|

市場調查報告書

商品編碼

2035148

含氟聚合物:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Fluoropolymer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

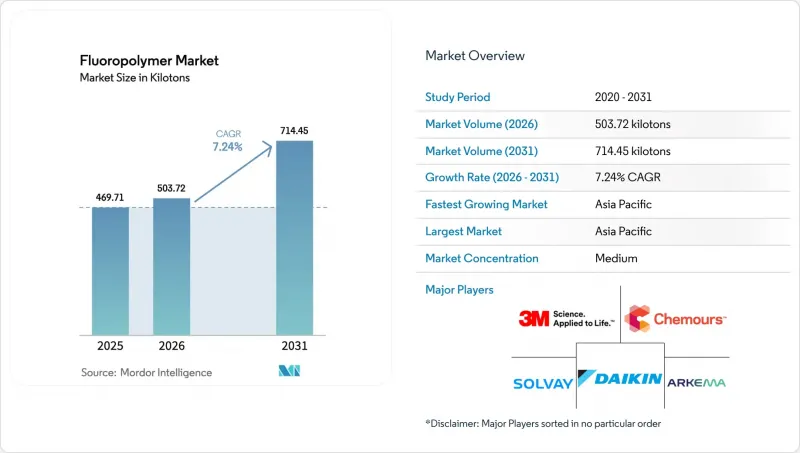

預計氟聚合物市場將從 2025 年的 469.71 千噸成長到 2026 年的 503.72 千噸,然後在 2031 年達到 714.45 千噸,2026 年至 2031 年的複合年成長率為 7.24%。

這項持續成長主要得益於對電動汽車電纜絕緣材料的需求、亞太地區半導體製造廠的擴張以及低VOC塗料法規的推動,這些法規充分利用了氟聚合物的化學特性。其卓越的化學惰性、熱穩定性和介電強度使其價格堅挺,從而延長了關鍵設備的使用壽命並降低了維護成本。主要供應商正在深化其在螢石開採和下游複合材料領域的垂直整合,以降低原料價格波動的風險。製程密度的提高和薄膜耐久性的增強正在推動綠色氫能專案對氟聚合物的廣泛應用。這些因素共同作用,增強了產業間的相互依存性,從而保護了氟聚合物市場免受週期性衰退的影響。

全球氟聚合物市場趨勢與洞察

電動車高性能線束材料的需求正在激增。

電動車 (EV) 依賴能夠承受 800V 電壓架構、-40 度C至 150 度C溫度循環以及電解洩漏的電纜絕緣層。 PVDF 和 ETFE 符合這些嚴苛條件,同時維持符合全球 OEM 安全測試標準的阻燃性能。特斯拉 Model S Plaid 和 Lucid Air Dream Edition 等高階車型採用氟聚合物絕緣線束,以確保即使在賽道駕駛條件下也能持續高功率運作。隨著 48V 輕混商用車的普及,市場正在擴大,電線電纜製造商正在推進等級預認證,以縮短新型電動車平台的檢驗週期。隨著汽車製造商縮短開發週期,能夠提供具有卓越顏色穩定性和輻射交聯性能的絕緣等級的供應商在規範採納方面獲得了優勢。此外,銅價持續上漲的壓力促使設計人員轉向更薄的絕緣材料,這使得具有高介電強度的氟聚合物成為首選。

PVDF作為鋰離子電池黏合劑的應用日益廣泛

聚偏氟乙烯(PVDF)憑藉其低至4.6V的電化學穩定性窗口,取代了傳統的黏合劑,從而能夠使用高鎳正極材料,提高電池組的能量密度。 PVDF在電池領域的應用日益廣泛,例如在隔膜塗層和電解添加劑方面的應用,都提升了每度電能的效益。中國電池製造商透過將國產PVDF樹脂與國產碳酸鋰結合,最大限度地減少對進口的依賴,並縮短前置作業時間。儘管其他水性黏合劑在高溫黏合方面面臨挑戰,且聚丙烯酸酯和生物材料體系的研發也在不斷推進,但PVDF的地位仍然穩固。預計到2030年,全球超級工廠的產能將超過3太瓦時(TWh),僅黏合劑需求的成長就有望推動PVDF供應商實現兩位數的成長。投資上游PVDF單體產能的製造商能夠確保原料供應,並保護利潤率免受原料價格波動的影響。

對美國和歐盟 PFAS 法規的審查

歐盟基於REACH法規提出的PFAS監管條例草案涵蓋範圍廣泛,列出了超過10,000種物質,其中包括含氟聚合物,但在關鍵應用領域除外。不確定性導致擴張項目停滯,投資者正在權衡合規成本與未來現金流。加州分階段禁止某些食品接觸材料的做法清楚地表明,區域性措施如何蔓延至全球供應鏈,迫使原始設備製造商(OEM)重新設計產品。半導體終端用戶正在遊說爭取豁免,並警告稱,如果沒有超潔淨的含氟聚合物管材,晶圓缺陷的風險將急劇增加。主動認證低萃取率含氟添加劑等級的公司正在增加獲得豁免的機會。

細分市場分析

2025年,聚四氟乙烯(PTFE)在含氟聚合物市場中佔48.05%的市場佔有率,這主要得益於其在化學加工墊片、航太密封件和半導體晶圓載體等領域的應用。預計到2031年,PTFE含氟聚合物市場規模將達到約333.6千噸,這主要得益於PFA襯裡熱交換器日益成長的需求。

相較之下,PVDF 的複合年成長率 (CAGR) 為 17.1%,預計到 2031 年產量將超過 12 萬噸,這主要得益於鋰離子電池正極黏合劑和質子交換膜的應用。中國和韓國佔已公佈的 PVDF 增產計畫的 70%,樹脂供應鏈的成長與電池超級工廠叢集的發展保持同步。 ETFE 在建築屋頂防水卷材和可耐受 200°C 高溫的電動汽車線材塗層領域正蓬勃發展。 FEP 的成長與半導體濕式製程台的升級密切相關,因為其萃取物含量極低。 PFA、ECTFE 和 PVF 在一些對符合 FDA 21 CFR 標準和太陽能電池背板耐久性要求較高的領域仍然存在小規模眾市場。

本氟聚合物市場報告按樹脂類型(ETFE、FEP、PTFE、PVF 等)、終端用戶產業(航太、汽車、建築施工、電氣電子、工業機械、包裝等)和地區(亞太地區、北美、歐洲、南美以及中東和非洲)進行細分。市場預測以數量(噸)和價值(美元)兩種單位呈現。

區域分析

預計到2025年,亞太地區將佔全球氟聚合物市場佔有率的53.92%,並在2031年之前以8.34%的複合年成長率成長。中國擁有國內大部分樹脂產能,並主導鋰離子電池生產,確保了國內正極材料製造商的PVDF穩定供應。台灣及韓國正大力投資7奈米及以下晶圓製造,使用超高純度PFA管材及PTFE波紋管以防止污染。在印度,需要耐腐蝕氟聚合物襯裡的電動車製造和化學加工項目正在不斷擴展。日本政府的獎勵正在支持PEM電解槽的推廣應用,進一步推動了PVDF和FEP薄膜的需求。

在北美,航太、國防和特種化學品產業的需求穩定,這些產業更注重性能而非成本。此外,美國嚴格的揮發性有機化合物(VOC)排放法規推動了建築板材向水性聚偏氟乙烯(PVDF)塗料的轉變。在墨西哥,汽車組裝產量的成長帶動了電池冷卻迴路用氟聚合物管材的需求增加;在加拿大,採礦作業中的酸浸迴路則指定使用聚四氟乙烯(PTFE)內襯。雖然整體成長率與亞洲相比較為溫和,但高價值應用支撐了利潤率。

在歐洲,對永續性和法規遵循的關注仍在繼續。綠色新政正在推動對需要氟聚合物薄膜的綠色氫氣工廠的投資,而德國原始設備製造商(OEM)正在擴大電動汽車零件生產線的產能,這些生產線需要使用聚偏二氟乙烯(PVDF)黏合劑和電纜絕緣層。然而,REACH法規下擬議的PFAS法規帶來了不確定性,一些產能擴張計劃已被推遲,直到豁免條款得到明確。航太、醫療和半導體等關鍵應用領域的豁免維持了對優質氟聚合物的需求。在南美、中東和非洲,隨著石化和採礦業使用耐腐蝕襯裡對設施進行現代化改造,市場正在出現成長,但基數小規模,因此其在預測期內對整體氟聚合物市場的影響將有限。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電動車高性能線束的需求正在激增。

- PVDF作為鋰離子電池黏合劑的應用日益廣泛。

- 亞洲半導體製造產能擴張

- 對低揮發性有機化合物塗料的嚴格監管

- 綠氫電解膜(PVDF、FEP)

- 市場限制因素

- 美國和歐盟 PFAS 監管趨勢

- 氟化鈣價格高且供應緊張

- 原物料價格波動

- 價值鏈分析

- 監理情勢

- 進出口分析

- 價格趨勢

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

- 新進入者的威脅

- 終端用戶領域的趨勢

- 航太(航太零件生產銷售)

- 汽車(汽車產量)

- 建築與施工(新建建築占地面積)

- 電氣和電子(電氣和電子產品生產產生的銷售收入)

- 包裝(塑膠包裝量)

第5章 市場規模和成長預測(價值和數量)

- 依樹脂類型

- 乙烯-四氟乙烯(ETFE)

- 氟化乙烯丙烯(FEP)

- 聚四氟乙烯(PTFE)

- 聚偏氟乙烯(PVF)

- 聚二氟亞乙烯(PVDF)

- 其他樹脂類型

- 按最終用戶行業分類

- 航太

- 車

- 建築/施工

- 電氣和電子

- 工業機械

- 包裝

- 其他終端用戶產業

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 馬來西亞

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 義大利

- 英國

- 俄羅斯

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 奈及利亞

- 南非

- 其他中東和非洲

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率** (%) / 排名分析

- 公司簡介

- 3M

- Arkema

- Daikin Industries Ltd.

- Dongyue Group

- Gujarat Fluorochemicals Ltd.(GFL)

- Kureha Corporation

- Shanghai 3F New Materials

- Sinochem

- Syensqo

- The Chemours Company

- Toray Industries Inc.

- Zhejiang Juhua Co., Ltd.

第7章 市場機會與未來展望

第8章:執行長面臨的關鍵策略挑戰

The Fluoropolymer market size is expected to grow from 469.71 kilotons in 2025 to 503.72 kilotons in 2026 and is forecast to reach 714.45 kilotons by 2031 at 7.24% CAGR over 2026-2031.

Sustained gains stem from electric-vehicle wire insulation, Asia-Pacific semiconductor fab expansion, and low-VOC coating mandates that favor fluoropolymer chemistries. Price resilience is linked to unmatched chemical inertness, thermal stability, and dielectric strength that extend service life and reduce maintenance costs for critical assets. Leading suppliers are deepening their vertical integration into fluorspar mining and downstream compounding to mitigate raw-material volatility. Process intensification and advances in membrane durability broaden the adoption of green-hydrogen projects. Collectively, these drivers reinforce multi-industry reliance, shielding the fluoropolymer market from cyclical downturns.

Global Fluoropolymer Market Trends and Insights

Surge in demand for high-performance wiring in EVs

Electric vehicles rely on cable insulation that withstands 800 V architectures, -40°C to 150°C thermal cycles, and electrolyte splash. PVDF and ETFE meet these stress profiles while maintaining flame retardancy that satisfies global OEM safety tests. Premium models such as Tesla Model S Plaid and Lucid Air Dream Edition specify fluoropolymer-insulated harnesses to secure continuous high-power operation under track conditions. Growth in 48 V mild-hybrid commercial vehicles broadens the addressable volume, and wire-and-cable compounders pre-qualify grades to shorten validation timelines for new EV platforms. Suppliers able to provide color-stable, irradiation-crosslinkable insulation grades gain specification wins as automakers compress development cycles. Continuous copper price pressure also pushes designers toward thinner-wall insulation, favoring high-dielectric-strength fluoropolymers.

Growing adoption of PVDF as Li-ion battery binder

PVDF replaced legacy binders by offering an electrochemical stability window to 4.6 V, enabling higher-nickel cathodes that lift pack energy density. Separator coatings and electrolyte additives extend PVDF's battery role and multiply revenue per kilowatt-hour. Chinese cell makers pair local PVDF resin with domestic lithium carbonate, minimizing import dependency and shortening lead times. Alternative water-based binders struggle with adhesion at high-temperature curing, keeping PVDF entrenched despite ongoing research and development in polyacrylic and biomaterial systems. As global gigafactory capacity surpasses 3 TWh by 2030, incremental binder demand alone sustains double-digit growth for PVDF suppliers. Producers investing in upstream VDF monomer capacity lock in feedstock and defend margins against raw-material price swings.

PFAS regulatory scrutiny in the US/EU

Broad PFAS proposals under EU REACH list more than 10,000 substances, covering fluoropolymers except where critical-use derogations apply. Uncertainty stalls expansion projects as investors weigh compliance costs against future cash flow. California's phased ban on certain food-contact articles illustrates how localized actions cascade through global supply chains, forcing OEMs to redesign. Semiconductor end-users lobby for exemptions, warning that wafer defect risk rises sharply without ultra-clean fluoropolymer tubing. Companies that proactively certify grades for low-extractable fluorinated additives improve their odds of securing derogations.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of semiconductor fab capacity in Asia

- Stringent low-VOC coating regulations

- High fluorspar costs and limited supply

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The PTFE category retained a 48.05% market share in the fluoropolymer market in 2025, driven by applications such as chemical-processing gaskets, aerospace seals, and semiconductor wafer carriers. The fluoropolymer market size for PTFE is expected to reach approximately 333.6 kilotons by 2031, driven by new demand for PFA-lined heat exchangers.

PVDF, by contrast, recorded an 17.1% CAGR and will cross 120 kilotons by 2031, fueled by lithium-ion cathode binders and proton-exchange membranes. China and South Korea account for 70% of incremental PVDF capacity announcements, aligning resin availability with the growth of battery gigafactory clusters. ETFE gains momentum in architectural roof membranes and 200°C EV wire jackets. FEP growth tracks semiconductor wet-bench upgrades given its ultra-low extractables profile. Smaller niches for PFA, ECTFE, and PVF persist where FDA 21 CFR compliance or photovoltaic backsheet durability is non-negotiable.

The Fluoropolymer Market Report is Segmented by Sub-Resin Type (ETFE, FEP, PTFE, PVF, and More), End-User Industry (Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and the Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons) and Value (USD).

Geography Analysis

The Asia-Pacific region owned 53.92% of the Fluoropolymer market in 2025 and is projected to grow at an 8.34% CAGR through 2031. China commands a significant portion of domestic resin capacity and dominates lithium-ion battery production, thereby ensuring a secure PVDF supply for local cathode manufacturers. Taiwan and South Korea invest heavily in sub-7 nm wafer fabrication, consuming ultra-pure PFA tubing and PTFE bellows to guard against contamination. India scales up EV manufacturing and chemical-processing projects that require corrosion-resistant fluoropolymer lining materials. Government incentives in Japan support the deployment of PEM electrolyzers, further boosting demand for PVDF and FEP membranes.

North America exhibits steady consumption in aerospace, defense, and specialty chemicals, where performance outweighs cost. The US also enforces strict VOC caps, prompting substitution toward waterborne PVDF coatings in architectural panels. Mexico's growing vehicle assembly output increases purchases of fluoropolymer tubing for battery coolant loops, and Canadian mining operations specify PTFE linings for acid-leach circuits. Overall growth is modest compared with Asia but underpinned by higher per-unit value applications that bolster margins.

Europe maintains focus on sustainability and regulatory compliance. The EU Green Deal catalyzes investment in green-hydrogen plants that require fluoropolymer membranes, while German OEMs ramp EV component lines that consume PVDF binder and cable insulation. Yet the proposed PFAS restriction under REACH injects uncertainty, delaying some capacity expansions until derogation clarity emerges. Critical-use exemptions for aerospace, medical, and semiconductor fields sustain premium-grade demand. South America, the Middle-East, and Africa register emerging growth as petrochemical and mining sectors modernize equipment with corrosion-proof linings, albeit from a smaller base, keeping their influence on the total Fluoropolymer market size moderate during the forecast.

- 3M

- Arkema

- Daikin Industries Ltd.

- Dongyue Group

- Gujarat Fluorochemicals Ltd. (GFL)

- Kureha Corporation

- Shanghai 3F New Materials

- Sinochem

- Syensqo

- The Chemours Company

- Toray Industries Inc.

- Zhejiang Juhua Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in demand for high-performance wiring in EVs

- 4.2.2 Growing adoption of PVDF as Li-ion battery binder

- 4.2.3 Expansion of semiconductor fab capacity in Asia

- 4.2.4 Stringent low-VOC coating regulations

- 4.2.5 Green-hydrogen electrolysis membranes (PVDF, FEP)

- 4.3 Market Restraints

- 4.3.1 PFAS regulatory scrutiny in US/EU

- 4.3.2 High fluorspar costs and limited supply

- 4.3.3 Raw-material price volatility

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Import and Export Analysis

- 4.7 Price Trends

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of Substitutes

- 4.8.4 Competitive Rivalry

- 4.8.5 Threat of New Entrants

- 4.9 End-use Sector Trends

- 4.9.1 Aerospace (Aerospace Component Production Revenue)

- 4.9.2 Automotive (Automobile Production)

- 4.9.3 Building and Construction (New Construction Floor Area)

- 4.9.4 Electrical and Electronics (Electrical and Electronics Production Revenue)

- 4.9.5 Packaging(Plastic Packaging Volume)

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Sub-Resin Type

- 5.1.1 Ethylenetetrafluoroethylene (ETFE)

- 5.1.2 Fluorinated Ethylene-propylene (FEP)

- 5.1.3 Polytetrafluoroethylene (PTFE)

- 5.1.4 Polyvinylfluoride (PVF)

- 5.1.5 Polyvinylidene Fluoride (PVDF)

- 5.1.6 Other Sub Resin Types

- 5.2 By End-User Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Building and Construction

- 5.2.4 Electrical and Electronics

- 5.2.5 Industrial and Machinery

- 5.2.6 Packaging

- 5.2.7 Other End-User Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 Australia

- 5.3.1.6 Malaysia

- 5.3.1.7 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 Italy

- 5.3.3.4 United Kingdom

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Nigeria

- 5.3.5.4 South Africa

- 5.3.5.5 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share**(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Daikin Industries Ltd.

- 6.4.4 Dongyue Group

- 6.4.5 Gujarat Fluorochemicals Ltd. (GFL)

- 6.4.6 Kureha Corporation

- 6.4.7 Shanghai 3F New Materials

- 6.4.8 Sinochem

- 6.4.9 Syensqo

- 6.4.10 The Chemours Company

- 6.4.11 Toray Industries Inc.

- 6.4.12 Zhejiang Juhua Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

8 Key Strategic Questions for CEOs

氟聚合物市場規模、佔有率和成長分析:按氟聚合物類型、終端用途產業、應用、配方、耐熱性和地區分類-2026-2033年產業預測

氟聚合物市場規模、佔有率和成長分析:按氟聚合物類型、終端用途產業、應用、配方、耐熱性和地區分類-2026-2033年產業預測 高純度氟聚合物(PFA)管材和管道-2026-2032 年全球市場佔有率和排名、總銷售額和需求預測。

高純度氟聚合物(PFA)管材和管道-2026-2032 年全球市場佔有率和排名、總銷售額和需求預測。 醫用氟聚合物市場:2026-2032年全球市場預測(按產品類型、形態、技術、應用和最終用途產業分類)氟聚合物市場:按類型、形態、製程和最終用戶分類-2026-2032年全球市場預測半導體氟聚合物管材市場:管材類型、材質、製造流程、直徑範圍、應用及最終用途-2026-2032年全球市場預測5G含氟聚合物市場:依產品類型、形態、製造流程和最終用途產業分類-2026-2032年全球預測

醫用氟聚合物市場:2026-2032年全球市場預測(按產品類型、形態、技術、應用和最終用途產業分類)氟聚合物市場:按類型、形態、製程和最終用戶分類-2026-2032年全球市場預測半導體氟聚合物管材市場:管材類型、材質、製造流程、直徑範圍、應用及最終用途-2026-2032年全球市場預測5G含氟聚合物市場:依產品類型、形態、製造流程和最終用途產業分類-2026-2032年全球預測 全球高通量纖維增強塑膠(HPF)市場(至2030年):按類型(PTFE、FEP、PFA/MFA、ETFE)、形狀、應用(塗層和襯裡、組件、薄膜、添加劑)、終端用戶產業(電氣和電子、工業流程、交通運輸、醫療)和地區分類

全球高通量纖維增強塑膠(HPF)市場(至2030年):按類型(PTFE、FEP、PFA/MFA、ETFE)、形狀、應用(塗層和襯裡、組件、薄膜、添加劑)、終端用戶產業(電氣和電子、工業流程、交通運輸、醫療)和地區分類 氟聚合物加工助劑市場分析與預測(至2035年):類型、產品類型、應用、技術、材料類型、最終用戶、製程、功能

氟聚合物加工助劑市場分析與預測(至2035年):類型、產品類型、應用、技術、材料類型、最終用戶、製程、功能 全球氟聚合物市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球氟聚合物市場規模、佔有率、趨勢和成長分析報告(2026-2034) 熔融加工型氟素樹脂的市場規模、成長與預測(至2034年)

熔融加工型氟素樹脂的市場規模、成長與預測(至2034年)