勃勃的大型計畫以及歐盟日益嚴格的零排放法規構成了短期需求的基礎。然而,需求結構正在改變。隨著中國高層建築竣工速度放緩,停工項目增加,國內起重機被迫尋求海外市場。租賃市場的滲透、數位雙胞胎技術的應用以及電氣化進程正在以傳統所有權模式無法適應的速度重塑採購趨勢。競爭優勢越來越依賴部署預測性維護軟體、電池混合動力裝置以及能夠適應模組化施工進度的中型起重機的能力。

全球塔式起重機市場趨勢與洞察

快速的都市化和摩天大樓的蓬勃發展

根據高樓與居住環境委員會(CTBUH)的數據,到2025年,全球將建造2,583棟高度超過200公尺的建築,其中2025年將新增141棟。中國佔這些竣工項目的65%,但有259個項目處於停滯狀態,這反映出開工率與實際起重機運轉率之間存在差距。平均竣工週期已延長至5.8年,導致租賃期延長,並促使市場向擁有完善維護網路的公司傾斜。高層建築建設活動正向沿岸地區轉移,其中重啟的1000米高的吉達塔和725米高的阿齊茲塔是多年期項目的標誌性建築。像沃爾夫克蘭這樣的原始設備製造商(OEM)已在利雅德和杜拜設立服務基地,因此能夠很好地掌握這項轉變帶來的機會。相較之下,過度依賴國內高層建築建築週期的中國品牌,如今在海外正面臨運轉率下降的困境。

亞洲和海灣合作理事會的基礎設施獎勵策略

中國的「一帶一路」計劃在2024年獲得了價值707億美元的建築契約,其中中東地區以390億美元的契約額超過非洲,成為最大的訂單地區。印度的地鐵網路已投入運作945公里,另有939公里正在興建中,其高速公路網路平均每天建設34公里。沙烏地阿拉伯的「2030願景」計劃,以NEOM和The Line為核心,如果得以實現,可能需要約2萬台塔式起重機。雖然這些規模龐大、相互交織的基礎設施項目保證了未來幾年的需求,但從資金籌措延誤到勞動力短缺等實施風險正在拖累最終的數字。

鋼鐵價格和供應鏈波動

根據美國勞工統計局的數據,2024年12月至2025年3月期間,起重機零件的生產者物價指數上漲了10%。計劃於2026年生效的232條款關稅延期將對移動式起重機的進口鋼材零件徵收約50%的關稅,這引發了人們對塔式起重機成本壓力可能進一步加劇的擔憂。同時,歐洲製造商面臨的電力成本是美國平均水平的數倍,即使是電動起重機的利潤率也受到擠壓。中國整機製造商正轉向在沙烏地阿拉伯和阿拉伯聯合大公國進行本地組裝以規避關稅,但這種地域分散增加了庫存持有成本,並使零件物流更加複雜。

細分市場分析

2025年,平頂式塔式起重機的銷售量佔比達46.37%。其無領桅杆結構允許多台起重機的吊臂相互重疊而不相互干擾,這在人口密集、高層建築林立的地區是一項顯著優勢。獨立式塔式起重機市場預計將以7.52%的複合年成長率成長,其成長速度將超過其他所有類型,這主要得益於歐洲和北美住宅建築商採用一日安裝方式,從而無需外部組裝起重機。

像馬尼托瓦克的Potan Hup 40-30(4噸,30米臂長)這樣的自立式起重機,將從安裝到吊裝的時間從幾天縮短到幾小時,從而降低了人事費用和道路封閉許可費用。同時,三一重工的STT3330平頭起重機起重能力達到3300噸米,吊鉤高度達到330米,顯示起重機的起重能力持續提升。動臂臂起重機適用於機場周邊嚴格空域限制區域的作業。同時,建築內吊機在摩天大樓這一細分市場仍然至關重要,但其訂單目前主要集中在海灣國家的項目中。

到2025年,額定起重能力為6至10噸的起重機將佔塔式起重機總銷量的37.25%,佔塔式起重機市場最大佔有率。由於預製外牆和模組化艙的吊裝作業很少超過此重量範圍,預計其複合年成長率將達到6.88%。 11至16噸級塔式起重機市場也受惠於模組化趨勢,但由於獲得重型起重作業許可證所需的前置作業時間較長,其成長速度較為緩慢。

利勃海爾550 EC-B 12 Fiber(12噸,70米臂長)在中端機型中實現了最佳平衡,其4噸的吊臂末端載荷;而沃爾夫克蘭7534.16型起重機可在不增加安裝面積的情況下處理高達16噸的重物。超過25噸後,運作將變得斷斷續續,且需依具體項目而定。三一重工STT2400(2400噸米)僅在大型專案和構成城市天際線的重型工業起重作業中才具有經濟效益。在低階機型方面,5噸以下的自組合式起重機在歐洲聯排別墅維修計畫中日益普及,但在亞洲仍屬於少數。這是因為亞洲地區由於對工人友好的法規和較高的施工密度,仍然更傾向於使用大型共用起重機。

區域分析

亞太地區對起重機的需求最為旺盛,主要得益於中國涵蓋55個城市、總長10,287公里的地鐵網路,以及印度雙軌鐵路和地鐵建設的蓬勃發展。然而,中國的起重機供應過剩導致2024年租金下降了20%,迫使企業將設備重新分配到菲律賓、越南和海灣國家的專案中。儘管高層建築的竣工速度有所放緩,但建築活動仍在繼續,導致建設活動的表面繁榮與塔式起重機的實際運作時間之間存在差距。中東地區正在消化這一過剩需求,其中沙烏地阿拉伯的「2030願景」走廊和阿拉伯聯合大公國杜拜不斷擴張的天際線推動了這一趨勢。 Wolfklan在利雅德成立的新合資企業已提交了90份競標,這反映了該地區卓越的服務網路。但執行風險依然存在。吉達塔樓計畫在停工數年後於2024年才重新開工,凸顯了工期的不確定性。

監管對歐洲前景構成重大挑戰。歐盟機械法規2023/1230和建築產品法規2024/3110對進口商實施了數位通行證和全生命週期義務,預計合規成本將降低8-12%。德國、法國和英國是需求的主要驅動力,但歐盟建築市場預計在2024年將萎縮2.1%,這將抑制市場前景。儘管建設產業整體低迷,但北海離岸風力發電的基礎工程支撐了對專用塔式起重機和橫樑起重機的需求。在北美,鋼鐵關稅使移動式起重機的成本增加了高達45%,間接促使建築商在多年期高層建築專案中轉向塔式起重機。設備租賃收入創歷史新高,但由於企業不再傾向於擁有起重機,因此擁有的起重機數量有所下降。 《基礎設施投資和就業法案》的資金正在緩解住宅市場的放緩,橋樑和鐵路項目也持續推進。

南美洲的成長取決於巴西「成長加速計畫」的重啟,該計畫旨在2026年建造200萬套住宅,以及聖保羅多條地鐵線的擴建計畫。然而,由於外匯波動和熟練勞動力供應不穩定,前景仍然不明朗。非洲仍在發展中,南非和奈及利亞的採礦計畫以及一些高層建築計畫是主要的亮點。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 快速的都市化和摩天大樓的蓬勃發展

- 亞洲和海灣合作理事會的基礎設施獎勵策略

- 向承包商租賃模式過渡

- 引入數位雙胞胎、物聯網和遠端控制

- 零排放場所強制電氣化

- 安全和自動化技術的進步

- 市場限制因素

- 鋼鐵價格和供應鏈波動

- 熟練操作人員短缺和勞動力老化

- 遵守歐盟和美國職業安全與健康管理局 (OSHA) 安全標準的相關成本增加

- 在中高層建築工地與高容量移動式起重機競爭

- 價值/供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模和成長預測(價值和數量)

- 起重機類型

- 錘頭起重機

- 平頭起重機

- 筏式懸臂起重機

- 自組合式起重機

- 爬升式塔吊

- 負載能力

- 5噸或以下

- 6-10噸

- 11-16噸

- 17-25噸

- 超過25噸

- 有意為之

- 頂部旋轉型

- 底部旋轉型

- 透過使用

- 住宅建築

- 商業建築

- 基礎設施項目

- 採礦和鑽探

- 工業項目

- 海洋/近海

- 最終用戶

- 建設公司

- 租賃公司

- 工業企業

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 土耳其

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Liebherr Group

- Zoomlion Heavy Industry Science&Technology Co., Ltd.

- XCMG Group

- SANY Group

- The Manitowoc Company, Inc.

- Terex Corporation

- Wolffkran International

- Comansa

- JASO Tower Cranes

- Raimondi Cranes

- Action Construction Equipment

- Sarens nv

- Maxim Crane Works

- Favelle Favco Berhad

- Fushun Yongmao

- FM Gru

- Saez Cranes

- Wilbert Tower Cranes

- Bigge Crane & Rigging

- NFT Group

第7章 市場機會與未來展望

The tower cranes market size was valued at USD 6.74 billion in 2025 and is estimated to grow from USD 7.18 billion in 2026 to reach USD 9.46 billion by 2031, at a CAGR of 5.68% during the forecast period (2026-2031).

Robust urban rail build-outs in the Asia-Pacific, ambitious giga-projects across the Gulf, and tightening EU zero-emission rules anchor near-term demand. Yet the volume picture is shifting: Chinese super-tall completions slowed while stalled projects climbed, pushing domestic fleets to seek work abroad. Rental penetration, digital-twin deployment, and electrification mandates are now shaping procurement faster than traditional ownership models can adapt. Competitive advantage increasingly rests on predictive-maintenance software, battery-hybrid power units, and the ability to mobilize mid-capacity cranes for modular construction schedules.

Global Tower Cranes Market Trends and Insights

Rapid Urbanization and Super-Tall Construction Boom

The Council on Tall Buildings and Urban Habitat tallied 2,583 buildings above 200 m completed globally by 2025, with 141 new additions that year. China accounted for 65% of these completions, yet 259 other projects stalled, exposing a decoupling of groundbreaks from actual crane utilization. Average completion times stretched to 5.8 years, lengthening rental tenures and shifting value toward firms with deep maintenance networks. High-rise activity is migrating to the Gulf, where the resumed 1,000 m Jeddah Tower and 725 m Burj Azizi anchor multiyear pipelines. OEMs with established Riyadh or Dubai service hubs, such as Wolffkran, are positioned to capture this pivot. In contrast, Chinese brands that over-indexed on domestic tall-building cycles face utilisation gaps abroad.

Infrastructure Stimulus Programs in Asia and GCC

China's Belt and Road Initiative booked USD 70.7 billion of construction contracts in 2024, with the Middle East replacing Africa as the top recipient at USD 39 billion. India's metro footprint reached 945 km in service, with another 939 km underway, while its highway program averages 34 km of construction per day. Saudi Arabia's Vision 2030 slate, led by NEOM and The Line, could need roughly 20,000 tower cranes if plans materialize. Large, overlapping infrastructure schemes lock in multiyear demand, although execution risks, ranging from funding delays to labor shortages, temper the headline numbers.

Steel Price and Supply-Chain Volatility

U.S. Bureau of Labor Statistics data show the crane-parts producer-price index jumping 10% between December 2024 and March 2025. Section 232 tariff extensions set to take effect in 2026 will apply a roughly 50% tax on the steel content of imported mobile cranes, raising concerns about cascading cost pressure on tower units. European fabricators, meanwhile, face electricity costs several multiples of U.S. averages, squeezing margins even on electric-drive models. Chinese OEMs respond by localizing assembly in Saudi Arabia and the UAE to dodge tariffs, but geographic dispersion increases inventory carrying costs and parts logistics complexity.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Rental Model Among Contractors

- Digital-Twin, IoT, and Remote Operation Adoption

- Stricter EU/OSHA Safety Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flat-top designs delivered 46.37% of 2025 revenue. Their collar-free mast segments allow multiple units to overlap jibs without interference, a key benefit in dense high-rise clusters. The tower crane market for self-erecting models is projected to grow at a 7.52% CAGR, outpacing all other types as European and North American residential contractors adopt single-day set-ups that bypass external erection cranes.

Self-erectors such as Manitowoc's Potain Hup 40-30 (4 t, 30 m jib) compress start-to-lift timelines from days to hours, saving labor and street-closure permits. Meanwhile, SANY's STT3330 flat-top reaches 3,300 t-m and 330 m hook height, underscoring that capacity ceilings continue to rise. Luffing-jib units defend tight air rights corridors near airports. At the same time, climbable in-building cranes remain indispensable for the mega-tall niche, though their order flow now centres on Gulf state projects.

Cranes rated 6-10 ton captured 37.25% of revenue in 2025, the most significant slice of the tower cranes market. Prefabricated facade and modular pod lifts rarely exceed this window, explaining a 6.88% forecast CAGR. The tower crane market size for the 11-16 ton bracket also benefits from modular trends, but grows more slowly as heavier picks require more extended permit lead times.

Liebherr's 550 EC-B 12 Fiber (12 t, 70 m jib) hits the mid-range sweet spot with four-ton tip loads, while Wolffkran's 7534.16 pushes to 16 t without enlarging the ground footprint. Above 25 t, utilization turns episodic and project-specific-SANY's STT2400 (2,400 t-m) only pays off on skyline-defining cores or industrial heavy-lift jobs. At the low end, sub-5 t self-erectors are growing in Europe's townhouse renovations but remain marginal in Asia, where labor-friendly regulations and higher site densities still favor larger, shared units.

The Tower Cranes Market Report is Segmented by Crane Type (Hammerhead and More), Lifting Capacity (Up To 5 Ton and More), Design (Top-Slewing and Bottom-Slewing), Application (Residential Buildings and More), End User (Construction Companies, Rental Companies, and More), and Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Both Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific shoulders the highest crane volumes due to China's 10,287 km operational metro grid across 55 cities and India's twin-track rail and metro boom. Yet oversupply in China drove a 20% erosion in rental rates in 2024, compelling fleets to redeploy into the Philippines, Vietnam, and Gulf projects. Super-tall completions slowed even as starts linger, decoupling headline construction activity from actual tower-crane hours. The Middle East soaks up excess capacity, with Saudi Arabia's Vision 2030 corridor and the UAE's ever-expanding Dubai skyline setting the pace. Wolffkran's new Riyadh joint venture has already bid for 90 units, reflecting the region's service network premium. Execution risk remains: Jeddah Tower only resumed in 2024 after a multiyear pause, underscoring schedule volatility.

Europe's outlook is regulatory-heavy. The EU Machinery Regulation 2023/1230 and Construction Products Regulation 2024/3110 layer digital passport and life-cycle duties on importers, reducing compliance spend by 8-12%. Germany, France, and the UK concentrate demand, but EU construction contracted 2.1% in 2024, tempering prospects. Offshore wind foundations in the North Sea support specialized tower and luffer demand despite broader building weakness. North America wrestles with steel tariffs that inflate mobile-crane costs by up to 45%, indirectly nudging contractors toward tower models for multi-year high-rise jobs. Equipment-rental revenues hit record highs, yet fleet counts slipped as firms de-emphasized ownership. Infrastructure Investment and Jobs Act funds cushion any residential slowdown, keeping bridge and rail projects in the queue.

South America's growth hinges on Brazil's revived Growth Acceleration Program, targeting 2 million housing units by 2026, and on multi-line Sao Paulo metro extensions. However, currency swings and uneven skill availability blur the outlook. Africa remains nascent, with mining shafts and select skyline projects in South Africa and Nigeria the main bright spots.

- Liebherr Group

- Zoomlion Heavy Industry Science&Technology Co., Ltd.

- XCMG Group

- SANY Group

- The Manitowoc Company, Inc.

- Terex Corporation

- Wolffkran International

- Comansa

- JASO Tower Cranes

- Raimondi Cranes

- Action Construction Equipment

- Sarens n.v.

- Maxim Crane Works

- Favelle Favco Berhad

- Fushun Yongmao

- FM Gru

- Saez Cranes

- Wilbert Tower Cranes

- Bigge Crane & Rigging

- NFT Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Urbanization and Super-Tall Construction Boom

- 4.2.2 Infrastructure Stimulus Programmes In Asia and GCC

- 4.2.3 Shift To Rental Model Among Contractors

- 4.2.4 Digital-Twin, IoT and Remote-Operation Adoption

- 4.2.5 Electrification Mandates For Zero-Emission Sites

- 4.2.6 Advancements In Safety And Automation Technologies

- 4.3 Market Restraints

- 4.3.1 Steel Price and Supply-Chain Volatility

- 4.3.2 Skilled Operator Shortage and Ageing Workforce

- 4.3.3 Stricter EU/OSHA Safety Compliance Costs

- 4.3.4 Competition From High-Capacity Mobile Cranes In Mid-Rise Jobs

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Crane Type

- 5.1.1 Hammerhead Cranes

- 5.1.2 Flat-Top Cranes

- 5.1.3 Luffing Jib Cranes

- 5.1.4 Self-Erecting Cranes

- 5.1.5 Climbable Tower Cranes

- 5.2 By Lifting Capacity

- 5.2.1 Up to 5 ton

- 5.2.2 6-10 ton

- 5.2.3 11-16 ton

- 5.2.4 17-25 ton

- 5.2.5 Above 25 ton

- 5.3 By Design

- 5.3.1 Top-Slewing

- 5.3.2 Bottom-Slewing

- 5.4 By Application

- 5.4.1 Residential Buildings

- 5.4.2 Commercial Buildings

- 5.4.3 Infrastructure Projects

- 5.4.4 Mining and Excavation

- 5.4.5 Industrial Projects

- 5.4.6 Marine/Offshore

- 5.5 By End User

- 5.5.1 Construction Companies

- 5.5.2 Rental Companies

- 5.5.3 Industrial Operators

- 5.5.4 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Turkey

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Liebherr Group

- 6.4.2 Zoomlion Heavy Industry Science&Technology Co., Ltd.

- 6.4.3 XCMG Group

- 6.4.4 SANY Group

- 6.4.5 The Manitowoc Company, Inc.

- 6.4.6 Terex Corporation

- 6.4.7 Wolffkran International

- 6.4.8 Comansa

- 6.4.9 JASO Tower Cranes

- 6.4.10 Raimondi Cranes

- 6.4.11 Action Construction Equipment

- 6.4.12 Sarens n.v.

- 6.4.13 Maxim Crane Works

- 6.4.14 Favelle Favco Berhad

- 6.4.15 Fushun Yongmao

- 6.4.16 FM Gru

- 6.4.17 Saez Cranes

- 6.4.18 Wilbert Tower Cranes

- 6.4.19 Bigge Crane & Rigging

- 6.4.20 NFT Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

塔式起重機市場:按類型、結構、起重機能力、最終用戶和地區分類

塔式起重機市場:按類型、結構、起重機能力、最終用戶和地區分類 塔式起重機市場規模、佔有率、趨勢和預測:按類型、起重能力、最終用途行業和地區分類,2026-2034年

塔式起重機市場規模、佔有率、趨勢和預測:按類型、起重能力、最終用途行業和地區分類,2026-2034年 塔式起重機市場規模、佔有率和趨勢分析報告:按產品、設計、起重能力、應用、地區和細分市場預測(2026-2033 年)

塔式起重機市場規模、佔有率和趨勢分析報告:按產品、設計、起重能力、應用、地區和細分市場預測(2026-2033 年) 全球塔式起重機市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球塔式起重機市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球塔式起重機市場報告

2026年全球塔式起重機市場報告 塔式起重機市場規模、佔有率和成長分析(按類型、應用、設計和地區分類)—2026-2033年產業預測

塔式起重機市場規模、佔有率和成長分析(按類型、應用、設計和地區分類)—2026-2033年產業預測 塔式起重機租賃市場規模、佔有率及成長分析(按類型、最終用戶和地區分類)-2026-2033年產業預測塔式起重機市場-2025-2030年預測

塔式起重機租賃市場規模、佔有率及成長分析(按類型、最終用戶和地區分類)-2026-2033年產業預測塔式起重機市場-2025-2030年預測 塔式起重機市場-全球產業規模、佔有率、趨勢、機會及預測(依產品、設計、起重能力、最終用戶、地區及競爭情況,2020-2030 年)

塔式起重機市場-全球產業規模、佔有率、趨勢、機會及預測(依產品、設計、起重能力、最終用戶、地區及競爭情況,2020-2030 年) 塔式起重機租賃市場:全球按容量、產品類型、最終用途產業和地區分類 - 預測至 2030 年

塔式起重機租賃市場:全球按容量、產品類型、最終用途產業和地區分類 - 預測至 2030 年