|

市場調查報告書

商品編碼

2043831

流程自動化:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Process Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

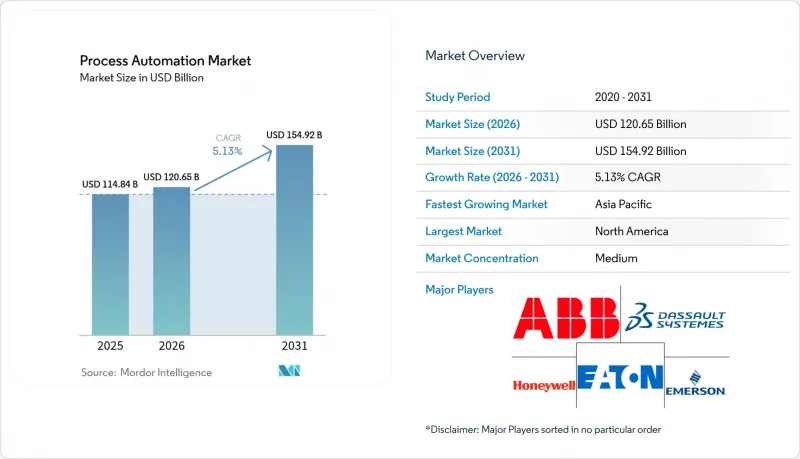

預計製程自動化市場將從 2025 年的 1,148.4 億美元和 2026 年的 1,206.5 億美元成長到 2031 年的 1,549.2 億美元,2026 年至 2031 年的複合年成長率為 5.13%。

這一成長曲線反映了維護方式從被動式向預測式、軟體定義控制架構的廣泛轉變,後者在邊緣整合了人工智慧。資本投資正從週期性的硬體升級轉向基於訂閱的製造執行平台,從而縮短了獲得洞察的時間。諸如藥品序列化和煉油廠廢氣回收等合規性要求,持續加速數位雙胞胎技術的應用。同時,石化公司正在對分散式控制系統 (DCS)維修,以最佳化波動性較大的原料產率。營運技術 (OT) 與雲端原生分析的整合也擴大了邊緣閘道器和安全連接層的目標市場。

全球流程自動化市場趨勢與洞察

擴大機器人技術的應用

2024年,工業機器人的部署數量達到553,052台,其中亞太地區佔73%。協作機器人目前正用於處理危險物質和進行無菌填充,在確保符合嚴格的暴露限值的同時,減少了工傷事故。由於偏遠石化廠勞動力短缺,營運商正在部署配備機器視覺系統的機器人進行法蘭檢測和閥門操作。一項聯合研究發現,將機器人技術與數位雙胞胎仿真相結合,可以將新產品的量產時間縮短22%。在製藥業,人形機器人的初步初步試驗正在無塵室中進行,這些機器人能夠在隔離器之間運輸物料,而不會影響A級潔淨室的環境條件。

人們越來越關注能源效率和成本降低。

歐盟已撥款1500億歐元(約1695億美元)在2040年前實現重工業脫碳,並專門撥款用於變頻驅動器等設備升級。美國能源局指出,製造業能源消耗的68%來自製程加熱,建議在爐窯中引入模型預測控制。根據供應商報告,人工智慧驅動的溫度控管軟體的應用已使天然氣消耗量降低了14%,並在不到18個月的時間內實現了投資回報。與獨立平台相比,直接連接到分散式控制網路的整合式能源管理系統已成功將公用事業成本降低了19%。

初始投資高且整合複雜

由於協議不一致等意外情況,棕地自動化專案通常超出預算30%至40%。儘管潛在回報可觀,但62%的北美工廠表示資金限制是阻礙計畫實施的因素。多供應商環境加劇了複雜性,系統整合商的工時費自2024年以來上漲了18%。營運商正在考慮採用雲端訂閱服務將資本支出(CapEx)轉化為營運支出(OpEx),但在數據主權法規嚴格的地區,人們仍然對此持懷疑態度。

細分市場分析

在製程自動化市場中,製造執行系統 (MES) 的成長速度最快,年複合成長率高達 5.29%,這主要得益於製藥和食品生產中序號追溯和批次溯源從「可選」轉變為「強制」。可程式邏輯控制器 (PLC) 在核心馬達和閥門迴路中仍保持著 27.63% 的市場佔有率,但隨著人們對軟體定義控制的認知不斷提高,PLC 正面臨著商品化帶來的壓力。

在煉油等連續運作的行業中,分散式控制系統 (DCS) 仍然至關重要,因為這些產業需要跨數百個迴路實現統一的歷史資料存取和簡化的警報功能。監控與資料擷取 (SCADA) 平台涵蓋地理位置分散的管道和水處理設施,而平板電腦和擴增實境 (AR) 頭顯等邊緣原生人機介面 (HMI) 則可減輕操作員的工作負荷。西門子發布的整合式 PCS neo 標誌著控制和安全功能在虛擬化主幹網路上的整合趨勢,從而減少了控制面板的面積並簡化了備件管理。

到2025年,有線乙太網路、現場匯流排和光纖鏈路憑藉其確定性延遲和電磁抗擾性,仍將佔據製程自動化市場63.72%的主導佔有率。受5G專用網路切片部署的推動,無線連線預計將以5.18%的複合年成長率成長。這些網路切片可保證低於10毫秒的服務延遲,這對於實現移動機器人和擴增實境(AR)維護等進階應用至關重要。

WirelessHART 和 ISA100.11a 支援對現有基礎設施改裝棕地,無需重新佈線,為預算有限的營運商提供了一條極具吸引力的遷移路徑。時間敏感網路 (TSN) 透過微秒同步端點,連接了有線和無線網路,其有效性已在跨廠商測試平台上得到驗證,並展現出伺服級效能。隨著網路安全監控的加強,無線節點現在標配 WPA3 加密和憑證管理功能,從而彌合了有線和無線網路在安全意識方面的差距。

區域分析

預計到2025年,北美將佔全球銷售額的33.28%,這主要得益於墨西哥灣沿岸地區石化工廠的維修以及由《基礎設施投資與就業法案》資助的供水事業SCADA系統的升級。 90年代引進的控制系統基礎設施正日趨成熟,即將停止支持,因此需要轉向採用加密協定和零信任分段的系統。加拿大油砂業者正在對蒸汽注入法(SAGD)技術進行邊緣分析,以在亨利港天然氣價格超過每百萬英熱單位3美元時降低天然氣需求。墨西哥的航太和汽車產業叢集正在美墨加協定框架下實施製造執行系統(MES),以確保原產地規則的可追溯性。

預計到2031年,亞太地區將以5.44%的複合年成長率成長,這主要得益於中國「十四五」規劃的推動,該規劃已認證了超過2100家「燈塔工廠」。印度的生產連結獎勵計畫正在津貼製藥和食品產業的自動化,加速中小企業採用自動化技術。日本的「社會5.0」計畫正在利用協作機器人和擴增實境(AR)頭顯來緩解勞動力短缺問題,因為65歲及以上的人口占日本總人口的29%。韓國半導體製造廠正在3奈米製程節點上實施先進的製程控制,證明在整合乙太網路骨幹網路上實現確定性閉迴路是可行的。

在歐洲,「清潔工業協議」和「網路韌性法案」草案正在推動能源監測和網路安全設計的強制性實施。德國2025年的預算包括100億歐元(113億美元)用於變頻驅動器和熱回收項目。英國的「先進製造計畫」為數位雙胞胎提供創新融資,目標是到2040年實現製造業淨零排放。南美洲、中東和非洲在實施上相對滯後,但沙烏地阿拉伯的NEOM和巴西的深海鹽鹽層下油田等大型企劃正在進行中,這些計畫從一開始就必須符合IEC 62443標準。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 機器人技術的廣泛應用

- 人們越來越關注能源效率和成本降低。

- 工業物聯網(IIoT)的興起

- 安全自動化系統的需求

- 人工智慧驅動的預測性維護平台的興起

- 推動制定碳中和製造法規

- 市場限制因素

- 初始投資大,整合難度高

- OT網路中的網路安全漏洞

- 特定領域自動化人員短缺

- 現有設施(棕地)互通性的陷阱

- 產業生態系分析

- 宏觀經濟因素的影響

- 監理情勢

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 依系統類型

- 監控與數據採集(SCADA)

- 可程式邏輯控制器(PLC)

- 分散式控制系統(DCS)

- 製造執行系統(MES)

- 閥門和執行器

- 電動機

- 人機介面(HMI)

- 製程安全系統

- 感測器和發送器

- 其他系統類型

- 透過通訊協定

- 有線協議

- 無線協定

- 按最終用戶行業分類

- 化工/石油化工

- 紙漿和紙漿

- 用水和污水處理

- 能源與公共產業

- 石油和天然氣

- 製藥

- 食品/飲料

- 其他終端用戶產業

- 部署模式

- 現場

- 基於雲端的

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 義大利

- 英國

- 法國

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ABB Ltd.

- Dassault Systemes SE

- Eaton Corporation plc

- Emerson Electric Co.

- Honeywell International Inc.

- Johnson Controls International plc

- Mitsubishi Electric Corporation

- Bosch Rexroth AG

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Texas Instruments Inc.

- Yokogawa Electric Corporation

- FANUC Corporation

- KUKA Aktiengesellschaft

- OMRON Corporation

- Keyence Corporation

- General Electric Company

- SEW-Eurodrive GmbH and Co. KG

- Phoenix Contact GmbH and Co. KG

- Advantech Co., Ltd.

- WAGO Kontakttechnik GmbH and Co. KG

- Beckhoff Automation GmbH and Co. KG

第7章 市場機會與未來展望

The process automation market size is projected to expand from USD 114.84 billion in 2025 and USD 120.65 billion in 2026 to USD 154.92 billion by 2031, registering a 5.13% CAGR between 2026 to 2031.

The growth curve reflects a broad pivot from reactive maintenance toward predictive, software-defined control architectures that embed artificial intelligence at the edge. Capital budgets are shifting away from cyclic hardware replacements and toward subscription-based manufacturing execution platforms that shorten time-to-insight. Compliance mandates such as pharmaceutical serialization and refinery flare-gas recovery continue to accelerate digital-twin adoption, while petrochemical operators retrofit distributed control systems to optimize volatile feedstock yields. Convergence of operational technology with cloud-native analytics is also expanding the addressable base for edge gateways and secure connectivity layers.

Global Process Automation Market Trends and Insights

Rising Adoption of Robotics

Industrial robot installations hit 553,052 units in 2024, with Asia Pacific accounting for 73% of deployments. Collaborative robots now handle hazardous materials and aseptic fills, reducing ergonomic injuries while maintaining compliance with stringent exposure limits. Talent shortages in remote petrochemical hubs are prompting operators to assign machine-vision-equipped robots to flange inspection and valve actuation. A joint study found that pairing robotics with digital-twin simulations accelerates new-product ramp-up by 22%. Early pilots of humanoid robots in pharmaceutical cleanrooms are underway, with the robots moving items between isolators without breaching Grade A conditions.

Growing Emphasis on Energy Efficiency and Cost Reduction

The European Union earmarked EUR 150 billion (USD 169.5 billion) to decarbonize heavy industry by 2040, explicitly funding upgrades such as variable-frequency drives. The United States Department of Energy identified process heating as 68% of manufacturing energy use and recommended model-predictive control for furnaces. Deployments of AI-driven thermal-management software have cut natural-gas consumption by 14% and delivered payback in less than 18 months, according to vendor filings. Integrated energy-management systems tied directly to distributed control networks have achieved 19% utility savings compared with standalone platforms.

High Initial Capital and Integration Complexity

Brownfield automation projects routinely exceed budgets by 30-40% due to unforeseen protocol mismatches, prompting 62% of North American plants to cite capital constraints as a barrier, despite attractive paybacks. Multi-vendor environments magnify complexity, and hourly rates for system integrators have climbed 18% since 2024. Operators are weighing cloud subscriptions that convert CapEx to OpEx, yet skepticism persists in jurisdictions with strict data-sovereignty rules.

Other drivers and restraints analyzed in the detailed report include:

- Emergence of Industrial Internet of Things (IIoT)

- Demand for Safety Automation Systems

- Cybersecurity Vulnerabilities in OT Networks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing execution systems experienced the fastest growth trajectory in the process automation market, expanding at a 5.29% CAGR as serial-number traceability and lot genealogy move from optional to mandatory in pharmaceuticals and food production. Programmable logic controllers safeguard their 27.63% market share in core motor and valve loops, yet face commoditization pressure as software-defined control gains mindshare.

Distributed control systems remain indispensable in continuous operations such as refining, where hundreds of loops demand unified historian access and alarm rationalization. Supervisory control and data acquisition platforms cover geographically dispersed pipelines and water utilities, while edge-native human-machine interfaces on tablets and AR headsets trim operator workload. Siemens' unified PCS neo release exemplifies the push to consolidate control and safety functions on a virtualized backbone, thereby shrinking cabinet footprints and simplifying spares management.

Wired Ethernet, fieldbus, and fiber links maintained a dominant 63.72% share of the process automation market in 2025, thanks to deterministic latency and electromagnetic immunity. Wireless connections are projected to grow at a compound annual growth rate (CAGR) of 5.18%, driven by the adoption of private 5G slices. These slices provide guaranteed sub-10-millisecond service levels, which are critical for enabling advanced applications such as mobile robotics and augmented reality (AR) maintenance.

WirelessHART and ISA100.11a support brownfield retrofits without recabling, offering migration paths that appeal to cash-constrained operators. Time-sensitive networking bridges wired and wireless domains by synchronizing endpoints within microseconds, validated in a cross-vendor testbed that delivered servo-class performance. Heightened cybersecurity scrutiny means wireless nodes now ship with WPA3 encryption and certificate management baked in, mitigating the perception gap between copper and air.

The Process Automation Market Report is Segmented by System Type (Valves and Actuators, Electric Motors, and More), Communication Protocol (Wired Protocol, and Wireless Protocol), End-User Industry (Chemical and Petrochemical, Paper and Pulp, Water and Wastewater Treatment, Oil and Gas, Pharmaceutical, and More), Deployment Mode (On-Premise, and Cloud-Based), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 33.28% of 2025 revenue, anchored by petrochemical retrofits along the Gulf Coast and water-utility SCADA upgrades funded by the Infrastructure Investment and Jobs Act. A maturing installed base of 1990-era control systems is approaching end-of-support, driving replacements that incorporate encrypted protocols and zero-trust segmentation. Canada's oil-sands operators apply edge analytics to steam-assisted gravity drainage, trimming natural-gas demand when Henry Hub prices spike above USD 3 per MMBtu. Mexico's aerospace and automotive clusters deploy manufacturing execution systems for rules-of-origin traceability under the USMCA framework.

Asia Pacific will expand at a 5.44% CAGR through 2031, propelled by China's 14th Five-Year Plan, which has already certified more than 2,100 lighthouse factories. India's production-linked incentives subsidize automation in pharmaceuticals and food, speeding adoption among small and medium-sized firms. Japan's Society 5.0 vision taps collaborative robots and AR headsets to mitigate labor shortages amid a population that is 29% over 65 years old. South Korea's semiconductor fabs implement advanced process control at 3-nanometer nodes, demonstrating that deterministic loop closure is achievable on converged Ethernet backbones.

Europe enforces energy-monitoring and cybersecurity-by-design mandates via the Clean Industrial Deal and the draft Cyber Resilience Act. Germany's 2025 budget channels EUR 10 billion (USD 11.3 billion) into variable-frequency drives and heat-recovery schemes. The United Kingdom's Advanced Manufacturing Plan offers innovation loans for digital twins, aiming to achieve net-zero manufacturing outcomes by 2040. South America, the Middle East, and Africa trail in installed base yet host megaprojects such as Saudi Arabia's NEOM and Brazil's deepwater presalt fields, which specify IEC 62443 compliance from day one.

- ABB Ltd.

- Dassault Systemes SE

- Eaton Corporation plc

- Emerson Electric Co.

- Honeywell International Inc.

- Johnson Controls International plc

- Mitsubishi Electric Corporation

- Bosch Rexroth AG

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Texas Instruments Inc.

- Yokogawa Electric Corporation

- FANUC Corporation

- KUKA Aktiengesellschaft

- OMRON Corporation

- Keyence Corporation

- General Electric Company

- SEW-Eurodrive GmbH and Co. KG

- Phoenix Contact GmbH and Co. KG

- Advantech Co., Ltd.

- WAGO Kontakttechnik GmbH and Co. KG

- Beckhoff Automation GmbH and Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Robotics

- 4.2.2 Growing Emphasis on Energy Efficiency and Cost Reduction

- 4.2.3 Emergence of Industrial Internet of Things (IIoT)

- 4.2.4 Demand for Safety Automation Systems

- 4.2.5 Rise of AI-Driven Predictive Maintenance Platforms

- 4.2.6 Regulatory Push Toward Carbon-Neutral Manufacturing

- 4.3 Market Restraints

- 4.3.1 High Initial Capital and Integration Complexity

- 4.3.2 Cybersecurity Vulnerabilities in OT Networks

- 4.3.3 Shortage of Domain-Specific Automation Talent

- 4.3.4 Legacy Brownfield Interoperability Pitfalls

- 4.4 Industry Ecosystem Analysis

- 4.5 Impact of Macroeconomic Factors

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By System Type

- 5.1.1 Supervisory Control and Data Acquisition (SCADA)

- 5.1.2 Programmable Logic Controller (PLC)

- 5.1.3 Distributed Control System (DCS)

- 5.1.4 Manufacturing Execution System (MES)

- 5.1.5 Valves and Actuators

- 5.1.6 Electric Motors

- 5.1.7 Human Machine Interface (HMI)

- 5.1.8 Process Safety Systems

- 5.1.9 Sensors and Transmitters

- 5.1.10 Other System Types

- 5.2 By Communication Protocol

- 5.2.1 Wired Protocol

- 5.2.2 Wireless Protocol

- 5.3 By End-User Industry

- 5.3.1 Chemical and Petrochemical

- 5.3.2 Paper and Pulp

- 5.3.3 Water and Wastewater Treatment

- 5.3.4 Energy and Utilities

- 5.3.5 Oil and Gas

- 5.3.6 Pharmaceutical

- 5.3.7 Food and Beverages

- 5.3.8 Other End-User Industries

- 5.4 By Deployment Mode

- 5.4.1 On-premise

- 5.4.2 Cloud-based

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 Italy

- 5.5.3.3 United Kingdom

- 5.5.3.4 France

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ABB Ltd.

- 6.4.2 Dassault Systemes SE

- 6.4.3 Eaton Corporation plc

- 6.4.4 Emerson Electric Co.

- 6.4.5 Honeywell International Inc.

- 6.4.6 Johnson Controls International plc

- 6.4.7 Mitsubishi Electric Corporation

- 6.4.8 Bosch Rexroth AG

- 6.4.9 Rockwell Automation Inc.

- 6.4.10 Schneider Electric SE

- 6.4.11 Siemens AG

- 6.4.12 Texas Instruments Inc.

- 6.4.13 Yokogawa Electric Corporation

- 6.4.14 FANUC Corporation

- 6.4.15 KUKA Aktiengesellschaft

- 6.4.16 OMRON Corporation

- 6.4.17 Keyence Corporation

- 6.4.18 General Electric Company

- 6.4.19 SEW-Eurodrive GmbH and Co. KG

- 6.4.20 Phoenix Contact GmbH and Co. KG

- 6.4.21 Advantech Co., Ltd.

- 6.4.22 WAGO Kontakttechnik GmbH and Co. KG

- 6.4.23 Beckhoff Automation GmbH and Co. KG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026年全球零接觸配置市場報告2026年全球工業製程自動化及控制系統市場報告2026年全球流程自動化與儀器市場報告

2026年全球零接觸配置市場報告2026年全球工業製程自動化及控制系統市場報告2026年全球流程自動化與儀器市場報告 流程自動化和儀器市場:按技術、最終用戶、儀器類型、自動化類型、國家和地區分類-全球產業分析、市場規模、市場佔有率及2025年至2032年預測

流程自動化和儀器市場:按技術、最終用戶、儀器類型、自動化類型、國家和地區分類-全球產業分析、市場規模、市場佔有率及2025年至2032年預測 自動旋轉攪拌器市場:按類型、功率等級、安裝方式、材料和最終用途行業分類,全球預測,2026-2032年

自動旋轉攪拌器市場:按類型、功率等級、安裝方式、材料和最終用途行業分類,全球預測,2026-2032年 全球過程自動化市場分析與預測(至2032年)

全球過程自動化市場分析與預測(至2032年) 工業控制市場分析及預測(至2035年),涵蓋製程自動化:按類型、產品、服務、技術、組件、應用、流程、部署、最終用戶及解決方案分類流程自動化與儀器市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、流程、最終使用者、功能分類

工業控制市場分析及預測(至2035年),涵蓋製程自動化:按類型、產品、服務、技術、組件、應用、流程、部署、最終用戶及解決方案分類流程自動化與儀器市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、流程、最終使用者、功能分類 全球零接觸式配置市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球零接觸式配置市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 零接觸配置市場 - 全球產業規模、佔有率、趨勢、機會及預測(按組件、設備類型、網路複雜性、公司規模、垂直產業、地區和競爭格局分類),2021-2031 年

零接觸配置市場 - 全球產業規模、佔有率、趨勢、機會及預測(按組件、設備類型、網路複雜性、公司規模、垂直產業、地區和競爭格局分類),2021-2031 年