|

市場調查報告書

商品編碼

2034991

GRC軟體:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)GRC Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

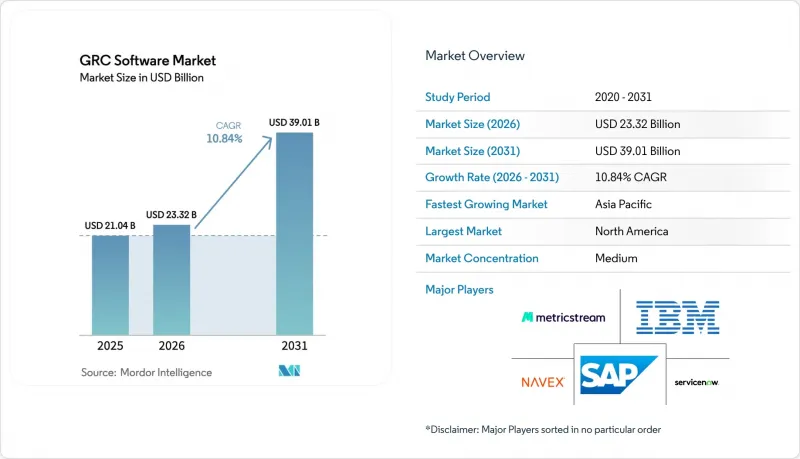

2025 年,管治、風險和合規 (GRC) 軟體市場價值為 210.4 億美元,預計到 2031 年將達到 390.1 億美元,而 2026 年為 233.2 億美元,在預測期(2026-2031 年)內複合年成長率為 10.84%。

監管差異的擴大、網路攻擊目標的增加以及董事會層面持續控制監控需求的上升,正促使企業轉向統一的雲端原生平台,以即時整合政策、風險和審計工作流程。儘管軟體元件仍佔據主導地位,但託管服務的兩位數成長表明,企業更傾向於專家主導的部署,以彌補內部技能缺口。隨著企業尋求對其全球分散式營運進行協調監管,雲端採用正在加速。同時,人工智慧驅動的分析正在改變管治、風險和合規 (GRC) 軟體市場,使其從被動的遵循成本轉向主動的風險情報投資。環境、社會和治理 (ESG)、隱私和業務永續營運要求的整合也在重塑平台藍圖,供應商正致力於提供模組化套件,將碳核算、人工智慧管治和網路保險證據收集功能整合到單一管理介面中。

全球 GRC 軟體市場趨勢與洞察

加強全球資料隱私法規

隨著跨境資料隱私法規的激增和嚴厲的經濟處罰,跨國公司正被迫用端到端平台取代其零散的工具集,以實現證據收集和資料外洩通知的自動化。諸如《數位營運彈性法案》等新法規擴大了可報告事件的範圍,並加強了第三方監管,促使企業將資料映射、同意管理和供應商風險管理工作流程整合到一個統一的管治、風險和合規 (GRC) 軟體市場平台中。合違規的連鎖效應——一個司法管轄區的缺陷可能引發其他地區的平行調查——凸顯了即時儀表板的價值,這些儀表板能夠提供區域管理差距的可見性。供應商正透過提供基於 400 多項全球法規的每日更新的政策庫來應對這項挑戰,並整合工作流程引擎,將糾正任務分配給業務部門負責人。提供機器可讀審計追蹤的平台能夠加快監管核准,降低外部審計成本,加速將預算從人工電子表格轉移到人工智慧驅動的合規中心。

雲端原生應用程式的普及

微服務、容器和無伺服器架構會產生傳統稽核簡介無法擷取的短暫資源,因此持續的控制監控至關重要。現代平台在 Kubernetes 准入控制器中整合了鉤子,可在部署時檢驗策略,並將遙測資料串流傳輸到風險模型,每隔幾秒鐘重新計算一次熱圖。這種動態監控在亞太地區尤其重要,因為該地區的數位新創公司每天部署數百次程式碼,監管機構也強制要求揭露營運彈性。對配置漂移、漏洞狀況和合規狀態進行即時關聯分析,可以將策略違規檢測的平均時間從數週縮短到數分鐘,從而幫助董事會證明對管治、風險和合規 (GRC) 軟體市場的額外投資是合理的。雲端服務供應商正與 GRC 供應商合作,開放合規 API,無需安裝代理,從而降低了小規模團隊的採用門檻。因此,雲端原生整合已將評估標準從複選框式的框架響應轉變為延遲、可擴展性和自動化修復的深度。

跨多個司法管轄區合規的複雜性和成本

規則手冊的碎片化導致文件冗餘,每年使合規總成本增加7,800億美元。報告標準、保存期限和風險評估頻率的差異都增加了對工具、流程和人員的需求。缺乏受控管治、風險和合規 (GRC) 軟體基礎的跨國公司,其反腐敗、隱私和業務永續營運計分類別運行不同的系統,導致資料孤島和審計疲勞。雖然平台整合會增加初始授權成本,但它可以透過減少外部顧問支出和降低違規罰款來帶來回報。儘管巴塞爾協議III等區域協調努力已顯示出部分趨同,但法國的《薩潘二號法案》和德國的《供應鏈法案》等新的國家特定法規的引入意味著,從長遠來看,成本壓力仍然很大。

細分市場分析

預計到2025年,軟體業務將維持71.65%的收入佔有率,這主要得益於企業對整合風險、審計、隱私和ESG模組的套件產品的偏好。然而,服務業務預計將成長最快,到2031年複合年成長率將達到12.98%,這凸顯了市場正向以結果為導向的合約模式轉變,這種模式將技術實施與專家指導相結合。託管服務供應商正在部署平台加速器,將控制措施與區域法規進行匹配,並代表內部資源有限的客戶營運持續監控中心。這種混合交付模式縮短了中型買家實現價值所需的時間,並減少了必須在數十個司法管轄區同時部署的大規模跨國公司的投資回收期。隨著供應商將諮詢、配置和營運服務整合到訂閱包中,管治、風險和合規(GRC)軟體的服務市場預計將穩定成長。先進的實施後分析功能可以對同業群體中的控制成熟度進行基準測試,這為希望透過糾正措施藍圖將洞察轉化為收益的顧問公司創造了交叉銷售機會。

平台提供者正透過人工智慧驅動的控制映射和自然語言策略匯入功能來增強其軟體,從而減少基準部署所需的人工工作量。他們還開放API,以促進與網路靶場測試、電子取證和低程式碼工作流程工具的生態系統整合。這種擴充性吸引合作夥伴擴展核心功能,並刺激間接收入來源。儘管自動化取得了進展,但諸如多帳本職責分離和細粒度資料主權分區等複雜配置任務仍然需要專家參與,這將維持穩健的業務收益基礎。在預測期內,企業買家預計將增加其總專案預算中分配給託管功能的比例,從而推動管治、風險和合規 (GRC) 軟體市場中軟體和服務的擴張。

預計到 2025 年,雲端採用將佔總收入的 62.90%,複合年成長率 (CAGR) 為 13.85%。這反映出企業對彈性可擴展性和協作監控的強勁需求。持續控制監控服務使風險管理團隊能夠分析從 SaaS、IaaS(基礎設施即服務)和本地連接器獲取的即時遙測數據,從而避免部署本地硬體相關的資本支出 (CAPEX)。這種架構支援快速策略更新、自動收集合規性證據和遠端審計訪問,這些功能深受分散式辦公團隊的重視。隨著整合藍圖的成熟以及供應商透過特定區域的租戶配置實現對嚴格資料居住法規的合規性,雲端解決方案的管治、風險和合規 (GRC) 軟體市場規模預計將超過本地解決方案。

在國防、公共安全和關鍵基礎設施等領域,本地部署仍將持續,因為空氣間隙環境仍然至關重要。這些領域的買家需要強大的設備、內部 API 閘道和離線報告功能。然而,供應商正在透過推出容器化版本模糊部署的界限,這些版本既可以在客戶的資料中心運行,也可以在自主雲端中運行。遷移藍圖通常從託管沙箱中的非生產工作負載開始,並在檢驗加密、金鑰管理和存取隔離標準後擴展到受監管的資料集。混合編配主機提供跨兩種模式的整合式儀表板,確保跨異質環境的策略一致性和稽核可追溯性。因此,管治、風險和合規 (GRC) 軟體市場正持續向「盡可能使用雲,必要時使用本地部署」的模式轉型,以平衡效能、自主性和成本。

管治、風險和合規 (GRC) 軟體市場報告按組件(軟體和服務)、部署模式(雲端和本地部署)、組織規模(大型企業、中小企業)、行業垂直領域(銀行、金融服務和保險、醫療保健和生命科學、製造業、IT 和電信等)以及地區(北美、南美、歐洲、亞太地區、中東和非洲)進行細分。

區域分析

預計到2025年,北美將佔全球收入的39.55%,這主要得益於成熟的法規結構、網路保險的高普及率以及股東訴訟率高,促使董事會課責。聯邦機構目前要求近乎即時地通知資料外洩事件,迫使企業實施持續監控和自動化證據管理,並將這些功能整合到領先的管治、風險和合規 (GRC) 軟體市場平台中。技術和諮詢服務提供者之間的整合也透過捆綁式諮詢服務和SaaS訂閱產品,簡化了採購流程,從而加速了該地區的採用。

在歐洲,大規模的用戶群體得益於《一般資料保護規範》(GDPR)和《歐盟人工智慧法案》等開創性立法,這些立法計劃將課責擴大到演算法透明度和生命週期監控。根據《數位營運韌性法案》,銀行、保險公司和能源營運商現在必須提交自我評估報告,這催生了對能夠模擬資訊通訊技術故障鏈的場景測試引擎的新需求。因此,強調消費者保護和系統穩定性的政策舉措,鞏固了歐洲市場對管治、風險和合規(GRC)軟體的佔有率。供應商正透過在其平台內設定符合「Schrems II」裁決要求的區域資料處理區、多語言政策庫和跨境資料傳輸檢查等機制來凸顯自身優勢。

亞太地區預計將以15.1%的複合年成長率成為全球成長最快的地區,這主要得益於快速的數位化、金融科技創新以及不斷擴大的碳排放交易體系。中國、日本、韓國和新加坡等國政府正在實施不同的永續性揭露標準,同時借鏡歐洲的相關法規。跨國公司也越來越傾向於採用可配置的平台,以便並行相容多種框架。該地區的中小型企業正擴大採用「按需計量收費」模式,以滿足全球品牌嚴格的供應商認證標準,這推動了對管治、風險和合規(GRC)軟體的需求。同時,在拉丁美洲、中東和非洲,GRC軟體的應用尚處於起步階段,但隨著外國直接投資者在註資前要求企業提供有據可查的管治控制結構,相關領域的關注度正在不斷提高。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加強全球資料隱私法規

- 雲端原生應用程式的普及

- 網路保險承保要求激增

- 擴大ESG報告義務

- 將人工智慧驅動的預測分析引入風險管理

- 董事會層面需要「持續控制監控」。

- 市場限制因素

- 跨多個司法管轄區合規的複雜性和成本

- 缺乏內部GRC專業知識

- 人工智慧管治方面的監管不確定性

- 對整合套件中供應商鎖定問題的擔憂

- 價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素的影響

- 波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 部署模式

- 雲

- 現場

- 按組織規模

- 大公司

- 中小企業

- 按行業

- 銀行、金融服務和保險(BFSI)

- 醫療保健和生命科學

- 製造業

- 資訊科技/通訊

- 政府/公共部門

- 能源與公共產業

- 零售和消費品

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- IBM Corporation

- SAP SE

- Oracle Corporation

- SAS Institute Inc.

- ServiceNow, Inc.

- Wolters Kluwer NV(Enablon)

- Thomson Reuters Corporation

- NAVEX Global, Inc.

- MetricStream, Inc.

- Diligent Corporation

- Riskonnect, Inc.

- Archer Technologies LLC(RSA)

- LogicGate, Inc.

- OneTrust, LLC

- Workiva Inc.

- Galvanize(A Diligent Company)

- Mitratech Holdings Inc.

- Ideagen PLC

- Sword GRC Limited

- SAI Global Pty Limited

- LogicManager, Inc.

- Quantivate, LLC

- ProcessGene Ltd.

- Continuity Logic, LLC

- RiskWatch International, LLC

第7章 市場機會與未來展望

The Governance, Risk, and Compliance (GRC) Software market size was valued at USD 21.04 billion in 2025 and estimated to grow from USD 23.32 billion in 2026 to reach USD 39.01 billion by 2031, at a CAGR of 10.84% during the forecast period (2026-2031).

Heightened regulatory divergence, growing cyber-attack surfaces, and board-level demand for continuous controls monitoring are steering enterprises toward unified, cloud-native platforms that integrate policy, risk, and audit workflows in real time. Software components continue to dominate, yet double-digit expansion of managed services signals a preference for expert-led implementations that offset internal skills shortages. Cloud deployment is accelerating as firms seek collaborative oversight across globally distributed operations, while AI-driven analytics are turning the Governance, Risk, and Compliance (GRC) Software market from a reactive compliance outlay into a proactive risk-intelligence investment. Convergence of ESG, privacy, and operational-resilience mandates is also reshaping platform roadmaps, pushing vendors toward modular suites that embed carbon accounting, AI governance, and cyber-insurance evidence collection within a single pane of glass.

Global GRC Software Market Trends and Insights

Intensifying Global Data-Privacy Regulations

Cross-border data privacy mandates are multiplying, and stiff financial penalties are forcing multinationals to replace patchwork toolsets with end-to-end platforms that automate evidence gathering and breach notification. New regimes such as the Digital Operational Resilience Act enlarge the scope of reportable incidents and impose strict third-party oversight, prompting enterprises to consolidate data-mapping, consent management, and vendor-risk workflows inside a single Governance, Risk, and Compliance (GRC) Software market platform. The cascading nature of non-compliance-where a lapse in one jurisdiction can trigger parallel investigations elsewhere-elevates the value of real-time dashboards that surface control gaps by geography. Vendors are responding with policy libraries updated daily against more than 400 global statutes, while integrated workflow engines route remediation tasks to line-of-business owners. Platforms that deliver machine-readable audit trails are achieving faster regulator sign-offs and lowering external-audit fees, reinforcing a cycle of budget reallocation from manual spreadsheets to AI-augmented compliance hubs.

Proliferation of Cloud-Native Applications

Microservices, containers, and serverless architectures generate ephemeral resources that evade traditional audit snapshots, making continuous controls monitoring indispensable. Modern platforms now embed Kubernetes admission-controller hooks that validate policy at deploy time, streaming telemetry into risk models that recalculate heat maps every few seconds. This dynamic oversight is especially critical in Asia-Pacific, where digital-first start-ups deploy code hundreds of times per day and regulators are mandating operational-resilience disclosures. Real-time correlation of configuration drift, vulnerability posture, and compliance posture cuts mean-time-to-detect for policy violations from weeks to minutes, helping boards justify additional investment in the Governance, Risk, and Compliance (GRC) Software market. Cloud service providers are partnering with GRC vendors to publish compliance APIs that remove the need for agent installation, reducing onboarding friction for small teams. As a result, cloud-native integration has shifted evaluation criteria from checkbox support for a framework to latency, scale, and automated remediation depth.

Complexity and Cost of Multi-Jurisdictional Compliance

Fragmented rulebooks add overlapping documentation duties that inflate the total cost of compliance by USD 780 billion annually. Each divergence-be it reporting thresholds, retention periods, or risk-assessment cadences-multiplies tooling, process, and staffing demands. Multinationals that lack an orchestrated Governance, Risk, and Compliance (GRC) Software market backbone juggle separate instances for anti-corruption, privacy, and operational-resilience programs, creating data silos and audit fatigue. Platform unification drives up-front licensing fees yet delivers payback through reduced external-consultant spend and fewer regulatory fines. While regional harmonization efforts such as Basel III offer partial convergence, new country-specific regimes like France's Sapin II or Germany's Supply-Chain Act continue to proliferate, keeping cost pressures acute over the long term.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Cyber-Insurance Underwriting Requirements

- Expansion of ESG Reporting Mandates

- Shortage of In-House GRC Domain Expertise

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software retained a 71.65% revenue share in 2025 thanks to enterprise preference for integrated suites that consolidate risk, audit, privacy, and ESG modules. Yet services posted the fastest expected expansion at a 12.98% CAGR through 2031, underscoring a market shift toward outcome-based engagements that fuse technology enablement with subject-matter guidance. Managed service providers deploy platform accelerators, map controls to regional regulations, and operate continuous monitoring centers on behalf of clients with limited in-house staff. This hybrid delivery approach improves time-to-value for mid-sized buyers and shortens payback periods for large multinationals that must roll out across dozens of jurisdictions simultaneously. The Governance, Risk, and Compliance (GRC) Software market size for services is projected to climb steadily as vendors package advisory, configuration, and run-time operations into subscription bundles. Enhanced post-deployment analytics that benchmark control maturity across peer cohorts create cross-sell pathways for consulting arms eager to monetize insights through remediation roadmaps.

Platform suppliers are enriching software with AI-aided control mapping and natural-language policy ingestion, decreasing the manual effort requirement for baseline deployment. They also expose open APIs to facilitate ecosystem integrations with cyber range testing, e-discovery, and low-code workflow tools. This extensibility attracts partners that extend core capabilities, stimulating indirect revenue streams. Despite automation advances, complex configuration tasks-such as multi-ledger segregation of duties or fine-grained data-sovereignty partitioning-still require specialist input, ensuring that the services revenue pool remains buoyant. Over the forecast window, enterprise buyers are expected to allocate an increasing share of total program budgets to managed capabilities, reinforcing the dual-track expansion of software and services within the Governance, Risk, and Compliance (GRC) Software market.

Cloud deployments accounted for 62.90% of revenue in 2025 and are on course to register a 13.85% CAGR, reflecting enterprise appetite for elastic scalability and collaborative oversight. Continuous controls monitoring delivered as a service allows risk teams to interrogate real-time telemetry drawn from SaaS, infrastructure-as-a-service, and on-premises connectors without the capex burden of local hardware. This architecture underpins faster policy updates, automated compliance evidence collection, and remote audit access, qualities valued by distributed workforces. The Governance, Risk, and Compliance (GRC) Software market size for cloud solutions is forecast to outpace on-premises equivalents as integration blueprints mature and as vendors achieve compliance with stringent data-residency statutes through region-specific tenancy.

On-premises deployments will persist in segments such as defense, public safety, and critical infrastructure, where air-gapped environments remain mandatory. These buyers demand hardened appliances, internal API gateways, and offline reporting capabilities. Nonetheless, vendors are introducing containerized editions that can run either in customer data centers or sovereign clouds, blurring the deployment boundary. Migration roadmaps often begin with non-production workloads in hosted sandboxes before extending to regulated data sets once encryption, key management, and access-segregation standards are validated. Hybrid orchestration consoles provide unified dashboards spanning both modes, ensuring policy consistency and audit traceability across heterogeneous estates. Consequently, the Governance, Risk, and Compliance (GRC) Software market continues its transformation toward a "cloud when possible, on-prem where required" paradigm that balances performance, sovereignty, and cost.

Governance, Risk, and Compliance (GRC) Software Market Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, and On-Premises), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Vertical (BFSI, Healthcare and Life Sciences, Manufacturing, IT and Telecommunications, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa).

Geography Analysis

North America commanded 39.55% of 2025 revenue, underpinned by mature regulatory frameworks, deep cyber-insurance penetration, and a high incidence of shareholder litigation that drives board accountability. Federal agencies now expect near-real-time breach notification, compelling firms to adopt continuous monitoring and automated evidence management embedded in leading Governance, Risk, and Compliance (GRC) Software market platforms. Consolidation among technology and consulting providers has also accelerated regional uptake by offering bundled advisory plus SaaS subscriptions that streamline procurement cycles.

Europe maintains a structurally large user base due to pioneering legislation such as GDPR and the upcoming EU AI Act, which extends accountability to algorithmic transparency and lifecycle monitoring. Banks, insurers, and energy operators must now submit Digital Operational Resilience Act self-assessments, creating fresh demand for scenario-testing engines that model ICT failure propagation. The Governance, Risk, and Compliance (GRC) Software market share associated with European buyers is therefore reinforced by policy activism that stresses both consumer protection and systemic stability. Vendors differentiate through localized data-processing zones, multilingual policy libraries, and in-platform cross-border data transfer checks that align with Schrems II requirements.

Asia-Pacific is projected to achieve a 15.1% CAGR, the highest globally, fueled by rapid digitization, fintech innovation, and expanding carbon-trading schemes. Governments across China, Japan, Korea, and Singapore have launched sustainability disclosure standards that mirror, yet diverge from, European rules, prompting multinationals to favor configurable platforms capable of addressing multiple frameworks in parallel. Regional SMEs increasingly adopt pay-as-you-grow pricing to meet stringent supplier-qualification metrics imposed by global brands, funneling incremental volume into the Governance, Risk, and Compliance (GRC) Software market. Meanwhile, Latin America, the Middle East, and Africa are at earlier stages of adoption but display rising interest as foreign direct investors require documented governance controls before releasing capital.

- IBM Corporation

- SAP SE

- Oracle Corporation

- SAS Institute Inc.

- ServiceNow, Inc.

- Wolters Kluwer N.V. (Enablon)

- Thomson Reuters Corporation

- NAVEX Global, Inc.

- MetricStream, Inc.

- Diligent Corporation

- Riskonnect, Inc.

- Archer Technologies LLC (RSA)

- LogicGate, Inc.

- OneTrust, LLC

- Workiva Inc.

- Galvanize (A Diligent Company)

- Mitratech Holdings Inc.

- Ideagen PLC

- Sword GRC Limited

- SAI Global Pty Limited

- LogicManager, Inc.

- Quantivate, LLC

- ProcessGene Ltd.

- Continuity Logic, LLC

- RiskWatch International, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Intensifying global data-privacy regulations

- 4.2.2 Proliferation of cloud-native applications

- 4.2.3 Surge in cyber-insurance underwriting requirements

- 4.2.4 Expansion of ESG reporting mandates

- 4.2.5 AI-driven predictive analytics adoption in risk management

- 4.2.6 Board-level demand for "continuous controls monitoring"

- 4.3 Market Restraints

- 4.3.1 Complexity and cost of multi-jurisdictional compliance

- 4.3.2 Shortage of in-house GRC domain expertise

- 4.3.3 Regulatory uncertainty around AI governance

- 4.3.4 Vendor lock-in concerns in integrated suites

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises (SMEs)

- 5.4 By Vertical

- 5.4.1 Banking, Financial Services and Insurance (BFSI)

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Manufacturing

- 5.4.4 IT and Telecommunications

- 5.4.5 Government and Public Sector

- 5.4.6 Energy and Utilities

- 5.4.7 Retail and Consumer Goods

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 SAP SE

- 6.4.3 Oracle Corporation

- 6.4.4 SAS Institute Inc.

- 6.4.5 ServiceNow, Inc.

- 6.4.6 Wolters Kluwer N.V. (Enablon)

- 6.4.7 Thomson Reuters Corporation

- 6.4.8 NAVEX Global, Inc.

- 6.4.9 MetricStream, Inc.

- 6.4.10 Diligent Corporation

- 6.4.11 Riskonnect, Inc.

- 6.4.12 Archer Technologies LLC (RSA)

- 6.4.13 LogicGate, Inc.

- 6.4.14 OneTrust, LLC

- 6.4.15 Workiva Inc.

- 6.4.16 Galvanize (A Diligent Company)

- 6.4.17 Mitratech Holdings Inc.

- 6.4.18 Ideagen PLC

- 6.4.19 Sword GRC Limited

- 6.4.20 SAI Global Pty Limited

- 6.4.21 LogicManager, Inc.

- 6.4.22 Quantivate, LLC

- 6.4.23 ProcessGene Ltd.

- 6.4.24 Continuity Logic, LLC

- 6.4.25 RiskWatch International, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

導航最佳化工具 - 2026 年至 2032 年全球市場佔有率和排名、總收入和需求預測

導航最佳化工具 - 2026 年至 2032 年全球市場佔有率和排名、總收入和需求預測 2026-2030年全球市場最佳化與詐欺預防技術市場

2026-2030年全球市場最佳化與詐欺預防技術市場 SEO軟體市場:按組件、部署類型、公司規模和產業分類-2026-2032年全球市場預測

SEO軟體市場:按組件、部署類型、公司規模和產業分類-2026-2032年全球市場預測 2026年全球搜尋引擎最佳化(SEO)工具市場報告2026年全球線上市場最佳化工具市場報告

2026年全球搜尋引擎最佳化(SEO)工具市場報告2026年全球線上市場最佳化工具市場報告 SEO軟體市場規模、佔有率和成長分析(按行銷類型、公司規模、部署類型和地區分類)-2026-2033年產業預測

SEO軟體市場規模、佔有率和成長分析(按行銷類型、公司規模、部署類型和地區分類)-2026-2033年產業預測 本地SEO軟體市場規模、佔有率和成長分析(按公司規模、功能、部署模式、最終用戶和地區分類)-2026-2033年產業預測

本地SEO軟體市場規模、佔有率和成長分析(按公司規模、功能、部署模式、最終用戶和地區分類)-2026-2033年產業預測 全球SEO軟體市場

全球SEO軟體市場 本地 SEO 軟體市場報告:趨勢、預測和競爭分析(至 2031 年)

本地 SEO 軟體市場報告:趨勢、預測和競爭分析(至 2031 年) 全球 SEO 軟體市場規模研究(按企業規模、部署、類型和區域預測 2022-2032)

全球 SEO 軟體市場規模研究(按企業規模、部署、類型和區域預測 2022-2032)