|

市場調查報告書

商品編碼

2035015

資產型代幣:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Asset Tokenization - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

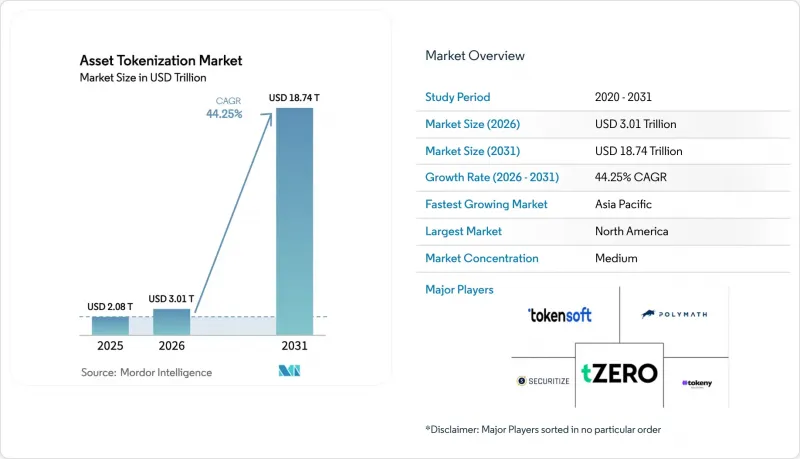

2025 年資產型代幣市場價值 2.08 兆美元,預計到 2031 年將達到 18.74 兆美元,而 2026 年為 3.01 兆美元,預測期(2026-2031 年)複合年成長率為 44.25%。

北美和歐盟監管政策的澄清、機構投資者資本重新配置的快速進展以及跨鏈互通性的日趨成熟,都為大規模代幣發行和二級市場的商業性可行性提供了支撐。儘管許可型架構在發行量方面仍佔據主導地位,但對開放網路的需求激增表明,隨著合規工具的改進,去中心化流動性正被越來越多的人接受。隨著企業利用排碳權和貴金屬代幣來對沖與環境、社會和治理(ESG)相關的債務和通膨風險,商品代幣化正成為一個明顯的成長領域。能夠將強大的法律包裝與無縫的ISO-20022通訊傳遞相結合的供應商,在獲得一級銀行的訂單具有明顯的優勢。

全球資產型代幣市場趨勢與洞察

機構投資者和代幣化基金的採用率不斷提高

機構投資者正加速將資金配置到代幣化貨幣市場和固定收益產品。貝萊德的美元機構數位流動性基金在推出幾個月內就募集了超過5.5億美元,這表明市場對提供每日分紅和日內贖回窗口的鏈上金融替代方案有著明顯的需求。高盛計畫在2025年底前推出三款代幣化產品,而摩根大通的Kinexys網路將在2024年底前處理1.5兆美元的代幣化交易,並正在試點鏈上外匯結算,預計將於2025年初發布。這些舉措正在產生網路效應,促使託管機構、基金管理人和資產管理公司建立相容的基礎設施。

對房地產部分所有權的需求

基於代幣的持分所有權結構降低了最低投資額,使更多投資者能夠進入優質房地產市場。 T-RIZE集團將一項價值3億美元的住宅開發項目代幣化,展示了發起人如何透過擴大市場覆蓋率並吸引多元化的投資者群體來降低資金籌措成本。透過不可竄改的業績數據提高透明度,可以緩解資訊不對稱這一長期存在的商業房地產投資障礙,從而增強二次性市場的流動性。美國和歐盟的群眾集資法規與代幣化框架一致,進一步增強了面向普通投資者的房地產產品的成長潛力。

網路安全與智慧合約漏洞

一系列備受矚目的攻擊事件持續削弱市場信心。 2024年1月,去中心化交易所KiloEx遭受700萬美元損失,因為攻擊者操縱了其鏈上價格Oracle,暴露了其即時資料檢驗的缺陷。因此,保險公司重新評估了風險,導致智慧合約保險保費上漲。為了恢復市場信心,各平台現在強制要求進行多層審計、自動電路斷流器和即時監控。然而,威脅情勢瞬息萬變,即使是經過嚴格審查的程式碼也可能存在潛在漏洞,因此安全性仍然是代幣化經營團隊的首要任務。

細分市場分析

房地產板塊是最大的收入來源,預計到2025年將佔資產型代幣市場的30.12%。機構投資者的需求集中在能夠產生可預測現金流的關鍵辦公大樓和物流資產上,而代幣結構降低了准入門檻,並促進了跨地域的多元化投資組合。此板塊採用許可型網路,經審計的智慧合約可自動分配租金收入,從而簡化基金經理人的對帳工作。大宗商品板塊雖然目前規模較小,但成長速度最快,預計到2031年將達到48.35%的複合年成長率,這主要得益於ESG支持的排碳權和貴金屬代幣的發行。可再生能源生產商將代幣視為兌現檢驗減排放的高流動性手段,這推動了數位商品交易所的雙向交易量成長。債務證券也受到持續關注,美國正在實施市政債券代幣試點項目,以實現當日結算並降低發行費用。

對於尋求跨境投資者基礎的房地產開發商而言,監管協調至關重要。在阿拉伯聯合大公國和盧森堡等司法管轄區,鏈上股東名冊現已獲準使用,從而促進了二級市場轉讓和抵押。在商品領域,諸如倫敦金銀市場協會(LBMA)的區塊鏈溯源項目等標準化舉措正在增強人們對數位黃金產品的信心。排碳權代幣的優勢在於其透明的生命週期數據,有助於企業買家進行合規報告。隨著互通性框架的日趨成熟,交易所將能夠上線包含房地產和商品代幣的多資產池,從而提高機構投資者投資組合的風險調整後收益,並擴大相關資產的代幣化市場。

到2025年,機構投資者將掌控69.10%的投資資本,這反映出他們有能力駕馭複雜的法律結構並管理龐大的資產負債表。資產管理公司正在利用代幣化基金來提高營運效率,包括近乎即時的股票上市和自動化的公司行為處理。在收購MG Stover之後,Securitize已發行的代幣總額已超過10億美元,目前管理著715只基金,資產規模達380億美元,並已確立了自身作為連接一級市場和二級市場的端到端服務供應商的地位。退休基金也將代幣化的房地產和基礎設施視為匹配長期債務的一種方式,並期望藉此提高流動性。

在合規眾群眾集資豁免和直覺易用的行動錢包的支持下,個人投資者參與度正以50.20%的複合年成長率快速成長。這些行動錢包巧妙地隱藏了區塊鏈的複雜性。經過認證的個人投資者扮演著橋樑角色,他們享受創投基金代幣和商業房地產小額投資帶來的許多好處,儘管他們的平均投資額較高。整合到發行平台中的教育入口網站指導新用戶創建錢包、了解風險披露資訊並完成稅務申報,從而提高了轉換率。展望未來,嵌入式金融與新型銀行的整合可望進一步降低進入門檻,並透過涵蓋新興經濟體中服務不足的群體,擴大整體資產型代幣市場。

資產型代幣市場按資產類別(房地產、債務證券、投資基金、私募股權等)、投資者類型(機構投資者、合格個人投資者等)、代幣化平台類型(許可型(私有)區塊鏈等)、交付方式(代幣化平台/中介件等)和地區進行細分。市場預測以美元計價。

區域分析

北美仍然是最大的區域貢獻者,預計到2025年將佔全球收入的39.10%。美國受益於美國證券交易委員會(SEC)於2025年4月發布的指導意見,該意見明確指出某些以美元為支撐的穩定幣不被視為證券,這鼓勵了銀行參與代幣化存款試點計畫。加拿大的監管沙盒正在支持代幣化抵押房屋抵押貸款池的實驗,該國的退休基金也開始收購基礎設施支持的安全符記的少數股權。創投也集中在該地區,根據PitchBook的數據顯示,專注於區塊鏈的基金在2024年完成了24億美元的新資金籌措,進一步加強了創新的良性循環。

亞太地區是成長最快的地區,預計到2031年將以53.75%的複合年成長率成長。新加坡的「守護者計畫」(Project Guardian)目前已吸引了40多家金融機構參與,在新加坡金融管理局(MAS)管理的互通帳本上試行代幣化債券、存款和基金。香港於2025年6月公佈的數位資產藍圖引入了穩定幣牌照制度和政府發行的代幣化債券,這表明當局給予了官方支持,並有望帶動區域銀行和保險公司的參與。日本正在推動一項框架,旨在重新界定某些數位資產的分類,為代幣化交易所交易基金(ETF)鋪平道路,並擴大個人投資者獲取另類資產的管道。

在歐洲,加密資產市場監管局 (MiCA) 正在穩步推進,該監管局為加密資產服務供應商建立了跨境許可通行證制度。德國的《電子證券法》允許在分散式帳本技術 (DLT) 帳本上發行不記名債券和共同基金佔有率,使公共部門發行機構能夠開始測試全數位化工作流程。在法國的公共區塊鏈沙盒中,三個專注於綠色債券流通的代幣化項目已獲核准,這反映了歐洲大陸對氣候融資的重視。同時,在中東和非洲,阿布達比和約翰尼斯堡的監管沙盒中正在進行能源支援安全符記的試點計畫;在南美洲,隨著基礎設施的完善,計畫正從概念驗證(PoC) 階段過渡到有限的公開發行階段。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場定義與研究假設

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 明確主要金融中心的相關法規

- 擴大機構投資者採用和代幣化基金

- 對房地產部分所有權的需求

- 區塊鏈互通性的進展

- ISO-20022 的整合實現了無縫支付。

- 代幣化碳權產品的出現

- 市場限制因素

- 監管碎片化和合規成本

- 網路安全與智慧合約漏洞

- Oracle營運與鏈下資料風險

- 破產案件中託管人的責任

- 價值/供應鏈分析

- 重要法規結構的評估

- 對關鍵相關人員的影響評估

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

- 宏觀經濟因素的影響

第5章 市場規模與成長預測

- 按資產類別

- 房地產

- 債務證券

- 投資基金

- 私募股權

- 公開股權

- 商品

- 按投資者類型

- 機構投資者

- 合格個人投資者

- 個人投資者

- 代幣化平台類型

- 許可型(私有)區塊鏈

- 無需許可(公共)區塊鏈

- 混合模式

- 報價

- 令牌化平台/中介軟體

- 智慧合約開發與審計

- 託管和錢包服務

- 合規與法律科技服務

- 二級交易和交易所

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Securitize Markets, LLC

- tZERO Group, Inc.

- Tokensoft Inc.

- Polymath Research Inc.

- Tokeny Solutions SA

- Fireblocks Inc.

- Chainlink Labs, Inc.

- INX Digital Company, Inc.

- Anchorage Digital Bank NA

- Bitbond GmbH

- Tassat Group LLC

- Rialto Markets, LLC

- ADDX Pte. Ltd.

- DigiShares A/S

- Smartlands Platform Ltd.

- Blockstream Corporation Inc.

- Figure Technologies, Inc.

- Provenance Blockchain, Inc.

- Maple Finance Ltd.

- Stokr SA

第7章 市場機會與未來趨勢

- 評估閒置頻段和未滿足的需求

The asset tokenization market size was valued at USD 2.08 trillion in 2025 and estimated to grow from USD 3.01 trillion in 2026 to reach USD 18.74 trillion by 2031, at a CAGR of 44.25% during the forecast period (2026-2031).

Regulatory clarity in North America and the European Union, rapid institutional capital re-allocation, and the maturing of cross-chain interoperability now underpin the commercial viability of large-scale token issuance and secondary trading. Permissioned architectures still dominate issuance volumes, yet surging demand for open networks signals rising comfort with decentralized liquidity as compliance tooling improves. Commodities tokenization is emerging as the clear growth frontier as corporates use carbon-credit and precious-metal tokens to hedge ESG liabilities and inflation exposure. Platform vendors that can fuse robust legal wrappers with seamless ISO-20022 messaging are gaining a tangible advantage in winning tier-1 banking mandates.

Global Asset Tokenization Market Trends and Insights

Rising Institutional Adoption and Tokenized Funds

Institutional allocations into tokenized money-market and fixed-income products are accelerating. BlackRock's USD Institutional Digital Liquidity Fund attracted over USD 550 million within months of launch, showing clear appetite for on-chain treasury alternatives that offer daily dividend distribution and intraday redemption windows. Goldman Sachs is preparing three tokenized products for roll-out by year-end 2025, while JPMorgan's Kinexys network has processed USD 1.5 trillion in tokenized transactions by end-2024 and is piloting on-chain foreign-exchange settlement for early-2025 release. These moves create network effects that encourage custodians, fund administrators, and asset managers to build compatible rails.

Demand for Fractional Real-Estate Ownership

Token-enabled fractional structures lower minimum ticket sizes, allowing a broader investor base to enter prime property markets. T-RIZE Group's USD 300 million residential development tokenization illustrates how sponsors are securing diverse investor pools while reducing financing costs through wider market reach . Enhanced transparency from immutable performance data also mitigates information asymmetry, a long-standing barrier in commercial real-estate investing, which in turn boosts secondary liquidity. Crowdfunding regulations aligned with tokenization frameworks in the United States and the European Union further reinforce growth potential for retail-accessible real-estate products.

Cyber-Security and Smart-Contract Vulnerabilities

High-profile exploits continue to dent market confidence. In January 2024 the KiloEx decentralized exchange lost USD 7 million after attackers manipulated an on-chain price oracle, exposing gaps in real-time data validation. Insurance premiums for smart-contract cover have since risen as underwriters reprice risk. Platforms are now mandating multi-layer audits, automated circuit breakers, and real-time monitoring to regain trust. Yet the evolving threat landscape means even rigorously vetted code can harbor latent flaws, keeping security a top-tier boardroom concern for tokenization providers.

Other drivers and restraints analyzed in the detailed report include:

- Advancements in Blockchain Interoperability

- ISO-20022 Integration Enabling Seamless Settlement

- Custodial Liability During Insolvency Events

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Real-estate contributes the largest revenue slice, accounting for 30.12% of the asset tokenization market in 2025. Institutional demand centers on flagship office towers and logistics assets that deliver predictable cash flows, while token structures reduce entry thresholds and amplify portfolio diversification across regions. The segment uses permissioned networks where audited smart contracts automatically distribute rental income, thus easing reconciliation for fund administrators. Commodities, though smaller today, are posting the fastest trajectory with a 48.35% CAGR through 2031, powered by carbon-credit and precious-metal token launches underpinned by ESG mandates. Renewable energy producers see tokens as a liquid instrument for monetizing verified emission reductions, which boosts bilateral trading volumes on digital commodity exchanges. Debt instruments also show steady interest, with municipal-bond token pilots in the United States offering same-day settlement and lower issuance fees.

Regulatory harmonization is pivotal for real-estate sponsors seeking cross-border investor pools. Jurisdictions such as the United Arab Emirates and Luxembourg now recognize on-chain share registries, easing secondary transfers and collateral pledges. For commodities, standardization initiatives like the London Bullion Market Association's blockchain provenance project are spurring confidence in digital gold products. Carbon-credit tokens benefit from transparent lifecycle data that supports compliance reporting for corporate buyers. As interoperability frameworks mature, exchanges can list multi-asset pools that bundle real-estate and commodities tokens, improving risk-adjusted returns for institutional portfolios and enlarging the addressable asset tokenization market.

Institutional investors controlled 69.10% of deployed capital in 2025, reflecting their readiness to navigate complex legal structures and their sizeable balance sheets. Asset managers leverage tokenized funds to gain operational efficiencies, including near-instant share issuance and automated corporate-action processing. Securitize has crossed USD 1 billion in issued tokens and now administers USD 38 billion across 715 funds after acquiring MG Stover, positioning itself as an end-to-end service provider linking primary issuance and secondary marketplaces. Pension funds also view tokenized real-estate and infrastructure as a match for long-duration liabilities given the potential for improved liquidity.

Retail participation is scaling swiftly at 50.20% CAGR, helped by compliant crowdfunding exemptions and intuitive mobile wallets that mask blockchain complexity. Accredited retail segments occupy a bridging role, bringing higher average ticket sizes yet still benefiting from fractional exposure to venture-fund tokens and commercial real-estate. Education portals embedded into issuance platforms guide new entrants through wallet creation, risk disclosures, and tax documentation, broadening funnel conversion rates. Looking ahead, embedded-finance integrations with neobanks will further lower onboarding friction, expanding the overall asset tokenization market by tapping under-served demographics in emerging economies.

Asset Tokenization Market is Segmented by Asset Class (Real Estate, Debt Instruments, Investment Funds, Private Equity, and More), Investor Type (Institutional Investors, Accredited Retail Investors, and More), Tokenization Platform Type (Permissioned (Private) Blockchains, and More), Offering (Tokenization Platforms / Middleware, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America remains the largest regional contributor, holding 39.10% of global revenue in 2025. The United States benefits from April 2025 SEC guidance clarifying that certain USD-backed stablecoins are not securities, which in turn catalyzes bank participation in tokenized deposit pilots. Canada's regulatory sandbox supports experimentation with tokenized mortgage pools, and its pension funds are beginning to acquire minority stakes in infrastructure-backed security tokens. Venture investment also concentrates in the region, with specialized blockchain funds closing USD 2.4 billion in fresh capital in 2024 according to PitchBook, further reinforcing the innovation loop.

Asia-Pacific is the fastest-growing region, expanding at a 53.75% CAGR through 2031. Singapore's Project Guardian now involves over 40 financial institutions testing tokenized bonds, deposits, and funds on interoperable ledgers governed by the Monetary Authority of Singapore. Hong Kong's June 2025 digital-asset roadmap introduces a stablecoin licensing regime and government tokenized-bond issuance, signaling official endorsement that will likely mobilize regional banks and insurers. Japan is advancing a framework that reclassifies certain digital assets, paving the way for tokenized exchange-traded funds and broadening retail access to alternative assets .

Europe posts steady progress under the Markets in Crypto-Assets (MiCA) regulation that sets passport-able licensing for crypto-asset service providers. Germany's electronic securities law recognizes bearer bonds and fund units on DLT registers, prompting public-sector issuers to test fully digital workflows. France's public blockchain sandbox accepted three tokenization projects focused on green-bond distribution, reflecting the continent's climate-finance focus. Meanwhile, the Middle East and Africa are piloting energy-backed security tokens inside regulatory sandboxes in Abu Dhabi and Johannesburg, and South America is evolving from proof-of-concepts toward limited public offerings as infrastructure matures.

- Securitize Markets, LLC

- tZERO Group, Inc.

- Tokensoft Inc.

- Polymath Research Inc.

- Tokeny Solutions SA

- Fireblocks Inc.

- Chainlink Labs, Inc.

- INX Digital Company, Inc.

- Anchorage Digital Bank N.A.

- Bitbond GmbH

- Tassat Group LLC

- Rialto Markets, LLC

- ADDX Pte. Ltd.

- DigiShares A/S

- Smartlands Platform Ltd.

- Blockstream Corporation Inc.

- Figure Technologies, Inc.

- Provenance Blockchain, Inc.

- Maple Finance Ltd.

- Stokr S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory clarity in key financial hubs

- 4.2.2 Rising institutional adoption and tokenized funds

- 4.2.3 Demand for fractional real-estate ownership

- 4.2.4 Advancements in blockchain interoperability

- 4.2.5 ISO-20022 integration enabling seamless settlement

- 4.2.6 Emergence of tokenized carbon-credit instruments

- 4.3 Market Restraints

- 4.3.1 Regulatory fragmentation and compliance costs

- 4.3.2 Cyber-security and smart-contract vulnerabilities

- 4.3.3 Oracle manipulation and off-chain data risks

- 4.3.4 Custodial liability during insolvency events

- 4.4 Value / Supply-Chain Analysis

- 4.5 Evaluation of Critical Regulatory Framework

- 4.6 Impact Assessment of Key Stakeholders

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Impact of Macro-economic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Asset Class

- 5.1.1 Real-Estate

- 5.1.2 Debt Instruments

- 5.1.3 Investment Funds

- 5.1.4 Private Equity

- 5.1.5 Public Equity

- 5.1.6 Commodities

- 5.2 By Investor Type

- 5.2.1 Institutional Investors

- 5.2.2 Accredited Retail Investors

- 5.2.3 Retail Investors

- 5.3 By Tokenization Platform Type

- 5.3.1 Permissioned (Private) Blockchains

- 5.3.2 Permissionless (Public) Blockchains

- 5.3.3 Hybrid Models

- 5.4 By Offering

- 5.4.1 Tokenization Platforms / Middleware

- 5.4.2 Smart-Contract Development and Audit

- 5.4.3 Custody and Wallet Services

- 5.4.4 Compliance and Legal-Tech Services

- 5.4.5 Secondary Trading and Exchanges

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Securitize Markets, LLC

- 6.4.2 tZERO Group, Inc.

- 6.4.3 Tokensoft Inc.

- 6.4.4 Polymath Research Inc.

- 6.4.5 Tokeny Solutions SA

- 6.4.6 Fireblocks Inc.

- 6.4.7 Chainlink Labs, Inc.

- 6.4.8 INX Digital Company, Inc.

- 6.4.9 Anchorage Digital Bank N.A.

- 6.4.10 Bitbond GmbH

- 6.4.11 Tassat Group LLC

- 6.4.12 Rialto Markets, LLC

- 6.4.13 ADDX Pte. Ltd.

- 6.4.14 DigiShares A/S

- 6.4.15 Smartlands Platform Ltd.

- 6.4.16 Blockstream Corporation Inc.

- 6.4.17 Figure Technologies, Inc.

- 6.4.18 Provenance Blockchain, Inc.

- 6.4.19 Maple Finance Ltd.

- 6.4.20 Stokr S.A.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-space and Unmet-need Assessment

數位資產代幣化平台市場預測至2034年-按資產類型、平台類型、組件、代幣類型、應用、最終用戶和地區分類的全球分析

數位資產代幣化平台市場預測至2034年-按資產類型、平台類型、組件、代幣類型、應用、最終用戶和地區分類的全球分析 代幣化市場:按類型、產品、資產類型、標準、部署模式、應用、產業和組織規模分類-2026-2032年全球市場預測

代幣化市場:按類型、產品、資產類型、標準、部署模式、應用、產業和組織規模分類-2026-2032年全球市場預測 2026年LLM代幣化最佳化全球市場報告

2026年LLM代幣化最佳化全球市場報告 資產代幣化市場規模、佔有率和趨勢分析報告:按資產類別、投資者類型、代幣化平台、產品、地區和細分市場預測(2026-2033 年)2026年全球標記化市場報告

資產代幣化市場規模、佔有率和趨勢分析報告:按資產類別、投資者類型、代幣化平台、產品、地區和細分市場預測(2026-2033 年)2026年全球標記化市場報告 代幣化市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、解決方案和模式分類

代幣化市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、解決方案和模式分類 全球代幣化市場規模、佔有率、趨勢和成長分析報告(2026-2034)代幣化市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034 年)

全球代幣化市場規模、佔有率、趨勢和成長分析報告(2026-2034)代幣化市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034 年) 代幣化市場-全球產業規模、佔有率、趨勢、機會與預測:按組件、應用、產業、地區和競爭格局分類,2021-2031年

代幣化市場-全球產業規模、佔有率、趨勢、機會與預測:按組件、應用、產業、地區和競爭格局分類,2021-2031年 中心化交易所代幣(CEX)市場規模、佔有率和成長分析(按區塊鏈平台、代幣類型、交易所類型和地區分類)—2026-2033年產業預測

中心化交易所代幣(CEX)市場規模、佔有率和成長分析(按區塊鏈平台、代幣類型、交易所類型和地區分類)—2026-2033年產業預測