|

市場調查報告書

商品編碼

2035032

傳統系統現代化:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Legacy Modernization - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

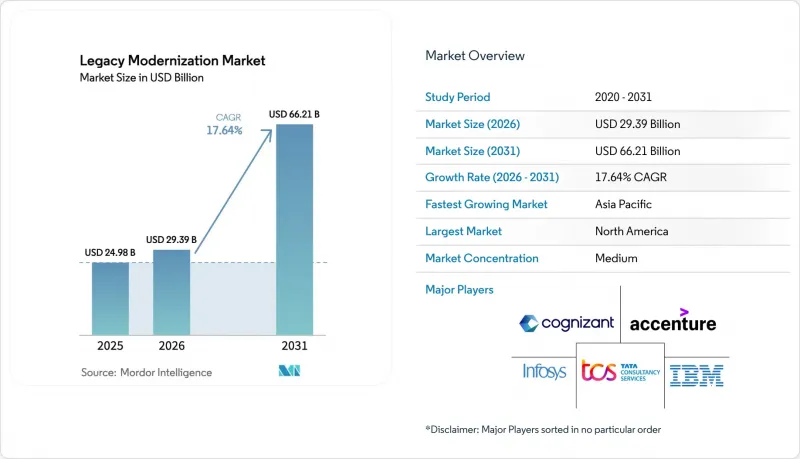

預計到 2026 年,傳統系統現代化市場規模將達到 293.9 億美元,高於 2025 年的 249.8 億美元,預計到 2031 年將達到 662.1 億美元。

預計 2026 年至 2031 年的複合年成長率為 17.64%。

這種快速成長凸顯了解決日益成長的技術債的迫切性,同時也需要實現雲端原生敏捷性和人工智慧驅動的效率。監管要求對容錯和即時數位報告提出了更高的要求,這促使各組織採取行動;而競爭壓力則使那些從被動維護轉向主動重建的公司獲得了優勢。雲端採用的普及、GenAI驅動的程式碼轉換的快速發展以及持續流入重建方法的資金,正在重新調整各主要產業的投資重點。隨著現代化進程的加速,服務主導的方法仍然至關重要,因為企業需要專業知識來降低複雜轉型時期的業務風險。系統整合商與超大規模雲端供應商之間的夥伴關係,透過將深厚的產業知識與可擴展的平台能力相結合,進一步推動了這一趨勢。

全球傳統系統現代化市場趨勢與洞察

透過雲端原生技術實現敏捷性的需求

企業正逐步摒棄單體架構,因為此類系統無法提供面向客戶的數位化產品如今所需的彈性擴展、微服務架構或API互通性。微軟與可口可樂達成的11億美元多重雲端協議便是全球品牌積極投資現代化改造以支援持續配置管道和全球覆蓋的絕佳例證。透過採用容器編排管理和無伺服器執行,企業將發布週期從數月縮短至數天,從而實現近乎即時的個人化和資料驅動的決策。隨著數位新興企業憑藉更快的產品迭代速度蠶食老牌企業的市場地位,這一趨勢正在加速發展。因此,傳統系統現代化改造市場仍傾向徹底的架構重建,而非漸進式的遷移方案。

COBOL 和大型主機資產的技術債不斷增加

對許多大型銀行和保險公司而言,老舊COBOL環境的年度維護成本如今已超過其現代化改造的投資。日本的「2025問題」凸顯了這一趨勢,該問題警告稱,資深開發人員的退休會帶來系統性風險。富士通與豐田的合作專案利用GenAI將系統更新週期縮短了50%,這表明替換存在漏洞的程式碼庫遠比維護它更具成本效益。由於組件和技能的短缺,每拖延一年,營運風險和成本曲線都會加劇。因此,董事會越來越重視現代化改造,不僅將其視為一項IT項目,更將其視為提升系統韌性的核心優先事項,這推動了舊有系統現代化改造市場的長期需求。

遷移的初始成本和業務風險

現代化改造預算通常包括新建基礎設施、工具、整合、員工再培訓以及詳細的變更管理方案。 Legal & General 正在與 Kyndryl 合作制定一項為期七年的資料中心剝離計劃,這凸顯了即使綠色能源效益能夠抵消營運成本,資本支出仍然必不可少。在過渡期間,諸如薪資核算或交易等關鍵業務應用程式的故障可能會導致經濟處罰和品牌價值下降。因此,傳統系統現代化改造市場需要不斷完善風險緩解框架、分階段部署計畫和基於結果的合約條款,以消除董事會的疑慮。

細分市場分析

到2025年,服務業將佔據傳統系統現代化市場58.05%的佔有率,這一主導地位源自於多年轉型專案的客製化特性。諮詢藍圖制定、投資報酬率建模、系統整合和託管轉型協同運作,以降低涉及財務帳簿、病患記錄或國家稅務系統等轉型過程中存在的風險。雖然自動化工具能夠提高生產力,但企業仍需要領域專家來協調分階段的轉型,以確保業務永續營運。

軟體產業雖然規模仍較小,但正以16.09%的複合年成長率快速成長。人工智慧驅動的程式碼分析器、相依性偵測工具和自動化管線產生工具現已整合到平台即服務 (PaaS) 套件中。訂閱模式消除了高昂的授權費用,並支援局部部署,這有望擴大軟體產業傳統系統現代化改造市場。這一趨勢正在加強系統整合商 (SI) 和獨立軟體供應商 (ISV) 之間的合作,雙方共同提供打包交付成果。

至2025年,雲端模式將佔據傳統系統現代化市場67.10%的佔有率。企業傾向於選擇公共雲端或多重雲端環境,因為它們能夠提供可擴展性、全球覆蓋範圍和資安管理服務,而無需承擔資本支出(CAPEX)。儘管由於敏感工作負載的區域性需求,混合雲模式正在興起,但即使在這些架構中,遙測資料也會被輸入到公共雲端分析引擎中,以提取資料洞察。

與純公共雲端採用相關的傳統系統現代化市場正以 17.98% 的複合年成長率 (CAGR) 成長。這主要得益於超大規模區域的不斷擴展以及互聯協議的達成,例如微軟和Oracle的「Azure 資料庫」擴展計劃,該計劃目前已覆蓋 15 個全球可用區。金融、遊戲和醫療保健服務提供者正在利用突發容量來應對季節性工作負載,同時透過主權區域和機密運算飛地確保合規性。

《傳統系統現代化市場報告》按組件(軟體和服務)、部署類型(本地部署和雲端部署)、現代化方法(重新託管、重新平台化、重新架構、重構和替換/COTS)、最終用戶行業(銀行、金融服務和保險、製造業、醫療保健、IT和電信等)、組織規模(大型企業和中小企業)以及金融服務和保險、製造業、醫療保健、IT和電信等)、組織規模(大型企業和中小企業)以及地區進行細分。

區域分析

預計到2025年,北美將佔據37.05%的銷售佔有率,佔據主導地位。這反映了該地區大型主機基礎設施的強大實力、雲端運算的早期應用以及聯邦政府對容錯架構的嚴格監管。美國證券交易委員會(SEC)等監管機構現在要求向資本市場提供近乎即時的報告,這推動了雲端原生資料倉儲和分析技術的發展。因此,全部區域傳統系統現代化市場持續保持較高的平均合約價值和長期託管服務續約合約。亞太地區正以15.71%的複合年成長率成長,這主要得益於日本即將面臨的技能短缺、印度的國家數位公共平台計畫以及東南亞金融科技的快速普及。 NTT Data斥資15億美元擴建資料中心以及富士通與豐田合作開展的基於GenAI的研發項目,都展現了本土創新如何與全球最佳實踐相融合。圍繞智慧製造和數位貿易走廊的政府經濟獎勵策略,正進一步為傳統現代化市場注入資金。在歐洲,隨著《一般資料保護規範》(GDPR)、《數位市場法案》和永續發展指令的整合,市場持續保持強勁成長動能。歐盟的《能源效率指令》要求資料中心記錄電力使用效率和碳排放,如果沒有現代遙測系統,這項挑戰將難以實現。德國、法國和西班牙的主權雲框架正推動許多現代化藍圖轉向混合設計,以大規模利用公共雲端的分析能力,同時將敏感資料保留在區域內。中東和非洲地區雖然規模仍然較小,但由於各國優先發展數位政府和無現金交易的多元化政策,該地區正在快速成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對雲端原生敏捷性的需求

- COBOL 和大型主機環境中的技術債增加

- 促進數位化報告和監管以增強韌性

- 利用 GenAI 的程式碼轉換工具數量迅速成長

- 資料中心的碳排放減少義務

- 併購主導的系統整合截止日期

- 市場限制因素

- 初始遷移成本與業務風險

- 傳統語言專家短缺

- 主權雲端和資料居住要求

- 小眾獨立軟體供應商工作負載的許可鎖定

- 重要法規結構的評估

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

- 對關鍵相關人員的影響評估

- 主要用例和案例研究

- 宏觀經濟因素對市場的影響

- 投資分析

第5章 市場區隔

- 按組件

- 軟體

- 服務

- 依部署類型

- 現場

- 雲

- 現代化方法

- 重新託管

- 平台遷移

- 重建

- 重構

- 替代/市售現成產品 (COTS)

- 按最終用戶行業分類

- BFSI

- 製造業

- 衛生保健

- 資訊科技/通訊

- 零售與電子商務

- 政府和公共部門

- 其他

- 按組織規模

- 大公司

- 中小企業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 其他歐洲地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 奈及利亞

- 其他非洲地區

- 中東

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 澳洲

- 紐西蘭

- 亞太其他地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- International Business Machines Corporation(IBM)

- Accenture plc

- Cognizant Technology Solutions Corporation

- Infosys Limited

- Tata Consultancy Services Limited

- Atos SE(Eviden SAS)

- Capgemini SE

- HCL Technologies Limited

- Wipro Limited

- DXC Technology Company

- Microsoft Corporation

- Amazon Web Services, Inc.

- Google LLC(Google Cloud)

- Oracle Corporation

- NTT DATA Corporation

- CGI Inc.

- Kyndryl Holdings, Inc.

- Tech Mahindra Limited

- Hexaware Technologies Limited

- OpenText Corporation(incl. Micro Focus)

第7章 市場機會與未來展望

Legacy modernization market size in 2026 is estimated at USD 29.39 billion, growing from 2025 value of USD 24.98 billion with 2031 projections showing USD 66.21 billion, growing at 17.64% CAGR over 2026-2031.

The sharp rise underscores the urgency to resolve mounting technical debt while unlocking cloud-native agility and artificial-intelligence-driven efficiencies. Regulatory mandates that demand resilient, real-time digital reporting push organizations to act, while competitive pressures reward firms that shift from reactive maintenance to proactive re-architecting. The dominance of cloud deployment, rapid progress in GenAI-assisted code conversion, and the steady inflow of capital toward re-architecting approaches together reshape investment priorities across every major vertical. As modernization accelerates, services-led engagements remain pivotal because enterprises require domain expertise that mitigates business-risk exposure during complex cut-over windows. Partnerships between systems integrators and hyperscale cloud providers further reinforce the momentum by coupling deep industry knowledge with scalable platform capabilities.

Global Legacy Modernization Market Trends and Insights

Cloud-Native Agility Imperative

Enterprises are steadily abandoning monolithic architectures because such systems cannot deliver the elastic scaling, microservices orientation, or API-first interoperability that customer-facing digital products now demand. A USD 1.1 billion multi-cloud agreement between Microsoft and Coca-Cola exemplifies how global brands fund aggressive modernization to support continuous deployment pipelines and worldwide reach. By adopting container orchestration and serverless execution, firms reduce release cycles from months to days, enabling near real-time personalization and data-driven decision-making. The trajectory intensifies as digital challengers erode incumbent market positions with faster product iteration. Consequently, the Legacy modernization market observes sustained preference for full re-architecting over incremental lift-and-shift movements.

Rising Technical Debt of COBOL and Mainframe Estates

Annual maintenance spending on aging COBOL estates now eclipses modernization investment in many large banks and insurers, a pattern vividly highlighted by Japan's "2025 cliff" that flags systemic risk as veteran developers retire. Fujitsu's work with Toyota, which cut system update time by 50% through GenAI-enabled transformation, proves that replacing brittle code bases is far cheaper than perpetuating them. With components and skills both scarce, each year of deferred action compounds operational risk and cost curves. As a result, boards increasingly treat modernization as a core resilience priority rather than an IT project, thereby boosting long-term demand for the Legacy modernization market.

Up-Front Migration Cost and Business Risk

Modernization budgets typically cover new infrastructure, tooling, integration, workforce reskilling, and detailed change-management programs. Legal and General committed to a seven-year data-center exit with Kyndryl, underlining capital outlays required even when green energy gains offset operational expense. Any disruption to mission-critical payroll, claims, or trading applications during cut-over can translate into financial penalties or brand erosion. Consequently, the Legacy modernization market must continually package risk-mitigation frameworks, phased deployment blueprints, and outcome-based commercial terms to reassure hesitant boards.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push for Digital Reporting and Resiliency

- Surge in GenAI-Assisted Code Conversion Tools

- Scarcity of Legacy-Language Specialists

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services controlled 58.05% of the Legacy modernization market in 2025, a lead rooted in the bespoke nature of multi-year transformation programs. Advisory road-mapping, ROI modeling, system integration, and managed transformation all converge to de-risk migrations that touch financial ledgers, patient records, or national tax systems. Automated tooling boosts productivity, yet enterprises still rely on domain specialists to orchestrate phased cutovers that safeguard business continuity.

Software, while smaller, is accelerating at a 16.09% CAGR. AI-augmented code analyzers, dependency discoverers, and automated pipeline generators are now embedded in platform-as-a-service suites. The Legacy modernization market size for software is predicted to broaden as subscription models eliminate large license fees and allow piecemeal adoption. The dynamic fosters tighter bonds between SI partners and ISVs who jointly offer packaged outcomes.

Cloud models captured 67.10% Legacy modernization market share in 2025. Enterprises favor public or multi-cloud footprints that deliver elasticity, global reach, and managed security services without capex overhead. Regional requirements for sensitive workloads produce hybrid patterns, but even these architectures pipe telemetry into public-cloud analytics engines to unlock data insights.

The Legacy modernization market size associated with pure public-cloud deployments is expanding at an 17.98% CAGR, helped by ever-growing hyperscale regions and interconnect agreements such as the Microsoft-Oracle "database-on-Azure" expansion that now spans 15 global zones. Financial, gaming, and healthcare providers leverage burst capacity for seasonal workloads while ensuring regulatory compliance via sovereign regions or confidential computing enclaves.

The Legacy Modernization Market Report is Segmented by Component (Software and Services), Deployment Type (On-Premises, and Cloud), Modernization Approach (Re-Hosting, Re-Platforming, Re-Architecting, Re-Factoring, and Replacement / COTS), End-User Industry (BFSI, Manufacturing, Healthcare, IT and Telecommunications, and More), Organization Size (Large Enterprises, and Small and Medium Enterprises (SMEs)), and Geography.

Geography Analysis

North America held a commanding 37.05% revenue share in 2025, reflecting an installed base of mainframes, early cloud adoption, and strict federal oversight that rewards resilient architecture. US regulators such as the Securities and Exchange Commission now impose near real-time reporting for capital markets, forcing cloud-native data warehousing and analytics to the foreground. As a result, the Legacy modernization market continues to enjoy high average contract values and long-term managed-services renewals across the region. Asia-Pacific is advancing at 15.71% CAGR, propelled by Japan's looming skills cliff, India's national digital-public-platform initiatives, and Southeast Asia's greenfield FinTech adoption. NTT DATA's USD 1.5 billion data-center expansion and Fujitsu's GenAI-assisted Toyota engagement illustrate home-grown innovation meeting global best practice. Government stimulus around smart manufacturing and digital trade corridors further injects capital into the Legacy modernization market. Europe maintains strong momentum as GDPR, the Digital Markets Act, and sustainability directives overlap. The EU Energy Efficiency Directive obliges datacenters to document power usage effectiveness and carbon emissions, a task achievable only with modern telemetry systems. Sovereign-cloud frameworks in Germany, France, and Spain steer many modernization roadmaps toward hybrid designs that keep sensitive data in-region while exploiting public-cloud analytics at scale. The Middle East and Africa, though smaller today, are accelerating thanks to national diversification agendas that prioritize digital government and cashless commerce.

- International Business Machines Corporation (IBM)

- Accenture plc

- Cognizant Technology Solutions Corporation

- Infosys Limited

- Tata Consultancy Services Limited

- Atos SE (Eviden SAS)

- Capgemini SE

- HCL Technologies Limited

- Wipro Limited

- DXC Technology Company

- Microsoft Corporation

- Amazon Web Services, Inc.

- Google LLC (Google Cloud)

- Oracle Corporation

- NTT DATA Corporation

- CGI Inc.

- Kyndryl Holdings, Inc.

- Tech Mahindra Limited

- Hexaware Technologies Limited

- OpenText Corporation (incl. Micro Focus)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-native agility imperative

- 4.2.2 Rising technical debt of COBOL and mainframe estates

- 4.2.3 Regulatory push for digital reporting and resiliency

- 4.2.4 Surge in GenAI-assisted code conversion tools

- 4.2.5 Carbon-reduction mandates on datacenters

- 4.2.6 Mand A-driven system harmonisation deadlines

- 4.3 Market Restraints

- 4.3.1 Up-front migration cost and business risk

- 4.3.2 Scarcity of legacy-language specialists

- 4.3.3 Sovereign-cloud and data-residency restrictions

- 4.3.4 Licence-lock-in of niche ISV workloads

- 4.4 Evaluation of Critical Regulatory Framework

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Impact Assessment of Key Stakeholders

- 4.8 Key Use Cases and Case Studies

- 4.9 Impact on Macroeconomic Factors of the Market

- 4.10 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Type

- 5.2.1 On-premises

- 5.2.2 Cloud

- 5.3 By Modernization Approach

- 5.3.1 Re-hosting

- 5.3.2 Re-platforming

- 5.3.3 Re-architecting

- 5.3.4 Re-factoring

- 5.3.5 Replacement / COTS

- 5.4 By End-User Industry

- 5.4.1 BFSI

- 5.4.2 Manufacturing

- 5.4.3 Healthcare

- 5.4.4 IT and Telecommunications

- 5.4.5 Retail and E-commerce

- 5.4.6 Government and Public Sector

- 5.4.7 Others

- 5.5 By Organization Size

- 5.5.1 Large Enterprises

- 5.5.2 Small and Medium Enterprises (SMEs)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Nordics

- 5.6.3.7 Rest of Europe

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 Saudi Arabia

- 5.6.4.1.2 United Arab Emirates

- 5.6.4.1.3 Turkey

- 5.6.4.1.4 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Egypt

- 5.6.4.2.3 Nigeria

- 5.6.4.2.4 Rest of Africa

- 5.6.4.1 Middle East

- 5.6.5 Asia-Pacific

- 5.6.5.1 China

- 5.6.5.2 India

- 5.6.5.3 Japan

- 5.6.5.4 South Korea

- 5.6.5.5 ASEAN

- 5.6.5.6 Australia

- 5.6.5.7 New Zealand

- 5.6.5.8 Rest of Asia-Pacific

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 International Business Machines Corporation (IBM)

- 6.4.2 Accenture plc

- 6.4.3 Cognizant Technology Solutions Corporation

- 6.4.4 Infosys Limited

- 6.4.5 Tata Consultancy Services Limited

- 6.4.6 Atos SE (Eviden SAS)

- 6.4.7 Capgemini SE

- 6.4.8 HCL Technologies Limited

- 6.4.9 Wipro Limited

- 6.4.10 DXC Technology Company

- 6.4.11 Microsoft Corporation

- 6.4.12 Amazon Web Services, Inc.

- 6.4.13 Google LLC (Google Cloud)

- 6.4.14 Oracle Corporation

- 6.4.15 NTT DATA Corporation

- 6.4.16 CGI Inc.

- 6.4.17 Kyndryl Holdings, Inc.

- 6.4.18 Tech Mahindra Limited

- 6.4.19 Hexaware Technologies Limited

- 6.4.20 OpenText Corporation (incl. Micro Focus)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

2026年全球應用開發與管理軟體市場報告

2026年全球應用開發與管理軟體市場報告 核心銀行系統轉型市場預測—全球轉型策略、轉型方法、技術基礎設施、服務和最終用戶分析—2034年2026年全球傳統系統現代化市場報告2026年全球客製化應用開發服務市場報告

核心銀行系統轉型市場預測—全球轉型策略、轉型方法、技術基礎設施、服務和最終用戶分析—2034年2026年全球傳統系統現代化市場報告2026年全球客製化應用開發服務市場報告 應用開發服務市場:按組件、技術、產業和組織規模分類-2026-2032年全球市場預測

應用開發服務市場:按組件、技術、產業和組織規模分類-2026-2032年全球市場預測 包覆成型服務市場規模、佔有率和成長分析:依製程技術、成型方法、材料組合、最終用途和地區分類-2026年至2033年產業預測2026年全球軟體開發服務市場報告2026年全球傳統軟體現代化市場報告2026年全球網際網路軟體開發服務市場報告

包覆成型服務市場規模、佔有率和成長分析:依製程技術、成型方法、材料組合、最終用途和地區分類-2026年至2033年產業預測2026年全球軟體開發服務市場報告2026年全球傳統軟體現代化市場報告2026年全球網際網路軟體開發服務市場報告 2025-2029年全球應用開發與整合市場

2025-2029年全球應用開發與整合市場