|

市場調查報告書

商品編碼

2043841

歐洲零售業分析:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Europe Retail Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

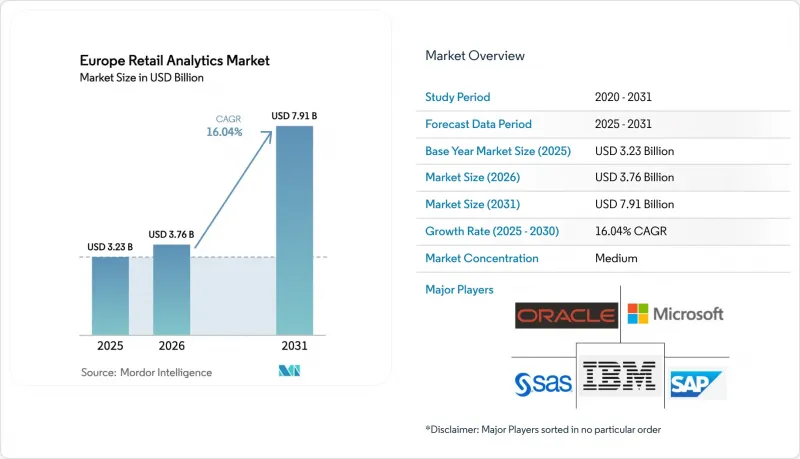

歐洲零售分析市場預計到 2025 年將達到 32.3 億美元,到 2026 年將達到 37.6 億美元,到 2031 年將達到 79.1 億美元,2026 年至 2031 年的複合年成長率為 16.04%。

第一方數據平台投資激增、通膨壓力下利潤率承壓以及統一商務的需求,正在加速全部區域的平台現代化進程。隨著零售商採用即時定價和電腦視覺相關工作負載,將彈性運算與先進人工智慧相結合的雲端原生服務正日益受到青睞。對隱私增強技術的日益依賴,促使企業加強對那些從設計階段就整合使用者授權管理和可解釋性功能的供應商的投入。同時,隨著現有ERP供應商將分析功能整合到核心工作流程中,以及資料平台專家透過開放架構和符合歐盟資料居住要求來脫穎而出,競爭日益激烈。

歐洲零售分析市場的趨勢與洞察

數據驅動的個人化能夠提高店內轉換率。

歐洲零售連鎖店正將預測模型整合到自助服務終端、行動應用程式和POS終端中,以展示個人化優惠,從而提高購買金額和回頭客數量。 Adobe 2024年的基準研究顯示,整合客戶數據平台使時尚和食品雜貨行業的轉換率提高了20%至30%。隨著GDPR「價值交換」概念的引入,這種個人化正從單純的差異化優勢轉變為一項競爭要求。畢馬威的一份報告指出,68%的零售商計劃在2026年增加其人工智慧主導的個人化預算。 「基於代理商的商務」試點計畫(即人工智慧代理商代表消費者協商產品組合和付款方式)將進一步提高即時使用者畫像的要求。隨著取得資料共用授權變得越來越困難,企業必須展現出實際的好處才能維繫與客戶的第一方關係。

人工智慧定價引擎最佳化了通貨膨脹的歐洲的利潤率。

通貨膨脹的波動迫使食品雜貨店和服裝零售商用演算法取代每週的價格週期,這些演算法每天多次調整庫存價格。根據麥肯錫2025年食品雜貨業調查,實施這些演算法的公司在2024年生活成本高企時期,毛利率提高了1-2個百分點。最新的演算法引擎會收集競爭對手數據、天氣資訊和當地活動訊息,以最佳化折扣方案,同時確保品牌形像不受損害。波士頓顧問公司(BCG)預測,如果透明度措施能夠緩解監管機構和消費者的擔憂,到2027年,利潤增加可能達到100億至150億歐元(113億至169億美元)。供應商目前正在打包可解釋性儀表板,以符合歐盟人工智慧法案(AI-Act)的資訊揭露要求。

透過GDPR和ePrivacy法規加強資料隱私保護

提案的《電子隱私條例》擴大了對 Cookie、裝置指紋識別和位置分析的明確同意要求,並限制使用第三方識別碼來支援個人化和歸因模型。歐盟委員會預測,到 2025 年,拒絕追蹤同意的比例將達到 62%,這將縮小宣傳活動的覆蓋範圍。 《一般資料保護規範》(GDPR) 第 22 條引入了自動化決策中的「人機互動」義務,減緩了動態定價的普及。零售商正在試行差分隱私、聯邦學習和合成資料集,但由於缺乏成熟的工具,成本和複雜性都在增加。

細分市場分析

到 2025 年,雲端將佔據歐洲零售分析市場 63.13% 的佔有率。這反映了即時定價和視覺工作負載向可擴展基礎架構的持續轉變。遷移到公共雲端也將託管人工智慧、災害復原和多區域複製等功能引入市場,從而降低硬體更換週期的總體擁有成本 (TCO)。對於食品零售商而言,尤其是德國和法國的零售商,本地部署環境仍然不可或缺,因為他們仍然受到傳統 ERP 系統和嚴格的資料居住要求的困擾。混合架構正逐漸成為一種合規解決方案,它允許敏感交易保留在本地,同時在雲端運行高負載的分析批次。微軟的 2025 年混合 SKU 可將 POS 資料同步至 Azure Synapse,而無需完全遷移。 Snowflake 的 2024 年資料居住管理功能可讓零售商透過單一介面查詢分散式資料倉儲,從而規避歐盟《一般資料保護規則》(GDPR) 第 44 條規定的跨境資料傳輸障礙。

提升系統彈性使零售商能夠透過在定價或影像處理工作負載高峰期啟動GPU叢集並在高峰期關閉叢集來顯著降低閒置成本。供應商透過為多年雲端合約提供授權折扣來促進向SAP和Oracle的遷移,從而有效地為遷移專案提供資金。因此,儘管預計到2031年,由雲端運算驅動的歐洲零售分析市場規模將進一步擴大領先優勢,但混合拓樸結構在受監管產業正逐漸獲得發展動力。隨著零售商將邊緣運算節點整合到門市中,混合拓撲結構將成為既需要低延遲的店內處理又需要雲端規模訓練週期的工作負載的主流選擇。

預計到2025年,行銷和客戶洞察套件將佔銷售額的27.54%,顯示市場對個人化和零售媒體衡量指標的需求持續強勁。然而,供應鏈和履約工具的成長速度最快,複合年成長率高達18.02%,這主要得益於自動補貨和最後一公里最佳化引擎釋放了營運資金。 Zalando在實施基於人工智慧的需求預測後,庫存過剩減少了15%,庫存準確率達到了98%。Accenture報告稱,其客戶已將安全庫存減少了10-20%,釋放了資金用於數位化領域的再投資。預計到2031年,與供應鏈模組相關的歐洲零售分析市場規模將超過傳統的商品組合規劃套件市場規模。由於相機價格下降以及ESG框架下對食品廢棄物報告的需求,結合電腦視覺和庫存損耗分析的損失預防方案正日益受到關注。

零售商採用新技術的速度取決於其成熟度。垂直整合的時尚公司專注於最佳化商品分配和降價以維持品牌價值,而連鎖超市則優先考慮需求預測以減少生鮮食品浪費。由於數十年來根深蒂固的商業規則,品類管理套件的用戶留存率很高,這限制了它們與新興的AI優先產品相比的成長。同時,整合了損益表和營運指標的財務績效儀表板,透過將多個傳統BI系統整合到單一視圖中,簡化了決策者的工作流程。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 數據驅動的個人化能夠提高店內轉換率。

- 人工智慧定價引擎最佳化了通貨膨脹的歐洲市場的利潤率。

- 邊緣分析在即時庫存監控中的應用

- 統一商務需要對客戶有一個統一的視野。

- 透過零售媒體網路分析開發新的收入來源

- 電腦視覺整合的符合ESG標準的收縮分析

- 市場限制因素

- 零售業資料科學人才短缺

- 根據GDPR和ePrivacy法規加強資料隱私保護

- 傳統POS系統的碎片化阻礙了資料整合。

- 中小零售商凍結資本投資

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按實現類型

- 現場

- 雲

- 混合

- 按功能

- 策略與規劃

- 行銷和客戶洞察

- 財務管理

- 門市營運和損失預防

- 商品行銷及品類最佳化

- 供應鍊和履約

- 按公司規模

- 小型企業

- 大公司

- 按零售業態

- 實體店面

- 電子商務

- 全通路零售

- 國家

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SAP SE

- Oracle Corporation

- IBM Corporation

- SAS Institute Inc.

- Microsoft Corporation

- Fractal Analytics

- Tableau Software LLC

- MicroStrategy Incorporated

- Sensormatic Solutions

- Alteryx Inc.

- RetailNext Inc.

- Blue Yonder GmbH

- NielsenIQ

- ThoughtSpot Inc.

- Sisense Ltd.

- Domo Inc.

- Looker Data Sciences(Google)

- Snowflake Inc.

- Databricks Inc.

- C3.ai Inc.

第7章 市場機會與未來展望

The Europe retail analytics market size is projected to be USD 3.23 billion in 2025, USD 3.76 billion in 2026, and reach USD 7.91 billion by 2031, growing at a CAGR of 16.04% from 2026 to 2031.

Surging investment in first-party data platforms, inflation-era margin pressure, and unified commerce mandates are accelerating platform renewals across the region. Cloud-native services that blend elastic compute with advanced AI are increasingly preferred as merchants deploy real-time pricing and computer-vision workloads. Growing reliance on privacy-enhancing technologies is steering spending toward vendors that embed consent management and explainability features by design. Competitive intensity, meanwhile, is rising as ERP incumbents embed analytics into core workflows and data-platform specialists differentiate on open architecture and EU data-residency options.

Europe Retail Analytics Market Trends and Insights

Data-Driven Personalization Lifts In-Store Conversion

European chains are embedding predictive models into kiosks, mobile apps, and point-of-sale terminals to surface individualized offers that lift basket size and drive repeat visits. Adobe's 2024 benchmarking found that unified customer-data platforms improved fashion and grocery conversion rates by 20%-30%. GDPR's value-exchange ethos makes such personalization a competitive necessity rather than a differentiator. KPMG reported that 68% of retailers plan to boost AI-led personalization budgets by 2026. Agentic commerce pilots, where AI agents negotiate bundles and payments on a shopper's behalf, will further intensify real-time profile requirements. As data-sharing consent becomes harder to secure, merchants must showcase tangible benefits to retain first-party relationships.

AI-Powered Pricing Engines Optimize Margin in Inflationary Europe

Inflation volatility pushed grocers and fashion retailers to replace weekly price cycles with algorithms that recalibrate shelf prices several times per day. McKinsey's 2025 grocery study documented 1-2 percentage-point gross-margin lifts among adopters during the 2024 cost-of-living squeeze. Modern engines ingest competitor feeds, weather updates, and local events, then optimize markdown calendars while guarding brand perception. BCG forecasts EUR 10 billion-EUR 15 billion (USD 11.3 billion-USD 16.9 billion) in incremental margin by 2027, provided transparency safeguards assuage regulator and consumer concerns. Vendors now bundle explainability dashboards to comply with EU AI-Act disclosure clauses.

Data-Privacy Tightening Under GDPR and ePrivacy Regulation

Proposed ePrivacy rules broaden explicit-consent demands for cookies, device fingerprinting, and location analytics, curtailing third-party identifiers that feed personalization and attribution models. The European Commission recorded a 62% refusal rate for tracking consent in 2025, shrinking campaign reach. Article 22 of GDPR introduces human-in-the-loop mandates for automated decision-making, slowing dynamic pricing rollouts. Retailers are piloting differential privacy, federated learning, and synthetic datasets, but lack of mature tooling raises cost and complexity.

Other drivers and restraints analyzed in the detailed report include:

- Unified Commerce Mandates Single View of Customer

- Proliferation of Edge Analytics for Real-Time Shelf Monitoring

- Shortage of Retail Data-Science Talent Pool

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud captured 63.13% of Europe retail analytics market share in 2025, reflecting merchants' shift toward scalable infrastructure for real-time pricing and vision workloads. Public-cloud migration also unlocks managed AI, disaster recovery, and multi-region replication, reducing total cost of ownership for mid-cycle hardware refreshes. On-premise estates persist among grocers with legacy ERP and stringent data-residency contracts, notably in Germany and France. Hybrid architectures are emerging as a compliance hedge, allowing sensitive transactions to stay on-premise while heavy analytics batches run in the cloud. Microsoft's 2025 hybrid SKU syncs point-of-sale data to Azure Synapse without full migration. Snowflake's 2024 residency controls let merchants query distributed warehouses through one interface, sidestepping Article 44 cross-border hurdles.

Greater elasticity means retailers can spin up GPU clusters during peak pricing or vision workloads, then shut them down, slashing idle costs. Vendors incentivize the transition to SAP and Oracle by discounting licenses for multi-year cloud terms, effectively funding migration projects. The Europe retail analytics market size attributable to cloud is thus forecast to widen its lead through 2031, while hybrid gains incremental traction among regulated sectors. As retailers embed edge-compute nodes inside stores, hybrid topologies will likely dominate workloads requiring both in-store latency and cloud-scale training cycles.

Marketing and customer insight suites held 27.54% revenue in 2025, underscoring continued appetite for personalization and retail-media measurement. Yet supply-chain and fulfillment tools are expanding fastest at an 18.02% CAGR, driven by autonomous replenishment and last-mile optimization engines that release working capital. Zalando cut overstock by 15% and achieved 98% in-stock accuracy after rolling out AI-based demand sensing. Accenture recorded 10%-20% safety-stock reductions among adopters, freeing cash for digital reinvestment. The Europe retail analytics market size attached to supply-chain modules is expected to outstrip legacy assortment-planning suites through 2031. Loss-prevention solutions fusing computer vision with shrinkage analytics are gaining ground as camera prices drop and ESG frameworks demand food-waste reporting.

Adoption trajectories differ by retailer maturity. Vertically integrated fashion houses focus on allocation and markdown optimization to preserve brand equity, while grocery chains prioritize demand forecasting to curb perishables. Category-management suites remain sticky because decades-old business rules are hard-wired, capping their growth relative to newer AI-first products. Meanwhile, financial-performance dashboards that blend P&L with operational metrics are consolidating multiple legacy BI stacks into single views, streamlining decision-maker workflows.

The Europe Retail Analytics Market Report is Segmented by Mode of Deployment (On-Premise, Cloud, and Hybrid), Module Type (Strategy and Planning, Marketing and Customer Insights, and More), Business Size (Small and Medium Enterprises, and Large Enterprises), Retail Format (Brick-And-Mortar, E-Commerce, and Omnichannel Retail), and Country (Germany, Italy, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- SAP SE

- Oracle Corporation

- IBM Corporation

- SAS Institute Inc.

- Microsoft Corporation

- Fractal Analytics

- Tableau Software LLC

- MicroStrategy Incorporated

- Sensormatic Solutions

- Alteryx Inc.

- RetailNext Inc.

- Blue Yonder GmbH

- NielsenIQ

- ThoughtSpot Inc.

- Sisense Ltd.

- Domo Inc.

- Looker Data Sciences (Google)

- Snowflake Inc.

- Databricks Inc.

- C3.ai Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Data-Driven Personalization Lifts In-Store Conversion

- 4.2.2 AI-Powered Pricing Engines Optimise Margin in Inflationary Europe

- 4.2.3 Proliferation of Edge Analytics for Real-Time Shelf Monitoring

- 4.2.4 Unified Commerce Mandates Single View of Customer

- 4.2.5 Retail Media Network Analytics Unlocking Incremental Revenue Streams

- 4.2.6 ESG-Aligned Shrinkage Analytics Integrating Computer Vision

- 4.3 Market Restraints

- 4.3.1 Shortage of Retail Data-Science Talent Pool

- 4.3.2 Data-Privacy Tightening Under GDPR and ePrivacy Regulation

- 4.3.3 Legacy POS Fragmentation Impedes Data Integration

- 4.3.4 Capital-Expenditure Freeze Among SME Retailers

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Mode of Deployment

- 5.1.1 On-Premise

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By Module Type

- 5.2.1 Strategy and Planning

- 5.2.2 Marketing and Customer Insights

- 5.2.3 Financial Management

- 5.2.4 Store Operations and Loss Prevention

- 5.2.5 Merchandising and Category Optimisation

- 5.2.6 Supply-Chain and Fulfilment

- 5.3 By Business Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By Retail Format

- 5.4.1 Brick-and-Mortar

- 5.4.2 E-Commerce

- 5.4.3 Omnichannel Retail

- 5.5 By Country

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 IBM Corporation

- 6.4.4 SAS Institute Inc.

- 6.4.5 Microsoft Corporation

- 6.4.6 Fractal Analytics

- 6.4.7 Tableau Software LLC

- 6.4.8 MicroStrategy Incorporated

- 6.4.9 Sensormatic Solutions

- 6.4.10 Alteryx Inc.

- 6.4.11 RetailNext Inc.

- 6.4.12 Blue Yonder GmbH

- 6.4.13 NielsenIQ

- 6.4.14 ThoughtSpot Inc.

- 6.4.15 Sisense Ltd.

- 6.4.16 Domo Inc.

- 6.4.17 Looker Data Sciences (Google)

- 6.4.18 Snowflake Inc.

- 6.4.19 Databricks Inc.

- 6.4.20 C3.ai Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

零售分析市場:按組件、功能、組織規模、最終用戶和部署方法分類-2026-2032年全球市場預測

零售分析市場:按組件、功能、組織規模、最終用戶和部署方法分類-2026-2032年全球市場預測 零售分析市場報告:按功能、組件、部署模式、最終用戶和地區分類(2026-2034 年)

零售分析市場報告:按功能、組件、部署模式、最終用戶和地區分類(2026-2034 年) 零售分析市場:按組件、部署模式、應用和區域分類

零售分析市場:按組件、部署模式、應用和區域分類 全球零售分析市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球零售分析市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球零售分析軟體與服務市場報告2026年全球零售分析市場報告零售分析市場規模、佔有率、成長率和全球行業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

2026年全球零售分析軟體與服務市場報告2026年全球零售分析市場報告零售分析市場規模、佔有率、成長率和全球行業分析:按類型、應用和地區分類的洞察,2026-2034 年預測 零售分析市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、最終用戶、部署類型、功能和解決方案分類

零售分析市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、最終用戶、部署類型、功能和解決方案分類 零售分析市場 - 全球產業規模、佔有率、趨勢、機會、預測(按組件、部署模式、應用、地區和競爭格局分類),2021-2031年

零售分析市場 - 全球產業規模、佔有率、趨勢、機會、預測(按組件、部署模式、應用、地區和競爭格局分類),2021-2031年 2026-2030年全球零售分析市場

2026-2030年全球零售分析市場