|

市場調查報告書

商品編碼

2043881

東協摩托車租賃市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)ASEAN Two-Wheeler Rental - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

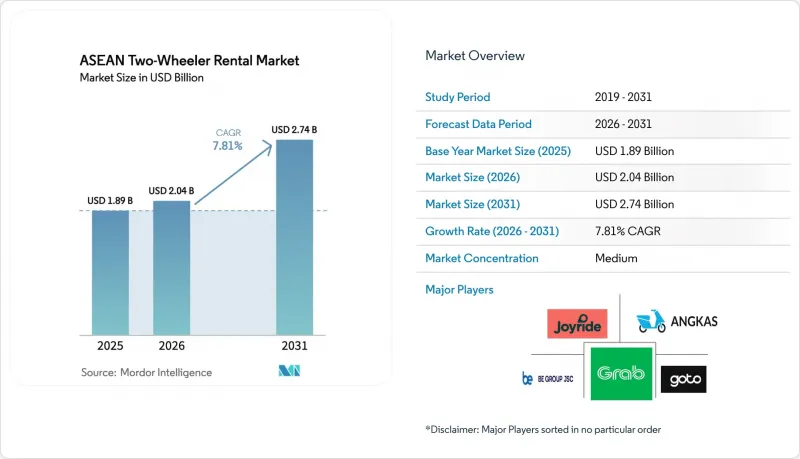

2025年東協摩托車租賃市場價值18.9億美元,預計到2031年將達到27.4億美元,高於2026年的20.4億美元,預測期(2026-2031年)複合年成長率為7.81%。

超級應用程式的出現,將租賃按鈕與共享出行功能相結合,正在加速從所有權模式轉變為按使用量模式的方式;與此同時,城市層級禁止內燃機摩托車的政策也在加速電動化。東南亞各地的遊客數量已經超過疫情前水平,峇裡島、普吉島和長灘島的短期租賃需求正在復甦。同時,雅加達、曼谷和馬尼拉大都會區長期存在的交通堵塞問題,促使通勤者轉向經濟實惠的電動滑板車,以便快速繞過擁擠路段,而不是選擇汽車。電池更換網路使駕駛者能夠在不到一分鐘的時間內更換耗盡的電池組,從而減少停機時間,並將每日出行次數提高30-40%。產業重組也在加速進行。 Grab、GoTo和Xanh SM等公司都在利用嵌入式小額信貸來留住用戶,而VinFast和Gogoro等原始設備製造商(OEM)也正在進軍租賃市場,利用規模經濟優勢以低於小規模店舖的價格提供服務。

東協摩托車租賃市場趨勢與洞察

後疫情時代旅遊業主導的需求復甦

預計到2025年,國際遊客數量將超過2019年的水平,這將帶動海灘和島嶼旅遊目的地對摩托車的需求再次激增。峇里島的自行車租賃業務已恢復到疫情前水平,日租金在5萬至15萬印尼幣(約合3.10至9.30美元)之間;而普吉島的租賃價格則為每日400至1800泰銖(約合11至50美元)。預計2024年,越南將迎來1,750萬遊客,峴港和芽莊的車輛數量將增加25%至30%。為了吸引具有環保意識的旅行者,營運商們正在引入電動滑板車,這一趨勢也體現在泰國Grab計劃於2024年在五個城市推出電動車服務。平均租賃時間已從三天延長至六天,提高了每輛車的收入,並穩定了淡季現金流。

都市區擁擠促進了經濟實惠的通勤方式。

曼谷通勤者每年因交通壅塞浪費61小時,馬尼拉的交通壅塞每年造成35億美元的損失,雅加達的平均通勤時間超過90分鐘。預計到2024年,印尼的叫車服務將達到90億次,成長13%,許多零工人員為了避免預付費用而轉向租賃模式。胡志明市擁有超過700萬輛摩托車,顯示密集的摩托車車隊在點對點行駛速度方面仍然優於汽車。企業對送貨騎士的補貼使每月租金降低了15-20%,使得訂閱模式更具吸引力。 Xanh SM的收入分成模式允許司機獲得80%的車費,使他們能夠實現每月超過700美元的收入目標。這些經濟因素正在鞏固東協摩托車租賃市場作為最後一公里物流重要支柱的地位。

事故率高,保險費高

在東協,摩托車事故佔道路交通事故死亡總數的43%,預計到2024年,印尼將有26,000人死於摩托車事故,越南將有10,500人死於摩托車事故。這迫使保險公司將高風險路段的保費提高15%至20%。在泰國,預計2024年將有15,000人死於摩托車事故,迫使保險公司對每輛摩托車的租賃加收5至10泰銖,導致租賃利潤率下降高達12%。據亞洲開發銀行稱,菲律賓遍遠地區的頭盔使用率低於50%,這導致保險索賠增加。營運商透過實施DRVR的遠端資訊處理系統來監控駕駛行為,已將竊盜率降低了20%,燃油消耗量降低了26%。然而,這使得保險公司可以根據每位駕駛員的風險來定價。這種精細化的定價可能會將高風險、低收入的騎士排除在外,從而可能損害嵌入式金融普惠性的承諾。

細分市場分析

預計到2025年,踏板車和輕型機踏車將佔總收入的58.16%,但電動車款的年成長率預計將達到14.92%,幾乎是東協摩托車租賃市場年複合成長率的兩倍。雖然內燃機摩托車的初始價格仍然較低,但由於需要降低電池更換成本以及即將實施的都市區內燃機摩托車禁令,營運商正在加速車隊的電氣化轉型。排氣量超過150cc的摩托車在山區旅遊區仍然很受歡迎,但其市佔率正在下降至41.84%。 Grab已在印尼新增8,500輛電動車,並計畫在2026年達到14,000輛,而VinFast計畫在2026年中期在印尼開設展示室。由汽車製造商支持的平台提供的價格低於獨立門市,這給整個東協摩托車租賃行業的利潤率帶來了壓力。

到2025年,電動滑板車將佔東協二輪車租賃市場滑板車佔有率的62%,預計到2031年將達到75%。電動滑板車的維護成本比汽油動力車輛低25%,透過更換電池運轉率,可使每輛車的日收入增加約35%。如果城市層級普遍禁止內燃機車輛,缺乏資金更換車輛的營運商將面臨市場佔有率下降的風險,因此資金籌措夥伴關係至關重要。

短期產品(主要為遊客提供一日租賃服務)在2025年佔總收入的64.08%。然而,長期訂閱業務正以11.03%的速度成長,因為共享滑板車用戶更傾向於包含維護、電池更換和保險的可預測的周租或月租價格。 Charged Asia在雅加達提供電動滑板車租賃服務,每月租金為120萬印尼幣(約71美元),其1500輛滑板車中90%都簽訂了訂閱合約。

東協摩托車租賃訂閱市場規模預計將從2026年的6.9億美元成長到2031年的11.5億美元,複合年成長率達10.8%。由於車輛利用率差距縮小,且債務償還與現金收入掛鉤,訂閱模式的車輛終身價值比按次付費租賃模式高出30-40%。整合錢包功能的平台可自動收取使用費,從而顯著降低違約風險。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 新冠疫情蔓延後,主導推動了需求復甦。

- 都市區擁擠促進了經濟實惠的通勤方式。

- 透過超級應用整合摩托車租賃服務

- 電池更換生態系統顯著減少了電動車的停機時間

- 隨著城市層面禁止內燃機(ICE)車輛,車隊正在轉向電動滑板車。

- 嵌入式小額信貸開啟了第二層促進因素。

- 市場限制因素

- 事故率高,保險費飆漲

- 東南亞國協法規的差異

- 由於使用非標準電池,導致零件成本高昂

- 季風季節運轉率下降

- 價值鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 產業間競爭

第5章 市場規模及成長預測(價值(美元)及數量(單位))

- 車輛類型

- 摩托車

- 踏板車/輕型機踏車

- 租賃期

- 短期

- 長期

- 透過使用

- 觀光

- 日常通勤

- 最終用戶

- 個人消費者

- 企業客戶

- 車隊營運商

- 按發行格式

- 線上平台

- 線下租賃機構

- 按地區

- 印尼

- 馬來西亞

- 新加坡

- 菲律賓

- 泰國

- 越南

- 緬甸

- 其他東南亞國協

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Grab Holdings Ltd.

- GoTo Group(Gojek)

- Angkas Holdings Inc.

- JoyRide Logistics and Transport Inc.

- Move It Philippines

- Be Group JSC

- Xanh SM(GSM JSC)

- Swap Energi Indonesia

- Electrum JV

- STROM EV Co. Ltd.

- Motorvina Co. Ltd.

- Viar Motor Indonesia

- Smoot(Kilats)

- Migo Bike Indonesia

- Beam Mobility Holdings

- GrabRentals Pte Ltd.

- Bird Rides Singapore Pte Ltd.

- TRYKE

- Skoot

第7章 市場機會與未來展望

The ASEAN Two-Wheeler Rental Market size was valued at USD 1.89 billion in 2025 and is estimated to grow from USD 2.04 billion in 2026 to reach USD 2.74 billion by 2031, at a CAGR of 7.81% during the forecast period (2026-2031).

A rapid shift from ownership to access-based mobility is underway as super-apps embed rental buttons beside ride-hailing, while city-level bans on internal-combustion motorcycles accelerate electrification. Tourism arrivals across Southeast Asia have already exceeded pre-pandemic levels, reviving short-term rental demand in Bali, Phuket, and Boracay. At the same time, chronic traffic congestion in Jakarta, Bangkok, and Metro Manila pushes commuters toward cost-efficient scooters that slip through gridlock faster than cars. Battery-swap networks now allow drivers to exchange depleted packs in under a minute, cutting downtime and lifting daily trip counts by 30-40%. Consolidation is accelerating: Grab, GoTo, and Xanh SM all use embedded microlending to lock in riders, while OEMs such as VinFast and Gogoro enter the rental arena and underprice smaller shops by leveraging manufacturing scale.

ASEAN Two-Wheeler Rental Market Trends and Insights

Tourism-Led Demand Rebound Post-COVID

International arrivals surpassed 2019 levels in 2025, reigniting scooter demand in beach and island destinations. Bali's motorcycle rentals recovered to pre-pandemic volumes at daily rates of 50,000-150,000 IDR (USD 3.10-9.30), while Phuket operators charge 400-1,800 THB (USD 11-50) per day. Vietnam welcomed 17.5 million visitors in 2024, spurring fleet expansions of 25-30% in Da Nang and Nha Trang. Operators add electric scooters to appeal to eco-minded travelers, as seen in Grab Thailand's 2024 EV rollout across five cities. Average rental length is stretching from three to six days, boosting revenue per unit and stabilizing offseason cash flow.

Urban Congestion Drives Cost-Effective Commuting

Bangkok commuters lose 61 hours annually in traffic, Manila's gridlock costs USD 3.5 billion each year, and Jakarta's average commute exceeds 90 minutes. Ride-hailing motorcycle trips in Indonesia jumped 13% to 9 billion in 2024, with many gig workers shifting to rental plans to avoid upfront purchases. Ho Chi Minh City's 7 million-plus motorcycles underscore how dense fleets still beat cars in point-to-point speed. Corporate subsidies for delivery riders shrink monthly rental costs by 15-20%, making subscriptions attractive. Xanh SM's revenue-share model lets drivers keep 80% of fares, pushing their monthly income target above USD 700. These economics cement the ASEAN two-wheeler rental market as a critical pillar of last-mile logistics.

High Accident and Insurance Premiums

Motorcycles cause 43% of ASEAN road deaths, with Indonesia logging 26,000 fatalities in 2024 and Vietnam 10,500, forcing insurers to raise premiums 15-20% on risky corridors. Thailand saw 15,000 motorcycle deaths in 2024, leading insurers to add 5-10 THB per-trip surcharges that cut rental margins by up to 12%. Helmet use below 50% in rural Philippines magnifies claims, says the Asian Development Bank. Operators deploy telematics from DRVR to monitor behavior, cutting theft by 20% and fuel by 26% but also letting underwriters price risk driver-by-driver. This granular pricing can exclude high-risk, low-income riders, undercutting the inclusivity promise of embedded finance.

Other drivers and restraints analyzed in the detailed report include:

- Super-Apps Integrate Two-Wheeler Rentals

- Battery-Swap Ecosystems Slash EV Downtime

- Regulatory Patchwork Across ASEAN

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Scooters and mopeds accounted for 58.16% of revenue in 2025, yet electric models will post 14.92% annual growth, nearly double the ASEAN two-wheeler rental market CAGR. Internal-combustion bikes still cost less up front, but battery-swap savings and looming urban bans are pushing operators to electrify fleets quickly. Motorcycles above 150 cc remain popular for hillier tourist zones, though their 41.84% share is slipping. Grab added 8,500 electric units in Indonesia, targeting 14,000 by 2026, while VinFast plans Indonesian showrooms by mid-2026. OEM-backed platforms undercut stand-alone shops, tightening margins across the ASEAN two-wheeler rental industry.

Electric scooters commanded 62% of the ASEAN two-wheeler rental market size for scooters in 2025 and are forecast to reach 75% by 2031. Their maintenance costs are 25% below those of petrol peers, and battery-swap uptime boosts daily revenue per vehicle by roughly 35%. Operators without capital for fleet replacement risk losing share once city-level ICE bans bite, making financing partnerships critical.

Short-term products, mostly daily rentals to tourists, contributed 64.08% of revenue in 2025. However, long-term subscriptions are expanding at 11.03%, as gig riders prefer predictable weekly or monthly fees that include maintenance, swaps, and insurance. Charged Asia leases e-scooters in Jakarta at 1.2 million IDR (USD 71) per month, with 90% of its 1,500-unit fleet on subscription.

The ASEAN two-wheeler rental market size for subscriptions is projected to climb from USD 0.69 billion in 2026 to USD 1.15 billion by 2031, reflecting a 10.8% CAGR. The lifetime value per bike is 30-40% higher than for ad-hoc hires because utilization gaps shrink and debt service aligns with cash receipts. Platforms with integrated wallets automatically collect dues, slashing default risk.

The ASEAN Two-Wheeler Rental Market Report is Segmented by Vehicle Type (Motorcycles and Scooters/Mopeds), Rental Duration (Short-Term and Long-Term), Application (Tourism and Daily Commuting), End User (Individual Consumers and More), Distribution Mode (Online Platforms and More), and Geography (Indonesia, Malaysia, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- Grab Holdings Ltd.

- GoTo Group (Gojek)

- Angkas Holdings Inc.

- JoyRide Logistics and Transport Inc.

- Move It Philippines

- Be Group JSC

- Xanh SM (GSM JSC)

- Swap Energi Indonesia

- Electrum JV

- STROM EV Co. Ltd.

- Motorvina Co. Ltd.

- Viar Motor Indonesia

- Smoot (Kilats)

- Migo Bike Indonesia

- Beam Mobility Holdings

- GrabRentals Pte Ltd.

- Bird Rides Singapore Pte Ltd.

- TRYKE

- Skoot

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tourism-Led Demand Rebound Post-COVID

- 4.2.2 Urban Congestion Drives Cost-Effective Commuting

- 4.2.3 Super-Apps Integrate Two-Wheeler Rentals

- 4.2.4 Battery-Swap Ecosystems Slash EV Downtime

- 4.2.5 City-Level ICE Bans Pivot Fleets to E-Scooters

- 4.2.6 Embedded Microlending Unlocks Tier-2 Driver Pool

- 4.3 Market Restraints

- 4.3.1 High Accident and Insurance Premiums

- 4.3.2 Regulatory Patchwork Across ASEAN

- 4.3.3 Non-Standard Batteries Inflate Spare-Part Costs

- 4.3.4 Monsoon-Season Utilization Dips

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size and Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Vehicle Type

- 5.1.1 Motorcycles

- 5.1.2 Scooters/Mopeds

- 5.2 By Rental Duration

- 5.2.1 Short-Term

- 5.2.2 Long-Term

- 5.3 By Application

- 5.3.1 Tourism

- 5.3.2 Daily Commuting

- 5.4 By End User

- 5.4.1 Individual Consumers

- 5.4.2 Corporate Clients

- 5.4.3 Fleet Operators

- 5.5 By Distribution Mode

- 5.5.1 Online Platforms

- 5.5.2 Offline Rental Agencies

- 5.6 By Geography

- 5.6.1 Indonesia

- 5.6.2 Malaysia

- 5.6.3 Singapore

- 5.6.4 Philippines

- 5.6.5 Thailand

- 5.6.6 Vietnam

- 5.6.7 Myanmar

- 5.6.8 Rest of ASEAN

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Grab Holdings Ltd.

- 6.4.2 GoTo Group (Gojek)

- 6.4.3 Angkas Holdings Inc.

- 6.4.4 JoyRide Logistics and Transport Inc.

- 6.4.5 Move It Philippines

- 6.4.6 Be Group JSC

- 6.4.7 Xanh SM (GSM JSC)

- 6.4.8 Swap Energi Indonesia

- 6.4.9 Electrum JV

- 6.4.10 STROM EV Co. Ltd.

- 6.4.11 Motorvina Co. Ltd.

- 6.4.12 Viar Motor Indonesia

- 6.4.13 Smoot (Kilats)

- 6.4.14 Migo Bike Indonesia

- 6.4.15 Beam Mobility Holdings

- 6.4.16 GrabRentals Pte Ltd.

- 6.4.17 Bird Rides Singapore Pte Ltd.

- 6.4.18 TRYKE

- 6.4.19 Skoot

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment