|

市場調查報告書

商品編碼

2043862

美國工具機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)United States Machine Tools - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

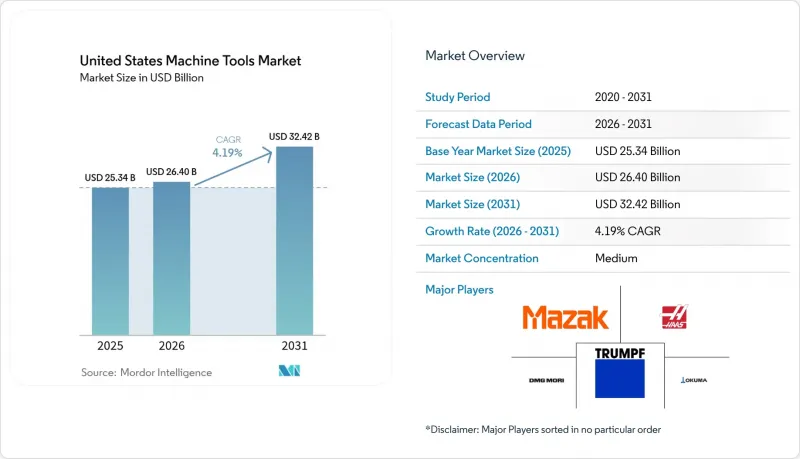

2025年美國工具機市場價值為253.4億美元,預計到2031年將達到324.2億美元,而2026年為264億美元,預測期(2026-2031年)複合年成長率為4.19%。

聯邦法律,例如《基礎設施投資與就業法案》、《晶片與科學法案》和《通貨膨脹控制法案》,已經核准了超過2兆美元的支出。預計2021年至2024年間,製造業建設支出將增加一倍,半導體、電池和國防領域對精密設備的需求也將激增。供應商正積極回應,推出人工智慧驅動的改裝套件,可將生產週期縮短高達12%,並協助買家在政策利率持續緩慢下調的情況下,證明資本投資的合理性。預計到2024年,熟練技工的薪資將比工廠平均薪資高出1.8個百分點,這使得自動化以節省勞動力變得更加迫切,但高昂的資金籌措成本也導致投資回收期延長。原物料價格的波動進一步加劇了這一局面。預計到 2025 年初,碳化鎢的價格將逐年上漲 22%,迫使 OEM 廠商修改其刀柄配置或推廣固定價格服務契約,以穩定其利潤率。

美國工具機市場趨勢與洞察

IRA、CHIPS 和 IIJA 等機構採取的資本投資獎勵策略

聯邦獎勵加速了原本需要十年才能完成的資本投資,使其縮短至三年。半導體和電池產業叢集訂購了先進的研磨、電火花加工中心以及能夠加工晶圓和電極的五軸加工中心。雖然最初的支出高峰出現在2024-2025年,但那些將付款條件與津貼里程碑掛鉤的供應商預計將在獲得額外私人資金之前保持其市場佔有率。供不應求,尤其是在電池隔膜和箔材方面,這可能會減緩2027年以後的工具機訂單。成功的關鍵在於使產品藍圖與《晶片和電池創新法案》(CHIPS Act)下剩餘的資金分配保持一致。

電動車和電池超級工廠對精密工具機的需求

超級工廠一直在活性化銷售雷射焊接機和高速壓力機,但由於現場加工需求低於預期,通用車床和銑床的訂單受到抑制。汽車製造商仍然保持謹慎,將內部電池生產與透過合資企業簽訂的供應合約進行比較。由於電池形狀和化學成分正在快速變化,強調可重建電池和IATF 16949認證的供應商正獲得越來越多的支持。將模組化設備定位為應對化學成分變化的保障措施,對於確保2026年至2028年間的延期訂單至關重要。

提高熟練工具機員的薪資

2024年,工具機員的平均時薪達到24.82美元,超過了普通工廠工人的工資水平,給價格競爭力較弱的代工製造商的利潤率帶來了壓力。雖然薪資上漲推動了企業自動化進程,但類似的成本壓力也提高了投資報酬率(ROI)的要求,導致訂單成長放緩。提供承包機器人單元並附帶性能保證的供應商正在緩解工資衝擊,並恢復買家信心。

細分市場分析

到2025年,銑床將占美國工具機市場銷售額的30.32%,佔最大佔有率。然而,多軸加工中心預計到2031年將以每年5.41%的速度成長,成為成長最快的子類別。其一次裝夾即可完成加工,符合FDA針對病患客製化植入的驗證指南及ASME B5.54性能標準。雷射加工中心、電火花加工中心、水刀加工中心及等離子加工中心合計約佔銷售額的20%,在非接觸式加工能減少刀具磨損的領域,對這類加工中心的需求日益成長。隨著供應鏈縮短和批量縮小,買家越來越重視加工柔軟性而非簡單的加工能力,因此他們更傾向於選擇多軸加工中心和雷射加工解決方案。

此外,多軸加工技術的引進使得固定成本能夠分攤到各種工件上,從而有效規避需求波動帶來的風險。 DMG MORI 和 Mazak 等公司正將數位雙胞胎與新機型結合,並透過虛擬試運行展示投資回報率。同時,TRUMPF 的斜切雷射系列產品可將焊接準備時間縮短高達 40%。這些優勢的結合,正在減少對單一用途鑽床和研磨的投資,進一步鞏固可配置平台在美國工具機市場的主導地位。

到2025年,CNC工具工具機將佔技術銷售額的66.56%,這反映了其在過去幾十年中在美國工具機市場的主導地位。預計到2031年,該細分市場將保持強勁成長,年複合成長率達5.19%,這主要得益於生成式人工智慧附加元件在無需更換底盤的情況下提高了生產效率。雖然傳統的手動設備仍在學校和維修店中使用,但由於工資上漲和安全法規日益嚴格,其使用量正在下降。混合型(積層製造和機械加工)設備的銷售額佔不到10%,但它正在航太原型和醫療植入等領域開闢利基市場,在這些領域,近淨成形製造可以減少廢棄物。

競爭格局日趨激烈。亞洲一些新晉參與企業提供的定位精準度與老牌廠商不相上下,但價格卻低了20%至30%。因此,老牌廠商紛紛將包括專有軟體生態系統、刀具磨損預測、雲端儀錶板和計量收費分析在內的服務打包銷售,以確保業務收益。這種以服務為中心的策略幫助他們在美國工具機產業硬體日益同質化的背景下,依然能夠維持利潤率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- IRA、CHIPS 和 IIJA 等機構採取的資本投資獎勵策略

- 電動車和電池超級工廠對精密工具的需求

- 鈦加工在民用和國防航太領域的回收。

- 加速向工業4.0改裝

- 美國國防部 (DoD) 高超音速材料加工的細分市場

- 人工智慧產生的自適應刀具路徑的投資報酬率

- 市場限制因素

- 熟練機械師的薪資上漲

- 透過高利率延長投資復甦期

- 鋼鐵和稀土元素的價格波動很大。

- 與 CMMC 2.0 合規相關的成本負擔

- 價值/供應鏈分析

- 監理趨勢(主要政府法規和措施)

- 技術概述

- 互聯自動化機器

- 先進的控制/運動系統

- 數位化和工業4.0

- 利用人工智慧提高金屬切削精度

- 金屬加工產業概覽

- 地緣政治對工具機市場的影響

- 產業吸引力—五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模及成長預測(價值,十億美元)

- 依產品

- 切削刀具

- 銑床

- 鑽床

- 車床

- 研磨

- 雷射切割機

- 電火花加工工具機(EDM)

- 水刀切割機

- 電漿切割機

- 多軸加工中心

- 其他(保齡球等)

- 金屬成型工具

- 壓力機(機械式、液壓式、伺服式)

- 鍛造機

- 折彎機

- 其他工藝(剪切、擠壓、軋延等)

- 切削刀具

- 透過技術

- 傳統機械(手動或半自動)

- CNC工具工具機

- 積層製造/混合機器

- 按最終用戶行業分類

- 車

- 航太/國防

- 電氣和電子

- 工業機械和設備

- 醫療設備

- 造船/造船

- 精密工程

- 能源與電力

- 金屬加工(合約製造商等)

- 其他行業(鐵路、其他一般製造業等)

- 按銷售管道

- 直接銷售(從OEM廠商到最終用戶)

- 經銷商和銷售代理商

- 線上/電子商務

- 其他(系統整合商、活動/展覽公司、翻新/維修公司等)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Haas Automation

- TRUMPF Inc.

- DMG MORI USA

- Mazak Corp.

- Okuma America

- Amada America

- Lincoln Electric

- Hardinge Inc.

- Hurco Companies

- Fives Machining Systems

- JTEKT(Toyoda)

- MC Machinery Systems

- Bystronic Inc.

- Mate Precision Tooling

- Cincinnati Inc.

- Koike Aronson

- FANUC America

- United Grinding NA

- Starrag USA

- GROB Systems

第7章 市場機會與未來展望

The United States machine tools market size was valued at USD 25.34 billion in 2025 and is estimated to grow from USD 26.40 billion in 2026 to reach USD 32.42 billion by 2031, at a CAGR of 4.19% during the forecast period (2026-2031).

Federal legislation, the Infrastructure Investment and Jobs Act, CHIPS and Science Act, and Inflation Reduction Act have already triggered more than USD 2 trillion in authorized outlays, doubling manufacturing construction spending between 2021 and 2024 and sharply lifting demand for precision equipment across semiconductor, battery, and defense corridors.Suppliers are responding with AI-enabled retrofit kits that shorten cycle times by up to 12%, helping buyers justify capex even as policy rates soften only gradually. Wage inflation for skilled machinists, which ran 1.8 percentage points ahead of average factory pay in 2024, is adding urgency to labor-saving automation but is also lengthening payback horizons where financing costs remain high.Commodity swings compound the picture: tungsten-carbide inputs rose 22% year-over-year in early 2025, forcing OEMs to alter toolholder compositions and push fixed-price service contracts to stabilize margins.

United States Machine Tools Market Trends and Insights

IRA, CHIPS & IIJA CapEx Stimulus

Federal incentives front-loaded what would have been a decade of capital spending into a three-year window. Semiconductor and battery corridors ordered advanced grinders, EDM units, and 5-axis centers capable of wafer and electrode processing. While early disbursements peaked in 2024-2025, suppliers tying payment terms to grant milestones stand to hold share until private follow-on funds materialize. The possibility of midstream supply-chain gaps, especially in battery separators and foils, could moderate tooling orders after 2027. Success will depend on synchronizing product roadmaps with the remaining CHIPS Act tranches.

EV and Battery-Gigafactory Precision-Tooling Demand

Gigafactories have driven brisk sales of laser welders and high-speed presses, yet lower-than-expected onsite machining intensity has curbed orders for general-purpose lathes and mills. Automakers remain cautious, weighing in-house cell production against joint-venture supply pacts. Vendors highlighting reconfigurable cells and IATF 16949 documentation gain traction because cell formats and chemistries evolve quickly. Positioning modular equipment as a hedge against chemistry shifts is central to capturing delayed orders in 2026-2028.

Skilled-Machinist Wage Inflation

Median machinist pay hit USD 24.82 per hour in 2024, outpacing general factory wages and compressing margins for low-pricing-power job shops. While higher pay pushes firms toward automation, the same cost pressure raises ROI hurdles, slowing orders. Suppliers bundling turnkey robotic cells with performance guarantees cushion the wage shock and rebuild buyer confidence.

Other drivers and restraints analyzed in the detailed report include:

- Commercial and Defense Aerospace Titanium-Machining Rebound

- Industry 4.0 Retrofit Acceleration

- High Interest-Rate-Driven Payback Extension

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Milling machines accounted for 30.32% of 2025 revenue, the largest slice of the United States machine tools market share. However, multi-axis machining centers are projected to grow at 5.41% annually through 2031, the fastest-rising subcategory. Their single-setup capability aligns with FDA validation guidance for patient-specific implants and with ASME B5.54 performance benchmarks. Laser, EDM, waterjet, and plasma units jointly hold roughly 20% of sales and gain traction where contactless processing reduces tool wear. As supply chains shorten and batch sizes shrink, buyers value flexibility over raw throughput, favoring multi-axis and laser solutions.

Multi-axis adoption also spreads fixed costs across varied workpieces, an important hedge against demand volatility. Companies like DMG MORI and Mazak bundle digital twins with new machines to prove ROI via virtual commissioning, while TRUMPF's bevel-cut laser series cuts weld-prep time by up to 40%. Collectively, these features are steering capital away from single-purpose drills or grinders, reinforcing a premium position for configurable platforms within the United States machine tools market.

CNC machines commanded 66.56% of 2025 technology sales, reflecting decades of installed-base advantages in the United States machine tools market. The segment is still forecast to advance at a robust 5.19% CAGR through 2031 as generative-AI add-ons lift productivity without requiring chassis replacement. Conventional manual equipment lingers in schools and repair shops but faces attrition as wages rise and safety regulations tighten. Hybrid additive-subtractive units, although below 10% of volume, are carving a niche in aerospace prototypes and medical implants where near-net shapes curb waste.

Competitive dynamics are intensifying. Several Asian entrants now match positional accuracy at 20-30% lower list prices. Incumbents therefore bundle proprietary software ecosystems, tool-wear prediction, cloud dashboards, and pay-per-use analytics to lock in service revenue. This service-centric stance helps defend margins even as hardware commoditizes within the broader United States machine tools industry.

The United States Machine Tools Market Report is Segmented by Product Type (Metal Cutting Tools (Milling Machines, and More), Metal Forming Tools (Presses and More)), by Technology (Conventional, CNC, Additive/Hybrid), by End-User Industry (Automotive, Aerospace & Defense, Electrical & Electronics, and More), and by Sales Channel (Direct Sales, Dealers, Online/E-commerce). Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Haas Automation

- TRUMPF Inc.

- DMG MORI USA

- Mazak Corp.

- Okuma America

- Amada America

- Lincoln Electric

- Hardinge Inc.

- Hurco Companies

- Fives Machining Systems

- JTEKT (Toyoda)

- MC Machinery Systems

- Bystronic Inc.

- Mate Precision Tooling

- Cincinnati Inc.

- Koike Aronson

- FANUC America

- United Grinding NA

- Starrag USA

- GROB Systems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 IRA, CHIPS & IIJA CapEx stimulus

- 4.2.2 EV & battery-gigafactory precision-tooling demand

- 4.2.3 Commercial & defence aerospace titanium-machining rebound

- 4.2.4 Industry 4.0 retrofit acceleration

- 4.2.5 DoD hypersonic-materials machining niche

- 4.2.6 Generative-AI adaptive tool-path ROI

- 4.3 Market Restraints

- 4.3.1 Skilled-machinist wage inflation

- 4.3.2 High interest-rate-driven payback extension

- 4.3.3 Volatile steel / rare-earth cost inflation

- 4.3.4 CMMC 2.0 compliance-cost burden

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook (Key Government Regulations & Initiatives)

- 4.6 Technology Snapshot

- 4.6.1 Connected & Automated Machines

- 4.6.2 Advanced Controls / Motion Systems

- 4.6.3 Digitalisation & Industry 4.0

- 4.6.4 AI-Enhanced Metal Cutting Accuracy

- 4.7 Metalworking Industry Snapshot

- 4.8 Impact of Geopolitics on the Machine Tools Market

- 4.9 Industry Attractiveness - Porter?s Five Forces

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Product

- 5.1.1 Metal Cutting Tools

- 5.1.1.1 Milling Machines

- 5.1.1.2 Drilling Machines

- 5.1.1.3 Turning (Lathe) Machines

- 5.1.1.4 Grinding Machines

- 5.1.1.5 Laser Cutting Machines

- 5.1.1.6 Electrical Discharge Machines (EDM)

- 5.1.1.7 Waterjet Cutting Machines

- 5.1.1.8 Plasma Cutting Machines

- 5.1.1.9 Multi-Axis Machining Centres

- 5.1.1.10 Others (Boring, etc.)

- 5.1.2 Metal Forming Tools

- 5.1.2.1 Presses (Mechanical, Hydraulic, Servo)

- 5.1.2.2 Forging Machines

- 5.1.2.3 Bending Machines

- 5.1.2.4 Others (Shearing, Extrusion, Rolling, etc.)

- 5.1.1 Metal Cutting Tools

- 5.2 By Technology

- 5.2.1 Conventional Machines (Manually or Semi-Manually)

- 5.2.2 CNC Machines

- 5.2.3 Additive Manufacturing / Hybrid Machines

- 5.3 By End-User Industry

- 5.3.1 Automotive

- 5.3.2 Aerospace & Defence

- 5.3.3 Electrical & Electronics

- 5.3.4 Industrial Machinery & Equipment

- 5.3.5 Medical Devices

- 5.3.6 Shipbuilding & Marine

- 5.3.7 Precision Engineering

- 5.3.8 Energy & Power

- 5.3.9 Metal Fabrication (Job Shops, etc.)

- 5.3.10 Other Industries (Railway, Other General Manufacturing, etc.)

- 5.4 By Sales Channel

- 5.4.1 Direct Sales (OEMs to End Users)

- 5.4.2 Dealers & Distributors

- 5.4.3 Online / E-commerce

- 5.4.4 Others (System Integrators, Events & Exhibitions, Rebuilders & Refurbished, etc.)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Haas Automation

- 6.4.2 TRUMPF Inc.

- 6.4.3 DMG MORI USA

- 6.4.4 Mazak Corp.

- 6.4.5 Okuma America

- 6.4.6 Amada America

- 6.4.7 Lincoln Electric

- 6.4.8 Hardinge Inc.

- 6.4.9 Hurco Companies

- 6.4.10 Fives Machining Systems

- 6.4.11 JTEKT (Toyoda)

- 6.4.12 MC Machinery Systems

- 6.4.13 Bystronic Inc.

- 6.4.14 Mate Precision Tooling

- 6.4.15 Cincinnati Inc.

- 6.4.16 Koike Aronson

- 6.4.17 FANUC America

- 6.4.18 United Grinding NA

- 6.4.19 Starrag USA

- 6.4.20 GROB Systems

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

工具機鋼市場:按類型、等級、產品、生產技術、應用和銷售管道分類-2026-2032年全球市場預測

工具機鋼市場:按類型、等級、產品、生產技術、應用和銷售管道分類-2026-2032年全球市場預測 S波段分路器市場預測至2034年-按類型、尺寸、技術、規格、應用和地區分類的全球分析主軸分析儀市場預測—按類型、組件、應用、最終用戶和地區分類的全球分析—2034年

S波段分路器市場預測至2034年-按類型、尺寸、技術、規格、應用和地區分類的全球分析主軸分析儀市場預測—按類型、組件、應用、最終用戶和地區分類的全球分析—2034年 刀柄市場規模、佔有率和成長分析:按刀柄類型、錐度類型、材質、應用、最終用戶產業、銷售管道和地區分類-2026-2033年產業預測

刀柄市場規模、佔有率和成長分析:按刀柄類型、錐度類型、材質、應用、最終用戶產業、銷售管道和地區分類-2026-2033年產業預測 2026年全球精密零件和刀具系統市場報告

2026年全球精密零件和刀具系統市場報告 工具機市場規模、佔有率和趨勢分析報告:按類型、技術、應用、地區和細分市場分類(2026-2033 年)

工具機市場規模、佔有率和趨勢分析報告:按類型、技術、應用、地區和細分市場分類(2026-2033 年) 工具機市場規模、佔有率、趨勢和預測:按刀具類型、技術、最終用途行業和地區分類,2026-2034年

工具機市場規模、佔有率、趨勢和預測:按刀具類型、技術、最終用途行業和地區分類,2026-2034年 工具機市場:依產品類型、材料類型、應用和地區分類2026年全球車輪主軸市場報告磁磚鋪設工具市場:依產品、材料、應用、最終用戶和銷售管道-2026-2032年全球預測

工具機市場:依產品類型、材料類型、應用和地區分類2026年全球車輪主軸市場報告磁磚鋪設工具市場:依產品、材料、應用、最終用戶和銷售管道-2026-2032年全球預測