|

市場調查報告書

商品編碼

2043848

非洲和中東汽車應用熱塑性聚合物複合材料:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)Africa And Middle-East Automotive Thermoplastic Polymer Composites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

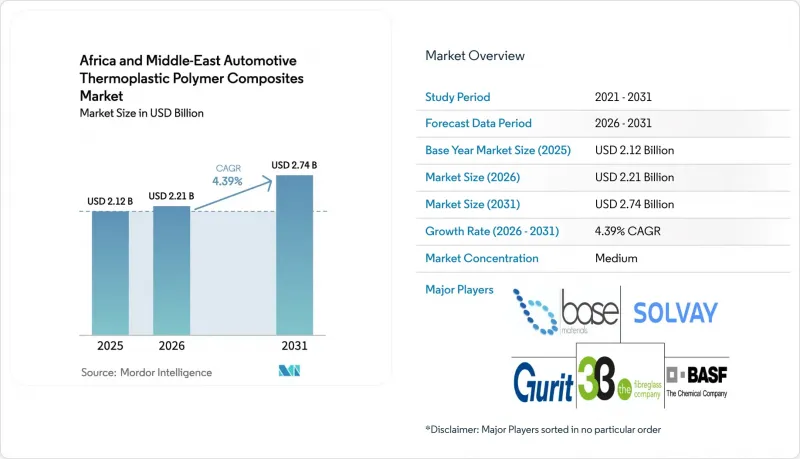

預計非洲和中東汽車熱塑性聚合物複合材料的市場規模將從 2025 年的 21.2 億美元成長到 2026 年的 22.1 億美元,然後從 2026 年到 2031 年以 4.39% 的複合年成長率成長,到 2031 年達到 27.4 億美元。

強制性減重、沙烏地阿拉伯和阿拉伯聯合大公國的在地化獎勵以及向電動車的轉型,正在推動對玻璃纖維和碳纖維增強聚丙烯及聚醯胺部件的需求成長。射出成型因其高產能,在內飾件和小型外飾件的生產中仍佔據主導地位。然而,壓縮成型正在迅速發展,這得益於連續纖維有機片材的應用,可將生產週期縮短至90秒以內。區域碳定價試點計畫雖然目前規模有限,但已發出明確的定價訊號,有利於能夠證明其生命週期排放減少的原始設備製造商(OEM)。因此,供應鏈策略正轉向區域複合生產和多年纖維採購契約,這有助於降低原物料價格波動的風險並縮短前置作業時間。

非洲和中東汽車熱塑性聚合物複合材料市場的趨勢和見解。

嚴格的區域二氧化碳排放法規和類似 CAFE(燃油經濟性標準)的車輛排放氣體法規

沙烏地阿拉伯計畫在2025年實現車隊平均燃油消耗目標,而埃及則採用了歐5排放標準,這些因素正推動著車門模組、前端支架和儀錶面板等零件中鋼材被長纖維玻璃增強聚醯胺(LGFPE)材料所取代。這項轉變將在滿足碰撞安全標準的前提下,達到30%至40%的減重。此外,阿拉伯聯合大公國的目標是到2030年將電動或混合動力汽車的銷量佔比達到50%,這也推動了這一趨勢,因為電池組增加導致車輛重量增加,從而刺激了對輕量化材料的需求。原始設備製造商(OEM)的競標文件中擴大引用ISO 14040生命週期評估標準,要求供應商衡量其從聚合到報廢回收的整個過程中的碳足跡。

沙烏地阿拉伯和阿拉伯聯合大公國自由區OEM在地化獎勵

在阿布達比的阿卜杜拉國王經濟城和阿布達比國際工業發展局(KIZAD),政府提供10年免稅期、設備免稅進口和土地補貼,以鼓勵一級加工商在當地建立複合材料和模塑生產設施。例如,Lucid Motors已將其美國工廠生產的長纖維玻璃增強聚丙烯內飾板轉移至沙烏地阿拉伯的工廠,降低了18%的物流成本,並將前置作業時間從8週縮短至3週。與中國材料製造商達成的類似協議也確保了電動車動力傳動系統零件所需的聚醯胺66和聚亞苯硫醚的擠出能力。

進口(玻璃纖維和碳纖維)導致原物料價格波動

2024年至2025年間,紅海航線中斷以及歐洲熔爐能源成本上漲導致玻璃纖維和碳纖維價格波動15%至25%。沙烏地阿拉伯和阿拉伯聯合大公國的原始設備製造商(OEM)透過簽訂多年合約,在一定程度上緩解了這些波動。然而,埃及和肯亞的中小型加工商則面臨挑戰,他們必須在承擔成本上漲和冒著失去固定價格零件合約的風險之間做出選擇。此外,貨幣貶值,例如2024年埃及鎊貶值18%和2025年南非幣貶值12%,進一步推高了以該地貨幣的纖維價格,給加工商的利潤率帶來了壓力。

細分市場分析

預計到2031年,壓縮成型將以4.78%的複合年成長率成長。射出成型在大批量生產應用中,例如內裝零件、引擎蓋和小塊外板,仍保持著成本優勢,預計到2025年將佔總產量的36.42% 。手工積層繼續應用於豪華車內裝等領域,但由於纖維分佈不均和人事費用高昂,其擴充性受到限制。樹脂轉注成形在電池機殼越來越受歡迎,使用快速固化的聚醯胺6可以將成型週期縮短至4-6分鐘。真空灌注成型目前仍主要局限於原型生產。

有機片材技術已成為壓縮成型的關鍵基礎技術。預固化的連續纖維嵌入熱塑性基體中,可實現少於90秒的成型週期和穩定的產品品質。 Ceer的首款電動車車型採用了壓縮成型的聚醯胺6底盤護板,使車身重量減輕了35%,並在車輛的整個生命週期內降低了20%的總擁有成本。阿拉伯聯合大公國法規要求提交ISO 527拉伸試驗和ISO 14125彎曲試驗數據,這促使企業採用自動化工藝來確保品質指標,從而加速了從手工層壓工藝向自動化工藝的轉變。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 各地區都有嚴格的二氧化碳排放法規,汽車排放氣體法規類似 CAFE(燃油效率標準)。

- 沙烏地阿拉伯和阿拉伯聯合大公國自由區OEM在地化獎勵

- 電動汽車零件的採購趨勢正在迅速轉向可回收的PP/PA複合材料。

- 海灣合作理事會國家的碳定價試點計畫正在提振對輕量材料的需求。

- 採用 3D 列印技術製造長纖維熱塑性聚合物模具,可降低資本投入。

- 市場限制因素

- 進口(玻璃纖維和碳纖維)導致原物料價格波動

- 北非和整個撒哈拉以南非洲地區缺乏熟練的複合材料技術人員。

- 混合熱塑性層壓板回收流程的碎片化

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 依產品類型

- 射出成型

- 手工積層

- 樹脂轉注成形(RTM)

- 真空灌注成型

- 壓縮成型

- 透過使用

- 內部的

- 外部的

- 結構組裝

- 動力傳動系統部件

- 其他用途

- 按地區

- 南非

- 埃及

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東和非洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- 3B-the fibreglass company

- Base Materials Ltd.

- BASF

- Chongqing Polycomp International Corporation(CPIC)

- Solvay

- BorgWarner

- Far-UK

- General Motors Company

- Gurit Holding AG

- Hexcel Corporation

- Johns Manville

- LyondellBasell

- Nippon Electric Glass

- Praana Group

- Saint-Gobain Vetrotex

- SGL Carbon

- Taishan Fiberglass

- Teijin Limited

第7章 市場機會與未來展望

The Africa And Middle-East Automotive Thermoplastic Polymer Composites Market size is expected to grow from USD 2.12 billion in 2025 to USD 2.21 billion in 2026 and is forecast to reach USD 2.74 billion by 2031 at 4.39% CAGR over 2026-2031. Light-weighting mandates, localization incentives in Saudi Arabia and the United Arab Emirates, and the growing transition to electric vehicles are driving increased demand for glass- and carbon-fiber-reinforced polypropylene and polyamide components. Injection molding continues to dominate in producing interior trim and small exterior parts due to its high-volume capabilities. However, compression molding is expanding rapidly, supported by the adoption of continuous-fiber organo-sheets, which reduce cycle times to under 90 seconds. Regional carbon-pricing pilots, though currently limited, are providing a clear price signal that benefits OEMs capable of demonstrating lower life-cycle emissions. Consequently, supply chain strategies are shifting toward in-region compounding and multi-year fiber offtake agreements, which help mitigate raw material price volatility and reduce lead times.

Africa And Middle-East Automotive Thermoplastic Polymer Composites Market Trends and Insights

Stringent Regional CO2/CAFE-Like Auto-Emission Policies

Fleet-average fuel-economy targets planned for Saudi Arabia in 2025 and Egypt's implementation of Euro 5 norms are driving the replacement of steel with long-glass-fiber polyamide in components such as door modules, front-end carriers, and instrument panels. This transition achieves 30%-40% mass savings while meeting crash-performance standards. Additionally, UAE programs aiming for 50% electric or hybrid vehicle sales by 2030 are reinforcing this trend, as battery packs increase vehicle curb weight, heightening the demand for lightweight materials. OEM bid documents increasingly reference ISO 14040 life-cycle assessments, requiring suppliers to measure carbon footprints from polymerization to end-of-life recycling.

OEM Localization Incentives in Saudi Arabia and UAE Free Zones

Ten-year tax holidays, duty-free equipment imports, and subsidized land in King Abdullah Economic City and Abu Dhabi's KIZAD are motivating tier-1 converters to establish local compounding and molding facilities. For instance, Lucid Motors shifted the production of long-glass-fiber polypropylene interior panels from U.S. plants to a Saudi-based source, reducing logistics costs by 18% and shortening lead times from eight weeks to three. Similar agreements with Chinese material producers are anchoring polyamide-66 and polyphenylene-sulfide extrusion capacities for EV powertrain components.

Import-Driven Raw-Material Price Volatility (Glass and Carbon Fiber)

Glass and carbon fiber costs experienced fluctuations of 15%-25% during 2024-2025 due to disruptions in Red Sea shipping and increased energy costs at European furnaces. Saudi and UAE OEMs managed to partially mitigate these fluctuations through multi-year contracts. However, smaller converters in Egypt and Kenya faced challenges, as they had to either absorb the cost increases or risk losing fixed-price component agreements. Additionally, currency depreciation, such as 18% for the Egyptian pound in 2024 and 12% for the South African rand in 2025, further increased local-currency fiber prices, putting pressure on converter margins.

Other drivers and restraints analyzed in the detailed report include:

- Rapid EV Component Sourcing Shift Toward Recyclable PP/PA Composites

- GCC Carbon-Pricing Pilots Boosting Lightweight Demand

- Deficit of Skilled Composite Technicians across North and Sub-Saharan Africa

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Compression molding is anticipated to grow at a 4.78% CAGR through 2031. Injection molding maintained 36.42% of 2025 output due to its cost advantages for high-volume applications such as interior trim, under-hood covers, and small exterior skins. Hand lay-up continues to be used for boutique luxury interiors, but its scalability is restricted by inconsistent fiber distribution and high labor costs. Resin transfer molding is gaining acceptance for battery enclosures, with fast-cure polyamide 6 reducing cycle times to 4-6 minutes. Vacuum infusion remains primarily limited to prototype production.

Organo-sheet technology serves as a key enabler for compression molding. Pre-consolidated continuous fibers embedded in a thermoplastic matrix enable cycle times of less than 90 seconds with consistent quality. Ceer's first electric vehicle model incorporates compression-molded polyamide-6 underbody shields, achieving a 35% weight reduction and a 20% decrease in total cost of ownership over the vehicle's lifecycle. UAE regulations requiring ISO 527 tensile and ISO 14125 flexural data favor automated processes that ensure quality metrics, accelerating the transition away from manual lay-ups.

The Africa and Middle-East Automotive Thermoplastic Polymer Composites Market Report is Segmented by Production Type (Injection Molding, Hand Lay-Up, and More), Application Type (Interior, Exterior, Structural Assembly, Powertrain Components, and More), and Geography (South Africa, Egypt, United Arab Emirates, Saudi Arabia, and Rest of Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3B - the fibreglass company

- Base Materials Ltd.

- BASF

- Chongqing Polycomp International Corporation (CPIC)

- Solvay

- BorgWarner

- Far-UK

- General Motors Company

- Gurit Holding AG

- Hexcel Corporation

- Johns Manville

- LyondellBasell

- Nippon Electric Glass

- Praana Group

- Saint-Gobain Vetrotex

- SGL Carbon

- Taishan Fiberglass

- Teijin Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent regional CO2/CAFE-like auto-emission policies

- 4.2.2 OEM localisation incentives in Saudi Arabia and UAE free-zones

- 4.2.3 Rapid EV component sourcing shift towards recyclable PP/PA composites

- 4.2.4 GCC carbon-pricing pilots boosting lightweight material demand

- 4.2.5 3D-printed long-fibre thermoplastic tooling lowering cap-ex

- 4.3 Market Restraints

- 4.3.1 Import-driven raw-material price volatility (glass and carbon fibre)

- 4.3.2 Deficit of skilled composite technicians across North and Sub-Saharan Africa

- 4.3.3 Fragmented recycling streams for mixed thermoplastic laminates

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Production Type

- 5.1.1 Injection Molding

- 5.1.2 Hand Lay-Up

- 5.1.3 Resin Transfer Molding (RTM)

- 5.1.4 Vacuum Infusion Processing

- 5.1.5 Compression Molding

- 5.2 By Application Type

- 5.2.1 Interior

- 5.2.2 Exterior

- 5.2.3 Structural Assembly

- 5.2.4 Powertrain Components

- 5.2.5 Other Application Types

- 5.3 By Geography

- 5.3.1 South Africa

- 5.3.2 Egypt

- 5.3.3 United Arab Emirates

- 5.3.4 Saudi Arabia

- 5.3.5 Rest of Middle-East and Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3B - the fibreglass company

- 6.4.2 Base Materials Ltd.

- 6.4.3 BASF

- 6.4.4 Chongqing Polycomp International Corporation (CPIC)

- 6.4.5 Solvay

- 6.4.6 BorgWarner

- 6.4.7 Far-UK

- 6.4.8 General Motors Company

- 6.4.9 Gurit Holding AG

- 6.4.10 Hexcel Corporation

- 6.4.11 Johns Manville

- 6.4.12 LyondellBasell

- 6.4.13 Nippon Electric Glass

- 6.4.14 Praana Group

- 6.4.15 Saint-Gobain Vetrotex

- 6.4.16 SGL Carbon

- 6.4.17 Taishan Fiberglass

- 6.4.18 Teijin Limited

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

汽車輕量材料市場預測至2034年-全球材料類型、零件、車輛類型、動力傳動系統、製造流程、應用及區域分析

汽車輕量材料市場預測至2034年-全球材料類型、零件、車輛類型、動力傳動系統、製造流程、應用及區域分析 汽車複合材料市場:按材料、製造流程、應用和最終用途分類-2026-2032年全球市場預測

汽車複合材料市場:按材料、製造流程、應用和最終用途分類-2026-2032年全球市場預測 2026年全球汽車複合材料市場報告

2026年全球汽車複合材料市場報告 汽車複合材料市場分析及預測(至2035年):依類型、產品、技術、組件、應用、材料類型、製程、最終用戶、功能及安裝類型分類2026年全球醫用可調力彈簧市場報告

汽車複合材料市場分析及預測(至2035年):依類型、產品、技術、組件、應用、材料類型、製程、最終用戶、功能及安裝類型分類2026年全球醫用可調力彈簧市場報告 汽車用矽橡膠市場規模、佔有率和成長分析(按類型、產品類型、固化機制、應用、最終用途產業和地區分類)-2026-2033年產業預測

汽車用矽橡膠市場規模、佔有率和成長分析(按類型、產品類型、固化機制、應用、最終用途產業和地區分類)-2026-2033年產業預測 全球汽車複合材料市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球汽車複合材料市場規模、佔有率、趨勢和成長分析報告(2026-2034) 全球汽車複合材料市場:市場規模、佔有率和趨勢分析(按產品、應用和地區分類),細分市場預測(2026-2033 年)

全球汽車複合材料市場:市場規模、佔有率和趨勢分析(按產品、應用和地區分類),細分市場預測(2026-2033 年) 汽車複合材料市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、材料、地區和競爭格局分類,2021-2031年汽車用碳奈米管材料市場(按碳奈米管類型、產品形式、車輛類型、最終用途、銷售管道和應用分類),全球預測,2026-2032年

汽車複合材料市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、材料、地區和競爭格局分類,2021-2031年汽車用碳奈米管材料市場(按碳奈米管類型、產品形式、車輛類型、最終用途、銷售管道和應用分類),全球預測,2026-2032年