|

市場調查報告書

商品編碼

2035001

日本資料中心電力市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Japan Data Center Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

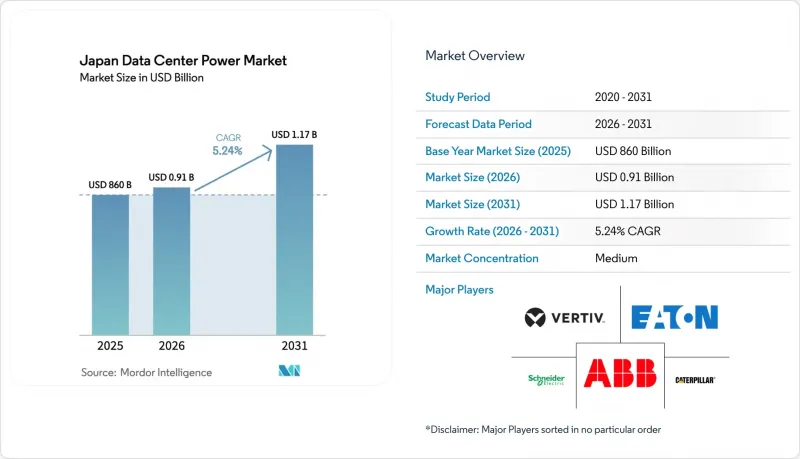

日本資料中心電力市場規模預計將從 2025 年的 8.6 億美元成長到 2026 年的 9.1 億美元,然後從 2026 年到 2031 年以 5.24% 的複合年成長率成長,到 2031 年達到 11.7 億美元。

穩健的「雲端優先」策略、人工智慧工作負載的激增以及對碳中和營運的持續承諾,正在推動對彈性且節能的基礎設施的需求。新的海底電纜登陸點、不斷擴展的連接選擇以及對沿海城市投資的促進,也推動了市場的發展。高電力消耗量的超大規模園區平均設施容量已從三年前的10-15兆瓦大幅提升至如今的40兆瓦以上。這迫使公用事業公司加強區域電網,並促使營運商部署現場可再生能源發電和大規模儲能系統。東部50赫茲電網和西部60赫茲電網之間的頻率差異持續使互聯策略變得複雜,但也促進了專注於頻率無關儲能技術的新夥伴關係的建立。 Google與Equinix簽署的2024-2025年購電協議(PPA)標誌著長期可再生能源採購協議的決定性轉變,這些協議能夠保護營運商免受電價波動的影響。

日本資料中心電力市場趨勢及洞察。

擴大超大規模和雲端設施的採用

超大規模營運商目前運作的園區容量已超過 40 兆瓦,機架密度高達 60 千瓦,有時甚至超過 100 千瓦。Softbank Corporation位於北海道的 300 兆瓦苫小牧資料中心就展示了巨型園區如何利用涼爽氣候,透過自然通風來分散處理負載。這種規模的擴張導致區域電網堵塞,尤其是在東京周邊地區,使得新增容量申請的前置作業時間長達 36 個月。因此,營運商正在探索採用模組化電源模組,以實現分階段擴展,不受電網容量限制。這一趨勢正在推動日本資料中心電力市場的快速現代化,資料中心紛紛採用基於鋰離子電池的 UPS 系統和母線槽配電來應對波動性較大的人工智慧工作負載。

政府主導的數位轉型(DX)計劃

日本的「綠色成長策略」設定了2030年將清潔能源在電網中的佔比提高到36%至38%的目標,並強制要求資料中心使用可再生能源。日本的「氣候變遷調適債券」計畫旨在籌集120兆日圓(約8,000億美元),用於資金籌措直接為數位基礎設施供電的可再生能源計畫。政府也為風能和太陽能資源豐富的縣的電力項目提供快速核准程序,從而引導資料中心投資流向東京-大阪走廊以外的地區。獎勵包括對提高電源使用效率(PUE)的設備提供稅收減免,這有助於提升日本資料中心電力市場的整體競爭力。

電網堵塞和供電供給能力限制

東京電網正因超大規模負載的累積而承受巨大壓力,變電站升級速度遠不及負載成長速度。營運商被迫排隊等待取得容量,導致專案運作日期延遲,預算大幅膨脹。電池儲能系統(BESS)結合購電協議(PPA)雖然提供了臨時解決方案,但也增加了初始成本。電力公司正在透過加強與新建海底電纜登陸點重疊的沿海輸電線路走廊來應對這一問題,但由於這項工作進展緩慢,電網擁塞仍然是日本資料中心電力市場面臨的主要障礙。

細分市場分析

至2025年,UPS系統將佔日本資料中心電力市場37.60%的佔有率,凸顯其作為抵禦電網不穩定的第一道防線的重要角色。鋰離子電池的採用雖然會帶來更高的價格,但可以縮短充電週期並減少面積。對於目標PUE低於1.3的超大規模資料中心而言,這是一個可以接受的權衡。在發電機方面,柴油燃料電池正逐步被氫燃料電池取代,例如,蜀南市的一個試點計畫就將改造後的汽車燃料電池與現場太陽能發電陣列結合。 PDU在高密度機架中佔據著至關重要的地位,由於其能夠提供精細的測量和遠端分支級監控,預計到2031年,PDU將成為所有組件中成長最快的,複合年成長率將達到6.45%。這項發展動能正推動日本資料中心電力市場持續專注於與DCIM平台整合的智慧配電技術。

UPS的更新週期與人工智慧驅動的運算叢集的需求相契合,這些集群需要大規模且穩定的電源供應,迫使供應商將預測電池健康分析功能整合到韌體中。整合到UPS框架中的儲能模組有助於降低尖峰需求費用並提高可再生能源的吸收率。隨著碳中和目標的日益嚴格,營運商依賴能夠與微電網同步運行的UPS架構,這些微電網會隨著雲量和風速的變化而波動。因此,組件配置正在朝向既能保護負載又能作為併網資產運作的系統演進,以滿足更廣泛的日本資料中心電力市場的需求。

託管服務提供者佔總消耗量的 60.95%。這主要歸功於企業對高度互聯的園區架構的重視,這些架構能夠提供對接不同通訊業者。超大規模雲端服務供應商雖然數量較少,但卻是成長最快的細分市場,在國內人工智慧和機器學習工作負載激增的推動下,其複合年成長率 (CAGR) 高達 7.85%。公共部門的數位轉型 (DX) 專案和金融科技的普及正在刺激對安全機櫃和專用機房的需求,進一步鞏固了託管服務提供者在日本資料中心市場的核心地位。

邊緣站點和企業級站點構成互補層,共同支援 5G 的延遲目標。這些站點佔地面積小規模,僅 1-5 兆瓦,並採用模組化電源系統和貨櫃式電池組以縮短前置作業時間。這些層級共同作用,使日本資料中心電力市場的容量配置更加多元化,減輕了電網負荷,並提高了整體韌性。國際企業正與當地電力專家合作,克服與頻率不匹配和抗震安全相關的監管障礙,確保無論是託管資料中心還是超大規模資料中心,從一開始就將強大的備用系統整合到新建設中。

日本資料中心電力市場按組件(電氣解決方案、服務)、資料中心類型(超大規模資料中心業者資料中心/雲端服務供應商、主機服務供應商等)、資料中心規模(小規模資料中心、中型資料中心、大型資料中心等)和等級(Tier I 和 II、Tier III、Tier IV)進行細分。市場預測以美元計價。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴大超大規模和雲端設施的採用

- 政府主導的數位轉型(DX)計劃

- 5G 的部署和邊緣基礎設施的擴展正在加速需求成長。

- 關於可再生能源和碳中和的法規

- 海底電纜在各地區的鋪設促進了農村地區的建設。

- 現場公司間購電協議 (PPA) 正在加速電池儲能的普及。

- 市場限制因素

- 安裝和維護需要大量資金投入

- 電網堵塞和供電供給能力限制

- 嚴格的地震合規成本

- 高壓電力工程師短缺

- 供應鏈分析

- 監理情勢

- 技術展望(先進UPS、儲能系統、固態開關設備)

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭強度

- 對與市場相關的宏觀經濟趨勢進行評估

第5章 市場規模與成長預測

- 按組件

- 電氣解決方案

- UPS系統

- 發電機

- 柴油發電機

- 瓦斯發電機

- 氫燃料電池發電機

- 配電單元

- 切換裝置

- 傳輸開關

- 遠端電源面板

- 能源儲存系統

- 服務

- 安裝和試運行

- 維護和支援

- 培訓和諮詢

- 電氣解決方案

- 依資料中心類型

- 超大規模資料中心業者雲端服務供應商/雲端服務供應商

- 託管服務提供者

- 企業和邊緣資料中心

- 按資料中心規模

- 小規模資料中心

- 中型資料中心

- 大型資料中心

- 超大型資料中心

- 超大型資料中心

- 等級

- 一級和二級

- Tier III

- Tier IV

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ABB Ltd

- Schneider Electric SE

- Vertiv Group Corp.

- Mitsubishi Electric Corp.

- Eaton Corporation

- Cummins Inc.

- Caterpillar Inc.

- Hitachi Energy Ltd.

- Legrand Group

- Rittal GmbH and Co. KG

- Fujitsu Ltd.

- Toshiba Energy Systems and Solutions

- Kohler Power Systems

- Fuji Electric Co. Ltd.

- Socomec Group

- Delta Electronics Inc.

- Huawei Technologies Co. Ltd.

- Nidec Corp.

- Rolls-Royce Power Systems(MTU)

- Cisco Systems Inc.

第7章 市場機會與未來展望

The Japan data center power market size is expected to grow from USD 860 million in 2025 to USD 910 million in 2026 and is forecast to reach USD 1.17 billion by 2031 at 5.24% CAGR over 2026-2031.

Robust cloud-first strategies, fast-rising AI workloads, and a sustained push for carbon-neutral operations are combining to raise demand for resilient, energy-efficient infrastructure. The market is also buoyed by new submarine-cable landings that widen connectivity options and stimulate investment in secondary coastal cities. Power-hungry hyperscale campuses are increasing average facility capacity from 10-15 MW three years ago to well above 40 MW today, forcing utilities to reinforce local grids and driving operators toward on-site renewable generation and large battery systems. Grid fragmentation between the 50 Hz east and 60 Hz west continues to complicate interconnection strategies, yet it is spurring new partnerships focused on frequency-independent storage technologies. Corporate Power Purchase Agreements (PPAs) signed by Google and Equinix in 2024-2025 mark a decisive shift toward long-term renewable procurement contracts that buffer operators against volatile utility tariffs.

Japan Data Center Power Market Trends and Insights

Rising adoption of hyperscale and cloud facilities

Hyperscale operators now commission campuses exceeding 40 MW, pushing rack densities past 60 kW and occasionally 100 kW.SoftBank's 300 MW Tomakomai complex in Hokkaido demonstrates how mega campuses decentralize processing loads while tapping cooler climates for free-air cooling advantages. Such scale drives localized grid congestion, especially around Tokyo, where new capacity requests face lead times of up to 36 months. Consequently, operators experiment with modular power blocks that work independently of grid constraints and allow phased expansion. This trend keeps the Japan data center power market on a steep modernization curve as facilities deploy lithium-ion-based UPS systems and busway distribution to accommodate volatile AI workloads

Government-led digital-transformation programs

The Green Growth Strategy requires data centers to draw from renewable sources as the national grid targets a 36-38% clean-energy share by 2030. Japan's Climate Transition Bond program seeks JPY 120 trillion (USD 800 billion) to finance renewable projects that directly feed digital infrastructure.Authorities also offer fast-track permitting for power projects in regional prefectures rich in wind or solar resources, redirecting data center investment beyond the Tokyo-Osaka corridor. Incentives include tax reductions for equipment that improves power usage effectiveness (PUE), which helps raise the overall competitiveness of the Japan data center power market.

Grid congestion and power-availability limits

Tokyo's distribution network is strained by cumulative hyperscale loads that outpace substation upgrades. Operators queue for capacity reservations, delaying go-live dates and inflating project budgets. Battery energy storage systems (BESS) paired with PPAs offer interim relief but add to upfront spend. Utilities respond by reinforcing coastal transmission corridors that coincide with new submarine-cable landings, yet the lag keeps grid congestion a material brake on the Japan data center power market.

Other drivers and restraints analyzed in the detailed report include:

- 5G roll-out and edge build-outs accelerating demand

- Renewable power and carbon-neutral mandates

- High installation and maintenance CAPEX

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

UPS systems controlled 37.60% of the Japan data center power market in 2025, underscoring their role as a first-line defense against grid instability. Lithium-ion adoption shortens recharge cycles and lowers footprint despite a price premium, an acceptable trade-off for hyperscale campuses that target sub-1.3 PUE levels. The generator category is undergoing a pivot from diesel toward hydrogen fuel cells, a shift highlighted by pilot deployments in Shunan City that pair reused automotive cells with on-site solar arrays. PDUs, holding a vital position for high-density racks, will post the fastest component growth at 6.45% CAGR to 2031 due to granular metering and remote branch-level monitoring. This momentum keeps the Japan data center power market squarely focused on intelligent distribution technologies that integrate with DCIM platforms.

The UPS refresh cycle aligns with AI-driven compute clusters that demand stable power delivery at scale, pushing vendors to embed predictive analytics for battery health inside their firmware. Energy-storage modules linked to UPS frameworks help shave peak demand charges and improve renewable absorption rates. As carbon-free targets tighten, operators rely on continuous-cycle UPS architectures capable of syncing with microgrids that fluctuate when cloud cover or wind speeds change. The component mix, therefore, evolves toward systems that safeguard loads yet also act as grid-interactive assets within the wider Japan data center power market.

Colocation providers account for 60.95% of total consumption because enterprises prize interconnection-rich campuses that deliver diverse carrier access and compliance clarity. Tokyo's multi-tenant facilities remain preferred on-ramp sites into the broader Asian cloud fabric. Hyperscale cloud operators, while fewer in number, represent the fastest growth slice at 7.85% CAGR as domestic AI and machine-learning workloads surge. Public-sector digital-transformation programs and fintech adoption spur demand for secure cages and dedicated halls, reinforcing colocation's central role in the Japan data center power market.

Edge and enterprise sites form a complementary layer that supports 5G latency targets. Their modest 1-5 MW footprints adopt modular power trains and containerized battery packs to shorten lead times. Combined, these tiers diversify locations at which Japan data center power market capacity is installed, cushioning the grid and raising overall resilience. International players partner with local power specialists to navigate regulatory hurdles tied to frequency mismatches and seismic safety, ensuring that new builds, whether colocation or hyperscale, integrate robust backup schemes from inception

Japan Data Center Power Market is Segmented by Component (Electrical Solutions, Services), Data Center Type (Hyperscaler/Cloud Service Providers, Colocation Providers, and More), Data Center Size (Small Size Data Centers, Medium Size Data Centers, Large Size Data Centers and More), Tier Type (Tier I and II, Tier III, Tier IV). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- ABB Ltd

- Schneider Electric SE

- Vertiv Group Corp.

- Mitsubishi Electric Corp.

- Eaton Corporation

- Cummins Inc.

- Caterpillar Inc.

- Hitachi Energy Ltd.

- Legrand Group

- Rittal GmbH and Co. KG

- Fujitsu Ltd.

- Toshiba Energy Systems and Solutions

- Kohler Power Systems

- Fuji Electric Co. Ltd.

- Socomec Group

- Delta Electronics Inc.

- Huawei Technologies Co. Ltd.

- Nidec Corp.

- Rolls-Royce Power Systems (MTU)

- Cisco Systems Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising adoption of hyperscale and cloud facilities

- 4.2.2 Government-led digital-transformation programs

- 4.2.3 5G roll-out and edge build-outs accelerating demand

- 4.2.4 Renewable power and carbon-neutral mandates

- 4.2.5 Regional submarine-cable landings boosting rural builds

- 4.2.6 On-site corporate PPAs driving battery storage uptake

- 4.3 Market Restraints

- 4.3.1 High installation and maintenance CAPEX

- 4.3.2 Grid congestion and power-availability limits

- 4.3.3 Stringent seismic-resilience compliance costs

- 4.3.4 Shortage of high-voltage power engineers

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook (advanced UPS, BESS, solid-state switchgear)

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

- 4.8 Assesment of Macroeconomic Trends on the Market

5 MARKET SIZE and GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Electrical Solutions

- 5.1.1.1 UPS Systems

- 5.1.1.2 Generators

- 5.1.1.2.1 Diesel Generators

- 5.1.1.2.2 Gas Generators

- 5.1.1.2.3 Hydrogen Fuel-cell Generators

- 5.1.1.3 Power Distribution Units

- 5.1.1.4 Switchgear

- 5.1.1.5 Transfer Switches

- 5.1.1.6 Remote Power Panels

- 5.1.1.7 Energy-storage Systems

- 5.1.2 Service

- 5.1.2.1 Installation and Commissioning

- 5.1.2.2 Maintenance and Support

- 5.1.2.3 Training and Consulting

- 5.1.1 Electrical Solutions

- 5.2 By Data Center Type

- 5.2.1 Hyperscaler/Cloud Service Providers

- 5.2.2 Colocation Providers

- 5.2.3 Enterprise and Edge Data Center

- 5.3 By Data Center Size

- 5.3.1 Small Size Data Centers

- 5.3.2 Medium Size Data Centers

- 5.3.3 Large Size Data Centers

- 5.3.4 Massive Size Data Centers

- 5.3.5 Mega Size Data Centers

- 5.4 By Tier Level

- 5.4.1 Tier I and II

- 5.4.2 Tier III

- 5.4.3 Tier IV

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ABB Ltd

- 6.4.2 Schneider Electric SE

- 6.4.3 Vertiv Group Corp.

- 6.4.4 Mitsubishi Electric Corp.

- 6.4.5 Eaton Corporation

- 6.4.6 Cummins Inc.

- 6.4.7 Caterpillar Inc.

- 6.4.8 Hitachi Energy Ltd.

- 6.4.9 Legrand Group

- 6.4.10 Rittal GmbH and Co. KG

- 6.4.11 Fujitsu Ltd.

- 6.4.12 Toshiba Energy Systems and Solutions

- 6.4.13 Kohler Power Systems

- 6.4.14 Fuji Electric Co. Ltd.

- 6.4.15 Socomec Group

- 6.4.16 Delta Electronics Inc.

- 6.4.17 Huawei Technologies Co. Ltd.

- 6.4.18 Nidec Corp.

- 6.4.19 Rolls-Royce Power Systems (MTU)

- 6.4.20 Cisco Systems Inc.

7 MARKET OPPORTUNITIES and FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment

資料中心電源管理市場規模、佔有率和成長分析:按組件、硬體類型、軟體和服務、資料中心類型、最終用途和地區分類-2026-2033年產業預測

資料中心電源管理市場規模、佔有率和成長分析:按組件、硬體類型、軟體和服務、資料中心類型、最終用途和地區分類-2026-2033年產業預測 資料中心電源市場:按組件類型、層級、資料中心類型和行業分類 - 全球市場預測(2026-2032 年)

資料中心電源市場:按組件類型、層級、資料中心類型和行業分類 - 全球市場預測(2026-2032 年) 資料中心電源市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、解決方案、交付模式

資料中心電源市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、解決方案、交付模式 2026年全球資料中心電力市場報告2026年全球資料中心電源管理市場報告伺服器電源市場:依產品類型、組件、額定功率、外形規格、應用、最終用戶和通路分類-2026-2030年全球預測資料中心以AC-DC電源市場:按組件、電源類型、冗餘方式和應用分類-2026-2032年全球預測資料中心電源系統氮化鎵市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、形式、材料類型、裝置及部署方式分類

2026年全球資料中心電力市場報告2026年全球資料中心電源管理市場報告伺服器電源市場:依產品類型、組件、額定功率、外形規格、應用、最終用戶和通路分類-2026-2030年全球預測資料中心以AC-DC電源市場:按組件、電源類型、冗餘方式和應用分類-2026-2032年全球預測資料中心電源系統氮化鎵市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、形式、材料類型、裝置及部署方式分類 全球資料中心電力市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球資料中心電力市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析及預測(2026-2034 年)

全球資料中心電力市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球資料中心電力市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析及預測(2026-2034 年)