|

市場調查報告書

商品編碼

2043870

軟性彈性發泡橡膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Flexible Elastomeric Foam - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

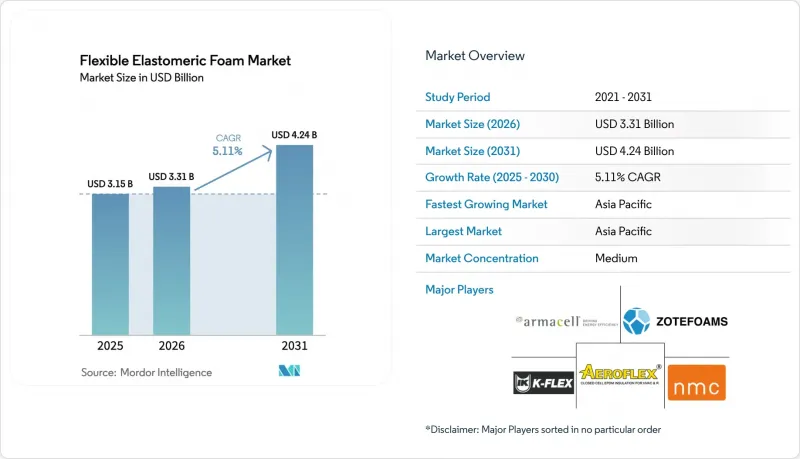

2025年,軟性彈性發泡橡膠市場價值為31.5億美元,預計到2031年將達到42.4億美元,而2026年為33.1億美元,預測期內(2026-2031年)複合年成長率為5.11%。

在亞太地區,日益嚴格的建築節能法規、暖通空調(HVAC)和冷凍系統的持續維修以及低溫運輸專案的快速擴張,都在推高基礎需求。隨著監管機構逐步淘汰高全球暖化潛勢(GWP)冷媒,設備現代化進程比預期更快。從R-410A到高壓R-32和R-454B冷卻器的過渡需要更厚、滲透性更低的管道隔熱材料。這種轉變顯著擴大了軟性彈性發泡橡膠的市場。此外,由於丁二烯和氯丁橡膠供應鏈面臨壓力,加工商正在加速向三元乙丙橡膠(EPDM)轉型。這種轉變不僅使材料成分多樣化,也推動了阻燃、無鹵化和低碳泡沫材料的創新。供應商重新採用氣凝膠、生質能平衡和超臨界二氧化碳發泡技術,正在獲得競爭優勢,尤其是在客戶要求其產品提供減少碳排放的證據的情況下。

全球軟性彈性發泡橡膠市場趨勢及洞察

暖通空調和冷凍系統的維修活動增加。

由於面臨強制性的洩漏維修和淘汰期限,商用暖通空調系統業主選擇比預期更早更換整個系統。隨著產業從R-410A過渡到R-32和R-454B,排氣壓力飆升。閉孔彈性體泡棉是少數幾種能夠應對這種日益增加的冷凝風險的隔熱材料之一。中國各省為加速向R-290過渡而提供的補貼,以及歐洲各地公共建築類似過渡的獎勵,進一步刺激了對這種隔熱材料的需求。阿姆斯壯的先進保溫材料部門也支持這一趨勢,其強勁的銷售成長凸顯了維修需求的影響。超級市場正在轉向二氧化碳跨臨界貨架,現在正在尋找能夠承受低至-40 度C溫度的泡沫材料,將其產品選擇範圍從NBR/PVC擴展到EPDM和氯丁橡膠。

落實分階段減少氟化氣體排放的最後期限。

歐盟計畫在2030年前逐步減少氫氟碳化合物(HFC)的配額,並在2027年和2029年設定了關鍵里程碑。此舉正在加速冷卻器的更換週期。建築業主面臨兩種選擇:要麼進行簡易維修(但仍需更換隔熱材料) ,要麼改用天然冷媒系統(需要更厚的隔熱材料)。這兩種選擇都導致短期採購需求激增。同樣,日本加速實施《基加利協定》以及韓國強制回收冷媒的政策也反映了這一趨勢,至少在2027年之前就已經出現需求高峰。歐盟各地的經銷商報告稱,軟性彈性發泡橡膠市場的訂單已訂單至六個月後,這表明2026年供應可能趨緊。

丁二烯和氯丁橡膠原料價格的波動

到了2025年初,亞太地區蒸汽裂解裝置的關閉以及石腦油價格的上漲,顯著推高丁二烯的現貨價格,直接影響了丁腈橡膠(NBR)的成本曲線。同時,杜邦公司拉普拉斯工廠的關閉導致全球氯丁橡膠供應趨緊,北美地區價格急劇上漲。由於利潤空間縮小,許多加工商轉而使用乙烯和丙烯供應更穩定的三元乙丙橡膠(EPDM)。雖然這種轉變有助於避免價格上漲,但需要與終端用戶進行相容性測試,並且會暫時延長出貨週期。

細分市場分析

2025年,隔熱保溫應用將佔總需求的75.22%,預計在2026年至2031年的預測期內將以5.29%的複合年成長率成長。這項成長主要受電動車電池外殼和鐵路車輛(需在500赫茲至2千赫茲範圍內進行減振)需求成長的驅動。美國和歐洲能源標準強制要求覆蓋材料,從而支撐了軟性彈性發泡橡膠在隔熱保溫應用領域的市場佔有率。相較之下,隔音應用更受到「能源與環境設計先鋒獎(LEED)」認證和租戶期望等自願性因素的影響。

隔熱應用也受益於冷媒的轉變,因為冷媒需要更厚的隔熱材料。同時,隨著企業在不犧牲柔軟性的前提下優先考慮隔音性能,聲學領域也獲得了優勢。由於電動車平台的擴展以及資料中心泵帶來的新的振動挑戰,聲學泡沫材料預計將會成長。然而,預計到2031年,隔熱應用在絕對銷售額方面仍將保持領先地位。

區域分析

2025年,亞太地區佔總銷售額的45.25%。隨著印度冷藏保管能力翻番,以及中國大規模推進暖通空調維修項目,預計該地區在2026年至2031年的預測期內將維持7.09%的強勁複合年成長率。阿姆斯壯已在浦那新建了一家氣凝膠生產廠,而華美等當地企業則透過利用在地採購和遵守行業標準來最佳化營運。

在北美,市場成長主要受2026年1月生效的洩漏修復法規以及加州和紐約州嚴格的建築圍護結構標準的推動。因此,分銷商正抓住領先採購機會,並將訂單積壓量擴大到2026年下半年。歐洲市場的成長則得益於氟化氣體的逐步減少,加速了冷卻器和熱泵的更換。為了應對高昂的人事費用,市場擴大採用瓶坯管段以縮短安裝時間,Hira Industries和K-Flex等公司正在積極應對這一趨勢。

南美、中東和非洲雖然在全球整體銷售額中所佔比例較小,但正經歷兩位數的成長。這種快速成長主要得益於高溫地區(氣溫超過攝氏45度)對醫藥物流和食品配送的需求。此外,日本和韓國正在推行冷媒回收政策,並計劃在2027年前禁止進口新的R-410A冷媒,預計將改變市場格局。這些措施可望推動東北亞走上類似歐洲的快速成長軌道,並確保即使建築業成長放緩,該地區的經濟活力也能得以維持。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 暖通空調和冷凍系統的維修活動增加。

- 落實分階段減少氟化氣體排放的最後期限。

- 加強建築物的能源效率法規

- 低溫運輸基礎設施快速擴張,協助最後一公里生鮮配送

- 提高高溫泡沫在太陽能集熱器的應用

- 市場限制因素

- 丁二烯和氯丁橡膠原料價格的波動

- 含鹵添加劑的防火安全法規

- 與 PFAS 相關的發泡供應風險

- 價值鏈分析

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按功能

- 隔熱材料

- 隔音和聲阻

- 按類型

- 天然橡膠/乳膠

- 丁腈橡膠/聚氯乙烯

- 乙烯丙烯二烯單體

- 氯丁二烯

- 其他類型(ECO、SBR 等)

- 透過使用

- HVAC

- 車

- 運輸

- 太陽能發電設備

- 冷凍系統

- 其他用途(醫療保健設備等)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Aeroflex USA, Inc.

- Armacell International SA

- BASF

- DuPont

- Era Polymers Pty Ltd

- Hira Industries LLC

- Huamei Energy-saving Technology Group Co., Ltd.

- Intec Foams Ltd

- Jinan Retek Industries Inc.

- Johns Manville(Berkshire Hathaway)

- Kingwell World Industries Inc.

- L'Isolante K-FLEX SpA

- NMC SA

- Owens Corning

- Rogers Corporation

- Rubberlite, Inc.

- Saint-Gobain

- Sekisui Chemical Co., Ltd.

- Trelleborg AB

- Zotefoams plc

第7章 市場機會與未來展望

The Flexible Elastomeric Foam Market size was valued at USD 3.15 billion in 2025 and is estimated to grow from USD 3.31 billion in 2026 to reach USD 4.24 billion by 2031, at a CAGR of 5.11% during the forecast period (2026-2031).

In the Asia-Pacific region, a surge in building-energy regulations, ongoing retrofits in HVAC and refrigeration, and a swift expansion of cold-chain projects are collectively driving up baseline demand. As regulators phase down high-GWP refrigerants, equipment replacements are occurring sooner than anticipated. Each transition from R-410A to the higher-pressure R-32 or R-454B chillers requires thicker, lower-permeability pipe insulation. This shift is significantly expanding the market for flexible elastomeric foam. Additionally, with supply-chain pressures on butadiene and neoprene, converters are increasingly turning to EPDM. This shift not only diversifies the material mix but also drives innovation in fire-safe, halogen-free, and low-carbon foams. Suppliers that integrate back into aerogel, biomass-balance, and super-critical CO2 foaming are gaining a competitive edge, especially as customers demand evidence of embodied-carbon reduction.

Global Flexible Elastomeric Foam Market Trends and Insights

Increasing Retrofitting Activities in HVAC and Refrigeration Systems

Owners of commercial HVAC equipment, facing mandatory deadlines for leak repairs or phase-outs, are opting to replace entire systems sooner than anticipated. As the industry transitions from R-410A to R-32 and R-454B, discharge pressures have surged. Closed-cell elastomeric foam stands out as one of the few insulation materials capable of managing this increased condensation risk. The demand for this insulation is further bolstered by provincial subsidies in China promoting R-290 conversions, along with incentives for such transitions in public-sector buildings across Europe. Armacell's Advanced Insulation division, which underscores this trend, reported robust revenue growth, highlighting the impact of retrofit-driven demand. Supermarkets making the switch to CO2 transcritical racks are now procuring foam rated for temperatures as low as -40°C, broadening their product selection from NBR/PVC to also encompass EPDM and chloroprene.

Implementation of F-Gas Phase-Down Compliance Deadlines

By 2030, the European Union is set to reduce its HFC quotas, with key checkpoints in 2027 and 2029. This move is hastening chiller-replacement cycles. Building owners face a choice: retrofit with drop-ins that still necessitate new insulation or transition to natural-refrigerant systems, which require a thicker wrap. Both options are driving a surge in near-term procurement. Similarly, Japan's expedited Kigali timeline and South Korea's enforced refrigerant reclamation are echoing this trend, pulling demand forward at least until 2027. Distributors throughout the EU are noting that orders for products in the flexible elastomeric foam market are booked out for six months, signaling a likely tight supply in 2026.

Butadiene and Neoprene Feedstock Volatility

By early 2025, steam-cracker outages and rising naphtha costs significantly increased butadiene spot prices in the Asia-Pacific, directly influencing NBR cost curves. At the same time, a shutdown at DuPont's LaPlace facility tightened the global neoprene supply, leading to a surge in North American prices. As margins narrowed, many converters shifted to EPDM, benefiting from its more stable ethylene and propylene streams. While this transition helps avoid price surges, it requires qualification testing with end users, temporarily delaying shipment cycles.

Other drivers and restraints analyzed in the detailed report include:

- Tightening Building Energy-Efficiency Regulations

- Rapid Growth of Cold-Chain Infrastructure for Last-Mile Grocery Delivery

- Fire-Safety Bans on Halogenated Additives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, thermal insulation accounted for 75.22% of the demand and is projected to grow at a CAGR of 5.29% during the forecast period of 2026-2031. This growth is primarily driven by the increasing demand for electric-vehicle battery housings and rail rolling stock, which require vibration dampening in the 500 Hz to 2 kHz range. The market share of flexible elastomeric foam in thermal applications is supported by a mandatory wrap requirement, as stipulated by U.S. and European energy codes. In contrast, its use in acoustic applications is influenced more by voluntary Leadership in Energy and Environmental Design (LEED) credits and tenant expectations.

Thermal applications are also benefiting from refrigerant transitions that necessitate thicker insulation. Meanwhile, the acoustic segment gains an advantage as companies emphasize sound transmission loss without compromising flexibility. With the expansion of electric vehicle platforms and emerging vibration challenges from data-center pumps, acoustic foam is poised for growth. However, thermal insulation is expected to maintain its lead in absolute revenues through 2031.

The Flexible Elastomeric Foam Market Report is Segmented by Function (Thermal Insulation, and Acoustic Insulation), Type (Natural Rubber/Latex, Nitrile Butadiene Rubber/Polyvinyl Chloride, Ethylene Propylene Diene Monomer, and More), Application (HVAC, Automotive, Transportation, and More), and Geography (Asia-Pacific, North America, Europe, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, the Asia-Pacific region accounted for 45.25% of total revenue. With India doubling its cold-storage capacity and China rolling out an extensive HVAC retrofit pipeline, the region is poised for a robust 7.09% CAGR during the forecast period of 2026-2031. Armacell has set up a new aerogel facility in Pune, while local players such as Huamei are optimizing their operations by leveraging localized supplies and aligning with industry codes.

In North America, leak-repair regulations that came into effect in January 2026, coupled with stringent envelope codes in California and New York, are driving the market. Consequently, distributors have bolstered their order books into late 2026, capitalizing on pre-buying opportunities. Europe's market growth is spurred by the F-Gas phase-down, which is accelerating the replacement of chillers and heat pumps. In response to high labor costs, markets are increasingly adopting pre-formed pipe sections to reduce installation time, a trend addressed by companies such as Hira Industries and K-Flex.

Although South America and the Middle-East and Africa hold a smaller share of global revenue, they are experiencing double-digit growth. This surge is largely fueled by the demands of pharmaceutical logistics and grocery deliveries in regions grappling with sweltering temperatures surpassing 45 degrees Celsius. Additionally, policy moves in Japan and South Korea are set to reshape the landscape by aiming to reclaim refrigerants and banning the import of virgin R-410A by 2027. Such initiatives position Northeast Asia on a rapid growth trajectory, mirroring Europe's ascent, ensuring the region remains buoyant even as the construction sector cools.

- Aeroflex USA, Inc.

- Armacell International S.A.

- BASF

- DuPont

- Era Polymers Pty Ltd

- Hira Industries LLC

- Huamei Energy-saving Technology Group Co., Ltd.

- Intec Foams Ltd

- Jinan Retek Industries Inc.

- Johns Manville (Berkshire Hathaway)

- Kingwell World Industries Inc.

- L'Isolante K-FLEX S.p.A.

- NMC SA

- Owens Corning

- Rogers Corporation

- Rubberlite, Inc.

- Saint-Gobain

- Sekisui Chemical Co., Ltd.

- Trelleborg AB

- Zotefoams plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing retrofitting activities in HVAC and refrigeration systems

- 4.2.2 Implementation of F-Gas phase-down compliance deadlines

- 4.2.3 Tightening building energy-efficiency regulations

- 4.2.4 Rapid growth of cold-chain infrastructure for last-mile grocery delivery

- 4.2.5 Rising adoption of high-temperature foam in solar-thermal collectors

- 4.3 Market Restraints

- 4.3.1 Butadiene and neoprene feedstock volatility

- 4.3.2 Fire-safety bans on halogenated additives

- 4.3.3 PFAS-linked blowing-agent supply risk

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Function

- 5.1.1 Thermal Insulation

- 5.1.2 Acoustic Insulation

- 5.2 By Type

- 5.2.1 Natural Rubber/Latex

- 5.2.2 Nitrile Butadiene Rubber/Polyvinyl Chloride

- 5.2.3 Ethylene Propylene Diene Monomer

- 5.2.4 Chloroprene

- 5.2.5 Other Types (ECO, SBR, etc.)

- 5.3 By Application

- 5.3.1 HVAC

- 5.3.2 Automotive

- 5.3.3 Transportation

- 5.3.4 Solar Installations

- 5.3.5 Refrigeration Systems

- 5.3.6 Other Applications (Medical and Healthcare Devices, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Aeroflex USA, Inc.

- 6.4.2 Armacell International S.A.

- 6.4.3 BASF

- 6.4.4 DuPont

- 6.4.5 Era Polymers Pty Ltd

- 6.4.6 Hira Industries LLC

- 6.4.7 Huamei Energy-saving Technology Group Co., Ltd.

- 6.4.8 Intec Foams Ltd

- 6.4.9 Jinan Retek Industries Inc.

- 6.4.10 Johns Manville (Berkshire Hathaway)

- 6.4.11 Kingwell World Industries Inc.

- 6.4.12 L'Isolante K-FLEX S.p.A.

- 6.4.13 NMC SA

- 6.4.14 Owens Corning

- 6.4.15 Rogers Corporation

- 6.4.16 Rubberlite, Inc.

- 6.4.17 Saint-Gobain

- 6.4.18 Sekisui Chemical Co., Ltd.

- 6.4.19 Trelleborg AB

- 6.4.20 Zotefoams plc

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Flexible elastomeric foam adoption in hyperscale data-centres

異戊二烯橡膠市場-全球產業規模、佔有率、趨勢、機會、預測:銷售管道、最終用途、地區和競爭格局(2021-2031年)

異戊二烯橡膠市場-全球產業規模、佔有率、趨勢、機會、預測:銷售管道、最終用途、地區和競爭格局(2021-2031年) 柔軟性彈性體泡棉市場:依產品類型、形狀和應用分類-2026-2032年全球市場預測彈性體泡棉市場:2026-2030年全球市場預測(依彈性體類型、形態、泡孔結構、應用、終端用戶產業及銷售管道)

柔軟性彈性體泡棉市場:依產品類型、形狀和應用分類-2026-2032年全球市場預測彈性體泡棉市場:2026-2030年全球市場預測(依彈性體類型、形態、泡孔結構、應用、終端用戶產業及銷售管道) 全球彈性體泡沫市場規模、佔有率、趨勢和成長分析報告(2026-2034)EPDM海綿墊片市場:依應用產業、形狀、硬度等級、顏色和通路-2026-2032年全球預測

全球彈性體泡沫市場規模、佔有率、趨勢和成長分析報告(2026-2034)EPDM海綿墊片市場:依應用產業、形狀、硬度等級、顏色和通路-2026-2032年全球預測 全球軟質合成橡膠泡棉市場:按類型、按功能、按最終用途行業、按地區 - 預測至 2029 年

全球軟質合成橡膠泡棉市場:按類型、按功能、按最終用途行業、按地區 - 預測至 2029 年 異戊二烯橡膠的全球市場 (2015-2032年):工廠生產能力、生產量、運作效率、供需數量、終端用戶產業、銷售管道、地區需求、國際貿易、企業佔有率

異戊二烯橡膠的全球市場 (2015-2032年):工廠生產能力、生產量、運作效率、供需數量、終端用戶產業、銷售管道、地區需求、國際貿易、企業佔有率