|

市場調查報告書

商品編碼

2035016

線上語言學習:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Online Language Learning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

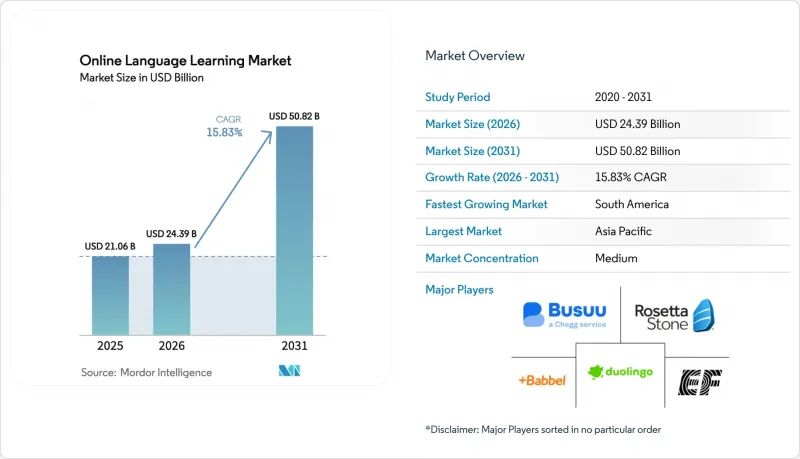

2025 年線上語言學習市場價值 210.6 億美元,預計到 2031 年將達到 508.2 億美元,而 2026 年為 243.9 億美元,預測期(2026-2031 年)複合年成長率為 15.83%。

由於跨境貿易的擴張、人口結構的變化以及行動裝置的快速普及,市場需求依然旺盛,而人工智慧驅動的個人化和身臨其境型技術則提升了學習效率。每個平台都提供豐富的課程目錄和自適應學習路徑,從而提高學習者的留存率,這在競爭日益激烈的市場中是關鍵的差異化優勢。企業正在加快投資,提升員工的語言技能,以實現環境、社會和治理(ESG)以及多元化、公平和包容(DEI)目標,而公共部門對多語言項目的預算增加也進一步擴大了學習者群體。另一方面,歐洲嚴格的資料隱私法規以及飽和的免費增值管道中不斷上漲的用戶獲取成本正在抑製成長,迫使平台公司最佳化其商業化戰略並實現收入來源多元化。

全球線上語言學習市場趨勢及洞察

全球化推動了跨境通訊的需求。

隨著國際貿易的活性化,語言技能已成為競爭力的核心要素。科技、旅遊、金融等行業的公司都在投資擴充性的線上語言課程,以克服溝通障礙。像Open English這樣的機構透過將英語能力定位為經濟流動性的手段,擴大了其在拉丁美洲的業務範圍。區域貿易集團也在增加對葡萄牙語和西班牙語的需求,這凸顯了英語以外的多元化成長趨勢。

利用人工智慧的自適應學習的普及

目前,人工智慧 (AI) 引擎正在即時調整內容順序、難度和回饋,以提高完成率和提升銷售潛力。多鄰國 (Duolingo) 正在整合生成式人工智慧,以實現複習循環和發音練習的個人化,這項投資在其 2024 年提交給美國證券交易委員會 (SEC) 的文件中有所詳述。創業融資也反映了這一趨勢。 Speak 的估值超過 10 億美元,此前該公司證明其對話式人工智慧能夠支援 10 億個音訊句子,並能推動高級會員計畫的普及。該平台將人工智慧與「隱私設計」原則相結合,在歐洲嚴格的數據法規下建立了永續的差異化優勢。

資料安全和隱私問題

GDPR法規禁止無限制地將語音資料傳輸給第三方人工智慧處理商,迫使平台建構自身成本高昂的語音辨識流程。新的在地化要求進一步增加了營運成本,擠壓了小規模參與企業的利潤空間,並將市場推向擁有內部合規團隊的大規模企業。

細分市場分析

預計到2025年,自學應用程式將佔線上語言學習市場收入的56.35%,成為該市場最大的交付管道。其主導地位得益於全天候的訪問性、微課設計以及降低每位學習者成本的演算法個人化。然而,教師主導的即時課程正以21.25%的複合年成長率快速成長,反映出人們對即時對話日益成長的需求,而演算法目前只能部分複製這種對話。將錄播模組與每週教師課程結合的混合模式正在成為提高用戶留存率的最佳解決方案,有助於平台維持訂閱價格。 Preply的市場平台展示了這種混合模式的經濟效益,隨著課程預訂量的增加,訂閱升級也隨之增加。隨著自動化排課和按分鐘收費系統的不斷創新,預計將有更多獨立教師加入此聚合平台,擴大課程供應並降低課程費用,這將進一步惠及學習者。

新興市場寬頻品質的提升進一步推動了即時教學的使用,降低了先前阻礙同步視訊學習的延遲。同時,現有的自學平台正在投資人工智慧語音助手,以模擬教師的回饋。這兩種策略表明,線上語言學習市場不會出現兩極化,而是整合式工作流程將成為主流。能夠根據學習者的學習進展動態切換自學和即時對話的平台,可望提升用戶終身價值並降低解約率。

到2025年,個人用戶將貢獻47.35%的收入,成為線上語言學習市場的基石。對價格敏感的消費者傾向於免費增值模式,迫使平台在廣告展示和功能限制之間尋求平衡。相較之下,企業客戶正以23.70%的複合年成長率快速成長,他們購買包含分析儀錶板和單一登入(SSO)整合的捆綁式許可證,使每用戶平均收入(ARPU)提高6到8倍。根據《Speak for Business》報告,85%的採用企業已在內部使用該服務,這表明該服務在企業部署中廣泛應用。

公共部門預算撥款正在推動學校和勞動力融合計畫的需求。例如,美國英語語言習得津貼正在促進學區採購自適應解決方案,從而引導學習者融入長期的線上生態系統。這種跨部門效應使供應商能夠將資金再投資於開發面向消費者的功能,展現了一種涵蓋更廣泛的線上語言學習市場中消費者和企業對企業(B2B)子市場的共生收入模式。

線上語言學習市場按學習模式(自學應用程式、教師指導學習、混合式學習等)、最終用戶(個人、企業學習者、教育機構等)、語言(英語、中文、西班牙語、法語等)、年齡層(13 歲以下、13-17 歲、18-30 歲等)、技術平台(行動應用程式、基於 Web 的平台等)和地區進行細分。

區域分析

亞太地區將持續引領線上語言學習市場,預計到2025年將佔全球收入的45.75%。中國的都市區學習者收費購買優質英語課程以助力出國留學,而印度的年輕行動用戶則利用免費增值模式來輔助準備考試。印尼和越南政府的多語言政策要求儘早接觸語言,從而擴大了K-12(幼兒園至高中)階段的語言學習群體。隨著區域內企業吸引外資,企業部門的需求也不斷成長,這促使供應商提供人力資源儀錶板,用於追蹤員工技能進展,以滿足合規報告的要求。

南美洲預計將以21.90%的複合年成長率成為成長最快的地區,這主要得益於巴西龐大的用戶群體以及墨西哥近岸外包的蓬勃發展(墨西哥優先考慮雙語人才)。智慧型手機費用補貼和4G網路覆蓋範圍的擴大拓寬了通路,使得平台能夠提供與通訊業者忠誠度計畫捆綁的英語課程。實踐證明,將當地文化元素(例如體育術語和地方俚語)融入課程內容可以提高完成率,這為線上語言學習市場的課程設計策略提供了關鍵的參考。

在北美和歐洲,人均支出很高,但學習者成長速度緩慢。在北美,移民學習母語這一細分市場以及企業多元化、公平和包容(DEI)預算為學習者成長提供了助力。在歐洲,GDPR合規成本提高了進入門檻,擁有內部法律和資訊安全團隊的成熟供應商具有競爭優勢。儘管如此,這兩個地區都成為了創新試驗場。在這裡完善的功能,例如即時流利度分析,隨後將推廣到亞太和南美,從而加強線上語言學習市場的全球研發擴散循環。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場定義與研究假設

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 全球化帶來的跨國通訊需求

- 利用人工智慧進行自適應學習的採用率

- 行動優先技術在新興市場的普及

- 強制要求企業改進有關 ESG 和 DEI 的詞彙量。

- K-12課程中強制性的早期語言教育

- 語音助理生態系中的技能市場

- 市場限制因素

- 資料安全和隱私問題

- 課程完成率低,解約率率高

- 免費增值模式的收入飽和

- 人工智慧版權和倫理方面的監管障礙

- 價值/供應鏈分析

- 重要法規結構的評估

- 對關鍵相關人員的影響評估

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

- 宏觀經濟因素的影響

第5章 市場規模與成長預測

- 不同的學習模式

- 自學應用程式

- 教師指導式教學

- 混合式學習

- 人工智慧自適應平台

- 最終用戶

- 個別學習者

- 企業培訓生

- 教育機構(小學、國中、高中和高等教育機構)

- 政府和非營利組織

- 按語言

- 英語

- 中文(國語)

- 西班牙語

- 法語

- 德文

- 日本人

- 其他語言

- 按年齡層

- 13歲以下

- 13-17歲

- 18-30歲

- 31-45歲

- 45歲或以上

- 透過技術平台

- 行動應用

- 網路為基礎的平台

- VR和AR工具

- 對話式語音助手

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Duolingo Inc.

- Babbel GmbH

- Busuu Ltd.

- Memrise Ltd.

- Preply Inc.

- Rosetta Stone LLC

- italki HK Ltd.

- Lingoda GmbH

- Enux Education Ltd.(LingoDeer)

- Berlitz Corporation

- EF Education First Ltd.

- VIPKid HK Ltd.

- HelloTalk Ltd.

- Speexx AG

- Mango Languages(Creative Empire LLC)

- Cambridge University Press and Assessment

- Kaplan International Languages

- Pimsleur(Simon and Schuster)

- FluentU Inc.

- Tandem Fundazioa(Tandem app)

- Voxy Inc.

- Open English LLC

- Lingvist OU

- Cambly Inc.

- Speaky Community SAS

第7章 市場機會與未來趨勢

- 評估閒置頻段和未滿足的需求

The online language learning market size was valued at USD 21.06 billion in 2025 and estimated to grow from USD 24.39 billion in 2026 to reach USD 50.82 billion by 2031, at a CAGR of 15.83% during the forecast period (2026-2031).

Growing cross-border trade, demographic shifts, and rapid mobile adoption keep demand high, while AI-driven personalization and immersive technologies strengthen learning effectiveness. Platforms deliver ever-larger course catalogues and adaptive paths that improve retention, a key differentiator in an increasingly competitive landscape. Corporates accelerate spending on workforce language skills to meet ESG and DEI goals, and public-sector budgets for multilingual programs further expand the accessible learner base. Meanwhile, strict data-privacy regimes in Europe and rising user-acquisition costs in saturated freemium channels temper growth, encouraging platforms to refine monetization strategies and diversify revenue streams.

Global Online Language Learning Market Trends and Insights

Globalisation-driven cross-border communication demand

Intensifying international trade turns language proficiency into a core competitiveness lever. Enterprises across technology, tourism, and finance invest in scalable online language programs to remove communication bottlenecks. Providers like Open English have broadened Latin American access by marketing English skills as an economic mobility enabler. Regional trade blocs also lift demand for Portuguese and Spanish, underscoring multi-directional growth beyond English .

AI-powered adaptive learning penetration

Artificial-intelligence engines now adjust content sequencing, difficulty, and feedback in real time, raising completion rates and upsell potential. Duolingo integrates generative AI to personalize review loops and pronunciation drills, an investment detailed in its 2024 SEC filing . Venture funding echoes this trend: Speak's valuation surpassed USD 1 billion after proving conversational AI can support a billion spoken sentences and premium adoption. Platforms that align AI with privacy-by-design guidelines build durable differentiation under Europe's strict data regime.

Data-security and privacy concerns

GDPR rules prohibit unchecked voice-data transfers to third-party AI processors, forcing platforms to build costly private speech-recognition pipelines. New localization mandates further raise overhead, compressing smaller entrants' margins and nudging the market toward scale players with in-house compliance teams.

Other drivers and restraints analyzed in the detailed report include:

- Mobile-first uptake in emerging economies

- Corporate ESG and DEI language-upskilling mandates

- Low course-completion and high churn rates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Self-learning apps generated 56.35% of 2025 revenue, underpinning the online language learning market's largest delivery channel. This dominance relies on always-on accessibility, micro-lesson design, and algorithmic personalization that lower per-learner cost. However, tutor-led live instruction is advancing at 21.25% CAGR, reflecting heightened demand for real-time conversation that algorithms still only partially simulate. Hybrid pathways-recorded modules plus weekly tutor sessions-emerge as the retention sweet-spot, helping platforms defend subscription pricing. Preply's marketplace illustrates the financial upside of such blended delivery, with session bookings rising alongside subscription upgrades. Continued innovation in scheduling automation and pay-per-minute billing is expected to pull more independent instructors onto aggregated platforms, deepening supply and compressing lesson prices to learners' benefit.

Rising broadband quality in emerging markets further boosts live tutoring uptake by mitigating latency that previously hindered synchronous video practice. Conversely, self-learning incumbents invest in AI voice partners to replicate tutor feedback. The dual strategy indicates the online language learning market will not polarize; rather, integrated workflows will dominate. Providers that dynamically route learners between self-study and live conversation based on progress signals could see higher lifetime value and lower churn.

Individuals held 47.35% of 2025 revenue-a foundational pillar of the online language learning market. Price-sensitive consumers gravitate toward freemium models, forcing platforms to balance ad loads and feature gating. In contrast, corporate clients, expanding at 23.70% CAGR, purchase bulk licences bundled with analytics dashboards and single-sign-on integrations that command 6-8X higher ARPU. Speak for Business reports 85% internal adoption within client firms, reinforcing the stickiness of enterprise rollouts.

Public-sector allocations strengthen demand from schools and workforce-integration programs. U.S. English Language Acquisition grants, for instance, stimulate district-level procurement of adaptive solutions, thereby funneling learners into long-term online ecosystems . The cross-subsidy effect allows vendors to reinvest in consumer feature development, illustrating the symbiotic revenue model spanning consumer and B2B sub-markets within the broader online language learning market.

The Online Language Learning Market is Segmented by Learning Mode (Self Learning Apps, Tutor-Led, Blended Learning, and More), End-User (Individual, Corporate Learners, Educational Institutions, and More), Language (English, Mandarin Chinese, Spanish, French, and More), Age Group (<< 13 Years, 13 - 17 Years, 18 - 30 Years, and More), Technology Platforms (Mobile Applications, Web-Based Platforms, and More), and Geography.

Geography Analysis

Asia-Pacific, with 45.75% of 2025 revenue, remains the engine of the online language learning market. China's urban learners pay for premium English tracks that facilitate overseas study, while India's young mobile-native population leans on freemium tiers to supplement exam preparation. Government multilingual policies in Indonesia and Vietnam mandate early exposure, broadening the K-12 funnel. Corporate-sector demand grows as regional firms court foreign investment, pushing vendors to launch HR dashboards that log skill progression for compliance reporting.

South America posts the fastest 21.90% CAGR outlook, propelled by Brazil's massive user base and Mexico's near-shoring boom that values bilingual staff. Subsidized smartphone plans and improved 4G coverage widen distribution channels, letting platforms bundle English courses with telecom loyalty programs. Local cultural references in content-sports idioms, regional slang-have proven to lift completion rates, a critical insight for the online language learning market's course-design strategy.

North America and Europe exhibit high per-capita spend yet slower learner-base expansion. North America benefits from immigration-driven heritage-language niches and enterprises' DEI budgets. Europe's GDPR compliance costs elevate entry barriers, tilting competitive advantage toward established providers with in-house legal and infosec teams. Nevertheless, both regions act as innovation testbeds-features perfected here, like real-time dysfluency analytics, later scale into Asia-Pacific and South America, reinforcing a global RandD diffusion cycle inside the online language learning market.

- Duolingo Inc.

- Babbel GmbH

- Busuu Ltd.

- Memrise Ltd.

- Preply Inc.

- Rosetta Stone LLC

- italki HK Ltd.

- Lingoda GmbH

- Enux Education Ltd. (LingoDeer)

- Berlitz Corporation

- EF Education First Ltd.

- VIPKid HK Ltd.

- HelloTalk Ltd.

- Speexx AG

- Mango Languages (Creative Empire LLC)

- Cambridge University Press and Assessment

- Kaplan International Languages

- Pimsleur (Simon and Schuster)

- FluentU Inc.

- Tandem Fundazioa (Tandem app)

- Voxy Inc.

- Open English LLC

- Lingvist OU

- Cambly Inc.

- Speaky Community SAS

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Globalisation-driven cross-border communication demand

- 4.2.2 AI-powered adaptive learning penetration

- 4.2.3 Mobile-first uptake in emerging economies

- 4.2.4 Corporate ESG and DEI language-upskilling mandates

- 4.2.5 Early-age language mandates in K-12 curricula

- 4.2.6 Voice-assistant ecosystem skill marketplaces

- 4.3 Market Restraints

- 4.3.1 Data-security and privacy concerns

- 4.3.2 Low course-completion and high churn rates

- 4.3.3 Freemium-model revenue saturation

- 4.3.4 AI copyright / ethics regulatory barriers

- 4.4 Value / Supply-Chain Analysis

- 4.5 Evaluation of Critical Regulatory Framework

- 4.6 Impact Assessment of Key Stakeholders

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Impact of Macro-economic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Learning Mode

- 5.1.1 Self-Learning Apps

- 5.1.2 Tutor-Led

- 5.1.3 Blended Learning

- 5.1.4 AI-Adaptive Platforms

- 5.2 By End-user

- 5.2.1 Individual Learners

- 5.2.2 Corporate Learners

- 5.2.3 Educational Institutions (K-12 and Higher-Ed)

- 5.2.4 Government and Non-profit Bodies

- 5.3 By Language

- 5.3.1 English

- 5.3.2 Mandarin Chinese

- 5.3.3 Spanish

- 5.3.4 French

- 5.3.5 German

- 5.3.6 Japanese

- 5.3.7 Other Languages

- 5.4 By Age Group

- 5.4.1 < 13 Years

- 5.4.2 13 - 17 Years

- 5.4.3 18 - 30 Years

- 5.4.4 31 - 45 Years

- 5.4.5 > 45 Years

- 5.5 By Technology Platform

- 5.5.1 Mobile Applications

- 5.5.2 Web-based Platforms

- 5.5.3 VR and AR Tools

- 5.5.4 Conversational Voice Assistants

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 UAE

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Egypt

- 5.6.5.2.4 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Duolingo Inc.

- 6.4.2 Babbel GmbH

- 6.4.3 Busuu Ltd.

- 6.4.4 Memrise Ltd.

- 6.4.5 Preply Inc.

- 6.4.6 Rosetta Stone LLC

- 6.4.7 italki HK Ltd.

- 6.4.8 Lingoda GmbH

- 6.4.9 Enux Education Ltd. (LingoDeer)

- 6.4.10 Berlitz Corporation

- 6.4.11 EF Education First Ltd.

- 6.4.12 VIPKid HK Ltd.

- 6.4.13 HelloTalk Ltd.

- 6.4.14 Speexx AG

- 6.4.15 Mango Languages (Creative Empire LLC)

- 6.4.16 Cambridge University Press and Assessment

- 6.4.17 Kaplan International Languages

- 6.4.18 Pimsleur (Simon and Schuster)

- 6.4.19 FluentU Inc.

- 6.4.20 Tandem Fundazioa (Tandem app)

- 6.4.21 Voxy Inc.

- 6.4.22 Open English LLC

- 6.4.23 Lingvist OU

- 6.4.24 Cambly Inc.

- 6.4.25 Speaky Community SAS

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-space and Unmet-need Assessment

2026-2030年全球線上語言學習市場

2026-2030年全球線上語言學習市場 2026年全球線上語言學習市場報告

2026年全球線上語言學習市場報告 線上語言學習市場規模、佔有率和成長分析(按學習模式、應用、語言類型、課程類型、實施模式和地區分類)—產業預測(2026-2033 年)

線上語言學習市場規模、佔有率和成長分析(按學習模式、應用、語言類型、課程類型、實施模式和地區分類)—產業預測(2026-2033 年) 線上語言學習-全球市場佔有率和排名、總收入和需求預測(2025-2031年)

線上語言學習-全球市場佔有率和排名、總收入和需求預測(2025-2031年) 線上語言學習市場按產品類型、最終用戶、學習模式、定價模式和交付平台分類的全球預測(2025-2032 年)

線上語言學習市場按產品類型、最終用戶、學習模式、定價模式和交付平台分類的全球預測(2025-2032 年) 全球線上語言家教市場

全球線上語言家教市場 線上語言學習市場規模、佔有率、趨勢分析報告(按學習模式、最終用途、地區、細分市場預測,2025 年至 2030 年)

線上語言學習市場規模、佔有率、趨勢分析報告(按學習模式、最終用途、地區、細分市場預測,2025 年至 2030 年) 北美線上語言學習市場規模、佔有率、預測、趨勢分析:按學習模式、年齡組、語言、最終用戶、國家/地區 - 預測到 2031 年全球線上語言學習市場

北美線上語言學習市場規模、佔有率、預測、趨勢分析:按學習模式、年齡組、語言、最終用戶、國家/地區 - 預測到 2031 年全球線上語言學習市場 全球線上語言課程市場規模、佔有率和趨勢分析:按語言提供、年齡層、水平、地區、前景和預測,2024-2031

全球線上語言課程市場規模、佔有率和趨勢分析:按語言提供、年齡層、水平、地區、前景和預測,2024-2031