|

市場調查報告書

商品編碼

2035117

中鏈甘油三酯(MCT):市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Medium Chain Triglycerides (MCT) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

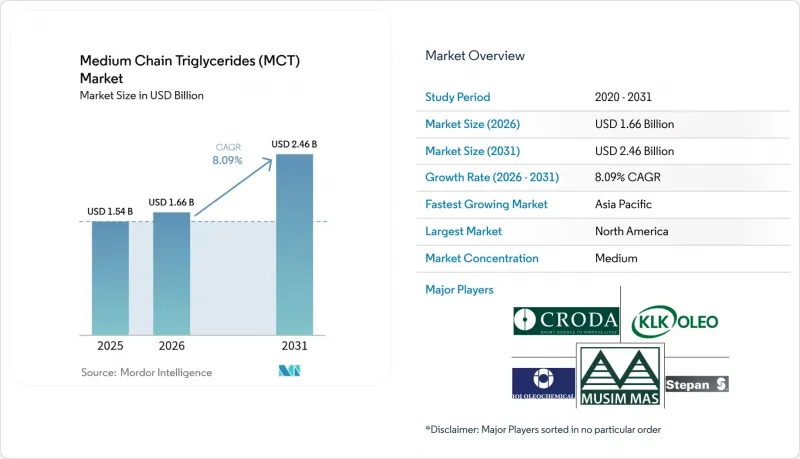

預計中鏈三酸甘油酯 (MCT) 市場將從 2025 年的 15.4 億美元成長到 2026 年的 16.6 億美元,到 2031 年將達到 24.6 億美元,2026 年至 2031 年的複合年成長率為 8.09%。

這一成長主要得益於中鏈三酸甘油酯(MCT)在運動營養、生酮飲食、高階嬰兒配方奶粉和脂質藥物遞送系統等領域的廣泛應用。液態MCT,尤其是椰子油衍生的MCT,因其易於與食品和飲料混合,且能快速、溫和地補充能量,正逐漸被主流市場接受。製藥公司正致力於研究MCT的門靜脈吸收途徑,以提高難溶性活性成分的生物利用度;而化妝品品牌則青睞MCT的輕盈質地和潔淨標示定位。供應鏈策略目前專注於原物料多元化,特別是認證棕櫚仁油和新興油籽,以對沖氣候變遷導致的價格波動。同時,技術投資則集中於提高MCT的純度並開發客製化的脂肪酸混合物。隨著垂直整合企業擴大生產規模,市場競爭仍然溫和,但一些專注於特定領域的創新企業正在臨床營養和特種化妝品領域獲得高價值合約。

全球中鏈三酸甘油酯 (MCT) 市場趨勢及洞察

在運動表現營養領域不斷擴大應用

由於主要成分為辛酸的油脂能在幾分鐘內生成酮體,從而在不引起血糖值飆升的情況下維持運動耐力,運動員擴大使用添加了中鏈甘油三酯(MCT)的凝膠、能量棒和粉末,作為長鏈脂肪酸和簡單碳水化合物的替代品。針對老年人的臨床研究表明,每日補充MCT可以改善肌肉質量,同時減少葡萄糖氧化,這表明MCT對恢復和健康老齡化具有協同作用。調查顯示,相當一部分運動營養產品購買者願意為符合潔淨標示飲食概念的知名單一產地脂肪支付溢價。品牌商現在會在包裝正面標明特定的鍊長比,以區分不同的性能特徵,這促使加工商提出更嚴格的分餾和純度要求。據一家北美契約製造稱,使用液態MCT來確保口感順滑和延長保存期限的生酮友好型即飲飲料的訂單正在實現兩位數成長。在我們的運動員產品線中,我們擴大採用 RSPO 認證的永續棕櫚仁油供應鏈來控制成本,同時實現環境、社會和管治(ESG) 目標。

生酮飲食和低碳水化合物飲食的傳播

生酮飲食的廣泛流行正在改變超市的格局,消費者紛紛尋找能夠快速提升血液酮體的成分。主要成分為辛酸的三辛酸甘油酯(TCP)比傳統椰子油更能有效促進酮體生成,因此在濃縮滴劑和飲品中佔據主導地位。由於中鏈三酸甘油酯(MCT)配方允許攝取比傳統生酮療法更高的碳水化合物,且不會影響癲癇控制,因此醫療專業人員現在開始為癲癇患者開立富含MCT的飲食處方。社群媒體上的美食部落客正在傳播這些臨床證據,加速了MCT在美國、加拿大和西歐家庭的普及。亞洲的都市區消費者也加入了這一潮流,電商平台銷售包含MCT油和葡甘露聚醣纖維的低碳水化合物入門套裝,促使當地精煉商增加小包裝產品和風味產品。這種飲食習慣的轉變透過維持強勁的基準需求和緩解季節性波動,穩定了垂直整合生產者的收入來源。

椰子油和棕櫚仁油的價格波動很大。

天氣造成的供應衝擊常常推高原物料價格。統計模型顯示,棕櫚仁油價格上漲1%會導致椰子油需求增加1.89%,因為買家會在兩種原料之間進行替代,進一步加劇價格波動。印尼和馬來西亞是棕櫚油供應的兩大支柱,兩國降雨不穩定導致鮮果產量下降,進而推高精煉油和油脂化學品的價格。此類價格飆升會對與食品生產商簽訂三個月固定價格合約的MCT精煉商的毛利率帶來壓力。垂直整合到人工林是一種天然的對沖工具,但缺乏農田的小規模加工商則被迫依賴金融衍生品和長期供應契約,這會增加他們的營運資金需求。

細分市場分析

預計到2025年,液體產品將佔銷售額的77.10%,佔據絕對領先地位,並且隨著運動飲料、即飲咖啡和醫療營養品牌青睞速溶易傾倒的產品形式,這一優勢有望進一步擴大。液體產品細分市場預計將以8.74%的複合年成長率成長,超過粉末產品。針對耐力運動員的單次注射安瓿產品便是這一趨勢的鮮明例證。配方研發人員正在實現無需乳化劑的等滲配方,並保持標籤檢視簡潔。相較之下,粉末產品更適合用於能量棒、烘焙混合料和袋裝產品等需要低水分含量和長保存期限的應用。噴霧乾燥和包封技術的進步顯著提高了脂肪含量,並降低了每克有效脂質的成本。然而,與堆積密度和口感相關的挑戰仍然限制了這些粉末產品的應用範圍。卵磷脂負載聚集顆粒等創新技術可望擴大其在即溶飲料的滲透率。

椰子油憑藉著良好的消費者評估和覆蓋菲律賓、印尼和印度的長期供應鏈,預計到2025年將維持75.60%的市場佔有率。在椰子油佔據主導地位的同時,棕櫚仁油的市場佔有率正在迅速擴張,預計其複合年成長率將達到8.56%。馬來西亞煉油商正在投資中游分餾技術,以供應醫藥級C8/C10餾分,這正逐步消除品牌所有者的固有觀念。儘管由於其氣候適應性強、產量穩定的特性,諸如馬卡巴油和合成酯等替代原料正受到越來越多的關注,但其應用仍然有限。跨國公司正在試驗混合多種原料的策略,以規避氣候風險並協調脂肪酸組成,徵兆著本十年末,供應多元化將成為行業標準。

《中鏈三酸甘油酯 (MCT) 報告》按形態(乾粉、液體)、來源(椰子油、棕櫚仁油、其他)、脂肪酸類型(辛酸 (C8)、癸酸 (C10)、月桂酸 (C12)、己酸 (C6))、應用領域(食品飲料、個人護理及化妝品、其他應用和歐洲地區(歐洲地區和歐洲地區進行歐洲地區)。市場預測以美元 (USD) 為單位。

區域分析

預計到2025年,北美將佔全球銷售額的37.90%。該地區受益於美國食品藥物管理局(FDA)明確的GRAS(公認安全)評級,從而促進了各品類產品的快速普及。加拿大機能性食品法規也推動了MCT補充劑的上市,鞏固了該地區的領先地位。

亞太地區是成長最快的地區,年複合成長率達8.76%。中國的「雙循環」政策正在推動國內高附加價值油脂化學品的生產,並帶動了諸如KLK在江蘇省擴建煉油廠等投資項目。印度和印尼不斷上升的出生率支撐了對嬰幼兒配方奶粉的強勁需求,而日本人口老化則推動了臨床營養產品的消費。 2024年,越南和泰國降低了精煉椰子油的進口關稅,刺激了東協內部貿易,並降低了當地混合商的進口成本。

在歐洲,技術主導市場仍佔據主導地位。在德國、法國和英國,高純度中鏈甘油三酯(MCT)被用於藥物傳輸平台和藥妝產品。歐盟2024年推出的新食品核准增強了監管的確定性,但即將訂定的森林砍伐法規提高了未分離棕櫚仁原料的合規門檻。因此,供應商正在加速部署基於衛星的溯源系統。東歐的加工業者正透過黑海走廊增加椰子油的進口,並在國內進行分餾,以避免支付RSPO(永續棕櫚油圓桌會議)的溢價費用。這種方法雖然可以降低成本,但需要嚴格的內部永續性審計。

在南美洲,巴西的運動營養品市場呈現穩定成長態勢,國內的馬卡巴種植園可望為未來提供穩定的原料供應。中東和非洲地區仍在發展中,但隨著醫療營養領域的競標以及海灣合作理事會(GCC)國家推出清真認證的個人保健產品,市場正在逐步開放。非洲大陸自由貿易區(AfCFTA)內的貿易獎勵措施預計將在未來十年內促進本地分餾中心的建立,儘管基礎設施和原料採購仍處於起步階段。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 中鏈三酸甘油酯在運動和體能營養領域的應用日益廣泛

- 生酮飲食和低碳水化合物飲食的傳播

- 在個人護理和化妝品領域不斷拓展應用。

- 基於脂質的藥物遞送系統中的MCT

- 亞洲對優質嬰兒配方奶粉的需求

- 市場限制因素

- 椰子油和棕櫚仁油價格波動

- 替代功能性脂質的可用性

- 棕櫚油採購中永續性認證的成本。

- 價值鏈分析

- 波特五力分析

- 供應商議價能力

- 買方的議價能力

- 新參與企業的威脅

- 替代品的威脅

- 競爭公司之間的競爭關係

第5章 市場規模與成長預測

- 按形狀

- 乾燥

- 液體

- 按原料

- 椰子油

- 棕櫚仁油

- 其他

- 按脂肪酸類型

- 辛酸(C8)

- 卡普里克(C10)

- 月桂酸(C12)

- 己酸(C6)

- 透過使用

- 食品/飲料

- 個人護理和化妝品

- 其他用途

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 土耳其

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 南非

- 奈及利亞

- 埃及

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- AAK AB

- ABITEC

- Acme-Hardesty

- Barlean's Organic Oils, LLC

- BASF SE

- ConnOils

- CREMER OLEO GmbH & Co. KG

- Croda International Plc

- Henry Lamotte Oils GmbH

- IOI Oleo GmbH

- Jarrow Formulas Inc.

- Kerry Group plc

- KLK Oleo

- Musim Mas Group

- Oleon NV

- Stepan Company

- Sternchemie GmbH & Co. KG

- The Nisshin OilliO Group Ltd.

- Vitaflo International Ltd.

- Wilmar International Ltd.

第7章 市場機會與未來展望

The Medium Chain Triglycerides market size is expected to grow from USD 1.54 billion in 2025 to USD 1.66 billion in 2026 and is forecast to reach USD 2.46 billion by 2031 at 8.09% CAGR over 2026-2031.

Growth is led by widening usage in sports nutrition, ketogenic diets, premium infant formulas, and lipid-based drug delivery systems. Liquid formats, particularly those sourced from coconut oil, underpin mainstream adoption because they blend easily into foods and beverages while delivering rapid, stomach-friendly energy. Pharmaceutical formulators value MCTs' portal-vein absorption pathway, which enhances bioavailability for poorly soluble actives, and cosmetic brands prize their light texture and clean-label positioning. Supply-side strategies now center on source diversification-especially into certified palm kernel oil and emerging oil crops-to hedge climate-related price swings, while technology investments focus on purity upgrades and tailored fatty-acid blends. Competitive intensity remains moderate as vertically integrated players scale production, yet niche innovators secure premium contracts in clinical nutrition and specialty cosmetics.

Global Medium Chain Triglycerides (MCT) Market Trends and Insights

Growing Usage in Sports & Performance Nutrition

Athletes increasingly replace long-chain fats and simple carbohydrates with MCT-fortified gels, shots, and powders because caprylic-dominant oils generate ketones within minutes, sustaining endurance without glycemic spikes. Clinical work in older adults shows that daily MCT supplementation enhances muscle quality while lowering glucose oxidation, hinting at crossover benefits for recovery and healthy aging. Research highlights that a significant portion of sports-nutrition buyers are willing to pay a premium for recognizable, single-origin lipids that align with clean-label diets. Brand owners now list specific chain-length ratios on front-of-pack claims to differentiate performance profiles, pushing processors toward tighter fractionation and purity specifications. North American contract-manufacturers report double-digit order growth for keto-friendly ready-to-drink beverages that rely on liquid MCTs for smooth mouthfeel and shelf stability. Sustainable palm kernel supply chains that carry RSPO certification are being tapped to manage cost while meeting Environmental, Social, and Governance (ESG) targets in athlete-focused product lines.

Rising Adoption of Ketogenic & Low-Carb Diets

Widespread interest in ketogenic eating is re-shaping grocery aisles as shoppers seek ingredients that elevate circulating ketone bodies quickly. Caprylic-dominant tricaprylin delivers the most efficient ketogenic response compared with traditional coconut oil, driving its dominance in concentrated drops and shots. Medical professionals now prescribe MCT-enriched meal plans to epilepsy patients because medium-chain triglyceride formulations allow higher carbohydrate intake than classical ketogenic protocols without compromising seizure control. Social-media recipe influencers amplify this clinical endorsement, accelerating household penetration in the United States, Canada, and Western Europe. Asian urban consumers are joining the trend as e-commerce platforms bundle MCT oil with glucomannan fibers in low-carb starter packs, prompting regional refiners to add smaller SKUs and flavored variants. The dietary shift sustains robust baseline demand and mitigates seasonality, anchoring revenue streams for vertically integrated producers.

Volatile Coconut & Palm Kernel Oil Prices

Weather-driven supply shocks frequently lift feedstock prices. Statistical modelling shows that a 1% uptick in palm kernel oil prices can push coconut-oil demand higher by 1.89% as buyers substitute between the two inputs, amplifying volatility. Erratic rainfall in Indonesia and Malaysia, the twin pillars of palm supply, depresses fresh-fruit bunch yields and spills into refined-oleochemical pricing. Such spikes compress gross margins for MCT refiners that operate on three-month fixed-price contracts with food manufacturers. Vertical integration into plantations offers a natural hedge, but smaller processors without acreage must rely on financial derivatives or long-term supply agreements, which can raise working-capital requirements.

Other drivers and restraints analyzed in the detailed report include:

- Expansion in Personal Care & Cosmetics Applications

- MCTs in Lipid-Based Drug Delivery Systems

- Availability of Alternative Functional Lipids

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Liquid products accounted for 77.10% sales in 2025, a commanding lead that will widen as sports-drink, RTD coffee, and medical-nutrition brands prefer pourable formats for quick dispersion. The liquid sub-category is projected to grow at 8.74% CAGR, outpacing powders. One-shot ampoules targeting endurance athletes illustrate the trend: formulators achieve isotonic profiles without emulsifiers, preserving label simplicity. In contrast, powders cater to bars, bakery mixes, and sachets, where low moisture and long shelf life matter. Advancements in spray-drying and encapsulation have significantly improved oil-load capacity, reducing the cost per gram of active lipid. However, challenges like bulk density and mouth-feel limitations continue to confine these powders to specialized applications. Innovations such as agglomerated granules with lecithin carriers could expand penetration into instant beverages.

Coconut oil retained a 75.60% share in 2025 thanks to positive consumer perception and long-standing supply chains across the Philippines, Indonesia, and India. That dominance masks rapid palm kernel oil gains: the latter is forecast at 8.56% CAGR. Malaysian refiners are investing in mid-stream fractionation to supply pharmaceutical-grade C8/C10 cuts, eroding brand-owner prejudice. Alternative feedstocks like macauba and synthetic esters are gaining attention due to their climate-resilient yields, despite their limited adoption. Multinationals trial blended-source strategies to hedge climate risks and harmonize fatty-acid spectra, a sign that supply diversification will become standard by the decade's end.

The Medium Chain Triglycerides Report is Segmented by Form (Dry, Liquid), Source (Coconut Oil, Palm Kernel Oil, Others), Fatty Acid Type (Caprylic (C8), Capric (C10), Lauric (C12), Caproic (C6)), Application (Food and Beverage, Personal Care and Cosmetics, Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 37.90% revenue in 2025. The region benefits from well-defined FDA GRAS rulings, enabling swift cross-category adoption. Canadian functional-food regulations similarly streamline MCT-supplement launches, cementing regional leadership.

Asia-Pacific is the fastest-growing territory at 8.76% CAGR. China's dual-circulation policy encourages domestic production of high-value oleochemicals, catalyzing investments such as KLK's expanded refinery in Jiangsu. Rising birth rates in India and Indonesia underpin robust infant-formula demand, while Japan's aging population fuels clinical-nutrition consumption. Import duties on refined coconut oil were cut in Vietnam and Thailand during 2024, facilitating intra-ASEAN trade and lowering landed costs for local blenders.

Europe maintains a technology-driven market. Germany, France, and the United Kingdom source high-purity MCTs for drug-delivery platforms and cosmeceuticals. The EU's 2024 novel-food approvals cement regulatory certainty, yet the imminent Deforestation Regulation raises compliance hurdles for non-segregated palm-kernel material; as a result, suppliers are accelerating satellite-based traceability systems. Eastern European processors increasingly import raw coconut oil via the Black Sea corridor, then fractionate internally to sidestep RSPO premium charges, a tactic that trims cost yet demands stringent in-house sustainability audits.

South America shows steady growth as Brazil's sports-nutrition category broadens and domestic macauba plantations promise future feedstock resilience. Middle East & Africa remain nascent but are opening via medical-nutrition tenders and halal-certified personal-care launches in the Gulf Cooperation Council states. Trade incentives in the African Continental Free Trade Area may foster local fractionation hubs over the next decade, though infrastructure and feedstock availability remain early-stage.

- AAK AB

- ABITEC

- Acme-Hardesty

- Barlean's Organic Oils, LLC

- BASF SE

- ConnOils

- CREMER OLEO GmbH & Co. KG

- Croda International Plc

- Henry Lamotte Oils GmbH

- IOI Oleo GmbH

- Jarrow Formulas Inc.

- Kerry Group plc

- KLK Oleo

- Musim Mas Group

- Oleon NV

- Stepan Company

- Sternchemie GmbH & Co. KG

- The Nisshin OilliO Group Ltd.

- Vitaflo International Ltd.

- Wilmar International Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing usage of MCTs in sports and performance nutrition

- 4.2.2 Rising adoption of ketogenic and low-carb diets

- 4.2.3 Expansion in personal care and cosmetics applications

- 4.2.4 MCTs in lipid-based drug delivery systems

- 4.2.5 Premium infant formula demand in Asia

- 4.3 Market Restraints

- 4.3.1 Volatile coconut and palm kernel oil prices

- 4.3.2 Availability of alternative functional lipids

- 4.3.3 Sustainability certification costs for palm sourcing

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Form

- 5.1.1 Dry

- 5.1.2 Liquid

- 5.2 By Source

- 5.2.1 Coconut Oil

- 5.2.2 Palm Kernel Oil

- 5.2.3 Others

- 5.3 By Fatty Acid Type

- 5.3.1 Caprylic (C8)

- 5.3.2 Capric (C10)

- 5.3.3 Lauric (C12)

- 5.3.4 Caproic (C6)

- 5.4 By Application

- 5.4.1 Food and Beverage

- 5.4.2 Personal Care and Cosmetics

- 5.4.3 Other Applications

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Malaysia

- 5.5.1.6 Thailand

- 5.5.1.7 Indonesia

- 5.5.1.8 Vietnam

- 5.5.1.9 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Turkey

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 South Africa

- 5.5.5.5 Nigeria

- 5.5.5.6 Egypt

- 5.5.5.7 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AAK AB

- 6.4.2 ABITEC

- 6.4.3 Acme-Hardesty

- 6.4.4 Barlean's Organic Oils, LLC

- 6.4.5 BASF SE

- 6.4.6 ConnOils

- 6.4.7 CREMER OLEO GmbH & Co. KG

- 6.4.8 Croda International Plc

- 6.4.9 Henry Lamotte Oils GmbH

- 6.4.10 IOI Oleo GmbH

- 6.4.11 Jarrow Formulas Inc.

- 6.4.12 Kerry Group plc

- 6.4.13 KLK Oleo

- 6.4.14 Musim Mas Group

- 6.4.15 Oleon NV

- 6.4.16 Stepan Company

- 6.4.17 Sternchemie GmbH & Co. KG

- 6.4.18 The Nisshin OilliO Group Ltd.

- 6.4.19 Vitaflo International Ltd.

- 6.4.20 Wilmar International Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

中鏈三酸甘油酯市場報告:按類型、原料、形態、應用和地區分類(2026-2034 年)

中鏈三酸甘油酯市場報告:按類型、原料、形態、應用和地區分類(2026-2034 年) 中鏈三酸甘油酯市場:依類型、原料、形態、應用及銷售管道分類-2026-2032年全球市場預測

中鏈三酸甘油酯市場:依類型、原料、形態、應用及銷售管道分類-2026-2032年全球市場預測 2026年全球中鏈脂肪酸市場報告

2026年全球中鏈脂肪酸市場報告 全球三丁基醚市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034)

全球三丁基醚市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034) 中鏈甘油三酯市場規模、佔有率和趨勢分析報告:按應用、地區和細分市場預測(2026-2033 年)日本中鏈三酸甘油酯市場報告(按類型(己酸、辛酸、癸酸、月桂酸)、來源、形態、應用和地區分類,2026-2034)

中鏈甘油三酯市場規模、佔有率和趨勢分析報告:按應用、地區和細分市場預測(2026-2033 年)日本中鏈三酸甘油酯市場報告(按類型(己酸、辛酸、癸酸、月桂酸)、來源、形態、應用和地區分類,2026-2034) 三丁酸甘油酯市場規模、佔有率和成長分析(按應用、最終用戶、原料、等級、包裝類型、類型和地區分類)—2026-2033年產業預測

三丁酸甘油酯市場規模、佔有率和成長分析(按應用、最終用戶、原料、等級、包裝類型、類型和地區分類)—2026-2033年產業預測 中鏈三酸甘油酯市場規模、佔有率和成長分析(按脂肪酸類型、形式、來源、應用和地區分類)—產業預測(2026-2033 年)

中鏈三酸甘油酯市場規模、佔有率和成長分析(按脂肪酸類型、形式、來源、應用和地區分類)—產業預測(2026-2033 年) 中鏈三酸甘油酯 (MCT) - 全球市場佔有率和排名、總收入和需求預測(2025-2031 年)

中鏈三酸甘油酯 (MCT) - 全球市場佔有率和排名、總收入和需求預測(2025-2031 年) 中鏈甘油三酸酯市場-全球產業規模、佔有率、趨勢、機會和預測(按脂肪酸類型、應用、地區和競爭細分,2020-2030 年)

中鏈甘油三酸酯市場-全球產業規模、佔有率、趨勢、機會和預測(按脂肪酸類型、應用、地區和競爭細分,2020-2030 年)