|

市場調查報告書

商品編碼

2035000

千兆廣播:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Gigacasting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

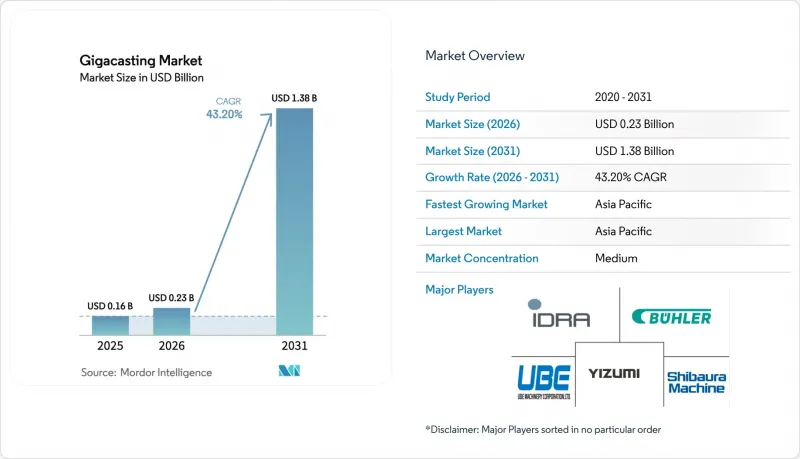

預計到 2026 年,千兆廣播市場規模將達到 2.2912 億美元,高於 2025 年的 1.6 億美元,預計到 2031 年將達到 13.8 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 43.20%。

這一成長清晰地表明,汽車製造商正專注於大規模高壓壓鑄,將眾多鈑金沖壓件整合為少數鋁製零件。特斯拉透過將Model Y的171個沖壓件減少到僅兩個後底盤鑄件,直接製造成本降低了高達40%。類似的成本降低、更短的生產週期以及日益嚴格的二氧化碳排放法規,正推動巨型鑄造市場在所有主要生產區域持續擴張。乘用車電氣化、再生鋁溢價上漲以及模組化沖壓生產線的引入進一步刺激了需求,而熟練焊工的短缺則迫使原始設備製造商(OEM)轉向高度自動化的鑄造單元。

全球千兆廣播市場趨勢與洞察

純電動車生產快速擴張

在全球各地的純電動車組裝廠中,GigaPress電池的引進速度正以遠超傳統焊接生產線的速度成長。現代汽車已在北美投資210億美元用於電氣化,其中包括在其Metaplant America工廠建造一條高噸位鑄造生產線。福特汽車已將其科隆工廠徹底改造為電氣化中心,引入了600多台機器人以縮短車身車間的生產週期。電池外殼需要深模壓成型結構,以確保碰撞安全性和熱性能,而GigaCasting技術是實現此類形狀的最快路徑。隨著純電動車年產量成長至數百萬輛,規模經濟效應將推動GigaCasting市場遠遠超越小眾市場。

對更輕、結構更緊湊的車身的需求

超級鑄造技術使汽車製造商能夠在不犧牲車身本體剛性的前提下減輕車身重量。特斯拉的後部鑄件減少了70個零件,從而降低了材料、焊接和物流成本。鋁材的高強度重量比和設計靈活性使得碰撞能量吸收路徑能夠整合到一個大型鑄件中,而這些路徑此前需要數十個沖壓件才能實現。日本一級供應商Ryobi正在將其產能轉向大型鋁鑄件,目標是將製造成本降低20%。隨著車輛平均二氧化碳排放法規日益嚴格以及人們對電動車續航里程的期望不斷提高,輕量化技術也在不斷發展。隨著越來越多的車型採用滑板式電池組,底盤鑄件自然而然地成為最佳化載荷路徑和提高封裝效率的有效途徑。

產能超過 6000 噸的壓平機需要大量的初始投資。

即使是一台9000噸的巨型壓機,造價也可能高達數千萬美元。沃爾沃位於斯洛伐克的工廠已向IDRA訂購了兩台壓平機,並為周邊鑄造廠、修邊線和基礎設施建設累計了8.55億歐元。一級供應商Nemac僅在其現有工廠增設兩台4500噸壓平機就花費了1800萬美元,這表明即使是中等噸位的壓機也需要大量投資。小規模的品牌難以憑藉有限的產量收回投資,這阻礙了巨型壓機的廣泛應用,並將市場推向了財力雄厚的企業。

細分市場分析

到2025年,車身總成將佔千兆電池市場58.05%的佔有率,並且仍將是大多數大規模生產部署的核心,而電池和底盤鑄件的複合年成長率將達到46.20%。由於所有純電動車都採用需要快速散熱和碰撞載荷傳遞路徑的底盤式電池組,與電池外殼相關的千兆電池市場預計將快速成長。特斯拉在後部鑄件方面的成功正在加速這一轉變,而Handtmann已採用Bühler的Carat-610電芯為其歐洲電動車專案大規模生產電池組框架。

整合式隧道鑄件的需求也在不斷成長,這種鑄件將側樑、橫樑和組件安裝座整合在一個鑄件中。引擎和電力驅動殼體正處於轉型期,內燃機鑄件的需求正在下降,而新型馬達安裝座則不斷湧入市場。隨著單速驅動系統的普及,變速箱鑄件的需求也正在下降。雖然航太和工業領域的一些細分應用正在研發中湧現,但在短期內,汽車應用仍將是推動巨型鑄件市場發展的主要動力。

由於鋁材在重量、成本和廢料回收效率方面表現出色,預計到2025年,鋁材仍將佔據73.85%的銷售佔有率。然而,鎂材45.60%的複合年成長率表明,該材料正經歷顯著的成長。根據美國汽車工程師協會(SAE)發布的研究,高溫鎂合金即使在300 度C的高溫下也能保持結構完整性,使其適用於馬達和逆變器支架等應用。同時,新型超高延展性鋁矽鎂合金使得Gigapress模具能夠採用更薄的壁厚,並滿足碰撞安全性能要求。

鋼鐵製造商正透過先進的電池機殼鑄造鋼材來維持其市場佔有率。安賽樂米塔爾推出了一款易於回收且碰撞安全性能相當的原型產品。鈦和鋅由於成本和密度方面的劣勢,仍然是小眾選擇。鋁能否保持其優勢取決於廢料的供應情況、能源價格以及多合金材料的壓製成型能力。

區域分析

預計到2025年,亞太地區將佔全球銷量的48.40%,並在2031年之前以47.90%的複合年成長率持續成長,這主要得益於中國在鋰離子電池供應領域的領先地位以及快速擴張的純電動汽車組裝產能。中國鑄造製造商已為本地整車製造商運作多台6000-8000噸的壓平機,而Ryobi計劃通過在廣島生產大型鋁鑄件來降低20%的成本。日本和韓國正透過供應商主導的投資以及現代汽車在北美斥資210億美元的電氣化計畫(該計畫仍沿用亞洲的設備設計)獲得發展動力。印度目前仍處於起步階段,但隨著政府推出政策支持電動車供應鏈在地化,預計未來該地區將擴大GigaPress的部署規模。

在北美,汽車製造商(OEM)持續加大資本投入,推動巨型鑄造市場的發展。福特斥資20億美元維修其科隆電動車中心,並以56億美元建造其位於藍橢圓城(Blue Oval City)的綜合設施,旨在整合用於生產下一代皮卡和跨界車的巨型鑄造單元。通用汽車(GM)已撥款40億美元升級其美國工廠,以實現年產能200萬輛的目標,其中大部分依賴單體鋁結構。美國目前面臨400萬噸的供不應求,而鋁坯供應也成為阻礙因素,因為從加拿大進口至關重要。

在歐洲,嚴格的碳排放政策與飆升的電價之間的微妙平衡,為數位轉型之路增添了微妙的變數。沃爾沃已在其科希策工廠投資8.55億歐元,購置了兩台9,000噸的IDRA壓機,目標是在2026年投產。德國豪華汽車製造商正在推進數位雙胞胎鑄造廠的引入,但他們需要應對電價波動的問題。南美洲目前的產能有限,但沿岸地區的能源出口國正在探索垂直整合的鋁和鑄造項目。這兩個地區都依賴於尋求企業發展多元化的全球汽車製造商的直接投資。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 純電動車生產快速擴張

- 對輕量化和結構流線型車輛結構的需求

- 與多部件白車身相比,降低零件成本並縮短生產週期。

- 由於熟練焊工短缺,原始設備製造商正在推動鑄造工藝的自動化。

- 高回收鋁含量排碳權溢價

- 模組化/可重構的 GigaPress 生產線能夠實現小批量生產的多樣化。

- 市場限制因素

- 產能超過 6000 噸的壓平機需要大量的初始投資。

- 能源價格導致鋁合金供應緊張

- 碰撞維修的複雜性日益增加,導致保險費上漲。

- 鑄件重量超過12,000噸時,廢品率和氣孔率風險增加。

- 價值/供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模及成長預測(價值(美元))

- 透過使用

- 車身總成

- 底盤/電池外殼

- 引擎和電力驅動部件

- 變速器和傳動系統部件

- 其他

- 材料

- 鋁合金

- 鎂合金

- 先進高抗張強度鋼(AHSS)鑄件

- 其他有色合金

- 車輛類型

- 搭乘用車

- 輕型商用車

- 中型和大型商用車輛

- 普雷斯頓(按數字)

- 6000至8000噸

- 8001-10000噸

- 超過1萬噸

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 埃及

- 土耳其

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- 一級供應商

- IDRA Srl(subsidiary of LK Technology)

- Buhler Group

- Haitian Die-Casting

- Shibaura Machine Co.

- UBE Machinery Corporation

- Yizumi Holdings

- Aisin Corporation

- Handtmann Group

- Ryobi Die Casting

- Gestamp

- Chongqing Dajiang Millison Die Casting Co., Ltd.

- Guangdong Hongtu Technology

- Chuzhou Duoli Automotive Technology

- OEM

- Tesla Inc.

- Toyota Motor Corporation

- Hyundai Motor Company

- Ford Motor Company

- General Motors Company

- Volvo Car AB

- 一級供應商

第7章 市場機會與未來展望

gigacasting market size in 2026 is estimated at USD 229.12 million, growing from 2025 value of USD 0.16 billion with 2031 projections showing USD 1.38 billion, growing at 43.20% CAGR over 2026-2031.

This rise underscores automakers' tight focus on large-format high-pressure die casting, which collapses scores of steel stampings into a handful of aluminum components. Tesla's move from 171 stamped parts to two rear under-body castings in the Model Y cut direct manufacturing expense by up to 40%. Similar cost-down examples, faster takt times, and stricter CO2 regulations continue to expand the gigacasting market footprint across every major production region. Passenger-car electrification, rising recycled-aluminum premiums, and modular press lines further amplify demand, while the shortage of skilled welders nudges OEMs toward highly automated casting cells.

Global Gigacasting Market Trends and Insights

Rapid Scale-up of BEV Production Volumes

Global BEV assembly plants are adding giga press cells faster than conventional weld lines. Hyundai earmarked USD 21 billion for North American electrification that includes high-tonnage casting lines at its Metaplant America complex . Ford re-tooled Cologne into an all-electric center using more than 600 robots to shorten body shop flow time. Battery housing demands deep, one-piece structures for crash and thermal performance, and gigacasting offers the shortest path to those geometries. As annual BEV volumes climb toward multi-million-unit levels, economies of scale lift the gigacasting market well beyond niche status.

Demand for Lightweight, Consolidated Vehicle Structures

Gigacasting lets automakers pull mass out of the body-in-white without sacrificing stiffness. Tesla's rear casting lowered part count by 70 components and saved material, welding, and logistics costs. Aluminum's high strength-to-weight ratio pairs with design freedom, so a single large casting can integrate crash-energy paths that once required dozens of stampings. Japanese Tier-one Ryobi is shifting capacity toward large aluminum castings, targeting 20% total-manufacturing-cost relief. Weight savings dovetail with stricter fleet-average CO2 limits and range expectations in battery vehicles. As more models adopt skateboard battery packs, under-body castings become natural enablers for load-path optimization and packaging efficiency.

High Upfront CAPEX for >= 6,000 t Presses

A single 9,000 t giga-press carries a price tag in the tens of millions. Volvo's Slovakian plant ordered twin IDRA units and budgeted EUR 855 million for the surrounding foundry, trim line, and infrastructure . Tier-one Nemak spent USD 18 million just to add two 4,500 t machines inside an existing facility-illustrating that even mid-range tonnage means deep pockets. Smaller brands struggle to amortize that spend over modest volumes, slowing widespread adoption and nudging the gigacasting market toward financially robust players.

Other drivers and restraints analyzed in the detailed report include:

- Per-part Cost & Takt-time Reductions vs. Multi-part Body-in-White

- Shortage of Skilled Welders Pushing OEMs to Casting Automation

- Energy-price-driven Aluminum-alloy Supply Tightness

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Body assemblies held 58.05% of the gigacasting market share in 2025 and remain core to most rollouts, yet battery and under-body castings are expanding at 46.20% CAGR. The gigacasting market size tied to battery housing is forecast to widen sharply as every BEV adopts a floor-mounted pack needing rapid heat dissipation and crash load pathways. Tesla's rear casting success story quickened the transition, while Handtmann installed Buhler Carat-610 cells to mass-produce pack frames for European EV programs.

Demand also grows for integrated tunnel castings that combine side rail, cross-member, and pack mounts in one pour. Engine and e-drive housings mark a transitional zone; internal-combustion castings taper while new e-motor mounts enter. Transmission castings decline as single-speed drivetrains rise. Niche aerospace and industrial uses surface in R&D pipelines, but automotive applications overwhelmingly steer the near-term gigacasting market.

Aluminum retained 73.85% of 2025 revenue due to its favorable mix of weight, cost, and scrap-loop efficiency. Even so, magnesium's 45.60% CAGR positions it as the stand-out gainer. Research published by SAE shows high-temperature Mg alloys holding structural integrity at 300 °C, opening doors for motor-inverter mounts. Concurrently, new super-ductile Al-Si-Mg grades meet crash performance while enabling thinner sections in giga-press molds.

Steel suppliers defend their share through advanced castable steels for battery enclosures; ArcelorMittal unveiled prototypes promising comparable crash metrics with easier recycling. Titanium or zinc remain niche options due to cost or density penalties. Whether aluminum keeps its lead will rest on scrap availability, energy prices, and multi-alloy press capabilities.

The Gigacasting Market Report is Segmented by Application (Body Assemblies, Under-body/Battery Housings, and More), Material (Aluminum Alloys, Magnesium Alloys, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Press Tonnage (6, 000 To 8, 000 T, 8, 001 To 10, 000 T, and More), Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 48.40% of 2025 revenue and is projected to expand at 47.90% CAGR to 2031, powered by China's dominance in lithium-ion battery supply and rapidly scaling BEV assembly capacity. Chinese foundries already operate multiple 6,000-8,000 t presses for local OEMs, and Ryobi aims for 20% cost relief by producing large aluminum castings in Hiroshima. Japan and South Korea add momentum through supplier-led investments and Hyundai's USD 21 billion North American electrification commitment, which still leverages Asian equipment design. India remains at an early stage but offers policy support for EV supply-chain localization, suggesting future upside for regional giga-press installations.

North America follows with a concentrated wave of OEM capex that underpins the gigacasting market. Ford's USD 2 billion Cologne Electric Vehicle Center overhaul and USD 5.6 billion BlueOval City complex integrate large-tonnage casting cells for next-generation pickups and crossovers. General Motors earmarked USD 4 billion for U.S. plant upgrades to reach 2-million-unit annual output, much of which relies on single-piece aluminum structures. Aluminum billet supply is a constraint, as the United States faces a 4 million t shortfall that keeps Canadian imports critical.

Europe balances strict carbon policy with elevated power prices, shaping a nuanced adoption curve. Volvo's Kosice site committed EUR 855 million for twin 9,000 t IDRA presses to start production in 2026. Germany's premium OEM cluster advances digital-twin foundries but must manage electricity-cost volatility. South America contributes limited volumes today, while Gulf energy exporters explore vertically integrated aluminum and casting projects; both regions hinge on foreign direct investment from global automakers seeking diversified footprints.

- Tier-1 Suppliers

- OEMs

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid scale-up of BEV production volumes

- 4.2.2 Demand for lightweight, consolidated vehicle structures

- 4.2.3 Per-part cost & takt-time reductions vs. multi-part body-in-white

- 4.2.4 Shortage of skilled welders pushing OEMs to casting automation

- 4.2.5 Carbon-credit premiums for high-recycled-content aluminum

- 4.2.6 Modular / re-configurable Giga-Press lines enabling low-volume variants

- 4.3 Market Restraints

- 4.3.1 High upfront CAPEX for greater than or equals 6,000 t presses

- 4.3.2 Energy-price-driven aluminum-alloy supply tightness

- 4.3.3 Collision-repair complexities inflating insurance premiums

- 4.3.4 Elevated scrap & porosity risks in above 12,000 t castings

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Application

- 5.1.1 Body Assemblies

- 5.1.2 Under-body/Battery Housings

- 5.1.3 Engine and e-Drive Parts

- 5.1.4 Transmission and Driveline Parts

- 5.1.5 Others

- 5.2 By Material

- 5.2.1 Aluminum Alloys

- 5.2.2 Magnesium Alloys

- 5.2.3 Advanced High-Strength Steel (AHSS) Castings

- 5.2.4 Other Non-ferrous Alloys

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Medium & Heavy Commercial Vehicles

- 5.4 By Press Tonnage

- 5.4.1 6,000 to 8,000 t

- 5.4.2 8 001 to 10 000 t

- 5.4.3 Above 10,000 t

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Egypt

- 5.5.5.4 Turkey

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Tier-1 Suppliers

- 6.4.1.1 IDRA Srl (subsidiary of LK Technology)

- 6.4.1.2 Buhler Group

- 6.4.1.3 Haitian Die-Casting

- 6.4.1.4 Shibaura Machine Co.

- 6.4.1.5 UBE Machinery Corporation

- 6.4.1.6 Yizumi Holdings

- 6.4.1.7 Aisin Corporation

- 6.4.1.8 Handtmann Group

- 6.4.1.9 Ryobi Die Casting

- 6.4.1.10 Gestamp

- 6.4.1.11 Chongqing Dajiang Millison Die Casting Co., Ltd.

- 6.4.1.12 Guangdong Hongtu Technology

- 6.4.1.13 Chuzhou Duoli Automotive Technology

- 6.4.2 OEMs

- 6.4.2.1 Tesla Inc.

- 6.4.2.2 Toyota Motor Corporation

- 6.4.2.3 Hyundai Motor Company

- 6.4.2.4 Ford Motor Company

- 6.4.2.5 General Motors Company

- 6.4.2.6 Volvo Car AB

- 6.4.1 Tier-1 Suppliers

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

千兆廣播市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、地區和競爭格局分類,2021-2031年

千兆廣播市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、地區和競爭格局分類,2021-2031年 全球一體式鑄造市場(至2035年):產業趨勢與預測

全球一體式鑄造市場(至2035年):產業趨勢與預測 熱軋軋延錨槽市場依產品類型、最終用途、錨固材料及通路分類,全球預測(2026-2032年)

熱軋軋延錨槽市場依產品類型、最終用途、錨固材料及通路分類,全球預測(2026-2032年) 日本鑄造市場規模、佔有率、趨勢及預測(按鑄造類型、製造程序、最終用途行業和地區分類),2026-2034年HALFEN預埋式槽鋼基礎設施市場:按產品類型、材料、承載能力、應用和最終用途產業分類的全球預測(2026-2032年)Halfen預埋槽市場依產品、材料、應用、最終用途產業及銷售管道,全球預測,2026-2032年冷軋鑄槽市場依產品類型、材質等級、表面處理、應用及銷售管道,全球預測(2026-2032年)嵌入式通道市場:按產品類型、分銷管道、材料、應用和最終用戶產業分類,全球預測(2026-2032)嵌入式錨固槽市場按產品類型、技術、應用、最終用戶和分銷管道分類,全球預測(2026-2032年)建築用半預埋槽鋼市場依產品類型、材料、表面保護及應用類型分類,全球預測(2026-2032年)

日本鑄造市場規模、佔有率、趨勢及預測(按鑄造類型、製造程序、最終用途行業和地區分類),2026-2034年HALFEN預埋式槽鋼基礎設施市場:按產品類型、材料、承載能力、應用和最終用途產業分類的全球預測(2026-2032年)Halfen預埋槽市場依產品、材料、應用、最終用途產業及銷售管道,全球預測,2026-2032年冷軋鑄槽市場依產品類型、材質等級、表面處理、應用及銷售管道,全球預測(2026-2032年)嵌入式通道市場:按產品類型、分銷管道、材料、應用和最終用戶產業分類,全球預測(2026-2032)嵌入式錨固槽市場按產品類型、技術、應用、最終用戶和分銷管道分類,全球預測(2026-2032年)建築用半預埋槽鋼市場依產品類型、材料、表面保護及應用類型分類,全球預測(2026-2032年)