|

市場調查報告書

商品編碼

2043875

汽車自動停車系統:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Automotive Automated Parking System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

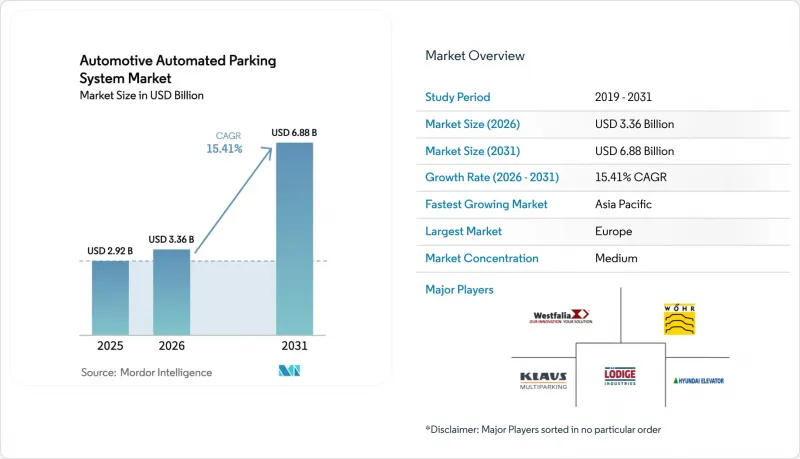

預計汽車自動停車系統的市場規模將從 2025 年的 29.2 億美元成長到 2026 年的 33.6 億美元,然後從 2026 年到 2031 年以 15.41% 的複合年成長率成長,到 2031 年達到 68.8 億美元。

城市地價上漲、鼓勵縮小用地面積的規劃激勵措施以及車輛電氣化的穩步推進,正促使開發商轉向節省空間的機器人停車系統。營運商透過引入軟體訂閱服務(除硬體外),將一次性建設項目轉變為持續的收入來源。自動代客泊車的ISO標準正在加速全自動系統的普及,而ESG評估框架則賦予封閉式、節能型建築特定的價值,這些建築有助於緩解城市熱島效應。這些因素共同推動了系統的強勁成長,但高昂的初始投資和網路安全風險在某些地區阻礙了其應用。

全球汽車自動停車系統市場趨勢與洞察

都市區土地短缺和房地產價格飆升

在曼哈頓,公寓停車位的價值極高。同時,在東京、新加坡和雪梨等城市,預計2020年至2025年間建築成本將大幅上漲。自動化停車系統減少了每輛車所需的空間,從而釋放了租賃面積,並提高了專案的內部收益率(IRR)。例如,阿姆斯特丹的維塞爾格拉赫特塔樓(Wieselgracht Tower)所需的土地面積遠小於傳統的坡道式停車庫,並且採用長期服務合約運作。同樣,邁阿密布里克爾區的開發商也正在利用這些優勢,透過公寓價格的上漲,在幾年內收回了自動化停車系統的投資。

關於連網停車基礎設施的智慧城市強制性舉措

到2027年,華盛頓特區計劃要求新商業建築的部分停車位預裝電動車充電線。同時,加州的CalGreen法規為符合最低標準的、採用自動化解決方案的停車位企業提供容積率獎勵。歐洲機場也在朝著這個方向發展。 2025年,法蘭克福機場將安裝超音波感測器,透過行動應用程式引導駕駛者找到可用的停車位。這些措施正在推動對能夠透過V2X鏈路傳輸即時運作資料的雲端連接系統的需求。

高額資本投入與投資報酬率的不確定性

在都市區,每輛車的高昂成本會導致更長的投資回收期。在郊區,較低的人口密度和需求會進一步延長投資回收期。布里克爾大樓的早期停車系統曾遭遇長達數天的系統故障,導致營運中斷,並於2024年被判支付巨額賠償金。此案例凸顯了運作帶來的巨大財務風險,尤其對於依賴系統穩定運作的業主而言更是如此。雖然「停車即服務」模式透過降低初始投資減輕了初期財務負擔,但服務供應商收取的收入分成可能會降低長期利潤率,並可能影響此類投資的整體財務可行性。

細分市場分析

2025年,硬體收入佔總營收的66.25%,但軟體正以18.65%的複合年成長率快速成長,成長遠超硬體。預計從2026年到2031年,汽車自動停車系統軟體平台市場規模將實現顯著的收入成長,營運商將透過數據、授權和行動支付實現獲利。 Smart Parking Limited 2024年的財務業績清晰地印證了這一模式,其雲端使用費、車牌識別(ANPR)罰款和分析服務收入支撐了可觀的毛利率。

對現有設施進行改造的需求依然強勁。奧蘭多國際機場已簽署一份價值超過1300萬美元的契約,計劃在2025年前在其五個現有停車場安裝基於鏡頭的引導系統,這將使駕駛員尋找停車位的時間減少40%。供應商也指出,整個行業的趨勢是軟體利潤率高達60-80%,而硬體利潤率僅為15-25%,這促使他們開發出涵蓋10-15年的綜合服務契約,以確保系統運轉率和穩定的現金流。

預計到2025年,全自動設計將佔總營收的55.03%,年複合成長率達23.01%。在里昂機場,多台Stan AGV自動導引車可在兩分鐘內完成車輛的停靠和取回,而半自動升降機則需要駕駛員將車輛放置在托盤上,這是無法實現的。在邁阿密的住宅大樓,也實現了類似的速度,取回車輛只需不到四分鐘,從而可以採用15%至30%的定價。

由於半自動停車平台的資本支出(CAPEX)比全自動周轉率較低的辦公大樓。但為了符合ISO 23374-1標準,車隊所有者正轉向支援無人值守車輛停靠的系統。預計到2031年,全自動停車系統的市佔率將顯著成長,進一步擴大其目前的領先優勢。

基於托盤的停車系統預計在2025年將佔總銷售額的58.12%,因為它們易於維修現有停車場,而且更換故障托盤只需幾個小時,而不是幾天。在諸如杜塞爾多夫的MIZAL等歐洲綜合用途開發項目中,配備電動車充電接點的托盤正被引入,以確保停車位能夠適應未來加速電氣化的趨勢。

無托盤AGV解決方案正以16.05%的複合年成長率快速成長,使新建設施的設計人員能夠將每層的天花板高度降低8英寸(約20厘米)。由於AGV直接抓取車輪,因此無需托盤即可搬運更重的電動SUV,從而減輕了額外的重量負擔。史丹利機器人公司(Stanley Robotics)的3噸級機器人可以將每立方公尺的儲存密度提高高達50%,從而在土地資源有限的機場實現關鍵的空間節省。

《汽車自動停車系統報告》按系統(硬體和軟體)、自動化程度(半自動和全自動)、平台類型(托盤式和非托盤式)、驅動技術(液壓、電子機械等)、停車層配置(地面塔式等)、最終用戶(住宅等)、銷售形式和地區進行細分。市場預測以美元計價。

區域分析

歐洲正引領自動化停車系統市場的發展,預計2025年將佔全球銷售額的40.18%,並有望在2031年之前維持顯著的複合年成長率。基於EN 14010和TUV認證的明確標準已將許可證獲取時間縮短至最短9個月,這使得像Klaus Multiparking這樣的德國供應商擁有了本土優勢。斯堪地那維亞的納維亞半島的城市正在引入機器人停車系統,將濱水區改造成自行車道;而在英國,重點則放在維修項目上,將系統整合到已有百年歷史的地下室中。

亞太地區成長最快,複合年成長率達16.35%。在中國,多個自動化停車場已運作,僅上海一地就正在試行建造地下停車系統,以配合智慧城市建設。在印度各大城市,由於車輛保有量龐大,地面停車位供應無法滿足需求,對節省空間的塔式停車場的需求激增。在日本,由於地震多發的地質條件,配備液壓阻尼器的筒倉式停車場是主流,而韓國的目標是在2026年前建立AGV平台出口體系。北美將在2025年佔據顯著的市場佔有率。包括奧斯汀-伯格斯特國際機場和奧蘭多國際機場在內的美國機場,在2025年至2026年間大力投資建造智慧停車場,顯示機場方面注重收益和用戶便利性。在邁阿密和多倫多,公寓開發商正在引入機器人停車系統以遵守嚴格的分區法規,而加州的 CalGreen 法規正在鼓勵在輕軌站周圍引入自動化系統。

中東和非洲也為全球收入做出了貢獻。在杜拜,自動化停車位正被整合到獲得LEED鉑金認證的高層建築中,這與阿拉伯聯合大公國雄心勃勃的2050年淨零排放目標相符。同時,利雅德的「2030願景」計畫在大型企劃中部署多個多層機器人停車系統。然而,在撒哈拉以南非洲,不穩定的電網和有限的專案資金阻礙了自動化停車系統的應用,使得拼圖升降機成為主流選擇。儘管佔有率較小,但南美洲正面臨經濟波動。聖保羅的購物中心正在試行使用自動導引車(AGV),但由於外匯波動,正式訂單已被推遲。在布宜諾斯艾利斯,商業房地產所有者選擇對現有設施進行感測器維修以提高入住率,而不是新建設施。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 都市區土地短缺和房地產價格飆升

- 智慧城市對連網停車基礎設施的要求

- 特大城市汽車保有量增加和交通壅塞加劇

- 為L4級自動駕駛車輛部署自動代客泊車(AVP)

- 面向業主的「停車即服務」收入模式

- ESG 和綠建築獎勵,鼓勵低佔地面積停車位

- 市場限制因素

- 高額資本投入與投資報酬率的不確定性

- 對運行可靠性和安全性的擔憂

- 物聯網連接停車塔的網路安全風險

- 機器人停車塔建築標準相關法規的製定出現延誤

- 價值鏈/供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模及成長預測(價值(美元))

- 系統特定

- 硬體

- 軟體

- 按自動化級別

- 半自動

- 全自動

- 依平台類型

- 托盤包裝

- 無調色板

- 透過驅動技術

- 油壓

- 電子機械

- 機器人(AGV/穿梭車)

- 按停車層配置

- 地面安裝塔

- 地下筒倉

- 拼圖/堆垛機

- 穿梭車和AGV基地

- 混合結構

- 最終用戶

- 住宅

- 獨立式住宅

- 多用戶住宅

- 商業的

- 辦公大樓

- 購物中心和零售中心

- 飯店及餐飲業

- 機場和交通樞紐

- 醫院和醫療設施

- 大學及教育機構

- 政府/市政當局

- 工業和物流設施

- 住宅

- 按銷售形式

- 新安裝

- 維修

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 南非

- 奈及利亞

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Westfalia Parking

- Wohr Parking

- Klaus Multiparking

- Lodige Industries

- CityLift Parking

- Parkmatic

- Unitronics Corporation

- ShinMaywa Industries

- Robotic Parking Systems Inc.

- ParkPlus Inc.

- Boomerang Systems

- Stanley Robotics(HL Robotics)

- Hyundai Elevator Co., Ltd.

- Valeo(Park4U)

- TreviPark

第7章 市場機會與未來展望

The automotive automated parking system market size is expected to grow from USD 2.92 billion in 2025 to USD 3.36 billion in 2026 and is forecast to reach USD 6.88 billion by 2031 at 15.41% CAGR over 2026-2031.

Surging land prices in dense downtowns, zoning incentives that reward footprint reduction, and the steady electrification of vehicle fleets are pushing developers toward space-saving robotic garages. Operators are layering software subscriptions on top of hardware, converting one-time construction projects into recurring revenue streams. ISO-based standards for automated valet parking are accelerating fully automated deployments, while ESG scoring frameworks now assign tangible value to enclosed, energy-efficient structures that curb heat-island effects. Collectively, these forces underpin robust growth even as high capital outlays and cybersecurity exposure temper adoption in some regions.

Global Automotive Automated Parking System Market Trends and Insights

Urban Land Scarcity and Real-Estate Inflation

In Manhattan, condominium parking spaces are highly valued. Meanwhile, construction costs have significantly increased in cities like Tokyo, Singapore, and Sydney during 2020-2025. Automated parking systems reduce the space required per car, freeing up leasable area and enhancing the internal rates of return for projects. For example, Amsterdam's Vijzelgracht tower requires substantially less land compared to a traditional ramp garage and operates under a long-term service contract. Similarly, developers in Brickell, Miami, are leveraging these benefits, recovering their automated parking investments within a few years through higher condo prices.

Smart-City Mandates for Connected Parking Infrastructure

By 2027, Washington, D.C. will require new commercial buildings to pre-wire a portion of their bays for electric vehicle (EV) charging. Meanwhile, California's CalGreen code offers density bonuses to those who meet parking minimums using automated solutions. European airports are also adapting: In 2025, Frankfurt Airport installed ultrasonic sensors, enabling mobile apps to direct drivers to available parking slots. These initiatives are driving up the demand for cloud-connected systems that can relay occupancy data in real-time through V2X links.

High Capex and ROI Uncertainty

In urban centers, capital outlays per stall can lead to extended payback periods, with suburban areas experiencing even longer durations due to lower population density and reduced demand. At Brickell House, an early-generation system encountered multi-day outages, which disrupted operations and culminated in a substantial legal judgment in 2024. This incident underscores the significant financial risks associated with operational downtime, particularly for property owners relying on consistent system performance. Although Parking-as-a-Service eases the upfront financial burden by reducing initial capital requirements, the revenue share taken by the service provider diminishes long-term profit margins, potentially impacting the overall financial viability of such investments.

Other drivers and restraints analyzed in the detailed report include:

- Rising Vehicle Ownership and Congestion in Mega-Cities

- Automated Valet Parking (AVP) Roll-Outs for Level-4 AV Fleets

- Operational Reliability and Safety Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware commanded 66.25% of 2025 revenue, yet software is expanding at an 18.65% CAGR, a notable increase posted by hardware. The automotive automated parking system market size for software platforms is projected to add significant revenue between 2026 and 2031 as operators monetize data, licensing, and mobile payments. Smart Parking Limited's FY 2024 results showcase the model, with cloud fees, ANPR penalties, and analytics underwriting significant gross margins .

Retrofit demand is strong: Orlando International Airport awarded over USD 13 million in 2025 to overlay camera-based guidance across five existing garages, cutting driver search time by 40%. Vendors echo a wider industrial shift where software enjoys 60-80% margins versus 15-25% for hardware, prompting bundled 10-15-year service contracts that guarantee uptime and steady cash flow.

Fully automated designs controlled 55.03% of 2025 sales and are climbing at 23.01% CAGR. At Lyon Airport, several Stan AGVs park or retrieve a vehicle in under two minutes, a metric impossible for semi-automated lifts that demand driver alignment onto pallets. Residential towers in Miami replicate the speed, retrieving cars within four minutes and enabling 15-30% premium fees.

Semi-automated platforms still suit low-turnover office blocks due to 20-30% lower capex, but ISO 23374-1 compliance is pushing fleet owners toward systems capable of hands-free drop-off. The automated parking system market share for fully automated configurations is expected to rise significantly by 2031, widening today's lead.

Pallet-based architectures held 58.12% of 2025 revenue because they retrofit easily into older garages, and a single seized pallet can be swapped in hours rather than days. European mixed-use developments, such as Dusseldorf's MIZAL, embed pallets fitted with EV-charging contacts, future-proofing stalls as electrification accelerates.

Non-palleted AGV solutions are scaling quickly with a 16.05% CAGR, where new builds allow designers to shave eight inches of headroom per level. AGVs directly grasp wheels, accommodating heavier electric SUVs without the pallet weight penalty. Stanley Robotics' 3-ton robots raise per-cubic-meter density by up to 50%, a decisive saving in land-scarce airports.

The Automotive Automated Parking System Report is Segmented by System (Hardware and Software), Automation Level (Semi-Automated and Fully Automated), Platform Type (Palleted and Non-Palleted), Drive Technology (Hydraulic, Electro-Mechanical, and More), Parking-Level Configuration (Above-Ground Tower, and More), End User (Residential and More), Mode of Sales, and Geography. Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe led the automated parking system market with 40.18% of 2025 revenue and is poised for a notable CAGR to 2031. Clear codes under EN 14010 and TUV certifications compress permitting to as little as nine months, giving German suppliers like Klaus Multiparking a home-field edge . Scandinavian cities deploy robotic garages to reclaim waterfront acreage for bicycle lanes, while the United Kingdom leans on retrofits that tuck systems into century-old basements.

Asia-Pacific delivers the steepest ascent at 16.35% CAGR. China fields several automated facilities and is piloting subterranean bays in Shanghai alone, aligning with its smart-city blueprint. With a significant number of registered vehicles, India's metros are outpacing surface supply, driving a surge in demand for space-efficient towers. In Japan, the earthquake-prone landscape leans towards hydraulic-damped silos, while South Korea gears up to export its AGV platforms by 2026. North America held a notable share of the market in 2025. United States airports, including Austin-Bergstrom and Orlando, invested heavily in 2025-2026 on smart garages, highlighting a focus on revenue and passenger ease. In Miami and Toronto, condo developers are turning to robotic parking to navigate stringent zoning laws, and California's CalGreen code is spurring automated setups close to light-rail stations.

The Middle East and Africa contributed to the global revenue. In Dubai, automated parking bays are being integrated into LEED-Platinum skyscrapers, aligning with the UAE's ambitious 2050 net-zero goals. Meanwhile, Riyadh's Vision 2030 is planning several multi-level robotic garages within its mega-projects. However, in sub-Saharan Africa, unreliable power grids and limited project financing hinder broader adoption, leaving puzzle lifts as the prevalent choice. South America, with a small share, grapples with economic fluctuations. While malls in Sao Paulo are testing AGV pilots, currency volatility has postponed definitive orders. In Buenos Aires, commercial landlords are opting for retrofit sensors to boost existing utilization instead of constructing new facilities.

- Westfalia Parking

- Wohr Parking

- Klaus Multiparking

- Lodige Industries

- CityLift Parking

- Parkmatic

- Unitronics Corporation

- ShinMaywa Industries

- Robotic Parking Systems Inc.

- ParkPlus Inc.

- Boomerang Systems

- Stanley Robotics (HL Robotics)

- Hyundai Elevator Co., Ltd.

- Valeo (Park4U)

- TreviPark

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Urban Land Scarcity and Real-Estate Inflation

- 4.2.2 Smart-City Mandates for Connected Parking Infrastructure

- 4.2.3 Rising Vehicle Ownership and Congestion in Mega-Cities

- 4.2.4 Automated Valet Parking (AVP) Roll-Outs for Level-4 AV Fleets

- 4.2.5 Parking-as-a-Service Revenue Models for Property Owners

- 4.2.6 ESG and Green-Building Incentives for Low-Footprint Car Bays

- 4.3 Market Restraints

- 4.3.1 High Capex and ROI Uncertainty

- 4.3.2 Operational Reliability and Safety Concerns

- 4.3.3 Cyber-Security Risks in IoT-Connected Parking Towers

- 4.3.4 Regulatory Lag in Robotic-Tower Building Codes

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By System

- 5.1.1 Hardware

- 5.1.2 Software

- 5.2 By Automation Level

- 5.2.1 Semi-Automated

- 5.2.2 Fully Automated

- 5.3 By Platform Type

- 5.3.1 Palleted

- 5.3.2 Non-Palleted

- 5.4 By Drive Technology

- 5.4.1 Hydraulic

- 5.4.2 Electro-Mechanical

- 5.4.3 Robotic (AGV/Shuttle)

- 5.5 By Parking-Level Configuration

- 5.5.1 Above-ground Tower

- 5.5.2 Underground Silo

- 5.5.3 Puzzle/Stacker

- 5.5.4 Shuttle and AGV based

- 5.5.5 Hybrid Structures

- 5.6 By End User

- 5.6.1 Residential

- 5.6.1.1 Single-family homes

- 5.6.1.2 Multi-family complexes

- 5.6.2 Commercial

- 5.6.2.1 Office buildings

- 5.6.2.2 Shopping malls and Retail centers

- 5.6.2.3 Hotels and Hospitality

- 5.6.2.4 Airports and Transportation hubs

- 5.6.2.5 Hospitals and Healthcare facilities

- 5.6.2.6 Universities and Education

- 5.6.3 Government and Municipal

- 5.6.4 Industrial and Logistics facilities

- 5.6.1 Residential

- 5.7 By Mode of Sales

- 5.7.1 New Installation

- 5.7.2 Retrofit

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Rest of North America

- 5.8.2 South America

- 5.8.2.1 Brazil

- 5.8.2.2 Argentina

- 5.8.2.3 Rest of South America

- 5.8.3 Europe

- 5.8.3.1 Germany

- 5.8.3.2 United Kingdom

- 5.8.3.3 France

- 5.8.3.4 Italy

- 5.8.3.5 Spain

- 5.8.3.6 Russia

- 5.8.3.7 Rest of Europe

- 5.8.4 Asia-Pacific

- 5.8.4.1 China

- 5.8.4.2 Japan

- 5.8.4.3 India

- 5.8.4.4 South Korea

- 5.8.4.5 Rest of Asia-Pacific

- 5.8.5 Middle East and Africa

- 5.8.5.1 Saudi Arabia

- 5.8.5.2 United Arab Emirates

- 5.8.5.3 Turkey

- 5.8.5.4 South Africa

- 5.8.5.5 Nigeria

- 5.8.5.6 Rest of Middle East and Africa

- 5.8.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Westfalia Parking

- 6.4.2 Wohr Parking

- 6.4.3 Klaus Multiparking

- 6.4.4 Lodige Industries

- 6.4.5 CityLift Parking

- 6.4.6 Parkmatic

- 6.4.7 Unitronics Corporation

- 6.4.8 ShinMaywa Industries

- 6.4.9 Robotic Parking Systems Inc.

- 6.4.10 ParkPlus Inc.

- 6.4.11 Boomerang Systems

- 6.4.12 Stanley Robotics (HL Robotics)

- 6.4.13 Hyundai Elevator Co., Ltd.

- 6.4.14 Valeo (Park4U)

- 6.4.15 TreviPark

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

自動停車系統市場:全球預測,2026-2032年

自動停車系統市場:全球預測,2026-2032年 自動停車系統市場預測至2034年-按自動化程度、組件、技術、停車類型、驅動系統、最終用戶和地區分類的全球分析自動轉向系統市場預測至2034年-按系統類型、車輛類型、自動駕駛等級、技術、最終使用者和地區分類的全球分析自動代客泊車可行性市場:未來預測(至2034年)-按車輛類型、停車基礎設施、技術、最終用戶和地區分類的全球分析

自動停車系統市場預測至2034年-按自動化程度、組件、技術、停車類型、驅動系統、最終用戶和地區分類的全球分析自動轉向系統市場預測至2034年-按系統類型、車輛類型、自動駕駛等級、技術、最終使用者和地區分類的全球分析自動代客泊車可行性市場:未來預測(至2034年)-按車輛類型、停車基礎設施、技術、最終用戶和地區分類的全球分析 2026年全球即時停車系統市場報告2026年全球自動停車系統市場報告垂直停車系統市場:按類型、技術、最終用戶、營運方式、車輛類型和容量分類,全球預測,2026-2032年垂直升降式多層車庫市場:按機制、容量、安裝方式、最終用戶和應用分類-2026-2032年全球預測

2026年全球即時停車系統市場報告2026年全球自動停車系統市場報告垂直停車系統市場:按類型、技術、最終用戶、營運方式、車輛類型和容量分類,全球預測,2026-2032年垂直升降式多層車庫市場:按機制、容量、安裝方式、最終用戶和應用分類-2026-2032年全球預測 全球自動停車系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球自動停車系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 自動停車系統市場 - 全球產業規模、佔有率、趨勢、機會及預測(按應用、自動化程度、組件、平台類型、結構類型、地區和競爭格局分類,2021-2031年)

自動停車系統市場 - 全球產業規模、佔有率、趨勢、機會及預測(按應用、自動化程度、組件、平台類型、結構類型、地區和競爭格局分類,2021-2031年)