|

市場調查報告書

商品編碼

2043859

聲吶系統:市佔率分析、產業趨勢與統計、成長預測(2026-2031)Sonar Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

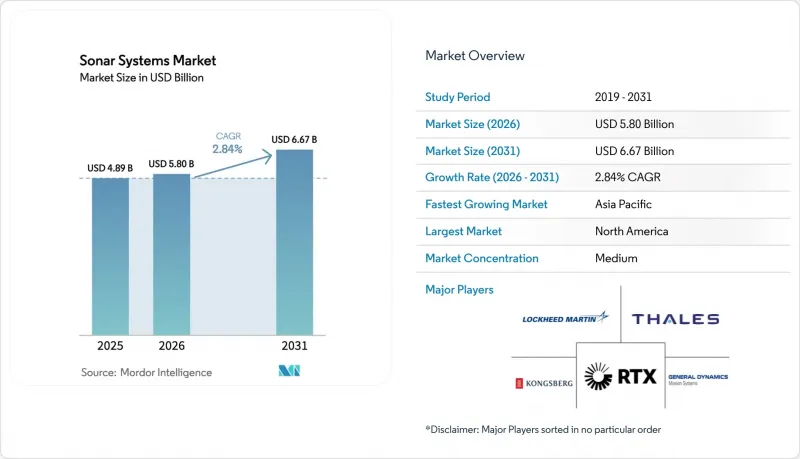

預計聲吶系統市場將從 2025 年的 48.9 億美元成長到 2026 年的 58 億美元,然後在 2031 年達到 66.7 億美元,2026 年至 2031 年的複合年成長率為 2.84%。

這種表面上的溫和成長背後隱藏著結構性轉變:採購預算正從大型船體安裝硬體轉向軟體定義的聲學陣列和自主水下航行器,這些設備覆蓋範圍更廣,同時還能降低生命週期成本。海軍正在為邊緣運算訊號處理分配資金,而私人公司則利用多靜態自主水下航行器(AUV)集群來縮短檢查週期並降低船舶租賃成本。由於離岸風力發電電場建設的不斷增加、國際海事組織(IMO)日益嚴格的水下噪音法規以及人工智慧目標分類技術的進步,商業市場持續擴張。然而,由於持續存在的網路安全漏洞以及光學和磁感等替代技術的出現,商業性壓力不斷加劇,迫使供應商透過開放架構、專有人工智慧軟體棧和承包服務模式來脫穎而出。

全球聲吶系統市場趨勢及洞察

海軍艦隊現代化計劃

冷戰時代的聲吶陣列正被嵌入網路中心架構的模組化軟體定義系統所取代。美國海軍在2025會計年度撥款5,750萬美元用於水下作戰應用研究,並撥款5,360萬美元用於聲學偵測感測器,這表明其優先考慮分階段升級聲吶系統,而非建造新艦。 AUKUS公司的核能以及日本海上自衛隊不斷成長的訂單,進一步提升了全部區域全生命週期支援、橫向陣列和訓練基礎設施的需求。諸如計劃於2026年首次部署的Mk 48魚雷先進處理器第六版(APB6)等項目,體現了海軍在邊緣端整合人工智慧推理、延長傳統平台壽命以及減少對衛星頻寬依賴的趨勢。隨著越來越多的艦隊選擇維修路線,在開放式架構韌體和自主運算領域擁有豐富經驗的供應商正在鞏固其市場地位。

擴大海洋能源探勘

由於天氣原因導致的運作阻礙了水面船舶的作業,深海油田運營商正轉向使用配備合成孔徑聲吶和側掃聲吶的自主水下航行器(AUV)進行巡邏。挪威國家石油公司(Equinor)已將北海的管線勘測週期從14天縮短至5天,並成功實現了2025年船舶成本降低60%的目標。離岸風力發電開發商,尤其是在歐洲和美國,要求在施工前進行高解析度多波束勘測,以繪製巨石區域和未爆彈的分佈圖。在漁業領域,分束迴聲測深儀結合卷積類神經網路,被用於即時區分目標魚類和兼捕魚類,從而幫助避免罰款。在水產養殖網箱中,類似的陣列被用於監測生物量密度和檢測箱體破損,以確保最佳飼料利用率並符合環境法規。這些發展正在將聲吶系統市場拓展到其傳統核心領域——海軍領域之外。

高昂的初始投資和生命週期成本

一套完整的護衛艦聲吶系統造價超過2,000萬美元,而25年的維修費用則需額外支付其中的60%。小規模的海軍優先考慮多用途巡邏艦的資金籌措,延後艦艇升級,導致反潛能下降。商用多波束聲吶系統的價格在50萬至100萬美元之間,每年的校準費用佔標價的10%至15%。租賃和服務捆綁模式雖然可以降低初始成本,但會為營運商帶來持續的營運費用。軟體定義陣列預計可將生命週期成本降低30%,但需要早期整合,而這對於舊有系統而言往往難以實現。

細分市場分析

預計到2025年,國防領域將佔聲吶系統市場規模的69.87%,並有望繼續保持最大佔有率,因為反潛作戰、水雷探測和港口保全任務的資金投入仍將優先考慮。商業領域預計將以4.30%的複合年成長率成長。這是因為海洋能源公司現在將高解析度海底數據視為營運必需品,而非可選項。無人巡邏使海軍和大型石油公司能夠在不將人員暴露於衝突區域的情況下實現全天候監視,這推動了該技術在這兩個客戶群中的應用。

預計到2025年,Equinor公司利用自主水下航行器(AUV)進行合成孔徑聲吶勘測,將使每條管道的船舶運作天數減少6天,這將促使其他公司在2026年增加其勘測宣傳活動的合約承包能力。在漁業和水產養殖領域,具有即時物種識別功能的分束陣列正被用於減少兼捕處罰。儘管私部門發展迅速,但高昂的研發壁壘和出口主導障礙將確保國防領域在2031年之前繼續主導銷售市場。

預計到2025年,被動陣列聲吶將佔總銷售額的54.70%,反映出對隱蔽敵方偵測的持續需求。多靜態聲吶架構將發送器和接收器分離,並透過三角測量法探測弱柴電推進艦艇的反射波,預計其複合年成長率將達到5.10%。這一成長使得多靜態聲吶成為聲吶系統市場中發展最快的技術領域。

MEDUSA無人水下航行器將透過協調分佈式節點,在無需水面艦艇護航的情況下覆蓋關鍵區域,從而擴大其在綠水和棕水作業中的應用。主動聲吶在水雷戰和港口防禦領域仍佔有一席之地,但它需要克服更嚴格的環境審查。這些技術差異表明,聲吶系統市場的未來發展方向是任務主導,而不是「通用型」。

區域分析

預計到2025年,北美將佔全球銷售額的36.98%,這得益於美國潛艦工業基地獲得的39億美元資金以及對邊緣運算聲吶技術的持續投資。憑藉大批量採購週期和獨家採購契約,該地區擁有結構性的規模經濟優勢,可以肯定的是,聲吶系統市場在2031年之前仍將以美國為主導。

亞太地區預計將以4.75%的複合年成長率實現最高成長,主要受澳洲根據「奧庫斯」計劃購買核能、日本擴大艦載聲吶部署以及韓國投資反水雷無人機等因素的推動。該地區各國政府認為,了解海底狀況對於確保能源安全和有效維護其專屬經濟區至關重要。亞太地區聲吶系統市場規模的成長主要得益於國防和海洋能源產業的同步發展。

在歐洲,英國和法國正在升級其梭魚級潛艦的側掃聲吶陣列,而小規模的北約成員國則逐步停止升級,從而維持了穩定的更新需求。挪威在管道保護方面的支出凸顯了海底監視投資的轉變。在中東,港口當局正在海水淡化廠的進水口周圍安裝周邊聲吶陣列,而巴西不斷擴張的近海開發正在推動南美洲需求的逐步成長。總而言之,這些地區呈現出一幅圍繞海洋主權和能源供應韌性而展開的成長熱點圖景。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 海軍艦隊現代化計劃

- 擴大海洋能源探勘

- 保護關鍵水下能源基礎設施

- 無人水下航行器(UUV)數量的激增

- 將人工智慧整合到訊號處理中

- IMO-2028 強制性水下噪音法規

- 市場限制因素

- 高昂的資本成本和生命週期成本

- 頻率管理和許可的障礙

- 非聲學檢測技術的有效性日益提高

- 在傳統平台上加強網路安全的挑戰

- 價值鏈分析

- 監管和技術前景

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 透過使用

- 防禦

- 反潛戰(ASW)

- 地雷探測與反制

- 港口安全

- 其他

- 商業的

- 海上油氣

- 水文測量與調查

- 漁業和水產養殖

- 防禦

- 透過技術

- 主動聲吶

- 被動聲吶

- 多站聲吶

- 透過部署平台

- 艦載

- 潛射型

- 機載型

- 無人平台(UUV/USV)

- 透過安裝方法

- 艦載型

- 拖曳陣列

- 懸吊式聲納

- 潛水艇安裝類型

- 按頻段

- 低頻

- 中頻

- 高頻率

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 南美洲其他地區

- 歐洲

- 英國

- 法國

- 德國

- 義大利

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Thales Group

- RTX Corporation

- L3Harris Technologies, Inc.

- Kongsberg Gruppen ASA

- Northrop Grumman Corporation

- General Dynamics Mission Systems, Inc.

- Ultra Electronics Holdings

- TKMS GmbH

- Teledyne Technologies Incorporated

- FURUNO ELECTRIC CO., LTD.

- Navico Group(Brunswick Corporation)

- ASELSAN AS

- GeoSpectrum Technologies Inc.

- Western Marine Electronics, Inc.

- EdgeTech

- Hanwha Systems Co., Ltd.

第7章 市場機會與未來展望

The sonar systems market size is expected to grow from USD 4.89 billion in 2025 to USD 5.80 billion in 2026 and is forecasted to reach USD 6.67 billion by 2031 at a 2.84% CAGR over 2026-2031.

This modest headline growth conceals a structural shift, as procurement budgets shift from large, hull-mounted hardware toward software-defined acoustic arrays and autonomous vehicles that deliver more exhaustive coverage at lower lifecycle costs. Navies are steering funds toward edge-compute signal processing, while commercial operators use multi-static AUV fleets to shorten inspection cycles and cut vessel charter costs. Increasing offshore wind construction, stricter International Maritime Organization underwater-noise rules, and AI-enabled target classification continue to broaden the commercial addressable base. At the same time, persistent cyber-hardening gaps and the rise of optical or magnetic sensing alternatives keep competitive pressure high, forcing vendors to differentiate themselves through open architectures, sovereign AI software stacks, and turnkey service models.

Global Sonar Systems Market Trends and Insights

Naval Fleet Modernization Programs

Cold-War era arrays are being replaced with modular, software-defined systems that slot into network-centric architectures. The US Navy allocated USD 57.5 million to Undersea Warfare Applied Research and USD 53.6 million to Acoustic Search Sensors in FY 2025, indicating a priority for incremental sonar upgrades over new hulls. AUKUS nuclear-powered submarines and Japan's expanded Maritime Self-Defense Force orders further amplify demand for through-life support, flank arrays, and training infrastructure across the Asia-Pacific. Programs such as the Mk 48 torpedo Advanced Processor Build 6, slated for its first operational use in 2026, demonstrate how navies are embedding AI inference at the edge to extend the life cycles of legacy platforms and reduce their dependency on satellite bandwidth. As more fleets opt for retrofit paths, vendors with open-architecture firmware and sovereign-compute credentials strengthen their foothold.

Expanding Offshore Energy Exploration

Deepwater oil operators are shifting to AUV patrols equipped with synthetic-aperture and side-scan sonar because weather downtime hinders surface vessels. Equinor reduced pipeline survey time in the North Sea from 14 days to 5 days, resulting in a 60% decrease in vessel costs by 2025. Offshore wind developers, especially in Europe and the United States, mandate high-resolution multibeam surveys to map boulder fields and unexploded ordnance before construction begins. Fisheries deploy split-beam echosounders coupled with convolutional neural networks to separate quota species from bycatch in real time, helping avoid fines. Aquaculture cages utilize similar arrays to monitor biomass density and detect net tears, ensuring optimal feed usage and environmental compliance. Together, these moves expand the sonar systems market beyond its historical naval core.

High Capital and Lifecycle Costs

A single frigate sonar suite costs more than USD 20 million and requires another 60% of that figure for support over 25 years. Smaller navies defer upgrades to fund multi-role patrol vessels, thereby reducing their anti-submarine capacity. Commercial multibeam rigs range from USD 500,000 to USD 1 million, with annual calibration consuming 10%-15% of the list price. Leasing and service-bundle models lower entry costs but shift operators into recurring fees. Software-defined arrays promise 30% lifecycle savings, yet they require an upfront integration commitment that legacy systems often cannot support.

Other drivers and restraints analyzed in the detailed report include:

- Protecting Critical Subsea Energy Infrastructure

- Surge in Unmanned Underwater Vehicles (UUVs)

- Spectrum-Management and Licensing Hurdles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Defense accounted for 69.87% of the sonar systems market size in 2025 and is expected to remain the largest segment, as anti-submarine warfare, mine detection, and port security missions continue to receive funding priority. The commercial segment is projected to register a 4.30% CAGR because offshore energy companies now treat high-resolution seabed data as an operational necessity rather than an optional cost line. Unmanned patrols enable navies and oil majors to achieve 24/7 coverage without exposing crews to contested waters, thereby supporting the broader adoption of this technology across both customer groups.

AUV-based synthetic-aperture sonar surveys saved Equinor six ship days per pipeline inspection in 2025, prompting similar operators to add contract capacity for 2026 campaigns. Fisheries and aquaculture use split-beam arrays with real-time species recognition to cut bycatch penalties. Despite the faster expansion on the civil side, high R&D barriers and export-control hurdles will keep defense in control of absolute revenue through 2031.

Passive arrays delivered 54.70% of 2025 revenue, reflecting the enduring need to detect adversaries while remaining silent. Multi-static architectures, where separated transmitters and receivers triangulate faint diesel-electric returns, are forecast to grow at a 5.10% CAGR. This uptick positions multi-static tools as the fastest-advancing technology segment in the sonar systems market.

MEDUSA UUVs will coordinate distributed nodes to cover chokepoints without a surface escort, amplifying adoption in both green- and brown-water operations. Active sonar keeps its niche in mine countermeasures and harbor defense but must navigate stricter environmental reviews. The technology split underscores a mission-driven rather than one-size-fits-all future for the sonar systems market.

The Sonar Systems Market Report is Segmented by Application (Defense, and Commercial), Technology (Active, Passive, and Multi-Static), Installation Platform (Ship, Submarine, Airborne, and Unmanned), Mounting (Hull, Towed Array, Dipping, and Seabed), Frequency Band (Low, Mid, and High), and Geography (North America, Europe, Asia-Pacific and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 36.98% of global revenue in 2025, underpinned by USD 3.9 billion in US Submarine Industrial Base funding and sustained investment in edge-compute sonar upgrades. High-volume procurement cycles and sole-source contracts give the region structural scale advantages, ensuring that the sonar systems market remains anchored in the United States through 2031.

The Asia-Pacific region is projected to register the fastest 4.75% CAGR as Australia procures nuclear-powered submarines under AUKUS, Japan expands hull-mounted deployments, and South Korea invests in mine countermeasure drones. Regional governments view seabed awareness as a prerequisite for ensuring energy security and effective enforcement of the exclusive economic zone. The sonar systems market size in the Asia-Pacific region is driven by simultaneous growth in defense and offshore energy.

Europe maintains steady replacement demand, with the UK and France upgrading their Barracuda-class flank arrays, while smaller NATO members stagger their upgrades. Norway's pipeline protection spend highlights a shift toward seabed monitoring investments. In the Middle East, port authorities are installing perimeter arrays around desalination intakes, and Brazil's offshore expansion is fueling South America's modest uptick. Collectively, these geographies form a mosaic where growth hotspots revolve around maritime sovereignty and energy supply resilience.

- Thales Group

- RTX Corporation

- L3Harris Technologies, Inc.

- Kongsberg Gruppen ASA

- Northrop Grumman Corporation

- General Dynamics Mission Systems, Inc.

- Ultra Electronics Holdings

- TKMS GmbH

- Teledyne Technologies Incorporated

- FURUNO ELECTRIC CO., LTD.

- Navico Group (Brunswick Corporation)

- ASELSAN A.S.

- GeoSpectrum Technologies Inc.

- Western Marine Electronics, Inc.

- EdgeTech

- Hanwha Systems Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Naval fleet modernization programs

- 4.2.2 Expanding offshore energy exploration

- 4.2.3 Protecting critical subsea energy infrastructure

- 4.2.4 Surge in unmanned underwater vehicles (UUVs)

- 4.2.5 Integrating AI for signal processing

- 4.2.6 Mandatory IMO-2028 under-water noise limits

- 4.3 Market Restraints

- 4.3.1 High capital and lifecycle costs

- 4.3.2 Spectrum-management and licensing hurdles

- 4.3.3 Rising efficacy of non-acoustic detection

- 4.3.4 Cyber-hardening gaps in legacy platforms

- 4.4 Value Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Defense

- 5.1.1.1 Anti-Submarine Warfare (ASW)

- 5.1.1.2 Mine Detection and Countermeasures

- 5.1.1.3 Port Secuirty

- 5.1.1.4 Others

- 5.1.2 Commercial

- 5.1.2.1 Offshore Oil and Gas

- 5.1.2.2 Hydrographic Survey and Research

- 5.1.2.3 Fisheries and Aquaculture

- 5.1.1 Defense

- 5.2 By Technology

- 5.2.1 Active Sonar

- 5.2.2 Passive Sonar

- 5.2.3 Multi-static Sonar

- 5.3 By Installation Platform

- 5.3.1 Ship-mounted

- 5.3.2 Submarine-mounted

- 5.3.3 Airborne

- 5.3.4 Unmanned Platforms (UUV/USV)

- 5.4 By Mounting

- 5.4.1 Hull-Mounted

- 5.4.2 Towed Array

- 5.4.3 Dipping Sonar

- 5.4.4 Seabed-Mounted

- 5.5 By Frequency Band

- 5.5.1 Low-Frequency

- 5.5.2 Mid-Frequency

- 5.5.3 High-Frequency

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 France

- 5.6.3.3 Germany

- 5.6.3.4 Italy

- 5.6.3.5 Russia

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Thales Group

- 6.4.2 RTX Corporation

- 6.4.3 L3Harris Technologies, Inc.

- 6.4.4 Kongsberg Gruppen ASA

- 6.4.5 Northrop Grumman Corporation

- 6.4.6 General Dynamics Mission Systems, Inc.

- 6.4.7 Ultra Electronics Holdings

- 6.4.8 TKMS GmbH

- 6.4.9 Teledyne Technologies Incorporated

- 6.4.10 FURUNO ELECTRIC CO., LTD.

- 6.4.11 Navico Group (Brunswick Corporation)

- 6.4.12 ASELSAN A.S.

- 6.4.13 GeoSpectrum Technologies Inc.

- 6.4.14 Western Marine Electronics, Inc.

- 6.4.15 EdgeTech

- 6.4.16 Hanwha Systems Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球聲吶系統市場:2026-2036年

全球聲吶系統市場:2026-2036年 聲吶系統市場規模、佔有率和趨勢分析報告:按產品、平台、應用、地區和細分市場預測(2026-2033 年)聲吶系統市場報告:趨勢、預測與競爭分析(至2035年)

聲吶系統市場規模、佔有率和趨勢分析報告:按產品、平台、應用、地區和細分市場預測(2026-2033 年)聲吶系統市場報告:趨勢、預測與競爭分析(至2035年) 聲納系統市場報告:按工作模式、產品類型、安裝配置、類別、應用、材質和地區分類(2026-2034 年)

聲納系統市場報告:按工作模式、產品類型、安裝配置、類別、應用、材質和地區分類(2026-2034 年) 聲吶系統市場:全球市場按平台類型、技術、頻段、應用和最終用戶分類的預測——2026-2032年水下聲吶市場規模、佔有率和趨勢分析報告:按聲吶類型、平台、應用、最終用戶產業、地區和細分市場預測(2026-2033 年)

聲吶系統市場:全球市場按平台類型、技術、頻段、應用和最終用戶分類的預測——2026-2032年水下聲吶市場規模、佔有率和趨勢分析報告:按聲吶類型、平台、應用、最終用戶產業、地區和細分市場預測(2026-2033 年) 2026年全球國防與安全側掃聲吶市場報告2026年全球潛水員探測聲吶市場報告2026年全球聲納系統市場報告

2026年全球國防與安全側掃聲吶市場報告2026年全球潛水員探測聲吶市場報告2026年全球聲納系統市場報告 聲吶系統市場:策略洞察與預測(2026-2031 年)

聲吶系統市場:策略洞察與預測(2026-2031 年)