|

市場調查報告書

商品編碼

2035130

玄武岩纖維:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Basalt Fiber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

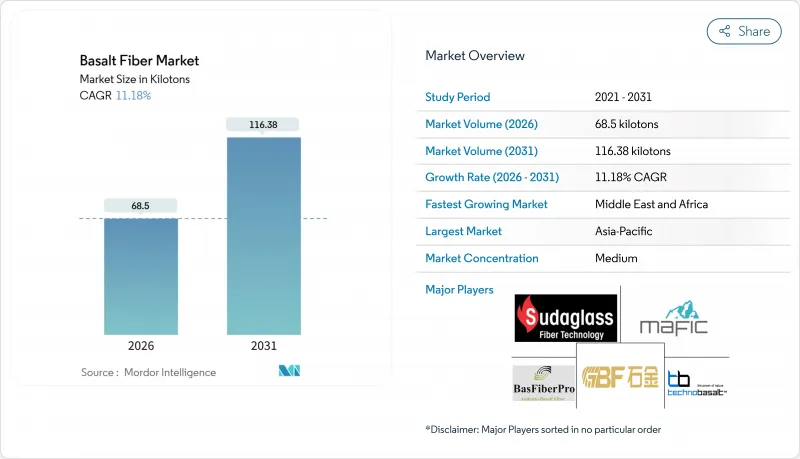

2026 年玄武岩纖維市場規模預計為 68.5 千噸,預計在預測期(2026-2031 年)內將以 11.18% 的複合年成長率成長,到 2031 年將達到 116.38 千噸。

這一成長與基礎設施脫碳計劃、離岸風力發電電場建設以及重視玄武岩纖維卓越耐腐蝕性和耐熱性的輕量化汽車法規密切相關。全球製造商正在擴大產能,以滿足渦輪葉片和汽車車體面板對連續粗紗的需求,同時用於混凝土混合料和隔熱材料的非連續纖維也越來越受歡迎。關鍵建築規範的監管核准以及對生命週期成本更嚴格的審查,正在加速玄武岩纖維的普及應用。日益激烈的競爭和早期技術的核准表明,未來五年將是玄武岩纖維市場發展的關鍵時期。

全球玄武岩纖維市場趨勢與洞察

歐盟淨零排放法規正在加速玄武岩鋼筋的應用。

修訂後的歐盟《淨零排放產業法》強制要求專案業主使用低全球暖化潛勢(GWP)的加固材料,因此玄武岩加固材料被納入橋面和防波堤的規範中。玄武岩的抗張強度為800-1200兆帕,耐腐蝕性是鋼材的三倍,即使在高氯化物濃度的環境中,也能將使用壽命延長至100年。玄武岩現已成為EN 13706標準中的參考材料,填補了先前的監管空白。在法國和德國,玄武岩加固材料正被試驗應用於橋面鋪裝層和沿海基礎設施。在這些地區,以往由於氯化物滲透,鋼材需要每25年更換一次。這項監管措施的推動將玄武岩加固材料在高暴露環境下的投資回收期縮短至15年以內,使其即使在受淨零排放成本限制的公共基礎設施預算內也具有經濟可行性。

製造離岸風力發電機葉片需要耐熱織物。

下一代15兆瓦風力渦輪機需要能夠承受高溫硬化和雷擊的葉片帽。玄武岩在高達650 度C的溫度下仍能保持強度,優於耐溫極限為460 度C的E玻璃纖維。其約400兆帕的抗彎強度足以支撐120公尺的葉片跨度。美國船級社(ABS)發布的浮體式海上風力發電機機指南指出,玄武岩纖維是錨碇和動態電纜保護系統的理想增強材料,建議監管機構核准並加快其在計劃於2030年前在北海和東海建設的80吉瓦海離岸風力發電項目中的應用。

易於取得替代品

在對性能要求不高的應用領域,例如通用複合材料和隔熱材料,玻璃纖維的成本優勢比玄武岩纖維高出10倍,限制了玄武岩纖維在全球玻璃纖維市場的滲透。該市場年產量達700萬噸。玻璃纖維的價格約為每公斤2-3美元,而玄武岩纖維的價格則高達每公斤20-30美元;只有在需要熱穩定性、耐腐蝕性或低溫性能時,這種價格差異才顯得合理。碳纖維的價格與玄武岩纖維相近,但在航太應用中,其比強度高出30%。由於鋼筋的標準成熟且施工人員對其非常熟悉,鋼筋仍佔據混凝土鋼筋市場95%的佔有率,這阻礙了玄武岩纖維在價格敏感地區的推廣應用。

細分市場分析

到2025年,連續粗紗將佔據68.18%的市場佔有率(按體積計),這主要得益於渦輪葉片和汽車車體面板對單向強度超過4800兆帕纖維的需求。同時,預計到2031年,非連續纖維的市場規模將以13.28%的複合年成長率成長。受預拌混凝土需求的推動(預拌混凝土可減少現場施工),預計2031年,離散玄武岩纖維的市場規模將超過3萬噸。測試結果表明,添加1%的離散纖維可使抗彎強度提高25%,並使地震荷載下的裂縫寬度減少40%。為了維持市場佔有率,連續纖維生產商正將業務拓展至隧道襯砌用纖維網格領域。

亞太和中東地區的專案業主更傾向於使用離散式混合料,因為其施工快捷,且能夠滿足嚴格的耐久性標準。美國混凝土學會 (ACI) 目前已提供連續和離散玄武岩纖維增強材料的設計指南,填補了技術空白。連續纖維供應商利用規模經濟優勢,生產適用於高階航太和優質汽車零件的 6–13 微米纖維。儘管連續纖維市場基礎穩固,但隨著建築規範的不斷完善,非連續玄武岩纖維的市場佔有率預計仍將持續成長。

《玄武岩纖維市場報告》按形態(連續和不連續)、應用(複合材料和非複合材料)、終端用戶行業(建築、汽車、工業、船舶、能源行業及其他(體育、化工、石油行業))和地區(亞太地區、北美、歐洲、南美以及中東和非洲)進行細分。市場預測以噸為單位。

區域分析

預計到2025年,亞太地區將佔全球總量的48.75%。中國憑藉橫店公司年產2萬噸的工廠以及自2019年以來新增的槽窯生產線,在市場上佔據領先地位。玄武岩正被用於日本和韓國的海岸維修項目,而印度耗資1.4兆美元的基礎建設項目也推動了對鋼筋的需求。接近性礦源和低廉的人事費用使該地區保持了價格競爭力。

預計到2031年,中東和非洲地區將以15.52%的複合年成長率成長,主要得益於海水淡化和液化天然氣領域的投資。沙烏地阿美已在其腐蝕性環境使用指南中指定玄武岩纖維增強複合材料(FRP)。南非礦業設施的現代化改造以及海灣合作理事會(GCC)國家的大型企劃正在擴大累積訂單,鞏固該地區作為玄武岩纖維市場成長最快叢集的地位。

在北美,一項價值1.2兆美元的基礎建設法案正在實施,緬因大學的ARPA-I計畫旨在更新AASHTO標準。在加拿大,玄武岩被用於北極地區的建築,而在墨西哥,玄武岩則被用於電動車電池機殼的製造。在歐洲,EN 13706標準和淨零排放要求正在推動沿海基礎設施和抗震維修。在南美洲,隨著巴西水力發電廠大壩的維修和阿根廷糧倉的建設,相關領域的發展勢頭正在增強,但進口成本阻礙了其廣泛應用。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 歐盟強制性的淨零排放目標正在加速對玄武岩鋼筋的需求。

- 隨著離岸風力發電機葉片的製造規模擴大,耐熱織物的需求也隨之增加。

- 各國制定汽車輕量化藍圖,鼓勵使用玄武岩纖維。

- 海灣合作理事會國家海水淡化計畫的擴張正在推動對玄武岩FRP管道的需求。

- 需要耐低溫加固的液化天然氣平台

- 市場限制因素

- 易於取得替代品

- 玄武岩礦石運費變化

- 由於加工設備磨損,營運成本(OPEX)增加。

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按形式

- 續篇

- 離散的

- 透過使用

- 複合材料

- 非複合材料

- 按最終用途行業分類

- 建築/施工

- 車

- 產業

- 船

- 能源產業

- 其他(體育、化工、石油業)

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞洲地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Albarrie Canada Limited

- Arab Basalt Fiber

- ARMBAS

- Basalt Engineering LLC

- Basaltex

- Basanite Industries LLC

- BASTECH

- Deutsche Basalt Faser GmbH

- EcoBasalt Solutions

- Fiberbas construction and building technologies

- Final Advanced Materials

- Galen Ltd

- Hengdian Group Holdings Limited

- INCOTELOGY GmbH

- Isomatex SA

- JiLin Tongxin Basalt Technology Co.,Ltd

- Kamenny Vek

- MAFIC SA

- Rockwool A/S

- Sudaglass Fiber Technology

- Technobasalt Invest

- Zhejiang Shijin Basalt Fiber Co., Ltd.

第7章 市場機會與未來展望

The Basalt Fiber Market size is estimated at 68.5 kilotons in 2026, and is expected to reach 116.38 kilotons by 2031, at a CAGR of 11.18% during the forecast period (2026-2031).

The surge is tied to infrastructure decarbonization programs, offshore wind construction, and vehicle lightweighting mandates that reward basalt fiber's superior corrosion and heat resistance. Global producers are scaling capacity to address demand for continuous rovings in turbine blades and automotive body panels, while discrete fiber formats for concrete mixes and insulation gain traction. Regulatory recognition in major codes, coupled with heightened lifecycle-cost scrutiny, is compressing the adoption curve. Intensifying competition and early technical approvals signal a pivotal phase for the basalt fiber market over the next five years.

Global Basalt Fiber Market Trends and Insights

EU Net-Zero Mandates Accelerating Basalt Rebar

The revised EU Net-Zero Industry Act compels project owners to adopt low-GWP reinforcements, placing basalt rebar on specification lists for bridge decks and seawalls. Tensile strengths of 800-1,200 MPa and triple the corrosion resistance of steel lengthen service life to 100 years in chloride-rich environments. EN 13706 now references basalt, removing earlier regulatory gaps. France and Germany are piloting basalt rebar in bridge deck overlays and coastal infrastructure, where chloride ingress has historically required steel replacement every 25 years. This regulatory push is compressing payback periods for basalt rebar to under 15 years in high-exposure applications, making it economically viable for public infrastructure budgets constrained by net-zero compliance costs.

Offshore Wind-Blade Build-Out Needs Heat-Resistant Fabrics

Next-generation 15 MW turbines require spar caps that withstand curing exotherms and lightning strikes. Basalt retains strength up to 650°C, outperforming E-glass at 460°C. Flexural strengths of roughly 400 MPa support 120-meter blade spans. The American Bureau of Shipping's guide for floating offshore wind turbines references basalt fiber as a compliant reinforcement for mooring and dynamic cable protection systems, signaling regulatory acceptance that will accelerate adoption in the 80-gigawatt offshore wind pipeline planned for the North Sea and East China Sea through 2030.

Easy Availability of Substitutes

Glass fiber maintains a 10-to-1 cost advantage over basalt fiber in non-performance-critical applications such as general-purpose composites and insulation, limiting basalt's penetration into the 7-million-tonne-per-year global glass fiber market. E-glass fiber costs approximately USD 2-3 per kilogram, whereas basalt fiber ranges from USD 20-30 per kilogram, a premium justified only when thermal stability, corrosion resistance, or cryogenic performance is required. Carbon fiber, priced similarly to basalt, offers 30% higher specific strength for aerospace. Steel rebar still holds a 95% share in concrete reinforcement, thanks to entrenched codes and installer familiarity, stalling basalt uptake in price-sensitive regions.

Other drivers and restraints analyzed in the detailed report include:

- Vehicle Lightweighting Roadmap Favoring Basalt Fiber Usage

- GCC Desalination Expansion Driving Basalt FRP Pipelines

- Basalt-Ore Freight-Rate Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Continuous rovings controlled 68.18% volume in 2025 as turbine blades and auto body panels require unidirectional strength exceeding 4,800 MPa. Discrete fiber volume will expand at a 13.28% CAGR to 2031. The basalt fiber market size for discrete formats is on track to surpass 30 kilotons by 2031, driven by ready-mix concrete mixes that cut on-site labor. Tests show 1% discrete addition lifts flexural strength 25% and shrinks crack width 40% under seismic load. Continuous makers are diversifying into fiber grids for tunnel linings to defend their share.

Project owners in Asia-Pacific and the Middle East favor discrete mixes because they pour faster and meet stricter durability codes. The American Concrete Institute now offers design guidance for both continuous and discrete basalt reinforcement, closing technical gaps. Continuous suppliers leverage economies of scale, producing 6-13 µm filaments suited to high-end aerospace and premium auto parts. As building codes evolve, the basalt fiber market share of discrete formats will keep rising despite the continuous fiber's entrenched base.

The Basalt Fiber Market Report is Segmented by Form (Continuous and Discrete), Usage (Composites and Non-Composites), End-Use Industry (Building and Construction, Automotive, Industrial, Marine, Energy Industry, and Other (Sports, Chemical Industry, Petroleum Industry)), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (tons).

Geography Analysis

Asia-Pacific held 48.75% volume in 2025. China leads through Hengdian's 20,000 tpa plant and additional tank-kiln lines since 2019. Japan and South Korea apply basalt in coastal retrofits, and India's USD 1.4 trillion infrastructure push fuels rebar demand. Proximity to ore and lower labor costs keep regional pricing competitive.

The Middle East and Africa, advancing at a 15.52% CAGR to 2031, will benefit from desalination and LNG investments. Saudi Aramco lists basalt FRP in corrosive service guidelines. South African mining upgrades and GCC megaprojects extend the order book, solidifying the region as the basalt fiber market's fastest-growing cluster.

North America leverages the USD 1.2 trillion Infrastructure Act, with the University of Maine's ARPA-I work aiming to update AASHTO codes. Canada deploys basalt in Arctic builds, and Mexico integrates it in EV battery enclosures. Europe's EN 13706 standards and net-zero mandates drive coastal and seismic retrofits. South America gains momentum in Brazil's hydro dam repairs and Argentina's grain silos, though import costs temper uptake.

- Albarrie Canada Limited

- Arab Basalt Fiber

- ARMBAS

- Basalt Engineering LLC

- Basaltex

- Basanite Industries LLC

- BASTECH

- Deutsche Basalt Faser GmbH

- EcoBasalt Solutions

- Fiberbas construction and building technologies

- Final Advanced Materials

- Galen Ltd

- Hengdian Group Holdings Limited

- INCOTELOGY GmbH

- Isomatex SA

- JiLin Tongxin Basalt Technology Co.,Ltd

- Kamenny Vek

- MAFIC SA

- Rockwool A/S

- Sudaglass Fiber Technology

- Technobasalt Invest

- Zhejiang Shijin Basalt Fiber Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EU Net-Zero Mandates accelerating basalt rebar

- 4.2.2 Offshore wind-blade build-out needs heat-resistant fabrics

- 4.2.3 Vehicle-lightweighting roadmap in several countries favoring basalt fiber usage

- 4.2.4 GCC desalination expansion driving basalt FRP pipelines

- 4.2.5 LNG platforms requiring cryogenic-tolerant reinforcements

- 4.3 Market Restraints

- 4.3.1 Easy availability of substitutes

- 4.3.2 Basalt-ore freight-rate volatility

- 4.3.3 Abrasive wear on processing equipment raising OPEX

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Volume)

- 5.1 By Form

- 5.1.1 Continuous

- 5.1.2 Discrete

- 5.2 By Usage

- 5.2.1 Composites

- 5.2.2 Non-Composites

- 5.3 By End-Use Industry

- 5.3.1 Building & Construction

- 5.3.2 Automotive

- 5.3.3 Industrial

- 5.3.4 Marine

- 5.3.5 Energy Industry

- 5.3.6 Other (Sports, Chemical Industry, Petroleum Industry)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Albarrie Canada Limited

- 6.4.2 Arab Basalt Fiber

- 6.4.3 ARMBAS

- 6.4.4 Basalt Engineering LLC

- 6.4.5 Basaltex

- 6.4.6 Basanite Industries LLC

- 6.4.7 BASTECH

- 6.4.8 Deutsche Basalt Faser GmbH

- 6.4.9 EcoBasalt Solutions

- 6.4.10 Fiberbas construction and building technologies

- 6.4.11 Final Advanced Materials

- 6.4.12 Galen Ltd

- 6.4.13 Hengdian Group Holdings Limited

- 6.4.14 INCOTELOGY GmbH

- 6.4.15 Isomatex SA

- 6.4.16 JiLin Tongxin Basalt Technology Co.,Ltd

- 6.4.17 Kamenny Vek

- 6.4.18 MAFIC SA

- 6.4.19 Rockwool A/S

- 6.4.20 Sudaglass Fiber Technology

- 6.4.21 Technobasalt Invest

- 6.4.22 Zhejiang Shijin Basalt Fiber Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

- 7.2 Increasing Adoption of Environmentally Friendly Materials

連續玄武岩纖維市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、加工技術、最終用戶、地區和競爭格局分類,2021-2031年

連續玄武岩纖維市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、加工技術、最終用戶、地區和競爭格局分類,2021-2031年 全球玄武岩纖維市場:依形狀、應用、終端用戶產業及地區分類-預測至2031年

全球玄武岩纖維市場:依形狀、應用、終端用戶產業及地區分類-預測至2031年 玄武岩纖維市場:按類型、產品類型、應用和產業分類-2026-2032年全球市場預測

玄武岩纖維市場:按類型、產品類型、應用和產業分類-2026-2032年全球市場預測 連續玄武岩纖維市場:依應用和地區分類

連續玄武岩纖維市場:依應用和地區分類 全球連續玄武岩纖維市場規模、佔有率、趨勢和成長分析報告(2026-2034年)玄武岩纖維市場規模、佔有率、成長及全球產業分析:按類型和應用分類,區域洞察及2026-2034年預測連續玄武岩纖維市場:依纖維類型、加工技術及終端應用產業分類-2026-2032年全球預測

全球連續玄武岩纖維市場規模、佔有率、趨勢和成長分析報告(2026-2034年)玄武岩纖維市場規模、佔有率、成長及全球產業分析:按類型和應用分類,區域洞察及2026-2034年預測連續玄武岩纖維市場:依纖維類型、加工技術及終端應用產業分類-2026-2032年全球預測 日本玄武岩纖維市場:規模、佔有率、趨勢和預測:按產品、類型、形態、製造方法、最終用途行業和地區分類,2026-2034年

日本玄武岩纖維市場:規模、佔有率、趨勢和預測:按產品、類型、形態、製造方法、最終用途行業和地區分類,2026-2034年 玄武岩纖維市場規模、佔有率和趨勢分析報告:按應用、最終用途、地區和細分市場分類,預測至2026-2033年

玄武岩纖維市場規模、佔有率和趨勢分析報告:按應用、最終用途、地區和細分市場分類,預測至2026-2033年 2025-2029年全球玄武岩纖維市場

2025-2029年全球玄武岩纖維市場