|

市場調查報告書

商品編碼

2043872

混凝土攪拌機:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Concrete Mixer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

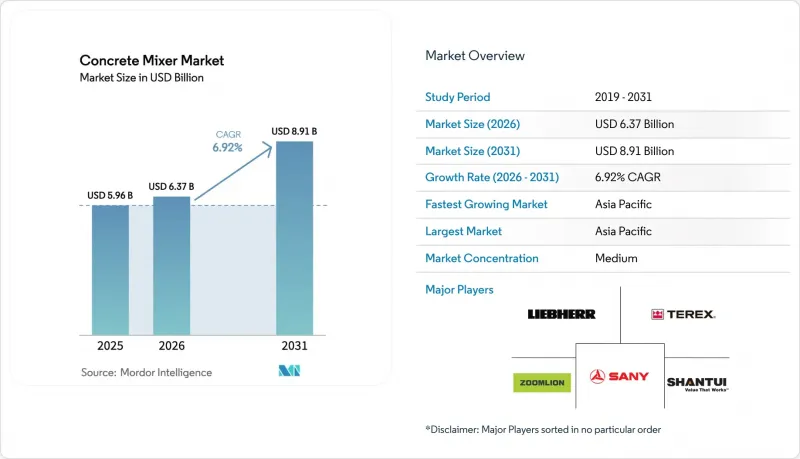

2025年混凝土攪拌機市值為59.6億美元,預計2031年將達到89.1億美元,而2026年為63.7億美元,預測期(2026-2031年)複合年成長率為6.92%。

亞太和中東地區蓬勃發展的公共工程項目、歐洲和北美日益嚴格的二氧化碳排放和噪音法規,以及租賃和「設備即服務 (EaaS)」合約模式的加速普及,正在重塑籌資策略。建築公司正在實現採購多元化,既採購用於大型企劃的大容量固定式設備,也採購用於都市區改造專案的可攜式電動設備;與此同時,加州和歐盟的車隊營運商正在柴油車輛折舊免稅額週期結束前將其淘汰。因此,大規模的基礎設施投資和強制性電氣化共同推動了對更大、更自動化、且擴大採用電池驅動的車型的需求。儘管競爭尚屬適中,但中國新進業者免費捆綁遠端資訊處理功能,正在擠壓老牌企業的利潤空間,迫使歐美原始設備製造商轉向能夠保證運作的訂閱模式。

全球混凝土攪拌機市場趨勢與洞察

大規模基礎設施投資激增(2026-2031年)

預計到2025年,全球各國政府將在基礎建設項目上投資2.3兆美元,其中亞太地區約佔已公佈項目的58%。光是印度的國家基礎建設計畫就計畫在2030年投入1.4兆美元的資本支出,優先建設需要持續供應混凝土的高速公路、地鐵和工業走廊。在沙烏地阿拉伯的特大城市“NEOM”和埃及的“新行政首都”,承包商正在以超過中東項目歷史平均水平的速度部署大容量固定式混凝土攪拌機,以盡量減少卡車前往偏遠沙漠建築工地的次數。據估計,每10億美元的基礎設施支出,大約需要120至150台混凝土攪拌機,具體數量取決於項目密度和混凝土攪拌站的距離。這種乘數效應在亞太地區最為顯著,該地區供應鏈中斷和預拌混凝土普及率低迫使建築商採用現場攪拌技術。因此,預計滾筒式和雙軸式機型的累積訂單將保持兩位數的成長,直到 2028 年。

自裝式和容積式攪拌機在偏遠地區迅速普及

自裝式和容積式攪拌機的年複合成長率高達16.52%,超過了傳統的滾筒式攪拌機。這是因為在偏遠礦區、風力發電廠地基和模組化住宅計畫中,固定式混凝土攪拌站的資本投資成本難以負擔。美國國家可再生能源實驗室 (NREL) 在2025年的一項研究發現,使用容積式攪拌機可以減少模組化建築工地的混凝土浪費,因為操作人員可以即時調整混凝土配比,以滿足結構規範的要求。在澳大利亞,力拓集團宣布將於2025年在其皮爾巴拉鐵礦石安裝47台自裝式攪拌機,與車載滾筒式攪拌機相比,混凝土交付前置作業時間將縮短22%。 2024年,英國運輸部審查了容積式攪拌機的重量限制。該部門提案將車輛總重限制提高到44噸,這將允許操作人員裝載更多骨材,進一步提高偏遠工地的經濟效益。此外,這些設備也獲得了拉丁美洲和撒哈拉以南非洲地區承包商的支持。在這些地區,道路基礎設施不足以容納大型預拌混凝土車,因此自主型攪拌站成為農村電氣化和灌溉工程的唯一實用選擇。

鋼材和零件價格的波動給OEM廠商的利潤率帶來了壓力。

根據經合組織鋼鐵委員會發布的2025年展望報告,2025年熱軋捲鋼均價將為每噸720美元,低於2022年每噸1150美元的尖峰時段,但仍比2019年的水平高出38%。混凝土攪拌機製造商通常在生產前6至9個月敲定鋼材契約,因此現貨價格飆升會對其利潤率造成壓力。中聯重科在2024年年度報告中揭露,原物料價格飆升導致其毛利率年減210個基點,迫使其在2025年初將產品標價上調4.5%。根據《工程新聞記錄》(Engineering News-Record)發布的2025年第三季成本報告,受半導體短缺和中國製造零件關稅增加的影響,2024年至2025年間,液壓元件、馬達和電控系統的價格上漲了12%至18%。根據國際貨幣基金組織(IMF)對2025年10月金屬價格的最新預測,電動車電池組和線束的關鍵材料鎳和銅的價格預計將在2027年之前持續高於長期平均水平25%,這將持續給零排放產品線帶來成本壓力。對沖能力有限的中小型原始設備製造商(OEM)最容易受到影響。為了避免簽訂不利的零件契約,一些歐洲製造商推遲了2025年新車的上市計劃,並將市場佔有率拱手讓給了生產自有鋼鐵和油壓設備的垂直整合型中國競爭對手。

細分市場分析

到2025年,滾筒式攪拌機將佔總銷量的58.16%,這反映了其在預拌混凝土(RMC)運輸領域的強勢地位,該領域優先考慮連續排放和高處理能力。隨著遠端經濟效益的推動,按需批量處理的需求日益成長,預計到2031年,自裝式和容積式混凝土攪拌機的市場規模將以16.52%的複合年成長率成長。在歐洲和日本,盤式和行星式攪拌機主要用於預製件和耐火材料等細分領域;而隨著中國和印度工業化建築需求的成長,雙臥軸攪拌機正迅速發展。澳洲和撒哈拉以南非洲地區對價格較為敏感的礦業公司擴大指定使用自裝式攪拌機以縮短運輸距離,這一趨勢正在削弱滾筒式攪拌機在這些地區的主導地位。

在預製構件生產中,雙軸攪拌機正穩步佔據市場,因為這些產業對混凝土的均勻性和快速的攪拌週期要求極高。行星式攪拌機仍然是石油化學和航太項目中超高強度混凝土的首選設備,這表明其長期需求穩定。盤式攪拌機則佔據著一個細分市場,在這個市場中,嚴格的品管比產量更為重要。因此,原始設備製造商(OEM)正在擴展其產品線,以涵蓋高產能的固定式攪拌站和高度移動的自裝式解決方案,旨在在項目類型日益多樣化的背景下保持市場佔有率。

2025年,容量在5立方公尺至10立方公尺之間的攪拌機佔出貨量的51.08%。此容量與大型卡車的標準負載容量限制以及物流倉庫、地鐵站和中層辦公大樓所需的混凝土批量大小相符。容量低於2立方公尺的攪拌機預計到2031年將以9.82%的複合年成長率成長,主要得益於DIY市場和郊區住宅熱潮對高移動性和低成本設備的青睞。容量超過10立方公尺的大型攪拌機則用於水壩、跑道和城市地基工程,這些工程需要最大容量的攪拌筒以減少連續混凝土澆築過程中的卡車運輸次數。

2立方米至5立方米容量的混凝土攪拌機市佔率正在萎縮。這是因為建築公司要么轉向高階機型以利用規模經濟,要么轉向低階機型以開拓維修工程等細分市場,導致容量偏好呈現啞鈴狀分佈。修訂後的ISO 18650標準統一了歐洲和美國的定義,簡化了跨境銷售,並使原始設備製造商(OEM)能夠更積極地在不同重量級別之間共用平台。

本「混凝土攪拌機市場報告」按產品類型(滾筒式、盤式、行星式、雙軸式)、容量(小於2立方米、2-10立方米、10立方米及以上)、應用領域(住宅、商業、其他)、型號類型(可攜式、固定式)、驅動系統(內燃機、電動)、操作方式(手動、其他)及其他地區(手法、固定式)及其他地區(南美、內燃機、電動)、操作方式(手動、其他)及其他地區(南美、固定式)及其他地區)。市場預測以美元計價。

區域分析

預計到2025年,亞太地區將佔全球銷售額的44.16%,並在2031年之前以6.18%的複合年成長率成長,這主要得益於中國地鐵項目和印度1.4兆美元的“Ghati Shakti”計劃。在中國成都和武漢等二線城市,2025年核准了18條新的地鐵線路,每條線路每月約需34萬立方公尺混凝土。在印度,主要道路沿線引入了自裝式混凝土攪拌車,以縮短運輸時間並緩解預拌混凝土供不應求。在日本,由於新建設放緩,混凝土出貨量下降了3.2%,但東京從2027年開始實施的柴油車限行政策加速了電動混凝土攪拌車的普及。在韓國,隨著預算轉向橋樑維修,對小型可攜式混凝土攪拌車的需求增加。

2025年,北美和歐洲合計佔總銷售額的38%。美國《基礎建設法案》撥款1,100億美元,確保攪拌機利用率在2026年之前維持在70%以上。在德國,利率上升導致產量下降1.8%,但電動攪拌機的銷量增加了42%,提前達到了2030年的二氧化碳排放上限目標。在英國,人手不足和海關摩擦迫使建築商轉向租賃可攜式攪拌機。在法國,「大巴黎快線」計畫提振了固定式攪拌機的訂單,而在義大利,歷史中心的抗震加固工程更傾向於使用可攜式攪拌機。西班牙沿海地區住宅建設的復甦導致人們更依賴租賃而非購買攪拌機。

南美洲和中東及非洲總合約佔總銷售額的18%。巴西一項價值240億美元的基礎設施開發項目提振了亞馬遜地區和東北部的銷售額,但電網的脆弱性限制了聖保羅以外地區電動攪拌機的普及。阿根廷的財政緊縮措施導致市場萎縮了7.2%。沙烏地阿拉伯的NEOM和埃及的新首都計畫於2025年安裝68台用於沙漠地區混凝土澆築的高容量攪拌機。儘管阿拉伯聯合大公國的住宅開工速度放緩,但憑藉2025年世博會的遺留項目,市場需求仍保持穩定。在南非,計畫內的停電打亂了我們的進度,阻礙了電池組的部署。土耳其由於地震重建和機場擴建,市場成長了9.4%,但外匯波動導致單位成本上漲了18%。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 大規模基礎設施投資激增(2026-2031年)

- 自裝式和容積式攪拌機在偏遠地區迅速普及

- 為因應二氧化碳排放法規,道路攪拌車電氣化進程正在進行中。

- 現場營運數位化(物聯網、遠端資訊處理、預測性維護)

- 租賃和「設備即服務 (EaaS)」經營模式的成長

- 先進安全和自動化技術的整合

- 市場限制因素

- 鋼材和零件價格的波動給OEM廠商的利潤率帶來了壓力。

- 新興市場電力短缺阻礙了全電動攪拌機的廣泛應用。

- 加強全球柴油桶裝貨車的噪音和排放法規

- 高昂的初始投資和維護成本限制了市場成長。

- 價值鏈/供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模及成長預測(價值(美元))

- 依產品類型

- 鼓式攪拌機

- 麵包攪拌機

- 行星攪拌機

- 雙軸攪拌機

- 按產能

- 小於 2 立方米

- 2~10 m3

- 10立方米或更多

- 透過使用

- 住宅

- 商業建築

- 基礎設施建設

- 道路和橋樑

- 其他

- 按型號

- 可攜式攪拌機

- 固定式攪拌機

- 按驅動類型

- 內燃機(ICE)

- 電的

- 透過駕駛模式

- 手動的

- 半自動

- 全自動

- 按地區

- 北美洲

- 美國

- 加拿大

- 南美洲

- 巴西

- 阿根廷

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 土耳其

- 北美洲

第6章 競爭情勢

- 公司簡介

- Liebherr Group

- SANY Group

- Zoomlion Heavy Industry Science & Technology Co. Ltd

- Schwing Stetter Group

- Shantui Construction Machinery Co. Ltd.

- AB Volvo

- KYB Corporation

- Caterpillar Inc.

- XCMG

- Terex Corp.

- CIFA SpA

- Putzmeister

- Sinotruk Hong Kong

- Tata Motors

- Aimix Group

- Altrad Belle

- Multiquip Inc.

- BHS-Sonthofen

- Speedcrafts Ltd.

- Crown Construction Equip.

第7章 市場機會與未來展望

The Concrete Mixer Market size was valued at USD 5.96 billion in 2025 and is estimated to grow from USD 6.37 billion in 2026 to reach USD 8.91 billion by 2031, at a CAGR of 6.92% during the forecast period (2026-2031).

Strong public-works pipelines in Asia-Pacific and the Middle East, stricter CO2 and noise regulations in Europe and North America, and the accelerating pivot to rental and equipment-as-a-service contracts are reshaping procurement strategies. Contractors are splitting purchases between high-capacity stationary plants for mega-projects and portable electric units for urban infill sites, while fleet operators in California and the EU are advancing diesel retirements ahead of depreciation cycles. Twin forces, mega-infrastructure spending and electrification mandates, are therefore nudging demand toward larger, automated, and increasingly battery-powered models. Competitive intensity is moderate, yet Chinese entrants that bundle telematics at zero cost are pressuring incumbent margins, pushing European and U.S. OEMs to pivot toward subscription models with guaranteed uptime.

Global Concrete Mixer Market Trends and Insights

Surge in Mega-Infrastructure Spending (2026-2031)

Governments worldwide committed USD 2.3 trillion to infrastructure projects in 2025, with Asia-Pacific accounting for approximately 58% of the announced pipeline value. India's National Infrastructure Pipeline alone targets USD 1.4 trillion in capital outlays through 2030, prioritizing highways, metro rail, and industrial corridors that require continuous concrete supply. Saudi Arabia's NEOM megacity and Egypt's New Administrative Capital are absorbing high-capacity stationary mixers at rates that exceed historical norms for Middle Eastern projects, as contractors seek to minimize truck cycles on remote desert sites. Estimates suggest that every USD 1 billion in infrastructure spending generates demand for approximately 120 to 150 concrete mixer units, depending on project density and the proximity of batching plants. This multiplier effect is most pronounced in Asia-Pacific, where fragmented supply chains and limited ready-mix penetration compel contractors to deploy on-site mixing capacity, thereby sustaining double-digit order books for drum and twin-shaft models through 2028.

Rapid Adoption of Self-Loading and Volumetric Mixers on Remote Sites

Self-loading and volumetric mixers are expanding at 16.52% CAGR, outpacing traditional drum units, because remote mining camps, wind-farm foundations, and modular housing projects cannot justify the capital cost of fixed batching plants. A 2025 study by the National Renewable Energy Laboratory found that modular construction sites reduce concrete waste when using volumetric mixers, as operators can adjust mix designs in real time to match structural specifications. In Australia, Rio Tinto deployed 47 self-loading units across its Pilbara iron-ore operations in 2025, citing a 22% reduction in concrete delivery lead times compared to truck-mounted drum mixers. The UK Department for Transport reviewed volumetric mixer weight limits in 2024. It proposed increasing the weight limit to 44 tons gross vehicle weight, allowing operators to carry larger aggregate payloads and further enhancing the economics of remote sites. These units also appeal to contractors in Latin America and Sub-Saharan Africa, where road infrastructure is inadequate for heavy ready-mix trucks, making self-contained batching the only viable option for rural electrification and irrigation projects.

Steel and Component Price Volatility Squeezing OEM Margins

Hot-rolled coil steel prices averaged USD 720 per tonne in 2025, down from the 2022 peak of USD 1,150 but still 38% above 2019 levels, according to the OECD Steel Committee's 2025 outlook. Concrete-mixer manufacturers typically lock in steel contracts 6 to 9 months ahead of production, exposing them to margin compression when spot prices spike; Zoomlion disclosed in its 2024 annual report that raw-material inflation eroded gross margin by 210 basis points year-over-year, forcing the company to raise list prices by 4.5% in early 2025. Engineering News-Record's Q3 2025 cost report noted that hydraulic components, electric motors, and electronic control units saw price increases of 12% to 18% in 2024-2025, driven by semiconductor shortages and tariff escalations on Chinese-manufactured parts. The International Monetary Fund's October 2025 metals-price update projects that nickel and copper-critical inputs for electric-mixer battery packs and wiring harnesses-will remain 25% above long-term averages through 2027, sustaining cost pressure on zero-emission product lines. Smaller OEMs with limited hedging capacity are most vulnerable: several European manufacturers delayed new-model launches in 2025 to avoid locking in unfavorable component contracts, ceding market share to vertically integrated Chinese competitors that produce steel and hydraulics in-house.

Other drivers and restraints analyzed in the detailed report include:

- Electrification of On-Road Mixer Fleets Amid CO2 Regulations

- Job-Site Digitalization (IoT, Telematics, and Predictive Maintenance)

- Grid-Power Scarcity Limiting Uptake of Full-Electric Mixers In Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Drum mixers delivered 58.16% of 2025 revenue, reflecting entrenched positions in ready-mix fleets that value continuous discharge and high throughput. The concrete mixer market size for self-loading and volumetric units is projected to expand at a 16.52% CAGR through 2031 as remote-site economics reward on-demand batching. Pan and planetary variants serve niche precast and refractory segments in Europe and Japan, while twin-shaft designs are gaining momentum in China and India's industrialized construction drive. Price-sensitive mining operators in Australia and Sub-Saharan Africa increasingly specify self-loading models to slash haul distances, a pivot that is eroding drum dominance in those geographies.

Twin-shaft mixers are securing a foothold in precast factories that prioritize homogeneity and rapid cycle times. Planetary types remain favored for ultra-high-performance concrete in petrochemical and aerospace projects, suggesting long-cycle, stable demand. Pan mixers occupy a niche where strict quality control trumps output volume. Consequently, OEMs are broadening portfolios to straddle both high-capacity stationary plants and agile self-loading solutions, aiming to retain wallet share as project profiles splinter.

Mixers rated 5 m3 to 10 m3 accounted for 51.08% of 2025 shipments, aligning with standard heavy-truck payload limits and the batch sizes required for logistics warehouses, metro stations, and mid-rise offices. Sub-2 m3 units are growing at a 9.82% CAGR through 2031 as the do-it-yourself segment and suburban housing boom favor maneuverable, lower-cost gear. Above-10 m3 giants serve dams, runways, and megacity foundations where continuous pours demand maximum drum capacity to cut truck cycles.

The concrete mixer market share for the 2 m3 to 5 m3 band is eroding as contractors either trade up to exploit economies of scale or trade down to tap renovation niches, creating a barbell distribution in capacity preferences. Revised ISO 18650 metrics now align European and U.S. definitions, simplifying cross-border sales and enabling OEMs to platform-share more aggressively across weight classes.

The Concrete Mixer Market Report is Segmented by Product Type (Drum, Pan, Planetary, and Twin-Shaft), Capacity (Below 2 M3, 2-10 M3, and Above 10 M3), Application (Residential, Commercial, and Others), Model Type (Portable and Stationary), Drive Type (ICE and Electric), Operating Mode (Manual and More), and Geography (North America, South America, and More). Market Forecasts are Provided in Value (USD).

Geography Analysis

Asia-Pacific contributed 44.16% of 2025 revenue and is set for a 6.18% CAGR to 2031, driven by China's metro tie-ups and India's USD 1.4 trillion Gati Shakti program. Chinese tier-2 cities such as Chengdu and Wuhan approved 18 new metro lines in 2025, each requiring roughly 340,000 m3 of concrete per month. India added self-loading mixers along highway corridors to curb haul times and mitigate ready-mix undersupply. Japan's shipments dipped 3.2% as new builds slowed, yet electric uptake rose due to Tokyo's diesel exclusion zone, which began in 2027. South Korea shifted its budget to bridge rehab, elevating demand for compact portable units.

North America and Europe jointly delivered 38% of 2025 sales. The U.S. Infrastructure Act's USD 110 billion allocation sustains mixer utilization above 70% through 2026. Germany's output slipped 1.8% under higher interest rates, but electric mixer sales grew 42% as fleets pre-complied with 2030 CO2 caps. The UK faced labor shortages and customs friction, nudging contractors toward portable rentals. France's Grand Paris Express buoyed stationary mixer orders, while Italy's seismic retrofits favored portable solutions for historic cores. Spain's coastal housing revival relied heavily on rental fleets rather than outright purchases.

South America, the Middle East, and Africa together held roughly 18% of revenue. Brazil's USD 24 billion infrastructure push buttressed sales in the Amazon and Northeast, yet grid weaknesses limited electric penetration outside Sao Paulo. Argentina's austerity led to a 7.2% contraction in the market. Saudi Arabia's NEOM and Egypt's New Capital absorbed 68 high-capacity mixers in 2025 for desert pours. The UAE leveraged Expo 2025 legacy projects to sustain demand despite softer residential starts. South Africa's load-shedding episodes disrupted our schedules, hurting the adoption of battery units. Turkey rebounded 9.4% on earthquake reconstruction and airport expansion, though currency volatility raised unit costs by 18%.

- Liebherr Group

- SANY Group

- Zoomlion Heavy Industry Science & Technology Co. Ltd

- Schwing Stetter Group

- Shantui Construction Machinery Co. Ltd.

- AB Volvo

- KYB Corporation

- Caterpillar Inc.

- XCMG

- Terex Corp.

- CIFA S.p.A.

- Putzmeister

- Sinotruk Hong Kong

- Tata Motors

- Aimix Group

- Altrad Belle

- Multiquip Inc.

- BHS-Sonthofen

- Speedcrafts Ltd.

- Crown Construction Equip.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Mega-Infrastructure Spending (2026-2031)

- 4.2.2 Rapid Adoption of Self-Loading and Volumetric Mixers on Remote Sites

- 4.2.3 Electrification of On-Road Mixer Fleets Amid CO2 Regulations

- 4.2.4 Job-Site Digitalization (IoT, Telematics and Predictive Maintenance)

- 4.2.5 Growth of Rental and "Equipment-As-a-Service" Business Models

- 4.2.6 Integration of Advanced Safety and Automation Technologies

- 4.3 Market Restraints

- 4.3.1 Steel and Component Price Volatility Squeezing OEM Margins

- 4.3.2 Grid-Power Scarcity Limiting Uptake of Full-Electric Mixers in Emerging Markets

- 4.3.3 Tightening Global Noise-Emission Limits For Diesel Drum Trucks

- 4.3.4 High Initial Investment And Maintenance Costs Restricting Market Growth

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power - Suppliers

- 4.7.2 Bargaining Power - Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Product Type

- 5.1.1 Drum Mixers

- 5.1.2 Pan Mixers

- 5.1.3 Planetary Mixers

- 5.1.4 Twin-Shaft Mixers

- 5.2 By Capacity

- 5.2.1 Below 2 m3

- 5.2.2 2 - 10 m3

- 5.2.3 Above 10 m3

- 5.3 By Application

- 5.3.1 Residential Construction

- 5.3.2 Commercial Construction

- 5.3.3 Infrastructure Development

- 5.3.4 Roads and Bridges

- 5.3.5 Others

- 5.4 By Model Type

- 5.4.1 Portable Mixers

- 5.4.2 Stationary Mixers

- 5.5 By Drive Type

- 5.5.1 Internal-Combustion Engine (ICE)

- 5.5.2 Electric

- 5.6 By Operating Mode

- 5.6.1 Manual

- 5.6.2 Semi-Automatic

- 5.6.3 Fully-Automatic

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.5 Middle East and Africa

- 5.7.5.1 United Arab Emirates

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 South Africa

- 5.7.5.4 Turkey

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Company Profiles

- 6.1.1 Liebherr Group

- 6.1.2 SANY Group

- 6.1.3 Zoomlion Heavy Industry Science & Technology Co. Ltd

- 6.1.4 Schwing Stetter Group

- 6.1.5 Shantui Construction Machinery Co. Ltd.

- 6.1.6 AB Volvo

- 6.1.7 KYB Corporation

- 6.1.8 Caterpillar Inc.

- 6.1.9 XCMG

- 6.1.10 Terex Corp.

- 6.1.11 CIFA S.p.A.

- 6.1.12 Putzmeister

- 6.1.13 Sinotruk Hong Kong

- 6.1.14 Tata Motors

- 6.1.15 Aimix Group

- 6.1.16 Altrad Belle

- 6.1.17 Multiquip Inc.

- 6.1.18 BHS-Sonthofen

- 6.1.19 Speedcrafts Ltd.

- 6.1.20 Crown Construction Equip.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

坍落度試驗設備市場預測至2034年-按類型、應用和地區分類的全球分析

坍落度試驗設備市場預測至2034年-按類型、應用和地區分類的全球分析 水泥攪拌機市場:按類型、運作模式和應用分類-2026-2032年全球市場預測混凝土攪拌機市場:全球市場按產品類型、類別、馬達類型、應用和分銷管道分類的預測,2026-2032年自走式混合貨車市場:按類型、容量、自動化程度、動力來源、應用和分銷管道分類,全球預測,2026-2032年雙臥軸混凝土攪拌機市場:依產品類型、動力來源、移動性、攪拌容量、應用、終端用戶產業分類,全球預測(2026-2032)

水泥攪拌機市場:按類型、運作模式和應用分類-2026-2032年全球市場預測混凝土攪拌機市場:全球市場按產品類型、類別、馬達類型、應用和分銷管道分類的預測,2026-2032年自走式混合貨車市場:按類型、容量、自動化程度、動力來源、應用和分銷管道分類,全球預測,2026-2032年雙臥軸混凝土攪拌機市場:依產品類型、動力來源、移動性、攪拌容量、應用、終端用戶產業分類,全球預測(2026-2032) 水泥攪拌機市場報告:按產品類型、最終用戶和地區分類(2026-2034 年)

水泥攪拌機市場報告:按產品類型、最終用戶和地區分類(2026-2034 年) 全球混凝土攪拌機市場規模、佔有率、趨勢和成長分析報告:2026-2034年

全球混凝土攪拌機市場規模、佔有率、趨勢和成長分析報告:2026-2034年 全球水泥攪拌機市場:按應用、最終用戶、產品類型、移動性、國家和地區分類-產業分析、市場規模、市場佔有率及2025-2032年未來預測

全球水泥攪拌機市場:按應用、最終用戶、產品類型、移動性、國家和地區分類-產業分析、市場規模、市場佔有率及2025-2032年未來預測 車載混凝土攪拌機市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、安裝車輛、攪拌能力、地區和競爭格局分類,2021-2031年

車載混凝土攪拌機市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、安裝車輛、攪拌能力、地區和競爭格局分類,2021-2031年 全球混凝土攪拌機市場(2026-2030 年)

全球混凝土攪拌機市場(2026-2030 年)