|

市場調查報告書

商品編碼

2035147

電解電容器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Aluminum Electrolytic Capacitors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

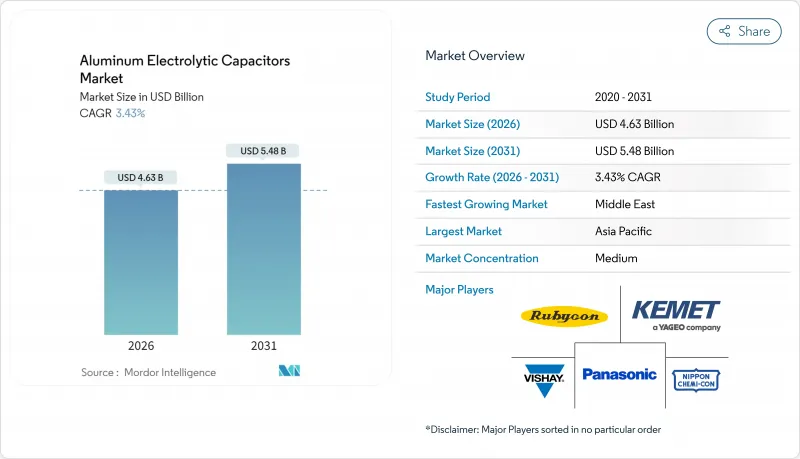

預計到 2026 年,電解電容器市場規模將達到 46.3 億美元,到 2031 年將達到 54.8 億美元,在此期間的複合年成長率為 3.43%。

這一成長主要得益於高壓逆變器拓撲結構、800V電動汽車電池平台以及對等效串聯電阻(ESR)和使用壽命要求更高的寬能隙功率裝置的轉變。智慧型手機元件小型化、電動車牽引逆變器漣波電流密度的增加以及中東地區可再生能源部署正在重塑產品設計和區域需求模式。供應商目前正將策略重點放在混合聚合物技術、內部蝕刻箔生產能力以及汽車可靠性認證上,以抵消鋁價波動帶來的風險。同時,區域專家正利用其地理位置接近性和成本優勢,在家用電子電器和工業自動化領域獲得設計應用。

全球電解電容器市場趨勢及洞察

PCB安裝面積的減少推動了超小型電容器的發展。

智慧型手機和平板電腦的電源管理電路正變得越來越小型化,迫使供應商在封裝尺寸上提供相同的電容值,與2023年的設計相比,基板面積將減少30%。厚度小於3毫米的表面黏著技術電解電容器正在取代並聯排列的噪音較大的陶瓷電容器,Nichicon公司於2025年推出的GYG混合系列產品就體現了這一成就。需求主要集中在亞太地區,該地區的契約製造製造商為了維持極低的利潤率,優先考慮即使是一平方毫米的空間縮減。這一因素導致複合年成長率(CAGR)上調了0.5%,反映了行動裝置出貨量的巨大成長。對薄型聚合物陰極線的資本投資凸顯了向傳統液態電解質的轉變。未能滿足小型化藍圖要求的供應商可能會被排除在下一代行動電話的參考設計之外。

電動車向 800V 電池系統的過渡將增加漣波電流需求。

汽車製造商正將電池組電壓從400V提升至800V,以縮短直流快速充電時間並減少銅用量。這項變化使直流鏈路電容器的電壓應力增加了一倍,導致漣波電流超過50A RMS,並使傳統的液態電解質組件過熱。PanasonicZL汽車系列和伊頓EHBSA混合系列是轉向符合AEC-Q200標準的混合聚合物解決方案的典型例子,其額定溫度為135°C,等效串聯電阻(ESR)小於10mΩ。電動車的普及推動市場年複合成長率(CAGR)達到0.7%,高壓系統的應用不僅在中國,在北美和歐洲也不斷推進。車載充電器和牽引逆變器的供應商擴大指定使用聚合物陰極,以避免降額,從而確保平均售價(ASP)的進一步提高。

鋁價波動給利潤率帶來壓力。

2025年12月,倫敦金屬交易所(LME)現貨價格達到每噸2,955美元,比年初至今的預測價格高出20%。這給電容器製造商的毛利率帶來了壓力,因為他們的價格表掛鉤。蝕刻箔約佔組件成本的30%,而價格上漲需要60-90天才能傳導,這阻礙了價格調整。美國能源局提案的碳邊境調節措施可能會進一步加劇依賴煤炭發電地區的成本壓力。年銷售額低於1億美元的中小型企業幾乎沒有避險的空間,面臨更高的破產風險,且研發預算有限。

細分市場分析

預計電壓超過500V的高壓電解電容器將以4.4%的年均複合成長率成長,超過電解電容器市場3.43%的整體複合年成長率,主要得益於太陽能逆變器和工業驅動器為提高效率而增加直流母線電壓。到2025年,低電壓元件仍將佔總銷售額的64.21%,這主要得益於智慧型手機、平板電腦和汽車軌道等電壓範圍在12V至48V之間的應用。高壓氧化膜需要每伏約1.2nm的陽極氧化精度,這促使人們增加對無塵室和線上缺陷檢測的投資。

中東地區的公用事業規模太陽能發電工程和800V電動汽車車載充電器正在模糊產品細分市場的界限,450-500V的電容器橫跨這兩個層級。PanasonicZL系列電容器憑藉其135°C的耐熱性,瞄準了這個跨界市場,凸顯了引擎室內環境溫度控管的挑戰。隨著寬能隙半導體技術的發展,600-700V的中間母線電壓成為可能,鋁電解電解市場預計將圍繞新的電壓範圍進行重組,而非傳統的500V結溫。

受5G基地台散熱需求的推動,固體聚合物電容器預計將以4.9%的複合年成長率成長,但到2025年,非固體(液態)設計將佔據61.47%的市場。混合聚合物組件結合了氧化鋁陽極和導電聚合物陰極,彌合了性價比差距,並在105°C下實現了10000小時的使用壽命。

在超過 125 度C 的環境中,固體聚合物的可靠性仍然是一個挑戰。導電聚合物的劣化限制了它們在汽車引擎室的應用。因此,在溫度低於 85 度C且均方根電流小於等於 2A 的應用中,液態電解質仍佔主導地位。尤其是在汽車 DC-DC 轉換器中,ESR 是熱設計的阻礙因素,隨著認證數據的積累,混合聚合物電解電容器的市場規模預計將穩定成長。

區域分析

亞太地區受中國智慧型手機組裝廠、日本汽車電子製造商和韓國晶圓代工廠的推動,預計到2025年將佔全球鋁電解電容器銷售額的45.38%。國內需求和出口量共同推動該地區成為電解電容器市場的中心。泰國、馬來西亞和越南政府提供稅收優惠,吸引了村田製作所和Panasonic等公司將產能轉移到該地區。

中東地區以4.7%的複合年成長率領跑,主要得益於沙烏地阿拉伯10吉瓦NEOM計畫和阿拉伯聯合大公國2.6吉瓦穆罕默德·本·拉希德·阿勒馬克圖姆太陽能園區等巨型太陽能電站的建設。這些電站的逆變器需要額定壽命為10萬小時、工作溫度為85攝氏度的600-900伏特電容器,從而推動了對高壓電容器的需求。日立能源西安工廠計劃在2025年將產能提高三倍,以滿足波灣合作理事會(GCC)成員國的設備需求,凸顯了該地區對中國產能的吸引力。

在北美,電動車組裝廠的擴張和需要低ESR直流母線電容器的超大規模資料中心的建設,為市場提供了順風。在歐洲,能源價格上漲構成不利因素,但強制性電氣化政策維持了對汽車和工業零件的高階需求。南美洲市場基數小規模,但巴西汽車零件供應商採用混合動力平台推動了市場成長。另一方面,非洲仍然是一個新興市場,專注於離網太陽能控制器。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- PCB安裝面積的減少推動了對超小型電容器的需求。

- 電動車向 800V 電池系統的過渡提高了漣波電流需求。

- 加大對公用事業級太陽能逆變器的投資

- 政府對智慧製造(工業4.0)的獎勵

- 利用寬能隙功率元件創造對低ESR大容量電源的需求。

- 在5G基地台採用邊緣AI硬體

- 市場限制因素

- 鋁價波動給利潤率帶來壓力。

- 高純度蝕刻箔的供應風險

- 人們對固體聚合物電容器在 125 度C以上溫度下的可靠性表示擔憂

- 設計概念轉向多層聚合物電容器

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 投資分析

- 波特五力分析

- 買方的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 透過電壓

- 高壓(超過500伏特)

- 低電壓(500伏特或以下)

- 按電解類型

- 非固體(液態)電解質

- 固體聚合物電解質

- 雜化聚合物

- 透過安裝配置

- 表面黏著技術

- 通孔(徑向、軸向)

- 卡扣式

- 螺絲端子

- 其他安裝配置

- 透過使用

- 工業自動化

- 溝通

- 家用電子電器

- 汽車(內燃機汽車和電動車)

- 能源與電力

- 其他用途

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 亞太其他地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nippon Chemi-Con Corporation

- Panasonic Holdings Corporation

- Yageo Corporation(KEMET)

- Vishay Intertechnology Inc.

- Nichicon Corporation

- Rubycon Corporation

- TDK Corporation(EPCOS Brand)

- Cornell Dubilier Electronics

- Lelon Electronics Corporation

- Samwha Capacitor Group

- Nantong Jianghai Capacitor Co.

- NIC Components Corp.

- Elna Co., Ltd.

- Suncon(Sanyo)

- Illinois Capacitor(Cornell)

- Hitano Enterprise Corp.

- Samyoung Electronics Co., Ltd.

- Taiwan Chinsan Electronics Industrial Co., Ltd.

- Cheng Tung Industrial Co., Ltd.

- CapXon Group

- Jianghai Europe Electronic Components GmbH

第7章 市場機會與未來展望

The aluminum electrolytic capacitors market size is USD 4.63 billion in 2026 and is forecast to reach USD 5.48 billion by 2031, reflecting a 3.43% CAGR through the period.

Momentum stems from a shift toward high-voltage inverter topologies, 800 V electric-vehicle (EV) battery platforms, and wide-bandgap power devices that demand lower equivalent series resistance (ESR) and longer lifetime. Component miniaturization in smartphones, higher ripple-current densities in EV traction inverters, and renewable-energy mandates in the Middle East are reshaping product design and geographic demand patterns. Supplier strategies now emphasize hybrid polymer technology, captive etched-foil capacity, and automotive reliability qualifications to offset aluminum price volatility. At the same time, regional specialists leverage proximity and cost advantages to win design slots in consumer electronics and industrial automation.

Global Aluminum Electrolytic Capacitors Market Trends and Insights

Shrinking PCB Real Estate Driving Ultra-Miniaturised Capacitors

Power-management circuits in smartphones and tablets continue to shrink, forcing suppliers to deliver identical capacitance in packages occupying 30% less board area than 2023 designs. Surface-mount aluminum electrolytic capacitors under 3 mm profile are displacing parallel banks of ceramics that create acoustic noise, an advantage demonstrated by Nichicon's GYG hybrid series released in 2025. Demand is concentrated in Asia Pacific, where contract manufacturers prioritize square-millimetre savings to sustain razor-thin margins. The driver's 0.5% uplift to the overall CAGR reflects the sheer shipment volume of mobile devices. Capital investment in low-profile polymer cathode lines underlines the transition from traditional liquid electrolytes. Suppliers that cannot meet miniaturization roadmaps risk exclusion from next-generation handset reference designs.

Push Toward 800 V Battery Systems in EVs Elevates Ripple Current Requirements

Automakers are migrating from 400 V to 800 V pack voltages to shorten DC-fast-charging sessions and trim copper mass. The change doubles voltage stress on DC-link capacitors and pushes ripple current beyond 50 A RMS, overheating conventional liquid-electrolyte parts. Panasonic's ZL automotive series and Eaton's EHBSA hybrid family illustrate the move to AEC-Q200 hybrid polymer solutions rated at 135 °C and ESR below 10 mΩ. EV adoption drives a 0.7% boost to market CAGR, with North America and Europe joining China in high-voltage rollouts. Onboard charger and traction-inverter suppliers increasingly stipulate polymer cathodes to eliminate derating, locking in higher average-selling-price (ASP) growth.

Aluminium Price Volatility Compressing Margins

London Metal Exchange spot prices reached USD 2,955 per metric ton in December 2025, 20% higher than early-year forecasts, trimming gross margins for capacitor makers locked into three-month customer price lists. Etched foil comprises roughly 30% of bill-of-material cost, and a 60- to 90-day pass-through lag hampers price adjustments. The U.S. Department of Energy's proposed carbon-border adjustments could add further cost pressure in coal-reliant grid regions. Smaller firms under USD 100 million revenue lack hedging leverage, heightening bankruptcy risk and limiting R&D budgets.

Other drivers and restraints analyzed in the detailed report include:

- Growing Investments in Utility-Scale Solar Inverters

- Wide-bandgap Power Devices Creating Need for Low-ESR Bulk Capacitance

- Supply Risk of High-Purity Etched Foil

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

High-voltage aluminum electrolytic capacitors above 500 V are forecast to grow at 4.4% annually, eclipsing the 3.43% aluminum electrolytic capacitors market CAGR as solar inverters and industrial drives lift DC-bus voltages for efficiency. Low-voltage parts still command 64.21% of 2025 revenue thanks to phones, tablets, and 12-48 V automotive rails. High-voltage oxide layers require anodization precision near 1.2 nm per volt, pushing cleanroom investments and inline defect inspection.

Utility-scale solar projects in the Middle East and 800 V EV onboard chargers blur segmentation boundaries, with 450-500 V capacitors straddling both tiers. Panasonic's ZL series targets this crossover with 135 °C endurance, underscoring thermal-management challenges in under-hood environments. As wide-bandgap semiconductors enable intermediate 600-700 V buses, the aluminum electrolytic capacitors market is likely to realign around new voltage clusters rather than the historical 500 V breakpoint.

Solid polymer capacitors should advance at 4.9% CAGR on the back of 5G base-station thermal demands, while non-solid liquid designs held 61.47% share in 2025. Hybrid polymer parts that marry aluminium oxide anodes with conductive-polymer cathodes bridge cost and performance gaps, extending life to 10,000 hours at 105 °C.

Solid polymer reliability above 125 °C remains a hurdle: conductive polymers degrade, limiting automotive under-hood deployment. Liquid electrolytes therefore retain dominance in applications below 85 °C and currents under 2 A RMS. The aluminum electrolytic capacitors market size for hybrid polymer formats is expected to expand steadily as qualification data accumulates, especially in automotive DC-DC converters where ESR dictates thermal-design budgets.

The Aluminum Electrolytic Capacitors Market Report is Segmented by Voltage (High Voltage (Above 500 V), and Low Voltage (Up To 500 V)), Electrolyte Type (Non-Solid Liquid, Solid Polymer, and Hybrid Polymer), Mounting Configuration (Surface-Mount, Through-Hole (Radial, and Axial), and More), Application (Industrial Automation, Telecommunications, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific captured 45.38% of 2025 revenue, anchored by Chinese smartphone assembly plants, Japanese auto electronics, and Korean foundries. Domestic demand plus export volumes make the region the epicentre of the aluminum electrolytic capacitors market. Governments in Thailand, Malaysia, and Vietnam offer tax holidays, drawing capacity from Murata, Panasonic, and others.

The Middle East posts the fastest 4.7% CAGR thanks to giga-scale solar farms such as Saudi Arabia's 10 GW NEOM project and the United Arab Emirates' 2.6 GW Mohammed bin Rashid Al Maktoum Solar Park. Inverters for these plants need 600-900 V capacitors rated for 100,000 hours at 85 °C, boosting high-voltage demand. Hitachi Energy's Xi'an line tripled output in 2025 to serve Gulf Cooperation Council installations, underlining the region's pull-on Chinese capacity.

North America benefits from EV assembly expansions and hyperscale datacentre builds that require low-ESR DC-bus capacitance. Europe faces energy-price headwinds but sustains premium demand for automotive and industrial parts through electrification mandates. South America grows from a smaller base, led by Brazilian auto suppliers adopting hybrid platforms, while Africa remains an emerging market focused on off-grid solar controllers.

- Nippon Chemi-Con Corporation

- Panasonic Holdings Corporation

- Yageo Corporation (KEMET)

- Vishay Intertechnology Inc.

- Nichicon Corporation

- Rubycon Corporation

- TDK Corporation (EPCOS Brand)

- Cornell Dubilier Electronics

- Lelon Electronics Corporation

- Samwha Capacitor Group

- Nantong Jianghai Capacitor Co.

- NIC Components Corp.

- Elna Co., Ltd.

- Suncon (Sanyo)

- Illinois Capacitor (Cornell)

- Hitano Enterprise Corp.

- Samyoung Electronics Co., Ltd.

- Taiwan Chinsan Electronics Industrial Co., Ltd.

- Cheng Tung Industrial Co., Ltd.

- CapXon Group

- Jianghai Europe Electronic Components GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shrinking PCB Real Estate Driving Ultra-miniaturised Capacitors

- 4.2.2 Push Toward 800 V Battery Systems in EVs Elevates Ripple Current Requirements

- 4.2.3 Growing Investments in Utility-Scale Solar Inverters

- 4.2.4 Government Incentives for Smart Manufacturing (Industry 4.0)

- 4.2.5 Wide-bandgap Power Devices Creating Need for Low-ESR Bulk Capacitance

- 4.2.6 Edge AI Hardware Proliferation in 5G Base-Stations

- 4.3 Market Restraints

- 4.3.1 Aluminium Price Volatility Compressing Margins

- 4.3.2 Supply Risk of High-Purity Etched Foil

- 4.3.3 Solid Polymer Reliability Concerns Above 125 °C

- 4.3.4 Design-in Shift Toward Multi-layer Polymer Capacitors

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Investment Analysis

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Bargaining Power of Buyers

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitute Products

- 4.9.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Voltage

- 5.1.1 High Voltage (Greater than 500 V)

- 5.1.2 Low Voltage (Up to 500 V)

- 5.2 By Electrolyte Type

- 5.2.1 Non-solid (Liquid) Electrolyte

- 5.2.2 Solid Polymer Electrolyte

- 5.2.3 Hybrid Polymer

- 5.3 By Mounting Configuration

- 5.3.1 Surface-Mount

- 5.3.2 Through-Hole (Radial, Axial)

- 5.3.3 Snap-In

- 5.3.4 Screw Terminal

- 5.3.5 Other Mounting Configurations

- 5.4 By Application

- 5.4.1 Industrial Automation

- 5.4.2 Telecommunications

- 5.4.3 Consumer Electronics

- 5.4.4 Automotive (ICE and EV)

- 5.4.5 Energy and Power

- 5.4.6 Other Applications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Rest of Asia Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Nippon Chemi-Con Corporation

- 6.4.2 Panasonic Holdings Corporation

- 6.4.3 Yageo Corporation (KEMET)

- 6.4.4 Vishay Intertechnology Inc.

- 6.4.5 Nichicon Corporation

- 6.4.6 Rubycon Corporation

- 6.4.7 TDK Corporation (EPCOS Brand)

- 6.4.8 Cornell Dubilier Electronics

- 6.4.9 Lelon Electronics Corporation

- 6.4.10 Samwha Capacitor Group

- 6.4.11 Nantong Jianghai Capacitor Co.

- 6.4.12 NIC Components Corp.

- 6.4.13 Elna Co., Ltd.

- 6.4.14 Suncon (Sanyo)

- 6.4.15 Illinois Capacitor (Cornell)

- 6.4.16 Hitano Enterprise Corp.

- 6.4.17 Samyoung Electronics Co., Ltd.

- 6.4.18 Taiwan Chinsan Electronics Industrial Co., Ltd.

- 6.4.19 Cheng Tung Industrial Co., Ltd.

- 6.4.20 CapXon Group

- 6.4.21 Jianghai Europe Electronic Components GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

電解電容器市場-全球產業規模、佔有率、趨勢、機會、預測:按電壓、應用、地區和競爭格局分類,2021-2031年

電解電容器市場-全球產業規模、佔有率、趨勢、機會、預測:按電壓、應用、地區和競爭格局分類,2021-2031年 2026年全球徑向引線電解電容器市場報告

2026年全球徑向引線電解電容器市場報告 電解電容器市場:2026-2032年全球市場預測(依產品類型、配置、額定電壓、電容範圍、終端用戶產業及銷售管道)低壓電解電容器市場(依電容範圍、額定電壓、產品類型、介質類型、安裝方式和應用分類)-全球預測,2026-2032年2026年全球螺絲端子電解電容器市場報告2026年電解電容器成型箔全球市場報告全球電解電容器用鋁箔市場報告(2026 年)低壓電解電容器市場按應用、終端用戶產業、產品類型、純度等級及分銷通路分類-2026-2032年全球預測多層聚合物電解電容器市場按產品類型、安裝技術、應用、額定電壓、電容範圍和最終用途行業分類 - 全球預測(2026-2032 年)

電解電容器市場:2026-2032年全球市場預測(依產品類型、配置、額定電壓、電容範圍、終端用戶產業及銷售管道)低壓電解電容器市場(依電容範圍、額定電壓、產品類型、介質類型、安裝方式和應用分類)-全球預測,2026-2032年2026年全球螺絲端子電解電容器市場報告2026年電解電容器成型箔全球市場報告全球電解電容器用鋁箔市場報告(2026 年)低壓電解電容器市場按應用、終端用戶產業、產品類型、純度等級及分銷通路分類-2026-2032年全球預測多層聚合物電解電容器市場按產品類型、安裝技術、應用、額定電壓、電容範圍和最終用途行業分類 - 全球預測(2026-2032 年) 電解電容器市場規模、佔有率及成長分析(按類型、組成、最終用戶和地區分類)-2026-2033年產業預測

電解電容器市場規模、佔有率及成長分析(按類型、組成、最終用戶和地區分類)-2026-2033年產業預測