|

市場調查報告書

商品編碼

2035105

印刷基板檢測設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Printed Circuit Board Inspection Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

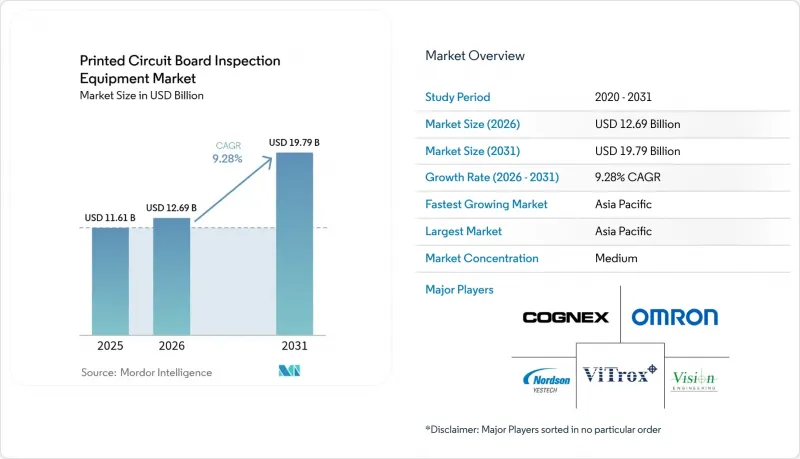

預計到 2026 年,印刷基板偵測設備的市場規模將達到 126.9 億美元,高於 2025 年的 116.1 億美元,預計到 2031 年將達到 197.9 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 9.28%。

快速小型化、汽車和醫療用電子設備中強制性的零缺陷要求以及先進封裝中亞微米級的公差要求,正在重新評估投資重點。雖然目前線上自動光學檢測 (AOI) 平台佔據了大部分市場需求,但隨著體積成像、共面性測量和收費檢測在高密度互連和晶片基板中變得至關重要,3D AOI 和 3D X光系統的應用正在加速。電子產品製造商也正在轉向「按次付費」的服務模式,將設備成本與吞吐量掛鉤,同時人工智慧 (AI) 驅動的缺陷分類正在減少誤報並提高有效生產能力。亞太地區在銷售額方面主導,其中汽車電子是成長最快的終端用戶領域,每輛電動車 (EV) 的電子元件價值增加 1,500 至 2,000 美元。

全球印刷基板檢測設備市場趨勢及洞察

電子元件小型化和元件密度提高的進展

智慧型手機元件間距已縮小至 0.3 毫米,迫使製造商放棄人工目視檢查,轉而採用能夠識別小於 20 微米微結構的 AOI 系統。 50 微米至 150 微米的微孔、盲孔和嵌入式通孔堆疊以及線路重布下方的銅柱在2D灰階影像中均無法顯示。

2024年,台灣工業技術研究院展示了一款採用深紫外線(DUV)技術、解析度為20奈米的原型機,用於檢測晶片基板上的微小裂縫。在當今時代,即使是價值5000美元的資料中心GPU基板的單一缺陷也可能導致報廢成本,因此,每基板只需15秒即可完成的線上3D檢測技術在經濟上是完全可行的。

汽車電子和電動汽車的發展

預計到 2024 年全球電動車產量將達到 1,400 萬輛,到 2030 年將超過 4,000 萬輛。每輛電動車都包含一個電源模組、一個電池管理板和一個駕駛輔助控制器,因此其 PCB 負載是內燃機汽車的三倍。

一級供應商正逐步過渡到100%線上X光檢測,以滿足IATF 16949可靠性標準;同時,ISO 26262標準要求對安全相關組件的檢測結果進行電子追溯。檢測標準的日益嚴格推動了對3D AOI和3D電腦斷層掃描(CT)平台的需求。

先進的AOI和AXI系統需要大量的初始投資。

基於雷射三角測量技術的3D AOI平台售價在15萬至40萬美元之間,而亞微米級精度的CT X光系統售價則超過60萬美元。如此高昂的成本構成了一項重大挑戰,尤其對於成本敏感型市場中的企業而言,因為這些設備需要大量的前期投資。 2022年至2024年間,利率上升導致加權平均資本成本(WACC)增加了150至200個基點,延長了投資回收期並延遲了設備訂購,進一步加重了企業的財務負擔。這些財務壓力迫使許多公司重新評估其資本配置策略。設備即服務(EaaS)透過將資本支出(CAPEX)轉化為營運支出(OPEX)來減輕企業的初始財務負擔,但其應用仍主要局限於已開發國家。這種有限的普及率歸因於這些地區先進的基礎設施、有利的法規環境以及較高的技術成熟度等因素。

細分市場分析

到2025年,自動化光學檢測將佔銷售額的56.93%,顯示2D和新興的3D光學技術能夠處理的任務範圍非常廣泛。同時,受球柵陣列(BGA)、量子點封裝(QFN)和矽封裝(SiP)模組普及的推動,X光檢測預計將以10.74%的複合年成長率成長至2031年。電腦斷層掃描器將取代破壞性的截面檢測,以1µm的體素解析度穿透矽通孔(TSV)內的微凸塊和空隙。雖然對於間距大於0.5mm的元件,光學檢測站仍具有成本效益,但隨著0.3mm間距元件的普及,其適用範圍將縮小。焊膏檢測已完全整合到表面黏著技術線中,透過及早發現鋼網缺陷,可將下游返工減少80%以上。

X光檢測技術的應用主要受半導體封裝趨勢的推動,這種趨勢正促使晶片組架構被引入PCB組裝線。 Comet和Waygate等供應商目前提供針對高產能基板線最佳化的CT掃描儀,這些掃描儀兼具半導體級解析度和輸送機式處理能力。光學檢測設備在低風險消費品領域仍佔據主導地位,但智慧型手機中屏下相機和可折疊軟性尾翼的體積檢測需求也在不斷成長。總體而言,X光檢測技術的成長正在推動印刷基板檢測設備市場的發展,因為它能夠檢測可見光無法觸及的區域。

預計到2025年,線上檢測系統將佔市場需求的60.72%,複合年成長率(CAGR)高達11.68%,是所有外形規格中成長率最高的。與輸送機整合,可在15-30秒內完成每塊電路基板的100%檢測,且不會中斷生產流程。與印表機和貼片機的封閉回路型回饋機制,使得缺陷偵測後能夠立即進行製程修正,這是離線偵測站無法實現的。按次計費的收費模式進一步促進了線上檢測系統的普及,因為它將檢測成本視為與小批量生產相關的可變成本。

在工程實驗室中,柔軟性比速度更重要,離線和桌上型工作站仍然被廣泛用於產品的第一手檢測,以及醫療設備和航空電子設備的小批量生產。然而,隨著契約製造製造商將多項任務整合到單一線上節點中,它們的部署數量正在逐漸下降。因此,印刷電路基板檢測設備市場越來越依賴線上平台,這不僅體現在規模上,也體現在智慧工廠環境所需的數據細節層面。

區域分析

預計到2025年,亞太地區將佔全球整體銷售額的37.88%,並在2031年之前以11.12%的複合年成長率持續成長。光是中國就佔全球電子製造業的28%,富士康和立訊精密等代工組裝均位於中國,使得線上AOI技術對智慧型手機、筆記型電腦和穿戴式裝置等產品線至關重要。韓國和台灣專注於用於記憶體模組和資料中心加速器的HDI基板,而日本在汽車和工業電子領域保持著高階利基市場的地位,這也解釋了為何能夠率先採用CT掃描技術。中國的「中國製造2025」和韓國的「K-Semiconductor戰略」等政府計畫正在津貼智慧工廠工具,進一步推動了區域需求。

預計到2025年,北美和歐洲將佔總總合的約44.62%。美國《晶片與科學法案》撥款520億美元用於半導體和先進封裝工廠,其中大部分將用於採購基板和中介層生產線的檢測設備。德國、法國和義大利正在擴大汽車電子產品的產能,並引入CT X光檢測技術以確保電池組和功率模組的品質。 FDA 21 CFR 820(醫療設備)和AS9100 (航太)等監理系統正在鞏固離線CT和聲學顯微鏡的銷售基礎。

中東、非洲和南美洲的成長呈現出區域差異,儘管它們的市場佔有率較小。以色列的國防和醫療設備產業需要IPC 3級可追溯性,這推動了CT設備的採購。沙烏地阿拉伯和阿拉伯聯合大公國已啟動國內電子產品項目,作為其經濟多元化政策的一部分,從而創造了對中端AOI設備的需求。巴西和阿根廷正在組裝家用電子電器和工業控制設備以供本地消費,它們傾向於選擇具有成本競爭力的2DAOI設備,同時也逐步採用工業4.0數據採集技術。這些新興地區正在擴大印刷基板檢測設備市場的規模,使其超越傳統的主要市場。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子元件小型化和元件密度提高的進展

- 透過工業4.0擴大智慧製造生產線的應用

- 汽車電子和電動汽車的發展

- 透過引入先進的人工智慧缺陷分類技術來減少誤報。

- 透過按次收費和設備即服務 (EaaS)經營模式。

- 先進封裝和晶片級PCB對亞微米3D檢測的需求

- 市場限制因素

- 先進的AOI/AXI系統需要大量的初始資本投資。

- 熟練的系統程式設計師和維修技術人員短缺

- 科技快速過時導致投資回報週期縮短

- 高功率X光偵測線的輻射安全合規成本

- 價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 透過測試方法

- 自動光學檢測(AOI)

- X光檢查(AXI)

- 焊膏測試(SPI)

- 其他特殊技術(聲學、雷射、熱成像)

- 依系統類型

- 線上系統

- 離線/桌上型系統

- 透過技術

- 2D AOI

- 3D AOI

- 2DX光

- 3D/CT X光

- 最終用戶

- 家用電子電器製造商

- 汽車電子製造商

- 工業和能源電子設備

- 航太/國防

- 醫療設備製造商

- 按PCB類型

- 剛性PCB

- 軟性基板和軟硬複合基板

- 高密度佈線(HDI)印刷基板

- 先進封裝基板

- 地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞洲地區

- 中東

- 以色列

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nordson Corporation

- Koh Young Technology Inc.

- Omron Corporation

- ViTrox Corporation Berhad

- Mirtec Co., Ltd.

- Viscom AG

- Saki Corporation

- CyberOptics Corporation

- Test Research Inc.

- KLA Corporation

- Camtek Ltd.

- Yamaha Motor Co., Ltd.(Yamaha SMT)

- Unicomp Technology Co., Ltd.

- Nikon Corporation

- Comet Yxlon GmbH

- Waygate Technologies GmbH

- Shenzhen JT Automation Equipment Co., Ltd.

- GOPEL electronic GmbH

- Machine Vision Products Inc.

- Pemtron Corporation

第7章 市場機會與未來展望

printed circuit board inspection equipment market size in 2026 is estimated at USD 12.69 billion, growing from 2025 value of USD 11.61 billion with 2031 projections showing USD 19.79 billion, growing at 9.28% CAGR over 2026-2031.

Rapid miniaturization, zero-defect mandates in automotive and medical electronics, and sub-micron tolerance requirements in advanced packaging are reshaping investment priorities. Inline automatic optical inspection (AOI) platforms dominate current demand, yet 3D AOI and 3D X-ray systems are accelerating because volumetric imaging, coplanarity measurement, and micro-void detection are now essential for high-density interconnect and chiplet substrates. Electronics manufacturers are also shifting toward pay-per-inspection service models that align equipment costs with throughput, while artificial-intelligence-enabled defect classification reduces false calls and lifts effective capacity. Asia-Pacific leads revenue generation, and automotive electronics is the quickest-expanding end-user segment as electric vehicles (EVs) add USD 1,500-2,000 of electronic content per unit.

Global Printed Circuit Board Inspection Equipment Market Trends and Insights

Increasing Miniaturization and Higher Component Densities in Electronics

Component pitch in smartphones has already tightened to 0.3 mm, forcing manufacturers to retire manual visual checks in favour of AOI systems able to resolve features below 20 µm. Microvias between 50 µm and 150 µm, blind or buried via stacks, and copper pillars beneath redistribution layers are invisible to 2D grayscale imaging.

Taiwan's Industrial Technology Research Institute demonstrated a deep-UV 20 nm-resolution prototype in 2024 that identifies micro-cracks in chiplet substrates. As a single defect on a USD 5,000 data-center GPU substrate now drives scrap cost, inline 3D inspection at 15 s per board is economically justified.

Growth in Automotive Electronics and Electric Vehicles

Global EV output climbed to 14 million units in 2024 and is expected to surpass 40 million units by 2030. Each EV integrates power modules, battery-management boards, and driver-assistance controllers that collectively triple PCB content versus internal-combustion vehicles.

Tier-1 suppliers have moved to 100% inline X-ray inspection to meet IATF 16949 reliability standards, while ISO 26262 mandates electronic traceability of inspection results for safety-related assemblies. Increased inspection intensity lifts demand for both 3D AOI and 3D computed tomography (CT) platforms.

High Initial Capital Investments for Advanced AOI And AXI System

Prices for a laser-triangulation 3D AOI platform range from USD 150,000 to 400,000, whereas a sub-micron CT X-ray system commands a price tag exceeding USD 600,000. These high costs pose significant challenges for companies, particularly those operating in cost-sensitive markets, as they require substantial upfront investments. Between 2022 and 2024, rising interest rates pushed the weighted average cost of capital up by 150 to 200 basis points, further straining financial resources by elongating payback periods and causing delays in equipment orders. This financial pressure has led many businesses to reassess their capital allocation strategies. While equipment-as-a-service offerings transform capital expenditure into operational expenditure (OPEX), enabling companies to reduce initial financial burdens, their adoption remains largely confined to mature economies. This limited uptake is attributed to factors such as the availability of advanced infrastructure, favorable regulatory environments, and higher levels of technological readiness in these regions.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption of Industry 4.0 Smart Manufacturing Lines

- Deployment of Advanced AI-Enabled Defect Classification Reducing False Calls

- Shortage Of Skilled Technicians for System Programming and Maintenance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Automatic optical inspection delivered 56.93% of 2025 revenue, demonstrating the breadth of tasks addressable by 2D and emerging 3D optics. X-ray inspection, however, is forecast to expand at an 10.74% CAGR through 2031 as ball-grid arrays, QFNs, and SiP modules proliferate. Computed-tomography units visualize voiding in micro-bumps and through-silicon vias at 1 µm voxel resolution, replacing destructive cross-sectioning. Optical-only stations remain cost-effective for components above 0.5 mm pitch, but their addressable share will narrow as 0.3 mm pitch becomes mainstream. Solder-paste inspection is fully integrated into surface-mount lines to catch stencil defects early, reducing downstream rework by more than 80%.

X-ray adoption draws support from semiconductor packaging trends that push chiplet architectures onto PCB assembly floors. Vendors such as Comet and Waygate now offer CT scanners tailored for high-throughput board lines, merging semiconductor-class resolution with conveyorized handling. Optical stations still dominate low-risk consumer products, yet even in smartphones volumetric checks are rising for under-display cameras and folded flex tails. Overall, x-ray growth lifts the printed circuit board inspection equipment market by unlocking inspection windows unreachable by visible light.

Inline systems held 60.72% of 2025 demand and are projected to progress at a 11.68% CAGR, the fastest among all form factors. Their conveyor integration enables 100% board coverage at 15-30 s per piece without interrupting flow. Closed-loop feedback with printers and placement machines converts defect detection into immediate process correction, a capability that offline stations cannot match. Pay-per-inspection agreements further tilt economics toward inline purchases by treating inspection as a variable cost tied to low volume.

Offline and benchtop stations continue to serve engineering labs, first-article inspections, and low-volume medical, and avionics builds where flexibility outweighs speed. Yet their installed base is slowly declining as contract manufacturers consolidate multiple tasks into single inline nodes. The printed circuit board inspection equipment market therefore leans on inline platforms not only for scale but also for data granularity needed in smart-factory environments.

The Printed Circuit Board Inspection Equipment Market Report is Segmented by Inspection Method (Automatic Optical Inspection, and More), System Type (Inline Systems, and More), Technology (2D AOI, 3D AOI, and More), End User (Consumer Electronics, Automotive Electronics, and More), PCB Type (Rigid PCBs, Flexible and Rigid-Flex PCBs, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific delivered 37.88% of global revenue in 2025 and is expected to expand at an 11.12% CAGR to 2031. China alone accounts for 28% of worldwide electronics manufacturing and hosts contract assemblers such as Foxconn and Luxshare Precision that mandate inline AOI across smartphone, laptop, and wearable lines. South Korea and Taiwan specialize in HDI substrates for memory modules and data-center accelerators, while Japan maintains a premium niche in automotive and industrial electronics that justifies early adoption of CT inspection. Government programs like China's Made in China 2025 and South Korea's K-Semiconductor Strategy subsidize smart-factory tools, further lifting regional demand.

North America and Europe jointly held roughly 44.62% of 2025 turnover. The United States CHIPS and Science Act allocate USD 52 billion for semiconductor and advanced-packaging plants, many of which will source inspection equipment for substrate and interposer lines. Germany, France, and Italy are upgrading automotive electronics capacity, installing CT X-ray to safeguard battery-pack and power-module quality. Regulatory regimes such as FDA 21 CFR 820 for medical devices and AS9100 for aerospace secure a baseline of offline CT and acoustic microscopy sales.

The Middle East, Africa, and South America contribute smaller shares but demonstrate patchy growth. Israel's defense and medical-device sector insist on IPC Class 3 traceability, prompting CT purchases. Saudi Arabia and the United Arab Emirates have launched domestic electronics programs as part of diversification agendas, adding mid-tier AOI demand. Brazil and Argentina assemble consumer electronics and industrial controls for regional consumption, favouring cost-competitive 2D AOI units yet gradually incorporating Industry 4.0 data collection. These emerging hubs collectively enlarge the printed circuit board inspection equipment market footprint beyond traditional strongholds.

- Nordson Corporation

- Koh Young Technology Inc.

- Omron Corporation

- ViTrox Corporation Berhad

- Mirtec Co., Ltd.

- Viscom AG

- Saki Corporation

- CyberOptics Corporation

- Test Research Inc.

- KLA Corporation

- Camtek Ltd.

- Yamaha Motor Co., Ltd. (Yamaha SMT)

- Unicomp Technology Co., Ltd.

- Nikon Corporation

- Comet Yxlon GmbH

- Waygate Technologies GmbH

- Shenzhen JT Automation Equipment Co., Ltd.

- GOPEL electronic GmbH

- Machine Vision Products Inc.

- Pemtron Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Miniaturization and Higher Component Densities in Electronics

- 4.2.2 Rising Adoption of Industry 4.0 Smart Manufacturing Lines

- 4.2.3 Growth in Automotive Electronics and Electric Vehicles

- 4.2.4 Deployment of Advanced AI-Enabled Defect Classification Reducing False Calls

- 4.2.5 Pay-Per-Inspection and Equipment-as-a-Service Business Models Lowering CapEx Barriers

- 4.2.6 Demand for Sub-Micron 3D Inspection in Advanced Packaging and Chiplet PCBs

- 4.3 Market Restraints

- 4.3.1 High Initial Capital Investments for Advanced AOI/AXI Systems

- 4.3.2 Shortage of Skilled Technicians for System Programming and Maintenance

- 4.3.3 Rapid Technology Obsolescence Leading to Compressed ROI Cycles

- 4.3.4 Radiation Safety Compliance Costs for High-Power X-Ray Inspection Lines

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Inspection Method

- 5.1.1 Automatic Optical Inspection (AOI)

- 5.1.2 X-Ray Inspection (AXI)

- 5.1.3 Solder Paste Inspection (SPI)

- 5.1.4 Other Specialized Methods (Acoustic, Laser, Thermography)

- 5.2 By System Type

- 5.2.1 Inline Systems

- 5.2.2 Offline / Benchtop Systems

- 5.3 By Technology

- 5.3.1 2D AOI

- 5.3.2 3D AOI

- 5.3.3 2D X-Ray

- 5.3.4 3D / CT X-Ray

- 5.4 By End User

- 5.4.1 Consumer Electronics Manufacturers

- 5.4.2 Automotive Electronics Manufacturers

- 5.4.3 Industrial and Energy Electronics

- 5.4.4 Aerospace and Defense

- 5.4.5 Medical Device Manufacturers

- 5.5 By PCB Type

- 5.5.1 Rigid PCBs

- 5.5.2 Flexible and Rigid-Flex PCBs

- 5.5.3 High-Density Interconnect (HDI) PCBs

- 5.5.4 Advanced Packaging Substrates

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia

- 5.6.4 Middle East

- 5.6.4.1 Israel

- 5.6.4.2 Saudi Arabia

- 5.6.4.3 United Arab Emirates

- 5.6.4.4 Turkey

- 5.6.4.5 Rest of Middle East

- 5.6.5 Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Egypt

- 5.6.5.3 Rest of Africa

- 5.6.6 South America

- 5.6.6.1 Brazil

- 5.6.6.2 Argentina

- 5.6.6.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Nordson Corporation

- 6.4.2 Koh Young Technology Inc.

- 6.4.3 Omron Corporation

- 6.4.4 ViTrox Corporation Berhad

- 6.4.5 Mirtec Co., Ltd.

- 6.4.6 Viscom AG

- 6.4.7 Saki Corporation

- 6.4.8 CyberOptics Corporation

- 6.4.9 Test Research Inc.

- 6.4.10 KLA Corporation

- 6.4.11 Camtek Ltd.

- 6.4.12 Yamaha Motor Co., Ltd. (Yamaha SMT)

- 6.4.13 Unicomp Technology Co., Ltd.

- 6.4.14 Nikon Corporation

- 6.4.15 Comet Yxlon GmbH

- 6.4.16 Waygate Technologies GmbH

- 6.4.17 Shenzhen JT Automation Equipment Co., Ltd.

- 6.4.18 GOPEL electronic GmbH

- 6.4.19 Machine Vision Products Inc.

- 6.4.20 Pemtron Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

半導體測試系統市場機會、成長要素、產業趨勢分析及2026-2035年預測

半導體測試系統市場機會、成長要素、產業趨勢分析及2026-2035年預測 直流探針台市場報告:趨勢、預測與競爭分析(至2035年)

直流探針台市場報告:趨勢、預測與競爭分析(至2035年) 半導體測試系統市場:按產品類型、組件和最終用戶分類 - 2026-2032年全球預測CoC老化測試儀市場按技術、腔室類型、壓力範圍、應用和最終用途分類,全球預測(2026-2032年)

半導體測試系統市場:按產品類型、組件和最終用戶分類 - 2026-2032年全球預測CoC老化測試儀市場按技術、腔室類型、壓力範圍、應用和最終用途分類,全球預測(2026-2032年) 半導體測試設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

半導體測試設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球印刷基板檢測設備市場報告2026年半導體檢測透鏡全球市場報告

2026年全球印刷基板檢測設備市場報告2026年半導體檢測透鏡全球市場報告 全球半導體測試設備市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034)SoC 和記憶體半導體測試儀市場(按測試模式、測試儀類型、製程節點、封裝類型、應用和最終用戶分類)—2026-2032 年全球預測SoC老化測試設備市場按容量、技術節點、處理器類型、測試解決方案和應用分類 - 全球預測(2026-2032年)

全球半導體測試設備市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034)SoC 和記憶體半導體測試儀市場(按測試模式、測試儀類型、製程節點、封裝類型、應用和最終用戶分類)—2026-2032 年全球預測SoC老化測試設備市場按容量、技術節點、處理器類型、測試解決方案和應用分類 - 全球預測(2026-2032年)