|

市場調查報告書

商品編碼

2043853

預防資料外泄(DLP):市場佔有率分析、產業趨勢與統計、成長預測 (2026-2031)Data Loss Prevention (DLP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

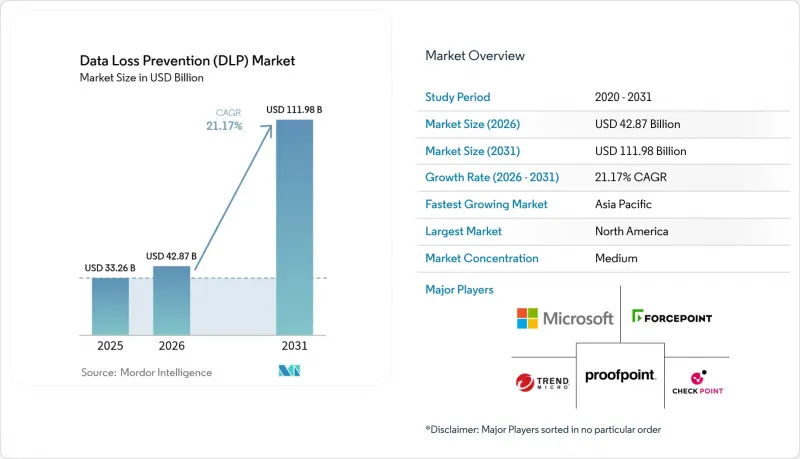

預計資料遺失防護 (DLP) 市場將從 2025 年的 332.6 億美元成長到 2026 年的 428.7 億美元,到 2031 年達到 1,119.8 億美元,2026 年至 2031 年的複合年成長率為 21.17%。

隨著 GDPR 2.0 和修訂後的 CCPA 法規對資料外洩的處罰加大,董事會正在核准更大的資料防洩漏 (DLP) 預算,因為現在每個外洩的記錄都會產生巨額成本。生成式人工智慧助理的出現正在聊天提示中創造新的資料外洩途徑,並將威脅模型從以文件為中心轉向以對話為中心。中國、俄羅斯、印度和歐盟強制推行的主權雲要求在國內進行資料處理,這迫使全球企業運行並行的 DLP 策略以符合當地的加密金鑰管理要求。供應商正在透過將雲端存取安全仲介)、資料安全態勢管理和 DLP 功能整合到單一主機中來應對這種複雜性,從而減少誤報並縮短引進週期。因此,雲端採用現在佔據了新增支出的大部分,終端代理的普及速度正在迅速超過網路設備。

全球預防資料外泄(DLP) 市場趨勢與洞察

GDPR 2.0 和 CCPA 修訂後,網路侵權罰款激增。

2025年,歐洲監管機構根據《一般資料保護規範》(GDPR)處以高達12億歐元的巨額罰款,較前一年大幅增加22%。這一成長清晰地表明了全部區域資料保護條例執行的加強。一個顯著的例子是TikTok被處以5.3億歐元的罰款,凸顯了跨國資料傳輸和GDPR合規性審查力度的加大。同時,修訂後的加州《消費者隱私法案》(CCPA)於2025年1月生效,引入了允許個人提起集體訴訟的新條款。這項變革使得企業可能面臨無限賠償責任,進一步強調了健全資料保護措施的重要性。由於罰款最高可達公司全球營收的4%,首席資訊安全(CISO)被迫實施先進的即時資料防洩漏(DLP)措施。這些措施旨在主動防止資料洩露,確保符合法律標準,並確保組織始終符合不斷變化的法規要求。

混合辦公模式導致資料擴散,增加了終端設備和雲端面臨的風險。

2024 年,Fortinet 的一項調查發現,77% 的組織都經歷過相關人員,其中近一半認為他們目前使用的資料防洩漏 (DLP) 工具效果不佳。自帶設備辦公室 (BYOD) 計劃和非託管文件共用應用程式的普及顯著擴大了潛在的資料外洩途徑,使得組織保護敏感資訊的難度越來越高。目前,企業平均使用 4.3 個基礎設施即服務 (IaaS) 平台,這使得跨平台實現一致的標籤和維護一致的資料保護策略成為一項重大挑戰。 IBM Security 的安全漏洞報告估計,每次資料外洩的平均成本高達 488 萬美元,凸顯了相關的財務風險,並強調了採取強力的預防措施的必要性。因此,董事會正在優先考慮預防策略,而不是事後調查,以降低風險並減少潛在損失。

多重雲端部署的複雜性與技能差距

ISC2在2024年指出,網路安全專業人員將出現350萬的嚴重缺口,凸顯了該領域對技能型專家的日益成長的需求。資料保護尤其重要,由於在保護敏感資訊方面的關鍵作用,資料保護人員的需求量龐大,薪資水準也比其他職位高出18%。包括AWS、Azure和Google Cloud在內的每個超大規模雲端平台都採用其獨特的策略語法,這給試圖跨平台映射標籤的工程師帶來了挑戰。這種缺乏標準化的情況常常迫使企業在遷移過程中並行兩套預防資料外泄(DLP)系統,持續時間長達12個月。這種方法不僅使營運成本翻倍,而且相關風險也隨之增加,進一步加劇了遷移過程的複雜性。

細分市場分析

到 2025 年,雲端部署將佔預防資料外泄(DLP) 市場收入的 67.31%,預計到 2031 年將以 21.23% 的複合年成長率成長。這表明,彈性運算和全球佈局正在推動內聯 API 檢測的發展。對於希望阻止資料流向雲端的國防機構和核能運營商而言,本地部署設備仍然有用,但 TLS 1.3 的日益普及降低了被動竊聽的可見性,迫使即使是受監管的公司也遷移到使用客戶管理金鑰的雲端代理。

此外,其強大的擴充性也降低了每個用戶的成本。由於 Zscaler 每天處理超過 3000 億筆交易,因此每個用戶的額外成本僅為幾美分,而不是幾美元。在混合模式下,SaaS 流量被路由到雲端代理,而檔案伺服器保護則保留在本地,但如果沒有統一的管理,就會出現策略不一致的情況。因此,供應商正在整合統一的主機,以便對兩種環境應用相同的標籤語法。

儘管網路工具在2025年佔總營收的34.23%,但終端代理預計將實現最快成長,到2031年複合年成長率預計將達到23.91%。這一成長主要得益於筆記型電腦、智慧型手機和物聯網感測器等設備的重要性日益提升,運作不再局限於傳統的邊界控制。隨著遠端辦公成為常態,與這些終端相關的資料遺失預防資料外泄(DLP)解決方案的市場規模預計將顯著擴大,這主要源於對強大安全措施的需求不斷成長,以保護分散式工作環境中的敏感資料。

Digital Guardian 即使在離線模式下也能監控剪貼簿、USB 和列印活動,主動阻止違反既定策略的傳輸。這種全面的監控確保即使設備與網路斷開連接,資料安全也能得到保障。另一方面,CrowdStrike 透過將警報與惡意軟體指標整合,增強了資料防洩漏 (DLP) 的有效性,從而縮短回應時間並提高整體威脅緩解能力。網路設備在與空氣間隙的軍事實驗室中仍然至關重要,領先的供應商正在更新其特徵庫,以保持其在這些特殊環境中的有效性。然而,顯而易見的是,成長趨勢嚴重偏向終端安全領域,這反映出隨著組織適應不斷發展的技術格局,安全優先順序正在發生更廣泛的轉變。

區域分析

預計到2025年,北美將佔總營收的40.12%,凸顯其市場主導地位。 2024年,美國記錄了驚人的3,205起資料外洩事件,影響了3.53億人。資料外洩事件的激增,使得經營團隊更加迫切需要實施強力的有效控制措施,以降低風險並確保合規性。加拿大的《個人資訊保護和電子文件法》(PIPEDA)和墨西哥的《資訊取得法》(INAI)都要求公司在72小時內發布資料外洩通知。因此,越來越多的公司正在實施持續監控系統,以主動識別漏洞,避免因違規面臨潛在的法律處罰。

亞太地區正崛起為主要市場參與者,以23.62%的驚人複合年成長率(CAGR)展現出強勁的成長動能。中國的《個人資料保護法》、印度的《數位個人資料保護法》以及日本擬議的《個人資訊保護法》(APPI)修正案,共同提升了該地區資料在地化和合規性的重要性[MEITY.GOV.IN]。這些監管趨勢迫使企業調整業務運營,以滿足嚴格的本地化要求。 IBM預測,受對安全合規資料儲存解決方案日益成長的需求驅動,全部區域的自主雲端支出將以每年31.5%的強勁速度成長。這一趨勢正在推動預防資料外泄(DLP)平台的普及,這些平台提供本地金鑰管理功能,以應對監管和安全方面的擔憂。

在GDPR的嚴格監管下,歐洲持續維持其監管領先地位,預計2025年將累計罰款12億歐元。 Schrems II裁決顯著增加了從美國傳輸數據的複雜性,給在該地區運營的跨國公司帶來了挑戰。為因應這些挑戰,這些組織正在透過實施先進的客戶端加密和利用託管在歐盟境內的金鑰來加強安全措施,以確保符合GDPR的要求。尤其是在2024年,英國、西班牙和義大利加強了執法力度,進一步凸顯了遵守資料保護條例的重要性。此舉增加了對能夠阻止資料傳輸到歐洲經濟區以外地區的策略引擎的需求,使企業能夠在保護敏感資訊的同時保持合規性。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- GDPR 2.0 和 CCPA 修訂後,網路安全違規行為的罰款金額增加。

- 混合辦公模式導致資料擴散,增加了終端設備和雲端的風險。

- DLP、CASB 和 DSPM 平台的整合

- 人工智慧驅動的政策調整可顯著降低誤報率。

- 零信任和SASE藍圖需要整合資料防洩漏功能

- 生成式人工智慧程式碼助理正在為資訊外洩開闢新的途徑。

- 市場限制因素

- 多重雲端部署的複雜性與技能差距

- 傳統本地部署策略的總擁有成本高

- 透過設計來保護隱私,限制了對詳細內容的檢查。

- 強制性主權雲導致全球政策體系碎片化

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 買方的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 不同的發展

- 現場

- 基於雲端的

- 透過解決方案

- 網路資料防洩漏

- 端點資料防洩漏

- 儲存/資料中心 DLP

- 其他

- 按最終用戶行業分類

- BFSI

- 資訊科技和通訊

- 政府/國防

- 衛生保健

- 零售和物流

- 製造業

- 其他

- 透過使用

- 雲端儲存安全

- 保護電子郵件和協作

- 智慧財產權保護和原始碼管治

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 亞太其他地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Broadcom Inc.

- Microsoft Corporation

- GTB Technologies, Inc.

- CoSoSys SRL

- Digital Guardian LLC

- Forcepoint LLC

- Proofpoint, Inc.

- Zscaler, Inc.

- Trend Micro Incorporated

- Check Point Software Technologies Ltd.

- Cisco Systems, Inc.

- Palo Alto Networks, Inc.

- CrowdStrike Holdings, Inc.

- Netskope, Inc.

- Trellix Corporation

- Spirion LLC

- Safetica, as

- Code42 Software, Inc.

- Nightfall AI, Inc.

- Cyera, Inc.

- Fortinet, Inc.

第7章 市場機會與未來展望

The Data loss prevention (DLP) market size expanded from USD 33.26 billion in 2025, to USD 42.87 billion in 2026, and will touch USD 111.98 billion by 2031, rising at a 21.17% CAGR during 2026-2031.

Penalty escalation under GDPR 2.0 and amended CCPA rules now assigns material cost to every breached record, so boards approve bigger DLP budgets. Gen-AI copilots have opened new exfiltration paths inside chat prompts, changing threat models from file-centric to conversation-centric vectors. Sovereign-cloud mandates in China, Russia, India, and the European Union require on-shore processing, so global companies run parallel DLP policies that respect local cryptographic-key custody. Vendors answer this complexity by merging cloud-access security broker, data-security-posture-management, and DLP functions inside one console, lowering false-positive rates and shortening deployment cycles. As a result, cloud deployments now dominate new spending, and endpoint agents outpace network appliances.

Global Data Loss Prevention (DLP) Market Trends and Insights

Escalating Cyber-Breach Fines Under GDPR 2.0 and CCPA Amendments

In 2025, European regulators imposed a substantial EUR 1.2 billion in fines under the GDPR, marking a significant 22% increase compared to the previous year. This rise underscores the growing enforcement of data protection regulations across the region. A notable case involved a EUR 530 million fine levied against TikTok, which highlighted the increasing scrutiny on cross-border data transfers and compliance with GDPR requirements. Meanwhile, California's updated CCPA, which came into effect in January 2025, introduced new provisions allowing private class actions. This change has the potential to expose companies to unlimited damages, further emphasizing the importance of robust data protection measures. With penalties reaching as high as 4% of a company's global turnover, chief information security officers are now compelled to implement advanced real-time Data Loss Prevention (DLP) measures. These controls are designed to prevent data exfiltration proactively, ensuring that legal thresholds are not breached and organizations remain compliant with evolving regulations.

Hybrid-Work Data Sprawl Raising Endpoint and Cloud Risk

In 2024, Fortinet found that 77% of organizations encountered insider incidents, and nearly half deemed their current DLP tools ineffective. The rise of bring-your-own-device programs and unmanaged file-sharing apps has significantly expanded avenues for potential data leakage, making it increasingly difficult for organizations to safeguard sensitive information. With enterprises now averaging 4.3 infrastructure-as-a-service platforms, achieving unified labeling and maintaining consistent data protection policies across platforms has become a considerable challenge. Highlighting the financial stakes involved, the IBM Security breach report pegged the average breach cost at a staggering USD 4.88 million, underscoring the need for robust preventive measures. As a result, boards are now prioritizing prevention strategies over post-incident forensics to mitigate risks and reduce potential losses.

Complexity and Skills Gap in Multi-Cloud Roll-Outs

In 2024, ISC2 identified a significant 3.5 million-person shortfall in the cybersecurity workforce, highlighting the growing demand for skilled professionals in this field. Data-protection roles, in particular, are in high demand, commanding an 18% salary premium due to their critical importance in safeguarding sensitive information. Each hyperscale cloud platform, including AWS, Azure, and Google Cloud, employs its own distinct policy syntax, which creates challenges for engineers attempting to map labels across these platforms. This lack of standardization often forces firms to operate dual DLP (Data Loss Prevention) stacks for an extended period of up to twelve months during migration processes. Consequently, this approach results in a doubling of both operational expenses and associated risks, further complicating the migration process.

Other drivers and restraints analyzed in the detailed report include:

- Convergence of DLP with CASB and DSPM Platforms

- AI-Assisted Policy Tuning Slashing False-Positive Rates

- High TCO for Legacy On-Prem Policies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployments held 67.31% of Data loss prevention (DLP) market revenue in 2025 and are forecast to climb at 21.23% CAGR to 2031, highlighting how elastic compute and global points of presence favor inline API inspection. On-prem appliances stay relevant for defense and nuclear operators that forbid cloud egress, yet rising TLS 1.3 usage reduces the visibility of passive taps, pushing even regulated firms toward cloud proxies with customer-managed keys.

Elastic scale also drives unit pricing lower. Zscaler processes more than 300 billion daily transactions, so each incremental user costs cents, not dollars. Hybrid models route SaaS traffic to cloud proxies while keeping file-server coverage on-premise, but policy drift emerges without federated management. Vendors are therefore embedding unified consoles that push the same label grammar to both environments.

While network tools accounted for 34.23% of the 2025 revenue, endpoint agents are set to experience the swiftest growth, boasting a projected CAGR of 23.91% through 2031. This surge is largely fueled by the rising prominence of laptops, smartphones, and IoT sensors, which increasingly operate beyond traditional perimeter controls. As remote work continues to be the norm, the market size for data loss prevention (DLP) solutions tied to these endpoints is anticipated to see a significant uptick, driven by the growing need for robust security measures to protect sensitive data in decentralized work environments.

Digital Guardian monitors clipboard, USB, and printing activities, even in offline mode, proactively blocking any transfers that breach established policies. This comprehensive monitoring ensures that data remains secure, even when devices are disconnected from the network. Meanwhile, CrowdStrike enhances the DLP's efficacy by linking alerts to malware indicators, thereby expediting the response time and improving overall threat mitigation. Although network appliances are still vital for air-gapped military laboratories, leading vendors are updating their signature packs to maintain relevance in these specialized environments. However, it's evident that the growth trajectory is heavily skewed towards the endpoint segment, reflecting the broader shift in security priorities as organizations adapt to evolving technological landscapes.

The Data Loss Prevention (DLP) Market Report is Segmented by Deployment (On-Premise, and Cloud-Based), Solution (Network DLP, Endpoint DLP, and More), End-User Industry (BFSI, IT and Telecom, Government and Defense, Healthcare, Retail and Logistics, and More), Application (Cloud Storage Security, Email and Collaboration Protection, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, North America accounted for a significant 40.12% of the total revenue, showcasing its dominance in the market. In 2024, the United States recorded a staggering 3,205 breach incidents, which impacted 353 million individuals. This alarming surge in breach volume has heightened urgency at the board level for implementing robust and effective controls to mitigate risks and ensure compliance. Both Canada's PIPEDA and Mexico's INAI regulations mandate firms to issue breach notices within a tight 72-hour window. As a result, companies are increasingly adopting continuous monitoring practices to proactively identify vulnerabilities and sidestep potential statutory penalties that could arise from non-compliance.

Asia-Pacific is emerging as a dominant player in the market, boasting an impressive 23.62% CAGR, which highlights its rapid growth trajectory. China's Personal Information Protection Law, India's Digital Personal Data Protection Act, and Japan's APPI amendments are collectively amplifying the stakes for data localization and compliance in the region [MEITY.GOV.IN]. These regulatory developments are compelling businesses to adapt their operations to meet stringent localization requirements. IBM projects a robust 31.5% annual growth in sovereign cloud spending across the region, driven by increasing demand for secure and compliant data storage solutions. This trend is fueling the adoption of Data Loss Prevention (DLP) platforms, particularly those offering in-country key management capabilities to address regulatory and security concerns.

Europe, under the stringent watch of GDPR, continues to maintain its position as a regulatory leader, levying fines totaling EUR 1.2 billion in 2025. The Schrems II ruling has introduced significant complexities for U.S. data transfers, creating challenges for multinational corporations operating in the region. In response, these organizations are bolstering their security measures by incorporating advanced client-side encryption and utilizing EU-hosted keys to ensure compliance with GDPR requirements. Notably, in 2024, the U.K., Spain, and Italy intensified their enforcement actions, further emphasizing the importance of adhering to data protection regulations. This escalation has led to a heightened demand for policy engines capable of blocking data transfers to regions outside the EEA, ensuring that businesses remain compliant while safeguarding sensitive information.

- Broadcom Inc.

- Microsoft Corporation

- GTB Technologies, Inc.

- CoSoSys SRL

- Digital Guardian LLC

- Forcepoint LLC

- Proofpoint, Inc.

- Zscaler, Inc.

- Trend Micro Incorporated

- Check Point Software Technologies Ltd.

- Cisco Systems, Inc.

- Palo Alto Networks, Inc.

- CrowdStrike Holdings, Inc.

- Netskope, Inc.

- Trellix Corporation

- Spirion LLC

- Safetica, a.s.

- Code42 Software, Inc.

- Nightfall AI, Inc.

- Cyera, Inc.

- Fortinet, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Cyber-Breach Fines Under GDPR 2.0 and CCPA Amendments

- 4.2.2 Hybrid-Work Data Sprawl Raising Endpoint and Cloud Risk

- 4.2.3 Convergence of DLP with CASB and DSPM Platforms

- 4.2.4 AI-Assisted Policy Tuning Slashing False-Positive Rates

- 4.2.5 Zero-Trust and SASE Road Maps Mandating Integrated DLP

- 4.2.6 Gen-AI Code Copilots Creating New Exfiltration Vectors

- 4.3 Market Restraints

- 4.3.1 Complexity and Skills Gap in Multi-Cloud Roll-Outs

- 4.3.2 High TCO for Legacy On-Prem Policies

- 4.3.3 Privacy-by-Design Push Limiting Deep Content Inspection

- 4.3.4 Sovereign-Cloud Mandates Fragmenting Global Policy Sets

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 On-Premise

- 5.1.2 Cloud-Based

- 5.2 By Solution

- 5.2.1 Network DLP

- 5.2.2 Endpoint DLP

- 5.2.3 Storage / Datacenter DLP

- 5.2.4 Others

- 5.3 By End-User Industry

- 5.3.1 BFSI

- 5.3.2 IT and Telecom

- 5.3.3 Government and Defense

- 5.3.4 Healthcare

- 5.3.5 Retail and Logistics

- 5.3.6 Manufacturing

- 5.3.7 Others

- 5.4 By Application

- 5.4.1 Cloud Storage Security

- 5.4.2 Email and Collaboration Protection

- 5.4.3 IP Protection and Source-Code Governance

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Broadcom Inc.

- 6.4.2 Microsoft Corporation

- 6.4.3 GTB Technologies, Inc.

- 6.4.4 CoSoSys SRL

- 6.4.5 Digital Guardian LLC

- 6.4.6 Forcepoint LLC

- 6.4.7 Proofpoint, Inc.

- 6.4.8 Zscaler, Inc.

- 6.4.9 Trend Micro Incorporated

- 6.4.10 Check Point Software Technologies Ltd.

- 6.4.11 Cisco Systems, Inc.

- 6.4.12 Palo Alto Networks, Inc.

- 6.4.13 CrowdStrike Holdings, Inc.

- 6.4.14 Netskope, Inc.

- 6.4.15 Trellix Corporation

- 6.4.16 Spirion LLC

- 6.4.17 Safetica, a.s.

- 6.4.18 Code42 Software, Inc.

- 6.4.19 Nightfall AI, Inc.

- 6.4.20 Cyera, Inc.

- 6.4.21 Fortinet, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

基於雲端的預防資料外泄市場:按組件、部署方式、組織規模、存取管道、技術和行業分類 - 全球市場預測(2026-2032 年)

基於雲端的預防資料外泄市場:按組件、部署方式、組織規模、存取管道、技術和行業分類 - 全球市場預測(2026-2032 年) 全球預防資料外泄(DLP) 先進技術市場:按組件、部署模式、DLP 類型、技術、組織規模和產業分類-市場規模、產業趨勢、機會分析及 2026-2035 年預測

全球預防資料外泄(DLP) 先進技術市場:按組件、部署模式、DLP 類型、技術、組織規模和產業分類-市場規模、產業趨勢、機會分析及 2026-2035 年預測 2026年企業預防資料外泄(EDLP)產品全球市場報告2026年全球企業預防資料外泄軟體市場報告

2026年企業預防資料外泄(EDLP)產品全球市場報告2026年全球企業預防資料外泄軟體市場報告 預防資料外洩(DLP) 市場規模、佔有率、成長率和全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測預防資料外泄(DLP) 市場:按組件、部署模型、組織規模和產業分類-2026-2032 年全球市場預測2026年大規模語言模型資料外洩防護全球市場報告2026年全球資料邊界執行平台市場報告2026年全球預防資料外泄市場報告

預防資料外洩(DLP) 市場規模、佔有率、成長率和全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測預防資料外泄(DLP) 市場:按組件、部署模型、組織規模和產業分類-2026-2032 年全球市場預測2026年大規模語言模型資料外洩防護全球市場報告2026年全球資料邊界執行平台市場報告2026年全球預防資料外泄市場報告 預防資料外泄(DLP) 市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶和解決方案分類

預防資料外泄(DLP) 市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶和解決方案分類