|

市場調查報告書

商品編碼

2035082

資料脫敏:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Data Masking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

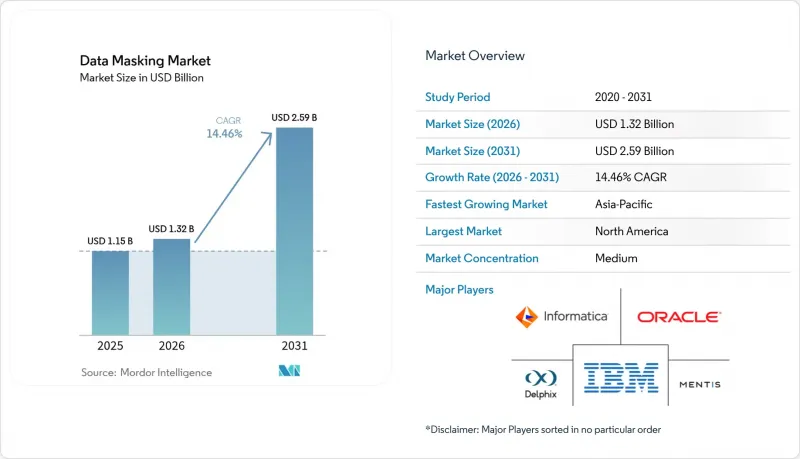

2025 年資料遮罩市場價值為 11.5 億美元,預計到 2031 年將達到 25.9 億美元,而 2026 年為 13.2 億美元,預測期(2026-2031 年)複合年成長率為 14.46%。

嚴格的監管、加速的雲端遷移以及勒索軟體攻擊的激增,正迫使企業從專案的匿名化方案轉向標準化的資料脫敏程序,以保護生產和非生產環境中的資料資產。供應商正在將人工智慧整合到其脫敏引擎中,以加速敏感欄位的發現;而DevOps團隊則將格式保留的脫敏副本作為持續測試的預設選項。隨著成熟企業收購專業領域專家以填補合成資料、敏感運算和非結構化資料保護的產品空白,產業整合勢必發生。儘管預計市場將保持強勁成長,但實施的複雜性、許可成本以及對數據效用的擔憂,在短期內仍是阻礙其採用的因素,尤其對於中小企業而言。

全球數據掩碼市場趨勢及洞察

加強資料隱私法規將推動合規投資。

隨著隱私權法的不斷擴展,尤其是在GDPR的推動下,以及數十億歐元的罰款威懾下,資料遮罩已成為企業風險管理挑戰的核心。目前,美國已有13個州實施了反映GDPR義務的產業通用隱私法,跨國公司也正從手動資料擦除轉向集中式資料遮罩平台。 ISO/IEC 29100:2024將資料遮罩列為官方認可的隱私增強技術之一,為首席資訊安全(CISO)的預算核准提供了基於標準的依據。跨境營運的銀行、零售商和醫療保健系統越來越需要調整政策,以在遵守司法管轄區居住規則的同時,強制執行統一的控制結構。供應商正透過提供模板來應對這項挑戰,這些模板規範了特定區域的資料擦除標準,從而加快了部署並降低了審計成本。

雲端優先的 DevOps 加速了測試資料管理的需求。

DevOps 團隊每天都要部署程式碼,他們需要與生產環境外觀和行為完全一致的高保真測試數據,同時也要避免洩露敏感資訊。與僅使用不切實際的合成資料相比,脫敏資料集可將發布週期縮短 73%,因此脫敏對於持續整合管道至關重要。容器化交付模型允許團隊為每個功能分支啟動脫敏副本,而格式保留的標記化則可確保複雜微服務之間的引用完整性。 Oracle Data Safe 和 IBM InfoSphere Optim 現在提供減敏 API,開發人員可以直接從 Terraform 腳本呼叫這些 API,從而簡化基礎架構即程式碼的自動化。隨著多重雲端採用率達到 76%,平台無關的脫敏仲介可確保在 AWS、Azure 和 Google Cloud 之間採用一致的策略。

實施的複雜性是企業採用此方案的一大挑戰。

由於大型主機、ERP 套件和雲端資料倉儲各自需要不同的連接器,據報道,在企業範圍內部署資料脫敏需要 18 個月的時間。維護數千個表的引用完整性需要重構儲存過程,這可能會增加數月的品質保證週期。如果令牌化儲存庫成為單點故障,架構師必須設計雙活集群,導致資本支出增加。有些公司為了簡化部署,即使犧牲即時回應能力,也選擇使用靜態簡介而不是動態資料脫敏。

細分市場分析

靜態方法憑藉關聯資料庫中可預測的吞吐量和極低的查詢開銷,在2025年佔了57.65%的收入佔有率。金融機構正優先考慮確定性令牌化,它能在嚴格的金鑰管理下確保帳號可恢復,從而允許將脫敏資料直接輸入匹配引擎而無需更改模式。動態工具以14.92%的複合年成長率成長,透過攔截查詢並動態重寫結果集來保護生產分析工作負載。早期採用者包括實施即時個人化服務的線上零售商,這類服務需要在毫秒時間內完成處理。動態解決方案的資料脫敏市場規模預計在2025年達到4.9億美元,並預計在2031年超過11.2億美元,這主要得益於Customer 360和開放銀行API的推動。格式保留加密彌合了兩者之間的差距,為架構師提供了一條遷移路徑,既能實現即時合規,又能分階段過渡到內聯脫敏閘道器。 Thales Vormetric 的「Vaultless Tokenization」(將於 2024 年年中發布)是這種混合模式的典型例子。

從 2026 年到 2031 年,靜態資料脫敏仍將是品質保證、培訓和離岸支援資料庫的預設選擇。然而,隨著企業向事件流架構轉型,能夠脫敏 Kafka 主題和 GraphQL 響應的動態資料脫敏將佔據更多市場佔有率。供應商將策略即代碼範本打包,並利用機器學習自動對欄位進行分類,這將降低技術門檻,並加速動態資料脫敏在受監管行業的應用。因此,資料脫敏市場將出現混合部署模式,即在同一企業內同時部署靜態和動態資料脫敏,並針對不同的延遲和成本需求進行最佳化。

即使到了2025年,仍有55.05%的脫敏資料在本地環境中處理,這主要是出於資料主權要求和現有資料中心投資的考量。然而,雲端採用率的複合年成長率(CAGR)高達15.18%,顯示市場佔有率正在迅速轉移,尤其是在那些希望擺脫傳統架構的數位化中小企業中。預計到2025年,雲端解決方案的資料脫敏市場規模將達到5.2億美元,並隨著多重雲端分析專案的推進而不斷擴大。諸如Intel SGX等敏感運算能力使脫敏引擎能夠在運算過程中保護金鑰,從而降低提供者的存取擔憂。 K2View的架構以Kubernetes Operator的形式部署,無需重新編碼即可在Redshift、Snowflake和BigQuery上統一應用規則。

到 2031 年,大多數大型企業將採用集中式策略引擎,並將執行決策權下放給本地和雲端工作人員。這種聯合模式將降低資料傳輸成本,並確保符合資料居住法規。計劃於 2025 年底發布的 ISO/IEC 27701 標準將定義雲端隱私影響評估 (PIA) 的隱私控制措施,資料脫敏供應商已在著手將這些控制措施映射到草案條款中。因此,資料脫敏市場將更加重視那些能夠與所有主流超大規模資料中心業者雲端平台原生整合,並可共用雲端安全態勢管理工具和資料處理歷程元資料。

區域分析

預計到2025年,北美將佔全球收入的37.05%。這主要得益於雲端運算的早期應用、嚴格的州法律以及勒索軟體攻擊的高風險。企業主管的預算反映了巨額資料外洩罰款,因此資料遮罩已成為網路安全藍圖上的重中之重。總部位於該地區的跨國公司正在部署統一平台,以在全球各子公司中一致地執行相關政策,從而簡化跨境審計。

在《一般資料保護規範》(GDPR) 和《人工智慧法案》等新法規的支持下,歐洲正在效仿。監管機構願意處以巨額罰款,例如對 Meta 公司處以 12 億歐元的罰款,這凸顯了實施資料遮罩技術的顯著投資回報率。 「數位歐洲計畫」已撥款 1.42 億歐元用於支持中小企業採用隱私技術,從而縮小了大型企業與中小企業之間長期存在的差距。

預計到2031年,亞太地區的複合年成長率將達到15.44%,位居全球之首。新加坡等國正在修訂其隱私法,以符合經合組織框架;中國則在其《個人資訊保護法》下強制要求本地資料處理。這加速了配備本地脫敏節點的區域資料中心的建置。印度IT外包商預設採用數據脫敏技術,以保護離岸交付中心的客戶數據,從而推動了對國內供應商的支出。儘管南美、中東和非洲在絕對值上落後,但隨著數位身分、金融科技和智慧城市計畫的日益成熟,尚未開發的市場機會正在湧現。當地經銷商正在將資料脫敏技術整合到符合合規要求的承包工程中,以加速市場初期滲透。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 全球數據量的成長

- 加強資料隱私法規(GDPR、CCPA 等)

- 雲端優先的 DevOps 需要脫敏測試數據

- 勒索軟體和網路攻擊激增

- 引入合成資料以增強人工智慧訓練

- 新興市場的數據居住要求

- 市場限制因素

- 實施和與舊有系統整合的複雜性

- 動態工具的總擁有成本高

- 數據在高階分析的效用下降

- 跨境合成資料集監理方面的不確定性

- 產業價值鏈分析

- 技術展望

- 監理情勢

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

- 主要宏觀經濟趨勢對市場的影響

第5章 市場規模與成長預測

- 按類型

- 靜止的

- 動態的

- 按部署模式

- 雲

- 現場

- 按組織規模

- 大公司

- 中小企業

- 按最終用戶行業分類

- BFSI

- 資訊科技和通訊

- 衛生保健

- 零售與電子商務

- 工業與國防

- 能源與公共產業

- 製造業

- 其他行業

- 透過數據環境

- 結構化資料

- 半結構化資料和非結構化數據

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 新加坡

- 澳洲

- 亞太其他地區

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- IBM Corporation

- Oracle Corporation

- Informatica Inc.

- Delphix Corp.

- Mentis Inc.

- Innovative Routines International Inc.

- Solix Technologies Inc.

- K2View Ltd.

- Redgate Software Ltd.

- Broadcom Inc.(CA Technologies)

- Protegrity USA, Inc.

- TokenEx, LLC

- Ekobit doo

- Dataguise Inc.(PKWARE)

- Micro Focus International plc

- Informatica LLC

- Baffle, Inc.

- Very Good Security, Inc.

- Immuta, Inc.

- Spirion, LLC

- Camouflage Software Inc.

- ARCAD Software SA

- IRI Voracity(Innovative Routines International)

- Dataprotect SA

- TripleBlind, Inc.

第7章 市場機會與未來展望

The data masking market size was valued at USD 1.15 billion in 2025 and estimated to grow from USD 1.32 billion in 2026 to reach USD 2.59 billion by 2031, at a CAGR of 14.46% during the forecast period (2026-2031).

Strong legislation, accelerating cloud migration, and a surge in ransomware incidents are pushing organizations to replace ad-hoc anonymization with standardized masking programs that protect production and non-production data estates. Vendors are embedding AI in masking engines to speed discovery of sensitive fields, while DevOps teams treat masked, format-preserving copies as the default for continuous testing. Consolidation is likely as incumbents acquire niche specialists to fill product gaps in synthetic data, confidential computing, and unstructured data protection. Despite healthy growth, implementation complexity, licensing costs, and data-utility concerns remain short-term brakes on adoption, particularly for small and medium enterprises (SMEs).

Global Data Masking Market Trends and Insights

Rising Data-Privacy Regulations Drive Compliance Investment

Expanding privacy laws, led by GDPR and backed by multi-billion-euro fines, have pushed masking to the center of corporate risk agendas. Thirteen U.S. states now enforce sector-agnostic privacy statutes that mirror GDPR obligations, prompting multinationals to replace manual scrubbing with centrally governed masking platforms. ISO/IEC 29100:2024 lists masking among formally recognized privacy-enhancing technologies, giving chief information security officers (CISOs) a standards-based reference for budget approvals. Banks, retailers, and health systems with cross-border footprints increasingly demand policy orchestration that maps to jurisdiction-specific residency rules yet enforces a single control posture. Vendors respond with templates that codify region-specific redaction thresholds, accelerating rollouts and lowering audit costs.

Cloud-First DevOps Accelerates Test Data Management Needs

DevOps teams deploy code daily and require full-fidelity test data that looks and behaves like production without exposing secrets. Masked datasets shorten release cycles by 73% compared to less realistic synthetic-only alternatives, making masking integral to continuous integration pipelines. Containerized delivery models let teams spin up a masked copy per feature branch, while format-preserving tokenization keeps referential integrity for complex microservices. Oracle Data Safe and IBM InfoSphere Optim now ship masking APIs that developers call directly from Terraform scripts, which simplifies infrastructure-as-code automation. As multicloud adoption reaches 76%, platform-agnostic masking brokers ensure consistent policies across AWS, Azure, and Google Cloud.

Implementation Complexity Challenges Enterprise Adoption

Enterprises report 18-month timelines to roll out enterprise-wide masking because mainframes, ERP suites, and cloud data warehouses require different connectors. Maintaining referential integrity across thousands of tables can mean refactoring stored procedures, adding months of QA cycles. Where tokenization vaults become a single point of failure, architects must design active-active clusters, increasing capital expense. Some firms defer dynamic masking in favor of static snapshots, trading real-time coverage for simpler deployments.

Other drivers and restraints analyzed in the detailed report include:

- Synthetic Data Adoption Transforms AI Training Paradigms

- Surge in Ransomware Attacks Elevates Data Protection Priority

- High Total Cost of Ownership Constrains SME Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Static techniques delivered 57.65% of 2025 revenue, underpinned by predictable throughput and minimal query overhead in relational databases. Financial institutions value deterministic tokenization that keeps account numbers reversible under strict key control, allowing masked data to feed reconciliation engines without schema changes. Dynamic tools, growing at a 14.92% CAGR, shield production analytics workloads by intercepting queries and rewriting result sets on the fly. Early adopters include online retailers running real-time personalization where milliseconds matter. The data masking market size for dynamic solutions is estimated at USD 0.49 billion in 2025, projected to exceed USD 1.12 billion by 2031 on the back of customer-360 and open-banking APIs. Format-preserving encryption bridges both camps, giving architects a migration path that delivers immediate compliance while enabling a gradual move to in-line masking gateways. Thales Vormetric's vaultless tokenization, launched mid-2024, exemplifies the hybrid model.

Across 2026-2031, static masking will remain the default for QA, training, and offshore support databases. However, as organizations modernize to event-stream architectures, dynamic masking that can redact Kafka topics or GraphQL responses will capture incremental spend. Vendors that bundle policy-as-code templates and auto-classify fields using machine learning lower the skills barrier, accelerating dynamic adoption in regulated verticals. As a result, the data masking market will likely see a blending of static-plus-dynamic deployments within single enterprises, each optimized for distinct latency and cost envelopes.

On-premise environments still processed 55.05% of masked data in 2025, driven by sovereignty mandates and sunk investments in data centers. Yet a 15.18% CAGR in cloud deployments points to rapid share transfer, especially among digitized SMEs that bypass legacy stacks. The data masking market size for cloud solutions reached USD 0.52 billion in 2025 and will climb in line with multicloud analytics programs. Confidential-computing features such as Intel SGX allow masking engines to protect keys during computation, mitigating fears around provider access. K2View's fabric deploys as Kubernetes operators, applying rules uniformly across Redshift, Snowflake, and BigQuery without re-coding.

By 2031, most large enterprises will run policy engines centrally and push enforcement decisions to both local and cloud workers. This federated pattern reduces egress charges and complies with residency laws. ISO/IEC 27701, scheduled for late-2025 release, will codify privacy controls for cloud PIAs, and masking vendors are already mapping controls to draft clauses. Consequently, the data masking market will reward platforms with native connectors to all major hyperscalers and the ability to share lineage metadata with cloud security posture management tools.

The Data Masking Market Report is Segmented by Type (Static and Dynamic), Deployment Model (Cloud and On-Premise), Organization Size (Large Enterprises and Small and Medium Enterprises), End-User Industry (BFSI, IT and Telecom, Healthcare, and More), Data Environment (Structured Data and Semi-Structured and Unstructured Data), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 37.05% of revenue in 2025, anchored by early cloud adoption, stringent state laws, and high ransomware exposure. C-suite budgets reflect sizable breach fines, pushing masking to the top of cybersecurity roadmaps. Multinationals headquartered in the region deploy unified platforms that apply policies consistently to subsidiaries worldwide, simplifying cross-border audits.

Europe follows with entrenched GDPR enforcement and emerging statutes such as the AI Act. Regulators' appetite for blockbuster fines, demonstrated by the EUR 1.2 billion Meta penalty, creates a clear ROI case for masking deployment. Funding from the Digital Europe Programme channels EUR 142 million toward SME privacy tech adoption, shrinking the historical gap between large enterprises and smaller firms.

Asia-Pacific posts the fastest 15.44% CAGR through 2031. Nations, including Singapore, update privacy laws to align with OECD frameworks, and China mandates data-local processing under PIPL, prompting regional data-center build-outs with local masking nodes. Indian IT outsourcers adopt masking by default to protect client data inside offshore delivery centers, boosting domestic vendor spend. South America, the Middle East, and Africa lag in absolute dollars but present green-field opportunities as digital ID, fintech, and smart-city initiatives mature. Local resellers bundle masking into turnkey compliance packages, accelerating initial penetration.

- IBM Corporation

- Oracle Corporation

- Informatica Inc.

- Delphix Corp.

- Mentis Inc.

- Innovative Routines International Inc.

- Solix Technologies Inc.

- K2View Ltd.

- Redgate Software Ltd.

- Broadcom Inc. (CA Technologies)

- Protegrity USA, Inc.

- TokenEx, LLC

- Ekobit d.o.o.

- Dataguise Inc. (PKWARE)

- Micro Focus International plc

- Informatica LLC

- Baffle, Inc.

- Very Good Security, Inc.

- Immuta, Inc.

- Spirion, LLC

- Camouflage Software Inc.

- ARCAD Software SA

- IRI Voracity (Innovative Routines International)

- Dataprotect S.A.

- TripleBlind, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase in global data volume

- 4.2.2 Rising data-privacy regulations (GDPR, CCPA, etc.)

- 4.2.3 Cloud-first DevOps requiring masked test data

- 4.2.4 Surge in ransomware and cyber-attacks

- 4.2.5 Synthetic-data adoption to augment AI training

- 4.2.6 Data residency mandates in emerging economies

- 4.3 Market Restraints

- 4.3.1 Implementation complexity and legacy integration

- 4.3.2 High total cost of ownership for dynamic tools

- 4.3.3 Reduced data utility for advanced analytics

- 4.3.4 Regulatory uncertainty on cross-border synthetic datasets

- 4.4 Industry Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Key Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Type

- 5.1.1 Static

- 5.1.2 Dynamic

- 5.2 By Deployment Model

- 5.2.1 Cloud

- 5.2.2 On-premise

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-User Industry

- 5.4.1 BFSI

- 5.4.2 IT and Telecom

- 5.4.3 Healthcare

- 5.4.4 Retail and E-commerce

- 5.4.5 Industrial and Defense

- 5.4.6 Energy and Utilities

- 5.4.7 Manufacturing

- 5.4.8 Other Industry Verticals

- 5.5 By Data Environment

- 5.5.1 Structured Data

- 5.5.2 Semi-structured and Unstructured Data

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Malaysia

- 5.6.4.6 Singapore

- 5.6.4.7 Australia

- 5.6.4.8 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Oracle Corporation

- 6.4.3 Informatica Inc.

- 6.4.4 Delphix Corp.

- 6.4.5 Mentis Inc.

- 6.4.6 Innovative Routines International Inc.

- 6.4.7 Solix Technologies Inc.

- 6.4.8 K2View Ltd.

- 6.4.9 Redgate Software Ltd.

- 6.4.10 Broadcom Inc. (CA Technologies)

- 6.4.11 Protegrity USA, Inc.

- 6.4.12 TokenEx, LLC

- 6.4.13 Ekobit d.o.o.

- 6.4.14 Dataguise Inc. (PKWARE)

- 6.4.15 Micro Focus International plc

- 6.4.16 Informatica LLC

- 6.4.17 Baffle, Inc.

- 6.4.18 Very Good Security, Inc.

- 6.4.19 Immuta, Inc.

- 6.4.20 Spirion, LLC

- 6.4.21 Camouflage Software Inc.

- 6.4.22 ARCAD Software SA

- 6.4.23 IRI Voracity (Innovative Routines International)

- 6.4.24 Dataprotect S.A.

- 6.4.25 TripleBlind, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

資料脫敏市場:2026-2032年全球市場預測(依脫敏類型、部署方式、組織規模、產業和應用分類)

資料脫敏市場:2026-2032年全球市場預測(依脫敏類型、部署方式、組織規模、產業和應用分類) 資料脫敏市場規模、佔有率和成長分析:按交付類型、部署模型、脫敏方法、企業規模、產業、資料類型和地區分類-2026-2033年產業預測

資料脫敏市場規模、佔有率和成長分析:按交付類型、部署模型、脫敏方法、企業規模、產業、資料類型和地區分類-2026-2033年產業預測 2026年全球數據標記化市場報告2026年全球資料脫敏市場報告

2026年全球數據標記化市場報告2026年全球資料脫敏市場報告 全球資料減敏市場:市場規模、佔有率和趨勢分析(按類型、解決方案、部署方法、最終用途和地區分類),細分市場預測(2026-2033 年)

全球資料減敏市場:市場規模、佔有率和趨勢分析(按類型、解決方案、部署方法、最終用途和地區分類),細分市場預測(2026-2033 年) 全球數據脫敏市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球數據脫敏市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 資料減敏市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、部署方式、最終用戶產業、地區和競爭格局分類,2021-2031 年資料減敏市場-2025年至2030年預測全球資料遮罩市場按部署類型、組件、垂直行業、區域範圍和預測

資料減敏市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、部署方式、最終用戶產業、地區和競爭格局分類,2021-2031 年資料減敏市場-2025年至2030年預測全球資料遮罩市場按部署類型、組件、垂直行業、區域範圍和預測