|

市場調查報告書

商品編碼

2043886

美國丙烷:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)United States Propane - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

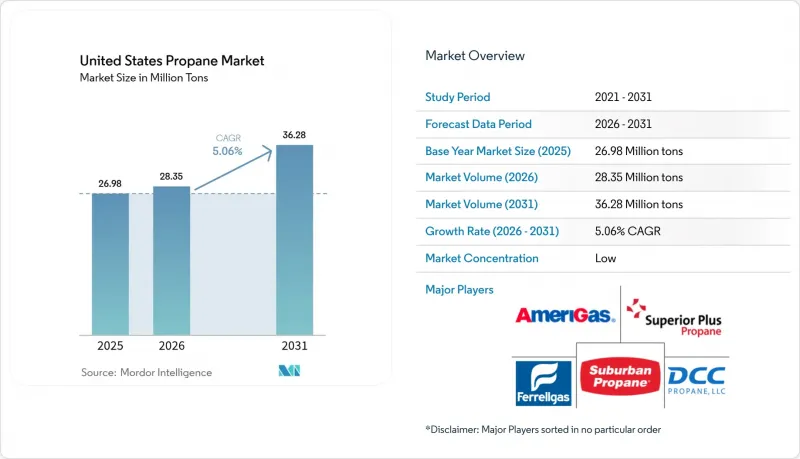

美國丙烷市場預計將從 2025 年的 2,698 萬噸和 2026 年的 2,835 萬噸成長到 2031 年的 3,628 萬噸,2026 年至 2031 年的年複合成長率(CAGR)為 5.06%。

在丙烷脫氫 (PDH) 設施的擴張和丙烷作為緊急電源的廣泛應用推動下,車輛燃料的轉型正在加速。這一趨勢正將需求重心從傳統上受天氣影響的住宅用氣轉向交通運輸和石化應用。預計到 2025 年,天然氣加工將佔總需求的大部分。然而,可再生丙烷也取得了顯著進展。這一成長主要得益於加州低碳燃料標準 (LCFS) 積分制度,該制度改變了採購經濟的結構。受校車燃料轉型和最後一公里配送擴張的推動,汽車燃料需求正在成長。這些轉型使得燃料成本相比柴油大幅降低,同時符合更嚴格的氮氧化物排放法規。對墨西哥灣沿岸地區 PDH 設施的投資正在創造對原料的結構性需求,並緩解供暖需求季節性波動的影響。同時,物聯網賦能的「丙烷即服務」模式正在革新分銷方式。透過減少經銷商的配送次數並提高客戶維繫率,這些模式使大型零售商能夠在原本分散的市場中保持強大的地位。

美國丙烷市場趨勢與洞察

柴油車法規的收緊正在加速車隊向汽車燃氣的過渡。

學區正利用「清潔校車計畫」的津貼來替換柴油車輛。由於丙烷比柴油更具成本效益,投資可在短短幾年內收回成本。丙烷缸內直噴引擎動力強勁,不僅能提供與柴油相當的扭矩,還能顯著降低氮氧化物排放。 Bluebird 的 7.3 昇平台和康明斯的 B6.7 丙烷引擎正將這項技術推廣到 6-7 級貨車車隊,目標市場規模達數十萬輛。車隊營運商的燃料成本大幅降低,遠端資訊處理數據也證實了車輛性能穩定,在年度運作週期內實現了優異的燃油效率。隨著大都會圈低排放氣體區的持續實施,丙烷系統相比純電動系統所需的初始投資更低,這正在加速這一轉型,預計這一趨勢將在 2026 年至 2031 年的預測期內持續下去。

石油化工PDH產能的提高將鞏固對原料的需求。

Enterprise Products Partners 的 PDH 2 工廠每天處理大量丙烷,生產聚合級丙烯。隨著利安德巴塞爾管道佈局的拓展,預計到 2028 年,該工廠的產能將進一步提升。由於 PDH 工廠目前在石化丙烷消費中佔據相當大的比例,因此其需求與煉油廠的運轉率脫鉤。同時,儘管面臨 ESG 融資方面的挑戰,但新型流化催化脫氫 (FCDh) 工廠憑藉其較低的資本成本,正在推動產能擴張。展望未來,強勁的石化需求預計將在 2026 年至 2031 年的預測期內提振美國丙烷市場。

價格波動給經銷商的利潤空間帶來了壓力。

2024年,溫暖的天氣和創紀錄的天然氣凝液(NGL)產量導致蒙特貝爾維尤現貨價格大幅下跌,給固定價格合約擁有者帶來了挑戰。全年出口量激增,大量桶裝供應轉向海外,主要受亞洲市場誘人溢價的推動。墨西哥灣沿岸與區域樞紐之間的基差風險經常導致避險不完全。因此,郊區丙烷公司(Suburban Propane)的銷售量有所成長,但本會計年度每加侖的毛利率卻有所下降。

細分市場分析

到2025年,天然氣加工將主導供應結構,佔高達78.72%的佔有率。這主要得益於蒙特貝爾維尤(Mont Bellevue)的分餾作業以及二疊紀盆地聯產氣的強勁產量。即使煉油產品供應下降,這些加工趨勢仍在鞏固美國丙烷市場。目前,可再生丙烷僅佔總供應量的一小部分,但其成長勢頭強勁,預計2026年至2031年預測期內的複合年成長率將達到9.95%。這一成長主要由低碳燃料標準(LCFS)積分驅動,創造了一個盈利的細分市場,吸引了加州和奧勒岡地區早期採用者的注意。在這個不斷發展的美國丙烷市場中,傳統的液態天然氣(NGL)開採滿足了商品需求,而開創性的低碳舉措則吸引了以積分為導向的買家。

併購清晰地展現了基礎設施價值的日益成長。 ONEOK收購Magellan,將兩家擁有強大分餾能力的巨頭公司合併在一起。 Enterprise正在系統性地擴大其儲罐,以提高出口柔軟性。儘管面臨嚴格的ESG(環境、社會和治理)審查,但由於丙烯脫氫(PDH)和出口市場需求穩定,生產商對加工項目仍保持樂觀態度。可再生能源領域的先驅Neste和Oberon正在建造緊湊型設施。透過利用現有的可再生柴油和二甲醚(DME)生產線,他們體現了一種擴大低碳供應的策略性和模組化方法。

《美國丙烷市場報告》按來源(天然氣加工、原油煉製、可再生能源)、應用(供暖和熱水、烹飪、汽車燃料、化學原料、發電及其他應用)和終端用戶行業(住宅、商業、工業、交通運輸、發電及其他終端用戶行業)進行細分。市場預測以噸為單位。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 車輛改裝為汽車燃氣(校車/送貨車/市政車輛)

- 提高石油化工PDH的生產能力

- 安裝備用發電機以提高電網的韌性。

- 丙烷即服務 (PaaS) 訂閱模式(物聯網儲罐監控)

- 用於區域寬頻塔的離網微電網

- 市場限制因素

- 與天然氣凝液和原油市場相關的價格波動

- 主要PADD地區的鐵路和管道瓶頸

- 受環境、社會和治理因素驅動的資產出售正在抑制上游產業的資本投資。

- 價值鏈分析

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按供應來源

- 天然氣加工

- 原油煉製

- 可再生丙烷(生物丙烷)

- 透過使用

- 暖氣和熱水供應

- 烹飪

- 汽車燃料

- 化工原料

- 發電

- 其他用途

- 按最終用戶行業分類

- 住宅

- 商業的

- 產業

- 運輸

- 發電

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- AmeriGas Propane, Inc.

- Blossman Gas

- CHS Inc.

- DCC Propane

- Energy Transfer LP

- Ferrellgas

- GROWMARK Inc.

- MFA Oil Company

- NGL Energy Partners LP

- Paraco

- Pinnacle

- Suburban Propane

- Superior Plus Propane

- ThompsonGas

第7章 市場機會與未來展望

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 車輛改裝為汽車燃氣(校車/送貨車/市政車輛)

- 提高石油化工PDH的生產能力

- 安裝備用發電機以提高電網的韌性。

- 丙烷即服務 (PaaS) 訂閱模式(物聯網儲罐監控)

- 用於區域寬頻塔的離網微電網

- 市場限制因素

- 與天然氣凝液和原油市場相關的價格波動

- 主要PADD地區的鐵路和管道瓶頸

- 受環境、社會和治理因素驅動的資產出售正在抑制上游產業的資本投資。

- 價值鏈分析

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按供應來源

- 天然氣加工

- 原油煉製

- 可再生丙烷(生物丙烷)

- 透過使用

- 暖氣和熱水供應

- 烹飪

- 汽車燃料

- 化工原料

- 發電

- 其他用途

- 按最終用戶行業分類

- 住宅

- 商業的

- 產業

- 運輸

- 發電

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- AmeriGas Propane, Inc.

- Blossman Gas

- CHS Inc.

- DCC Propane

- Energy Transfer LP

- Ferrellgas

- GROWMARK Inc.

- MFA Oil Company

- NGL Energy Partners LP

- Paraco

- Pinnacle

- Suburban Propane

- Superior Plus Propane

- ThompsonGas

第7章 市場機會與未來展望

The United States Propane Market size is projected to expand from 26.98 million tons in 2025 and 28.35 million tons in 2026 to 36.28 million tons by 2031, registering a CAGR of 5.06% between 2026 to 2031.

Fleet conversions are gaining momentum, driven by expanding propane dehydrogenation (PDH) capacities and robust standby-power deployments. These developments are shifting volumes away from a traditionally weather-dependent residential base and toward transportation and petrochemical applications. By 2025, natural-gas processing accounted for the majority of the total volume. However, renewable propane has been making significant progress. This growth is largely attributed to California's Low Carbon Fuel Standard (LCFS) credits, which have transformed the economics of sourcing. The demand for motor fuel has been rising, driven by conversions in school buses and last-mile deliveries. These transitions are resulting in notable savings in fuel costs compared to diesel, all while adhering to stricter NOx emissions limits. Investments in PDH facilities along the Gulf Coast have created a structural pull for feedstock, providing insulation from seasonal heating fluctuations. On another front, IoT-enabled "Propane-as-a-Service" models are revolutionizing the distribution landscape. By reducing distributor truck rolls and boosting customer retention, these models are empowering large retailers to maintain their foothold in an otherwise fragmented market.

United States Propane Market Trends and Insights

Autogas Fleet Conversions Accelerate as Diesel Rules Tighten

School districts are utilizing Clean School Bus Program grants to replace diesel units. By securing propane at a cost lower than diesel, they achieve paybacks in just a few years. Propane direct-injection engines, with their impressive horsepower, not only replicate diesel torque but also significantly reduce NOx emissions. Blue Bird's 7.3-liter platform and Cummins' B6.7 Propane are advancing this technology into Class 6-7 delivery fleets, targeting a market of hundreds of thousands of vehicles. Fleet operators are experiencing substantial fuel savings, and telematics confirm steady performance with annual duty cycles achieving impressive mileage. As more metropolitan areas adopt low-emission zones, the lower capital requirement of propane - compared to battery-electric systems - is accelerating conversions, a trend projected to persist during the forecast period of 2026-2031

Petrochemical PDH Capacity Additions Lock In Feedstock Demand

Enterprise Products Partners' PDH 2, which processes a substantial daily volume of propane, produces polymer-grade propylene. By 2028, LyondellBasell's Channelview expansion will add to this capacity. With PDH units now commanding a significant portion of petrochemical propane consumption, their demand has become decoupled from refinery operating rates. Meanwhile, newer fluid catalytic dehydrogenation (FCDh) designs, which come with lower capital costs, are driving capacity expansions, despite hurdles in ESG financing. Looking ahead, robust petrochemical demand during the forecast period of 2026-2031 is expected to bolster the United States propane market.

Price Volatility Compresses Distributor Margins

In 2024, warm weather and record NGL output caused a significant drop in Mont Belvieu spot prices, posing challenges for holders of fixed-price contracts. Throughout the year, exports surged, with barrels being redirected offshore due to attractive premiums in Asia. The basis risk between the Gulf and regional hubs often resulted in imperfect hedges. As a result, Suburban Propane experienced a decline in its fiscal-year gross margin per gallon, even with increased volumes.

Other drivers and restraints analyzed in the detailed report include:

- Stand-by Generator Installations Rise with Grid-Reliability Investments

- Propane-as-a-Service Subscription Models Boost Margins

- Rail and Pipeline Bottlenecks Elevate Logistics Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, natural-gas processing dominated the supply landscape, commanding a substantial 78.72% share. This was largely driven by fractionation activities at Mont Belvieu and robust outputs from the Permian's associated gas. Such processing dynamics fortify the U.S. propane market, even as contributions from refinery coproducts diminish. Although renewable propane currently holds a modest slice of the supply pie, it is on an impressive growth trajectory, boasting a 9.95% CAGR during the forecast period of 2026-2031. This surge is largely attributed to LCFS credits, carving out a lucrative niche that has piqued the interest of early adopters in the California-Oregon region. In this evolving U.S. propane landscape, traditional NGL extraction aligns with commodity demands, while pioneering low-carbon initiatives draw in credit-centric buyers.

Mergers and acquisitions underscore the escalating value of infrastructure: ONEOK's takeover of Magellan unified two powerhouses with substantial fractionation capabilities. In a bid to bolster export flexibility, Enterprise is methodically expanding its storage caverns. Even amidst ESG scrutiny, producers maintain an optimistic outlook on processing projects, buoyed by consistent demand from PDH and export markets. Renewable trailblazers, Neste and Oberon, are establishing compact facilities. By harnessing existing renewable-diesel or DME trains, they are exemplifying a strategic, modular approach to scaling low-carbon supplies.

The United States Propane Market Report is Segmented by Source (Natural Gas Processing, Crude Oil Refining, and Renewable), Application (Space and Water Heating, Cooking, Motor Fuel, Chemical Feedstock, Power Generation, and Other Applications), and End-User Industry (Residential, Commercial, Industrial, Transportation, Power Generation, and Other End-User Industries). The Market Forecasts are Provided in Terms of Volume (Tons).

List of Companies Covered in this Report:

- AmeriGas Propane, Inc.

- Blossman Gas

- CHS Inc.

- DCC Propane

- Energy Transfer LP

- Ferrellgas

- GROWMARK Inc.

- MFA Oil Company

- NGL Energy Partners LP

- Paraco

- Pinnacle

- Suburban Propane

- Superior Plus Propane

- ThompsonGas

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Autogas fleet conversions (school buses/delivery/municipal)

- 4.2.2 Petrochemical PDH capacity additions

- 4.2.3 Stand-by generator installations for grid resiliency

- 4.2.4 Propane-as-a-Service subscription models (IoT tank monitoring)

- 4.2.5 Off-grid microgrids for rural broadband towers

- 4.3 Market Restraints

- 4.3.1 Price volatility tied to NGL and crude markets

- 4.3.2 Rail/pipeline bottlenecks in key PADDs

- 4.3.3 ESG-driven divestment limiting upstream capex

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Source

- 5.1.1 Natural Gas Processing

- 5.1.2 Crude Oil Refining

- 5.1.3 Renewable Propane (Bio-Propane)

- 5.2 By Application

- 5.2.1 Space and Water Heating

- 5.2.2 Cooking

- 5.2.3 Motor Fuel

- 5.2.4 Chemical Feedstock

- 5.2.5 Power Generation

- 5.2.6 Other Applications

- 5.3 By End-user Industry

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.3.4 Transportation

- 5.3.5 Power Generation

- 5.3.6 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 AmeriGas Propane, Inc.

- 6.4.2 Blossman Gas

- 6.4.3 CHS Inc.

- 6.4.4 DCC Propane

- 6.4.5 Energy Transfer LP

- 6.4.6 Ferrellgas

- 6.4.7 GROWMARK Inc.

- 6.4.8 MFA Oil Company

- 6.4.9 NGL Energy Partners LP

- 6.4.10 Paraco

- 6.4.11 Pinnacle

- 6.4.12 Suburban Propane

- 6.4.13 Superior Plus Propane

- 6.4.14 ThompsonGas

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

丙烷市場預測至2034年:按形態、等級、最終用戶和地區分類的全球分析

丙烷市場預測至2034年:按形態、等級、最終用戶和地區分類的全球分析 丙烷市場:2026-2032年全球市場預測(依產品類型、儲存類型、銷售管道及最終用途產業分類)

丙烷市場:2026-2032年全球市場預測(依產品類型、儲存類型、銷售管道及最終用途產業分類) 丙烷市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年

丙烷市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年 全球丙烷市場:依等級、最終用途及地區分類的分析-市場規模、產業趨勢、機會分析及2026年至2035年預測

全球丙烷市場:依等級、最終用途及地區分類的分析-市場規模、產業趨勢、機會分析及2026年至2035年預測 丙烷市場規模、佔有率、趨勢和預測:按形態、等級、最終用途行業和地區分類,2026-2034年三羥甲基丙烷市場按技術、形態和應用分類,全球預測(2026-2032年)全球三羥甲基丙烷市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

丙烷市場規模、佔有率、趨勢和預測:按形態、等級、最終用途行業和地區分類,2026-2034年三羥甲基丙烷市場按技術、形態和應用分類,全球預測(2026-2032年)全球三羥甲基丙烷市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球丙烷市場報告

2026年全球丙烷市場報告 丙烷市場規模、佔有率和成長分析(按形態、應用、等級和地區分類)-2026-2033年產業預測

丙烷市場規模、佔有率和成長分析(按形態、應用、等級和地區分類)-2026-2033年產業預測 丙烷市場-全球產業規模、佔有率、趨勢、機會和預測,按形態、最終用戶、地區和競爭格局分類,2020-2030年預測

丙烷市場-全球產業規模、佔有率、趨勢、機會和預測,按形態、最終用戶、地區和競爭格局分類,2020-2030年預測