|

市場調查報告書

商品編碼

2043887

疊層匯流排:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Laminated Busbar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

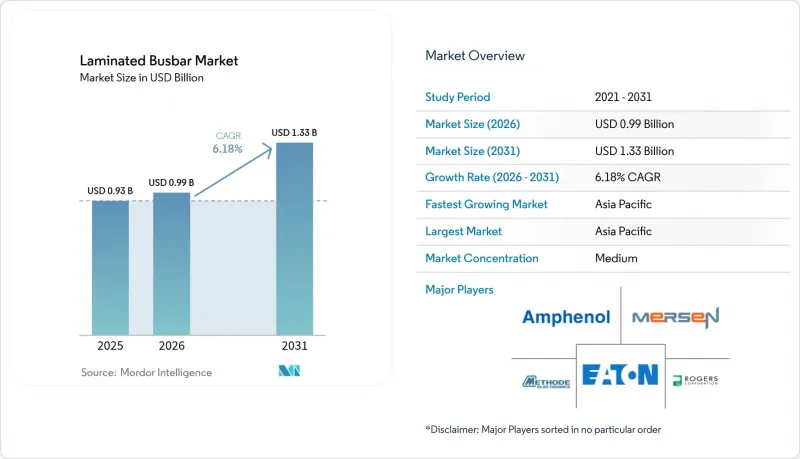

預計到 2026 年,層壓匯流排市場價值將達到 9.8747 億美元,高於 2025 年的 9.3 億美元,預計到 2031 年將達到 13.3 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 6.18%。

這一成長主要由電動交通設備、可再生能源逆變器以及高密度資料中心的電源背板推動,這些應用都需要低電感、高熱效率的緊湊型配電組件。雖然銅仍然是性能關鍵型系統中的主要導體,但鋁和混合金屬組合在對重量敏感的應用中日益受到關注。穩定的原料供應和寬能隙功率模組的不斷進步,推動了新的設計需求,即優先採用層壓結構而非傳統的條形和線束結構。銅價波動帶來的價格壓力,部分被製造效率的提高以及終端用戶越來越願意為更高的安全性和節省空間的功能支付更高的價格所抵消。

全球層壓匯流排市場趨勢與洞察

電動車和混合動力車的普及推動了緊湊型電源解決方案的發展。

汽車製造商正在加速採用疊層匯流排,以縮小電池組面積並提升熱性能。特斯拉的結構電池和比亞迪的刀片式電池已經證明,疊層導體可以在保持高電流密度的同時,將組裝複雜性降低40%。 [1] 冷包覆鋁銅混合材料兼具輕量化和高導電性,而超音波焊接和銀塗層則解決了鋁氧化的問題。隨著汽車平臺向400V-800V系統過渡,需要能夠適應不斷變化的電池化學成分且不影響安全裕度的靈活匯流排形狀。因此,隨著供應商數量的增加以及材料專家和一級整合商之間為爭取長期供應合約而展開的競爭,疊層匯流排市場正在煥發活力。

可再生能源逆變器的日益普及將加速電網併網。

太陽能和風能原始設備製造商 (OEM) 正在為低電感、大電流逆變器等級指定多層匯流排。碳化矽 (SiC) 和氮化鎵 (GaN) 開關目前的工作頻率遠高於 50 kHz,其多層結構可將雜散電感降低高達 90%,從而提高轉換效率,並支援與儲能系統結合的資產中的雙向功率流動。 [2] 標準化介面簡化了儲能模組的更換,內建感測器可實現預測性維護,防止大型電站逆變器停機,並進一步擴大多層匯流排市場。

銅和鋁價格波動

2024年7月,銅價達到每磅6.20美元,由於原物料成本佔總成本的70%之多,零件供應商將表提高了45%。多年期逆變器和電網合約限制了成本轉嫁的能力,進一步壓縮了利潤空間。隨著混合動力系統市場佔有率的成長,鋁價波動加劇了不不確定性。一些原始設備製造商(OEM)正透過長期供應合約來規避風險,或考慮採用銅包鋁導體,這種導體可以在不影響導電性的前提下降低風險。

細分市場分析

到2025年,銅將佔據疊層匯流排市場71.05%的佔有率,這得益於其無與倫比的導電性和成熟的加工工藝。高功率逆變器和電池組對電阻損耗和溫升的容忍度極低,這推動了銅的市場主導地位。然而,由於汽車製造商可以透過犧牲密度來減輕重量,並將原料成本降低40%,鋁製品市場預計將以7.85%的複合年成長率成長。 Samuel Taylor等公司生產的冷覆雙金屬帶能夠實現無縫的鋁銅連接,從而保持電流通路和機械完整性。因此,規範設計工程師擴大核准在800V驅動逆變器和充電模組中使用混合材料,重新定義了材料清單標準。

鋁材的採用迫使絕緣實驗室重新考慮介質層厚度,以適應熔點較低的導體;而鍍銀和鍍鎳製程則延長了接頭表面的使用壽命。最佳化重量的軌道設計降低了長續航電動車電池組的重量,從而增加了千瓦時容量或負載容量。面向疊層匯流排產業的供應商正在投資超音波焊接生產線和自動化品管,以確保大規模批量生產中包覆層的完整性始終如一。

環氧粉末塗料兼具強大的機械保護性能和低廉的單件成本,預計到2025年將佔銷售額的37.45%,成為開關設備和FA櫃的首選塗料。然而,聚酯和聚醯亞胺薄膜正以7.55%的複合年成長率迅速普及,因為它們更薄的層壓結構可以降低電感並改善導熱路徑。特種薄膜能夠承受SiC牽引模組中常見的快速溫度波動,即使在結溫超過175 度C的情況下也能正常工作而不開裂。

這種薄膜層壓技術能夠製造厚度小於2毫米的匯流排,這些匯流條以蜿蜒曲折的方式排列在電池組的狹窄腔體內。耐熱纖維增強材料和陶瓷填料提高了介電擊穿電壓,同時保持了材料的柔軟性。環境、健康與安全 (EHS) 團隊也指出,這種新型無溶劑薄膜黏合劑減少了生產過程中揮發性有機化合物 (VOC) 的排放,有助於企業在不犧牲產品壽命的前提下實現其永續發展目標。

《疊層匯流排市場報告》依導電材料(銅、鋁、混合材料)、絕緣材料(環氧粉末塗層、聚酯等)、匯流排配置(多層、高層、軟性/薄型匯流排)、額定電壓(低壓等)、應用(可再生能源等)、最終用戶(電力公司、運輸設備製造商等地區(北美地區細分)和地區(北美地區細分)和地區(北美地區細分。

區域分析

預計到2025年,亞太地區將引領疊片匯流排市場,佔40.95%的市佔率。該地區預計將以7.2%的複合年成長率成長,這主要得益於中國、日本和韓國垂直整合的供應鏈,這些供應鏈縮短了前置作業時間並降低了成本。該地區疊片匯流排市場受益於擁有多年合約的大規模電動車生產線,而這些生產線的建設又受到電池組產量成長的推動。此外,印度可再生能源逆變器的快速普及也進一步提升了該地區對疊片母線產能的需求。

北美則位居第二,這主要得益於超大規模資料中心的維修和雄心勃勃的汽車電氣化計畫。光是特斯拉的結構電池專案就推動了對客製化導體佈局的需求激增,而雲端園區向48V機架的轉換也確保了預設計背板套件的穩定訂單。聯邦政府鼓勵關鍵零件製造在地化的獎勵正在促進美國對層壓板的投資。

在歐洲,嚴格的環境指令和工業自動化推動了相關技術的穩定應用。風電設備製造商在海上換流站中採用匯流排與碳化矽功率模組相結合的方案,而德國工具機製造商則透過採用層壓基板維修工廠配電盤,以減少機櫃面積。區域供應商則透過採購低碳銅和推行「從生產到處置」的回收計畫來實現差異化競爭,從而與歐盟的永續性目標保持一致。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電動車和混合動力車的普及

- 可再生能源逆變器安裝現狀

- 對資料中心電源背板的需求正在激增。

- 工業電氣化和自動化快速發展

- 採用基於SiC/GaN的高壓模組

- 模組化電動垂直起降飛行器電池組架構

- 市場限制因素

- 銅鋁價格波動

- 低成本的傳統匯流排作為替代方案

- 電壓超過 1 kV 時出現散熱和分層現象

- 制定航太標準/文件的負擔

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 透過導電材料

- 銅

- 鋁

- 混合(銅鋁複合材料)

- 按類型分類的隔熱材料

- 環氧粉末塗料

- 聚偏氟乙烯薄膜

- 聚酯纖維

- 耐熱纖維

- 聚醯亞胺/聚亞醯胺膜

- 其他

- 匯流排配置

- 多層(3-5層)

- 高層建築(超過5層)

- 軟性/超薄匯流排

- 按額定電壓

- 低電壓(低於1千伏特)

- 中壓(1-35千伏特)

- 高壓(35千伏或更高)

- 透過使用

- 電動車和混合動力汽車

- 可再生能源(太陽能、風能、儲能系統)

- 資料中心和雲端基礎設施

- 工業驅動裝置與機械

- 鐵路和公共交通

- 航太和電動垂直起降飛行器

- 最終用戶

- 電力公司

- 工業OEM

- 運輸設備製造商

- 住宅/商業建築

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 東南亞國協

- 亞太其他地區

- 南美洲

- 阿根廷

- 巴西

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略性舉措(併購、合作、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Eaton Corporation plc

- Rogers Corporation

- Mersen SA

- Methode Electronics Inc.

- Amphenol Corporation

- Molex LLC

- Sun.King Power Electronics Group Ltd

- Zhuzhou CRRC Times Electric Co., Ltd

- Storm Power Components

- Segue Electronics Inc.

- EMS Industrial & Service Company

- Ryoden Kasei Co., Ltd

- Shanghai Eagtop Electronic Technology Co., Ltd

- Suzhou West Deane Machinery Inc.

- Raychem RPG Private Limited

- Zhejiang RHI Electric Co., Ltd

- Electronic Systems Packaging LLC

- Idealec SAS

- Advanced Energy Industries, Inc.

- Delta Electronics, Inc.

- Siemens AG

- ABB Ltd

- Schneider Electric SE

- Littelfuse Inc.

第7章 市場機會與未來展望

Laminated Busbar market size in 2026 is estimated at USD 987.47 million, growing from 2025 value of USD 0.93 billion with 2031 projections showing USD 1.33 billion, growing at 6.18% CAGR over 2026-2031.

Momentum comes from electrified transportation, renewable energy inverters, and high-density data center power backplanes, all of which demand compact power distribution assemblies with low inductance and high thermal efficiency. Copper remains the baseline conductor for performance-critical systems, while aluminum and hybrid metal combinations build traction in weight-sensitive applications. Supply security for raw materials and continuing advances in wide-bandgap power modules underpin new design requirements that favor laminated architectures over conventional bar or cable harnesses. Pricing pressure from volatile copper costs is partially offset by manufacturing productivity gains and the growing willingness of end users to pay a premium for enhanced safety and space savings.

Global Laminated Busbar Market Trends and Insights

EV & HEV Proliferation Drives Compact Power Solutions

Automakers are accelerating the adoption of laminated busbars to reduce battery-pack footprints and improve thermal performance. Tesla's structural battery and BYD's blade format demonstrate how laminated conductors reduce assembly complexity by 40% while maintaining high current density.[1] Aluminum-copper hybrids produced via cold-cladding now combine weight savings with conductivity, and ultrasonic welding, along with silver coatings, resolve aluminum oxidation hurdles. Vehicle platforms shifting to 400 V-800 V systems require flexible busbar geometries that accommodate changing cell chemistries without compromising safety margins. The cascading effect is a broadened supply base, with materials specialists and tier-one integrators vying for long-term supply awards, boosting the laminated busbar market.

Renewable-Energy Inverter Roll-outs Expand Grid Integration

Solar and wind OEMs specify laminated busbars for low-inductance, high-current inverter stages. SiC and GaN switches now operate well past 50 kHz, and laminated geometries cut stray inductance by up to 90%, improving conversion efficiency and enabling bidirectional power flow in storage-combined assets.[2] Standardized interfaces simplify the swapping of energy-storage modules, while embedded sensors enable predictive maintenance that prevents inverter downtime in utility-scale parks, further expanding the laminated busbar market.

Volatile Copper & Aluminum Prices

Copper reached USD 6.20 per pound in July 2024, prompting component suppliers to increase their price lists by up to 45%, as raw materials account for up to 70% of the cost. Multi-year inverter or grid contracts limit pass-through ability, eroding margins. Aluminum swings add another layer of uncertainty just as hybrids gain share. Some OEMs hedge their bets with long-term supply agreements or explore copper-clad aluminum conductors that reduce exposure without compromising conductivity.

Other drivers and restraints analyzed in the detailed report include:

- Data-Center Power-Backplane Demand Spike

- Industrial Electrification & Automation Surge

- Heat-Dissipation & Delamination Beyond 1 kV

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Copper captured 71.05% of the laminated busbars market share in 2025, driven by its unmatched conductivity and mature processing routes. This dominance is anchored by high-power inverters and battery packs that cannot compromise on resistive losses or heat rise. However, aluminum sections are expected to accelerate at an 7.85% CAGR as vehicle OEMs trade density for weight savings and achieve a 40% reduction in raw-material costs. Cold-clad bimetal strip from Samuel Taylor and similar suppliers enables jointless aluminum-copper interfaces that maintain current paths and mechanical integrity. As a result, specification engineers increasingly approve hybrids for 800 V traction inverters and charging modules, reshaping bill-of-materials norms.

Aluminum adoption forces insulation labs to rethink dielectric thickness for lower melting-point conductors, while silver-flash or nickel-plate coatings extend mating-surface life. Weight-optimized rail designs trim pack mass in long-range EVs, unlocking extra kilowatt-hours or payload. Suppliers targeting the laminated busbars industry invest in ultrasonic welding lines and automated quality control to guarantee consistent clad integrity across large production batches.

Epoxy powder coating accounted for 37.45% of the revenue in 2025 by combining robust mechanical protection with low per-part costs, making it the default choice for switchgear and factory automation cabinets. Yet polyester and polyimide films are gaining traction at a 7.55% CAGR because thinner stacks translate to lower inductance and better thermal pathways. Specialty films withstand the rapid temperature swings commonly seen in SiC traction modules, supporting junction temperatures exceeding 175°C without cracking.

Film laminates enable busbars under 2 mm thick that snake through cramped battery-pack cavities. Heat-resistant fiber reinforcements and ceramic fillers raise breakdown voltage while maintaining flexibility. Environmental, health, and safety teams also note that newer solvent-free film adhesives lower volatile organic compound emissions in production, advancing corporate sustainability targets without sacrificing product lifespan.

The Laminated Busbar Market Report is Segmented by Conducting Material (Copper, Aluminum, and Hybrid), Insulation Material (Epoxy Powder Coating, Polyester, and More), Busbar Configuration (Multi-Layer, High-Layer, and Flex/Thin Busbars), Voltage Rating (Low Voltage, and More), Application (Renewable Energy, and More), End-User (Power Utilities, Transportation OEMs, and More), and Geography (North America, Asia-Pacific, and More).

Geography Analysis

The Asia-Pacific region dominated the laminated busbars market in 2025, with a 40.95% share, and is expected to expand at a 7.2% CAGR as vertically integrated supply chains in China, Japan, and South Korea compress lead times and reduce costs. The laminated busbars market size in the region benefits from large-volume EV production lines that secure multiyear busbar contracts tied to battery-pack ramps. India accelerates renewable-energy inverter deployment, adding further pull for regional lamination capacity.

North America ranked second, driven by hyperscale data-center retrofits and ambitious automotive electrification timelines. Tesla's structural battery programs alone create recurring demand spikes for custom conductor layouts, while 48V rack conversions in cloud campuses secure steady orders for pre-engineered backplane kits. Federal incentives to localize critical-component manufacturing add momentum to US-based lamination investments.

Europe relies on stringent environmental directives and industry automation to maintain steady adoption. Wind-energy OEMs rely on busbars that pair with SiC power modules in offshore converter stations, whereas German machine-tool makers retrofit factory panels with laminated boards to shrink cabinet footprints. Regional suppliers differentiate through low-carbon copper sourcing and cradle-to-grave recycling programs, resonating with EU sustainability goals.

- Eaton Corporation plc

- Rogers Corporation

- Mersen SA

- Methode Electronics Inc.

- Amphenol Corporation

- Molex LLC

- Sun.King Power Electronics Group Ltd

- Zhuzhou CRRC Times Electric Co., Ltd

- Storm Power Components

- Segue Electronics Inc.

- EMS Industrial & Service Company

- Ryoden Kasei Co., Ltd

- Shanghai Eagtop Electronic Technology Co., Ltd

- Suzhou West Deane Machinery Inc.

- Raychem RPG Private Limited

- Zhejiang RHI Electric Co., Ltd

- Electronic Systems Packaging LLC

- Idealec SAS

- Advanced Energy Industries, Inc.

- Delta Electronics, Inc.

- Siemens AG

- ABB Ltd

- Schneider Electric SE

- Littelfuse Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV & HEV proliferation

- 4.2.2 Renewable energy inverter roll-outs

- 4.2.3 Data-center power-backplane demand spike

- 4.2.4 Industrial electrification & automation surge

- 4.2.5 SiC/GaN-based high-voltage modules adoption

- 4.2.6 Modular eVTOL battery pack architectures

- 4.3 Market Restraints

- 4.3.1 Volatile copper & aluminum prices

- 4.3.2 Low-cost conventional busbars as substitutes

- 4.3.3 Heat-dissipation & delamination beyond 1 kV

- 4.3.4 Aerospace qualification/documentation burden

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Conducting Material

- 5.1.1 Copper

- 5.1.2 Aluminum

- 5.1.3 Hybrid (Cu-Al composite)

- 5.2 By Insulation Material

- 5.2.1 Epoxy Powder Coating

- 5.2.2 Polyvinyl Fluoride Film

- 5.2.3 Polyester

- 5.2.4 Heat-Resistant Fiber

- 5.2.5 Polyimide/Kapton

- 5.2.6 Others

- 5.3 By Busbar Configuration

- 5.3.1 Multi-layer (3 to 5 layers)

- 5.3.2 High-layer (More Than 5 layers)

- 5.3.3 Flex/Thin busbars

- 5.4 By Voltage Rating

- 5.4.1 Low Voltage (Below 1 kV)

- 5.4.2 Medium Voltage (1 to 35 kV)

- 5.4.3 High Voltage (Above 35 kV)

- 5.5 By Application

- 5.5.1 Electric and Hybrid Vehicles

- 5.5.2 Renewable Energy (Solar, Wind, ESS)

- 5.5.3 Data Centers and Cloud Infrastructure

- 5.5.4 Industrial Drives and Machinery

- 5.5.5 Rail and Mass Transit

- 5.5.6 Aerospace and eVTOL

- 5.6 By End-User

- 5.6.1 Power Utilities

- 5.6.2 Industrial OEMs

- 5.6.3 Transportation OEMs

- 5.6.4 Residential and Commercial Construction

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germnay

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Russia

- 5.7.2.7 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 Australia

- 5.7.3.6 ASEAN Countries

- 5.7.3.7 Rest of Asia Pacific

- 5.7.4 South America

- 5.7.4.1 Argentina

- 5.7.4.2 Brazil

- 5.7.4.3 Rest of South America

- 5.7.5 Middle East and Africa

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 South Africa

- 5.7.5.4 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Eaton Corporation plc

- 6.4.2 Rogers Corporation

- 6.4.3 Mersen SA

- 6.4.4 Methode Electronics Inc.

- 6.4.5 Amphenol Corporation

- 6.4.6 Molex LLC

- 6.4.7 Sun.King Power Electronics Group Ltd

- 6.4.8 Zhuzhou CRRC Times Electric Co., Ltd

- 6.4.9 Storm Power Components

- 6.4.10 Segue Electronics Inc.

- 6.4.11 EMS Industrial & Service Company

- 6.4.12 Ryoden Kasei Co., Ltd

- 6.4.13 Shanghai Eagtop Electronic Technology Co., Ltd

- 6.4.14 Suzhou West Deane Machinery Inc.

- 6.4.15 Raychem RPG Private Limited

- 6.4.16 Zhejiang RHI Electric Co., Ltd

- 6.4.17 Electronic Systems Packaging LLC

- 6.4.18 Idealec SAS

- 6.4.19 Advanced Energy Industries, Inc.

- 6.4.20 Delta Electronics, Inc.

- 6.4.21 Siemens AG

- 6.4.22 ABB Ltd

- 6.4.23 Schneider Electric SE

- 6.4.24 Littelfuse Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment