|

市場調查報告書

商品編碼

2043844

歐洲智慧家庭:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Europe Smart Homes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

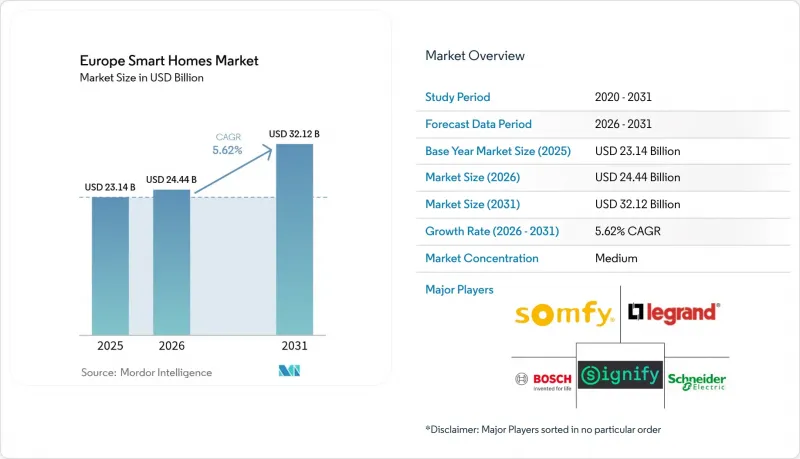

歐洲智慧家庭市場預計將從 2025 年的 231.4 億美元和 2026 年的 244.4 億美元成長到 2031 年的 321.2 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 5.62%。

強制性零排放建築法規、補貼熱泵部署以及動態電價體系,正將連網設備從單純的小玩意提升為監管要求。北歐國家和荷蘭的電網營運商正在發布定價API,鼓勵自動負載轉移,從而加速需量反應恆溫器和智慧充電器的普及。同時,鹵素燈的逐步淘汰和竊盜保險索賠的增加,正促使家庭轉向連網照明和安防系統。供應商之間的競爭仍然激烈,老牌建築自動化公司堅持其安裝管道,而直接面對消費者的專業公司則競相爭奪DIY升級市場。監管合規驅動的需求、日益成熟的Matter標準以及組件價格的下降,共同推動了歐洲智慧家庭市場的中期成長動能。

歐洲智慧家庭市場的趨勢與洞察

歐盟對住宅建築的強制性能源性能要求。

修訂後的《建築能源性能指令》要求所有成員國在2026年前將零排放標準納入本國法律,迫使開發商和住宅在其專案中採用自動化加熱、照明和通風系統。德國的一項法案草案規定,所有在2026年1月之後建造的暖氣系統都必須安裝智慧溫控器;法國則強制要求大規模多用戶住宅引入照明控制系統,這有效地擴大了歐洲智慧家庭市場的規模。將「自動化準備度」納入合規性評估,正在推動從單一功能設備向整合生態系統的轉變,這將使擁有端到端平台的供應商受益。

現有住宅對安防和照明設施升級的需求激增。

德國、法國和英國的保險公司為認證的智慧安防套餐提供5%至15%的保費折扣,使得智慧門鈴和智慧鎖成為一項切實可行的投資,並能在短期內獲得投資回報。同時,歐盟對鹵素燈的禁令加速了LED燈的普及,也自然地推動了智慧燈泡的普及。根據昕諾飛(Signify)的報告顯示,到2025年,三分之一的照明設備將配備智慧模組,而2023年這一比例僅略高於五分之一。這些因素共同推動了現有住宅的維修需求,並使歐洲智慧家庭市場在早期用戶群體之外保持了持續成長。

高昂的初始硬體和安裝成本

一套完整的智慧家庭系統平均售價在3,500歐元至8,000歐元(3,920美元至8,960歐元)之間,專業安裝費用另需1,200歐元至2,500歐元(1,344美元至2,800歐元)。在一些南歐低關稅市場,投資回收期可能長達九年甚至更久,使得中等收入家庭望而卻步。售價低於500歐元(560美元)的模組化入門套件降低了進入門檻,但通常缺乏實現全屋自動化所需的互通性,從而減緩了歐洲智慧家庭市場的快速成長。

細分市場分析

預計到2025年,安防和門禁控制市場將創造68.6億美元的收入,佔歐洲智慧家庭市場佔有率的29.63%,其中暖通空調和氣候控制將以6.73%的複合年成長率推動成長。需要與智慧溫控器整合的補貼熱泵是符合監管要求的投資重點。適用於改造的無線溫控器、預測式鍋爐控制器以及配備多個感測器的空氣處理器,其銷售量目前已超過傳統的單區設備。能源管理設備也受惠於動態定價機制的日益普及。同時,照明控制市場正經歷快速成長,這主要得益於鹵素燈的逐步淘汰計畫和Matter認證的推廣。智慧家電和娛樂設備由於更換週期較長以及用戶普遍認為其便利性不足,成長速度有所放緩。

因此,競爭格局也在改變。Schneider Electric和博世正在將暖通空調、能源和安防系統整合到一個統一的控制面板中,並透過捆綁式解決方案賺取溢價。同時,通用Wi-Fi晶片的普及降低了准入門檻,給專業攝影機製造商的利潤率帶來了壓力。能夠提供整合暖通空調、照明和儀表的統一解決方案的供應商,很可能在歐洲智慧家庭市場的下一波需求浪潮中佔據主導地位。

預計到2025年,維修項目將佔總支出的63.41%。這是因為歐洲有超過2.2億套住宅建於1990年之前。 Thread和Zigbee等無線標準減少了現有建築的鑽孔工作,從而降低了約三分之一的人事費用。儘管如此,在零排放指令和智慧建築標準的推動下,新建築智慧系統市場正以5.94%的強勁複合年成長率成長。在德國和荷蘭,由於強勁的在建工程儲備,新建建築智慧系統的市佔率已超過40%。

專業批發商針對這兩種形式提供差異化的產品線。羅格朗和ABB為不具備網路專業知識的電工提供維修產品線,而博世則為開發商提供預裝導軌。到2031年,維修市場仍將是歐洲智慧家居市場銷售的主要驅動力。然而,隨著智慧建築在歐洲逐漸普及,預計銷售差距將會縮小。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 歐盟範圍內對住宅建築的能源性能要求

- 現有住宅對安防和照明昇級的需求激增。

- 消費者越來越偏好整合式、語音控制的生態系統

- 國家電氣化計畫下的智慧家庭設備補貼

- 用於歷史建築維修的模組化套件的發展

- Dynamic Talf 對家庭能源管理平台的需求

- 市場限制因素

- 高昂的初始硬體和安裝成本

- 對資料隱私和網路安全的持續擔憂

- 協議標準的碎片化阻礙了互通性。

- 認證智慧家庭安裝人員短缺

- 產業價值鏈分析

- 生態系分析

- 監理情勢

- 技術展望

- 主要通訊和連接技術

- 主要行業標準和政策

- 產品創新和對網路安全的關注

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

- 宏觀經濟趨勢對市場的影響

第5章 市場規模與成長預測

- 依產品類型

- 照明控制

- 能源管理設備

- 安全和存取控制

- 智慧娛樂

- 智慧家庭設備

- 暖通空調和空調控制

- 按安裝類型

- 新建工程一體化系統

- 現有住宅的維修和升級

- 透過分銷管道

- 專業人士/安裝人員的頻道

- 零售與電子商務(DIY)

- 透過通訊技術

- Wi-Fi

- Zigbee

- Z-Wave

- 藍牙和低功耗藍牙

- Thread

- 其他通訊技術(EnOcean、Matter、RF 等)

- 透過使用

- 安全保障

- 能源和公用事業管理

- 舒適度和照明

- 娛樂與生活方式

- 健康與長期護理

- 國家

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Signify NV

- Robert Bosch GmbH(Bosch Smart Home)

- Schneider Electric SE

- Legrand SA

- Somfy SA

- ABB Ltd.

- Lutron Electronics Co., Inc.

- TP-Link Deutschland GmbH

- Netatmo SAS

- Eve Systems GmbH

- tado GmbH

- Nuki Home Solutions GmbH

- Fibaro Group SA

- Gira Giersiepen GmbH and Co. KG

- Hager Group

- Devolo GmbH

- Ekinex SpA

- Centrica Hive Limited

- AXIS Communications AB

- Johnson Controls International plc

- Control4 Corporation(Wirepath Home Systems, LLC)

- Ring(Amazon subsidiary)

第7章 市場機會與未來展望

The Europe smart homes market size is projected to expand from USD 23.14 billion in 2025 and USD 24.44 billion in 2026 to USD 32.12 billion by 2031, registering a CAGR of 5.62% between 2026-2031.

Mandated zero-emission construction rules, subsidy-linked heat-pump rollouts, and dynamic power tariffs are repositioning connected devices as regulatory necessities rather than discretionary gadgets. Grid operators across the Nordics and the Netherlands now expose tariff APIs that reward automated load-shifting, accelerating uptake of demand-responsive thermostats and smart chargers. Meanwhile, the halogen-lamp phase-out and rising burglary claim severities are steering households toward networked lighting and security bundles. Vendor rivalry remains intense as building-automation incumbents defend installer channels while direct-to-consumer specialists capture do-it-yourself upgrades. Compliance-anchored demand, a maturing Matter standard, and falling component prices collectively underpin the Europe smart homes market's medium-term momentum.

Europe Smart Homes Market Trends and Insights

EU-wide Energy-Performance Mandates For Residential Buildings

The revised Energy Performance of Buildings Directive compels every member state to transpose zero-emission standards by 2026, forcing developers and homeowners to embed automation for heating, lighting, and ventilation into project scopes. Germany's draft law requires smart thermostats on all new heating systems after January 2026, while France extends mandatory lighting controls to large multifamily blocks, effectively enlarging the addressable Europe smart homes market. Vendors with end-to-end platforms benefit because compliance assessments now score "automation readiness", nudging buyers toward integrated ecosystems rather than single-purpose gadgets.

Surge In Security And Lighting Upgrades Among Existing Homeowners

Insurers across Germany, France, and the United Kingdom offer 5-15% premium rebates for certified smart-security packages, turning doorbells and smart locks into quick-return investments. Concurrently, the EU halogen ban is accelerating LED adoption, giving smart bulbs a natural entry point. Signify reported that one-third of its 2025 luminaires included connectivity modules, up from just over one-fifth in 2023. Together these forces amplify retrofit demand and sustain the Europe smart homes market beyond early adopters.

High Upfront Hardware And Installation Costs

Comprehensive smart-home packages average EUR 3,500-8,000 (USD 3,920-8,960) and professional labor adds EUR 1,200-2,500 (USD 1,344-2,800). Payback stretches beyond nine years in some Southern markets where tariffs are lower, deterring middle-income households. Modular starter kits below EUR 500 (USD 560) soften entry barriers but often lack the interoperability necessary for whole-home automation, tempering immediate growth in the broader Europe smart homes market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Consumer Preference For Integrated, Voice-Controlled Ecosystems

- Smart-Appliance Subsidies Under National Electrification Programs

- Persistent Data-Privacy And Cyber-Security Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Security and access-control delivered USD 6.86 billion of 2025 revenue, equal to 29.63% of the Europe smart homes market share, yet HVAC and climate-control leads growth with a 6.73% CAGR. Subsidy-eligible heat pumps that must couple with smart thermostats position HVAC as the centerpiece of compliance spending. Retrofit-friendly wireless thermostats, predictive boiler controllers, and sensor-rich air handlers now outsell traditional single-zone units. Energy-management devices ride similar tailwinds as dynamic tariffs spread, while lighting controls surge on the back of the halogen withdrawal timetable and Matter certification. Smart appliances and entertainment linger behind because replacement cycles are longer and perceived incremental utility remains thin.

The competitive map is shifting accordingly. Schneider Electric and Bosch integrate HVAC, energy, and security under single dashboards, capturing bundle premiums. Conversely, camera specialists face margin pressure as generic Wi-Fi silicon lowers entry hurdles. Vendors that weld HVAC, lighting, and metering into coherent packages stand to win the next wave of Europe smart homes market demand.

Retrofit projects tallied 63.41% of 2025 spending because more than 220 million European dwellings predate 1990. Wireless Thread and Zigbee kits reduce drilling requirements in heritage structures and cut labor costs by nearly one-third. Nevertheless, zero-emission directives and smart-ready building codes propel new-build smart systems at a brisk 5.94% CAGR. Germany and the Netherlands, buoyed by healthy construction pipelines, already see new-build share crest 40%.

Professional wholesalers stock differentiated lines for the two formats. Legrand and ABB aim retrofit ranges at electricians lacking networking expertise, while Bosch packages premounted rails for developers. Through 2031 retrofit will remain the volume anchor of the Europe smart homes market, yet the revenue gap will narrow as smart-ready construction becomes the continental norm.

The Europe Smart Homes Market is Segmented by Product Type (Lighting Controls, and More), Installation Type (New-Build Integrated Systems and Retrofit/Existing-Home Upgrades), Distribution Channel (Professional/Installer Channel and Retail and E-Commerce), Communication Technology (Wi-Fi, Zigbee, and More), Application (Security and Safety, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Signify N.V.

- Robert Bosch GmbH (Bosch Smart Home)

- Schneider Electric SE

- Legrand SA

- Somfy SA

- ABB Ltd.

- Lutron Electronics Co., Inc.

- TP-Link Deutschland GmbH

- Netatmo SAS

- Eve Systems GmbH

- tado GmbH

- Nuki Home Solutions GmbH

- Fibaro Group S.A.

- Gira Giersiepen GmbH and Co. KG

- Hager Group

- Devolo GmbH

- Ekinex S.p.A.

- Centrica Hive Limited

- AXIS Communications AB

- Johnson Controls International plc

- Control4 Corporation (Wirepath Home Systems, LLC)

- Ring (Amazon subsidiary)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EU-wide Energy-Performance Mandates for Residential Buildings

- 4.2.2 Surge in Security and Lighting Upgrades Among Existing Homeowners

- 4.2.3 Rising Consumer Preference for Integrated, Voice-Controlled Ecosystems

- 4.2.4 Smart-Appliance Subsidies Under National Electrification Programs

- 4.2.5 Growth of Retrofit-Ready Modular Kits for Heritage Housing

- 4.2.6 Dynamic-Tariff Driven Demand for Home Energy-Management Platforms

- 4.3 Market Restraints

- 4.3.1 High Upfront Hardware and Installation Costs

- 4.3.2 Persistent Data-Privacy and Cyber-Security Concerns

- 4.3.3 Fragmented Protocol Standards Hinder Interoperability

- 4.3.4 Shortage of Certified Smart-Home Installers

- 4.4 Industry Value Chain Analysis

- 4.5 Ecosystem Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.7.1 Major Communication and Connectivity Technologies

- 4.7.2 Key Industry Standards and Policies

- 4.7.3 Product Innovations and Cyber-Security Emphasis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Lighting Controls

- 5.1.2 Energy-Management Devices

- 5.1.3 Security and Access-Control

- 5.1.4 Smart Entertainment

- 5.1.5 Smart Appliances

- 5.1.6 HVAC and Climate-Control

- 5.2 By Installation Type

- 5.2.1 New-Build Integrated Systems

- 5.2.2 Retrofit/Existing-Home Upgrades

- 5.3 By Distribution Channel

- 5.3.1 Professional/Installer Channel

- 5.3.2 Retail and E-commerce (DIY)

- 5.4 By Communication Technology

- 5.4.1 Wi-Fi

- 5.4.2 Zigbee

- 5.4.3 Z-Wave

- 5.4.4 Bluetooth and BLE

- 5.4.5 Thread

- 5.4.6 Other Communication Technologies (EnOcean, Matter, RF, etc.)

- 5.5 By Application

- 5.5.1 Security and Safety

- 5.5.2 Energy and Utilities Management

- 5.5.3 Comfort and Lighting

- 5.5.4 Entertainment and Lifestyle

- 5.5.5 Health and Assisted Living

- 5.6 By Country

- 5.6.1 United Kingdom

- 5.6.2 Germany

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Netherlands

- 5.6.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Signify N.V.

- 6.4.2 Robert Bosch GmbH (Bosch Smart Home)

- 6.4.3 Schneider Electric SE

- 6.4.4 Legrand SA

- 6.4.5 Somfy SA

- 6.4.6 ABB Ltd.

- 6.4.7 Lutron Electronics Co., Inc.

- 6.4.8 TP-Link Deutschland GmbH

- 6.4.9 Netatmo SAS

- 6.4.10 Eve Systems GmbH

- 6.4.11 tado GmbH

- 6.4.12 Nuki Home Solutions GmbH

- 6.4.13 Fibaro Group S.A.

- 6.4.14 Gira Giersiepen GmbH and Co. KG

- 6.4.15 Hager Group

- 6.4.16 Devolo GmbH

- 6.4.17 Ekinex S.p.A.

- 6.4.18 Centrica Hive Limited

- 6.4.19 AXIS Communications AB

- 6.4.20 Johnson Controls International plc

- 6.4.21 Control4 Corporation (Wirepath Home Systems, LLC)

- 6.4.22 Ring (Amazon subsidiary)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026年全球智慧冷藏櫃支付市場報告

2026年全球智慧冷藏櫃支付市場報告 環境生活輔助和智慧家庭市場規模、佔有率和成長分析:按組件、應用、最終用戶、分銷管道和地區分類-2026-2033年產業預測全球智慧家庭市場:機會與策略展望(至2035年)2026年全球低軌道(LEO)連結服務管理市場報告

環境生活輔助和智慧家庭市場規模、佔有率和成長分析:按組件、應用、最終用戶、分銷管道和地區分類-2026-2033年產業預測全球智慧家庭市場:機會與策略展望(至2035年)2026年全球低軌道(LEO)連結服務管理市場報告 智慧生活:市場數據概覽(2026 年第二季)

智慧生活:市場數據概覽(2026 年第二季) 智慧家庭系統市場預測至2034年-全球分析(按組件、系統類型、連接方式、技術、應用、最終用戶和地區分類)

智慧家庭系統市場預測至2034年-全球分析(按組件、系統類型、連接方式、技術、應用、最終用戶和地區分類) 智慧家庭市場:2026-2032年全球市場預測(按產品、使用者介面、應用、分銷管道和最終用戶分類)

智慧家庭市場:2026-2032年全球市場預測(按產品、使用者介面、應用、分銷管道和最終用戶分類) 智慧家庭市場規模、佔有率、趨勢和預測:按組件、應用和地區分類,2026-2034 年

智慧家庭市場規模、佔有率、趨勢和預測:按組件、應用和地區分類,2026-2034 年 智慧家庭支付市場:按組件、支付方式、應用和地區分類2026年全球單戶智慧家庭市場報告

智慧家庭支付市場:按組件、支付方式、應用和地區分類2026年全球單戶智慧家庭市場報告