|

市場調查報告書

商品編碼

2034972

日本農藥市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Japan Pesticides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

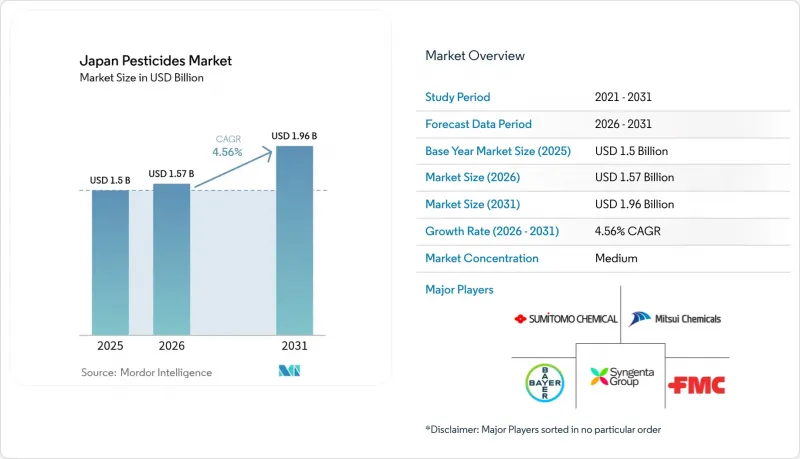

日本農藥市場預計將從 2025 年的 15 億美元成長到 2026 年的 15.7 億美元,然後從 2026 年到 2031 年以 4.56% 的複合年成長率成長,到 2031 年達到 19.6 億美元。

該預測表明,成熟的農業部門正穩步向數據驅動、低殘留解決方案、精準噴灑系統以及生物活性成分的廣泛應用轉型。這項複合年成長率受多種因素共同驅動,包括政府為降低農藥風險而獎勵、氣候變遷加劇病蟲害壓力、農業勞動力快速老化並採用省力技術,以及微膠囊化和無人機相容配方方面的持續創新。隨著本地需求趨於穩定,競爭策略正轉向產品組合多元化和跨境擴張,而原料短缺暴露了對進口材料的依賴,因此供應鏈韌性已成為經營團隊的首要任務。

日本農藥市場的趨勢與洞察

政府在永續食品方面的努力和政策

日本的「綠色策略」要求到2050年將風險加權化學農藥的使用量減少50%,並累計2.2683兆日圓(約151億美元)津貼那些將合成農藥使用量減半的農民。透過直接補貼、加快低劑量活性成分的核准以及標籤獎勵等一系列舉措,日本農藥市場正朝著提高單位面積農藥功效和更廣泛地使用生物防治劑的方向發展。符合這些指導方針的供應商能夠獲得優先註冊,而出口型企業則利用日本的高標準在國際市場上脫穎而出。這項政策壓力也加速了低劑量配方(既能滿足殘留限量要求又能維持產量)的研究,這也是日本國內創新者關注的重點。

氣候變遷導致害蟲危害加劇

天氣波動加劇了遷徙性害蟲的湧入。粉蝨的情況尤其顯著,它們擴大借助有利的風向抵達九州地區。這種現象縮短了最佳噴藥期,迫使農民使用大面積殺蟲劑並進行連續噴灑,推高了日本農藥市場的需求。高解析度的S-18氣候模型資料能夠實現區域性的產品定位,使生產者能夠將預測性害蟲分析整合到其諮詢平台中,從而贏得農民的信任。

嚴格的註冊和最大殘留限量合規時間表

日本厚生勞動省將白菜中滅多威的殘留基準值從0.7毫克/公斤降至0.5毫克/公斤,並於2024年新增141種物質納入監管審查範圍。這些變化增加了毒性測試的成本,延緩了產品上市,給日本農業化學品市場中小規模的註冊農藥企業帶來了沉重壓力。為因應這些挑戰,各公司正在其全球子公司之間共用數據,並優先採用符合日本和歐盟法規的兩用化學品,從而分攤申請文件的成本。

細分市場分析

到2025年,合成農藥在日本農藥市場仍將佔70.40%的佔有率,這主要得益於其顯著的有效性、易於儲存以及廣譜防治等優勢,這些優勢尤其受到老齡化農民的青睞。生物基產品正以8.75%的複合年成長率成長,這主要得益於市場放鬆管制和消費者需求的推動。由於農民可以透過減少50%的合成農藥使用來獲得直接補貼,生物來源替代品的吸引力日益增強。同時,跨國公司正從本土新創公司獲得微生物活性物質的授權,以避免對合成農藥的依賴。

生物基農藥提倡採用低劑量化學物質和生物製劑結合的複合配方,在有效控制病蟲害的同時降低毒性負荷指數。這種混合策略使供應商能夠在不犧牲產量的前提下實現「綠色」目標。農林水產省(MAFF)的「永續糧食系統策略」法規結構為生物來源產品提供優惠待遇,包括加速註冊流程和提供財政獎勵,這正在重塑合成農藥和生物基農藥之間的競爭格局。

預計到2025年,除草劑將佔銷售額的44.95%,因為不願實現農田機械化的稻農開始採用只需一次施用即可控制雜草的產品。然而,除草劑抗藥性的風險日益增加,這推動了殺蟎劑和殺菌劑的創新。受溫室種植的番茄和黃瓜中爆發的紅蜘蛛疫情的推動,殺蟎劑的年複合成長率高達8.36%。雖然由於溫室種植的擴張,殺菌劑的需求保持穩定,但殺蟲劑正面臨著來自綜合蟲害管理(IPM)的推廣和替代生物防治方法的興起的壓力。殺線蟲劑是針對高價值作物和需要控制土壤傳播害蟲的保護性栽培系統而專門開發的細分市場。

除草劑產業正面臨日益嚴峻的抗藥性挑戰。包括台灣稗草在內的多種雜草正在對1類和2類除草劑產生抗藥性,因此需要採取輪換策略並開發新型活性成分。庫邁化學的吡唑磺隆類除草劑在2013年至2023年間實現了26%的複合年成長率,顯示市場對高效新型化學品的需求旺盛。國家農業食品研究機構針對入侵物種開發的系統性除草劑控制方法,體現了除草劑施用技術和抗藥性管理策略的持續創新。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 政府在永續食品方面的努力和政策

- 氣候變遷導致害蟲危害加劇

- 農業人口老化加速了省力除草劑的普及應用。

- 生物基農藥的迅速擴散

- 利用無人機進行精準噴灑的擴展

- 保護性栽培設施的擴張推高了對殺菌劑的需求。

- 市場限制因素

- 嚴格的註冊和最大殘留限量(MRL)合規期限

- 加強消費者對化學殘留物的監督

- 抗除草劑雜草數量增加

- 基本醫藥輔料間歇性供不應求

- 監理情勢

- 噴塗和配方技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 按原產地

- 合成

- 生物基

- 按類型

- 除草劑

- 消毒劑

- 殺蟲劑

- 殺蟎劑

- 殺線蟲劑

- 其他類型(滅鼠劑、消毒劑等)

- 配方

- 濃縮液

- 可濕性粉

- 顆粒

- 微膠囊化

- 懸浮濃縮物

- 按作物類型

- 穀物和穀類

- 豆類和油籽

- 水果和蔬菜

- 經濟作物

- 觀賞作物

- 其他用途(草坪維護、林業育苗等)

- 透過使用

- 葉面噴布

- 土壤處理

- 種子處理

- 化學

- 空中噴灑/無人機噴灑

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Sumitomo Chemical Co., Ltd.

- Syngenta CropProtection AG(Syngenta Group)

- Bayer AG

- Mitsui Chemicals Agro, Inc.(Mitsui Chemicals, Inc.)

- BASF SE

- FMC Corporation

- Nissan Chemical Corporation

- Nihon Nohyaku Co., Ltd(ADEKA Corporation)

- Kumiai Chemical Industry Co., Ltd

- UPL Limited

- OAT Agrio Co., Ltd

- Corteva Agriscience

- Hokko Chemical Industry Co., Ltd

- Nippon Soda Co., Ltd

- Ishihara Sangyo Kaisha, Ltd

第7章 市場機會與未來展望

The Japan pesticides market size is expected to grow from USD 1.5 billion in 2025 to USD 1.57 billion in 2026 and is forecast to reach USD 1.96 billion by 2031 at 4.56% CAGR over 2026-2031.

This projection highlights the steady transition of a mature farming sector toward data-driven, low-residue solutions, precision delivery systems, and increased deployment of biologically active ingredients. Behind the headline CAGR lies a confluence of drivers: government incentives that reward pesticide-risk reduction, climate variability that elevates pest pressure, a rapidly aging farming population that embraces labor-saving technologies, and continuous innovation in microencapsulation and drone-ready formulations. Competitive strategies are shifting toward portfolio diversification and cross-border expansion as local demand plateaus, while supply-chain resilience has become a boardroom priority after ingredient shortages exposed dependencies on imported raw materials.

Japan Pesticides Market Trends and Insights

Government initiatives and policies for Sustainable Food

Japan's MIDORI Strategy mandates a 50% reduction in risk-weighted chemical pesticide use by 2050 and allocates JPY 2.2683 trillion (USD 15.1 billion) for subsidizing farmers who halve synthetic applications. The combination of direct payments, expedited approvals for low-dose actives, and labeling incentives is pushing the Japan pesticides market toward higher efficacy per hectare and wider use of biocontrol agents. Suppliers that align portfolios with these guidelines are securing preferential registration, while export-oriented firms leverage Japan's elevated standards to differentiate in international markets. The policy pressure also accelerates research into micro-dosed formulations that maintain yield while satisfying residue targets, a focal point for domestic innovators.

Rising pest pressure driven by climate volatility

Weather volatility is intensifying migrant pest influx, notably the brown planthopper that now reaches Kyushu under favorable wind currents more frequently. The phenomenon compresses spray windows and forces farmers to adopt broad-spectrum or sequential applications, strengthening demand within the Japan pesticides market. High-resolution S-18 climate modelling data enable region-tailored product positioning, while manufacturers incorporate predictive pest analytics into advisory platforms to secure growers' loyalty.

Stringent registration and MRL compliance timelines

The Ministry of Health, Labour and Welfare cut cabbage methomyl residue limits from 0.7 mg/kg to 0.5 mg/kg, and 141 new substances entered regulatory scrutiny in 2024. These shifts raise toxicology study costs, delay product launches, and weigh on smaller registrants in the Japan pesticides market. Companies respond by pooling data across global subsidiaries and prioritizing dual-use chemistries designed for Japan and European Union alignment to amortize dossiers.

Other drivers and restraints analyzed in the detailed report include:

- Accelerated adoption of labor-saving herbicides by aging farmers

- Growth of protected horticulture complexes boosting fungicide demand

- Heightened consumer scrutiny of chemical residues

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Synthetic-based pesticides retained a 70.40% grip on the Japan pesticides market share in 2025 due to proven efficacy, ease of storage, and broad-spectrum performance valued by aging growers. Bio-based products are climbing at a 8.75% CAGR on the back of regulatory accelerators and consumer pull. Farmers cutting synthetic volume by 50% unlock direct payment eligibility, reinforcing the appeal of biological alternatives. At the same time, multinationals are licensing microbial actives from local startups to hedge against synthetic dependency.

The bio-based pesticides foster co-formulations that blend low-dose chemistry with living organisms, delivering robust control at reduced toxic-load indices. This hybrid strategy positions suppliers to satisfy MIDORI targets without compromising yield. Regulatory frameworks under MAFF's Strategy for Sustainable Food Systems provide preferential treatment for biological products, including expedited registration processes and financial incentives that are reshaping competitive dynamics between synthetic and bio-based segments.

Herbicides secured 44.95% of sales in 2025 as mechanization-averse rice farmers adopted single-shot weed knockdown products. Yet herbicide resistance is a mounting risk that propels miticide and fungicide innovation. Miticides are accelerating at 8.36% CAGR, fueled by spider-mite outbreaks in greenhouse tomatoes and cucumbers. Fungicides maintain steady demand through greenhouse cultivation expansion, while insecticides face pressure from integrated pest management adoption and biological control alternatives. Nematicides represent a specialized segment serving high-value crops and protected cultivation systems requiring soil-borne pest control.

The herbicide segment confronts escalating resistance challenges, with multiple weed species, including Taiwan barnyardgrass, developing resistance to Groups 1 and 2 herbicides, necessitating rotation strategies and novel active ingredients. Kumiai Chemical's pyroxasulfone herbicide demonstrated 26% compound annual growth from 2013 to 2023, indicating market appetite for effective new chemistries. The National Agriculture and Food Research Organization's development of systematic herbicide control methods for invasive species demonstrates ongoing innovation in application techniques and resistance management strategies.

The Japan Pesticides Market Report is Segmented by Origin (Synthetic, and Bio-Based), Type (Herbicide, Fungicide, Insecticide, Miticide, and More), Formulation (Liquid Concentrates, Wettable Powders, and More), Crop Type (Grains and Cereals, Pulses and Oilseeds, and More), and Application (Foliar Spray, Soil Treatment, Seed Treatment, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Sumitomo Chemical Co., Ltd.

- Syngenta CropProtection AG (Syngenta Group)

- Bayer AG

- Mitsui Chemicals Agro, Inc. (Mitsui Chemicals, Inc.)

- BASF SE

- FMC Corporation

- Nissan Chemical Corporation

- Nihon Nohyaku Co., Ltd (ADEKA Corporation)

- Kumiai Chemical Industry Co., Ltd

- UPL Limited

- OAT Agrio Co., Ltd

- Corteva Agriscience

- Hokko Chemical Industry Co., Ltd

- Nippon Soda Co., Ltd

- Ishihara Sangyo Kaisha, Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government initiatives and policies for Sustainable Food

- 4.2.2 Rising pest pressure driven by climate volatility

- 4.2.3 Accelerated adoption of labor-saving herbicides by aging farmers

- 4.2.4 Rapid uptake of bio-based pesticides

- 4.2.5 Expansion of drone-enabled precision spraying

- 4.2.6 Growth of protected horticulture complexes boosting fungicide demand

- 4.3 Market Restraints

- 4.3.1 Stringent registration and MRL compliance timelines

- 4.3.2 Heightened consumer scrutiny of chemical residues

- 4.3.3 Escalating herbicide-resistant weed populations

- 4.3.4 Intermittent shortages of critical formulation additives

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook in Application and Formulation

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Origin

- 5.1.1 Synthetic

- 5.1.2 Bio-based

- 5.2 By Type

- 5.2.1 Herbicide

- 5.2.2 Fungicide

- 5.2.3 Insecticide

- 5.2.4 Miticide

- 5.2.5 Nematicide

- 5.2.6 Other Types (Rodenticide, Bactericide, etc.)

- 5.3 By Formulation

- 5.3.1 Liquid Concentrates

- 5.3.2 Wettable Powders

- 5.3.3 Granules

- 5.3.4 Microencapsulated

- 5.3.5 Suspension Concentrates

- 5.4 By Crop type

- 5.4.1 Grains and Cereals

- 5.4.2 Pulses and Oilseeds

- 5.4.3 Fruits and Vegetables

- 5.4.4 Commercial Crops

- 5.4.5 Ornamental Crops

- 5.4.6 Other Applications (Turfgrass Management, Forestry Seedlings, etc.)

- 5.5 By Application

- 5.5.1 Foliar Spray

- 5.5.2 Soil Treatment

- 5.5.3 Seed Treatment

- 5.5.4 Chemigation

- 5.5.5 Aerial / Drone Application

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Sumitomo Chemical Co., Ltd.

- 6.4.2 Syngenta CropProtection AG (Syngenta Group)

- 6.4.3 Bayer AG

- 6.4.4 Mitsui Chemicals Agro, Inc. (Mitsui Chemicals, Inc.)

- 6.4.5 BASF SE

- 6.4.6 FMC Corporation

- 6.4.7 Nissan Chemical Corporation

- 6.4.8 Nihon Nohyaku Co., Ltd (ADEKA Corporation)

- 6.4.9 Kumiai Chemical Industry Co., Ltd

- 6.4.10 UPL Limited

- 6.4.11 OAT Agrio Co., Ltd

- 6.4.12 Corteva Agriscience

- 6.4.13 Hokko Chemical Industry Co., Ltd

- 6.4.14 Nippon Soda Co., Ltd

- 6.4.15 Ishihara Sangyo Kaisha, Ltd

7 Market Opportunities and Future Outlook

緩釋和控釋農藥市場-全球產業規模、佔有率、趨勢、機會和預測:按農藥類型、應用、地區和競爭格局分類,2021-2031年農業化學品市場-全球產業規模、佔有率、趨勢、機會和預測:按配方類型、產品類型、成分、類型、應用、地區和競爭格局分類,2021-2031年

緩釋和控釋農藥市場-全球產業規模、佔有率、趨勢、機會和預測:按農藥類型、應用、地區和競爭格局分類,2021-2031年農業化學品市場-全球產業規模、佔有率、趨勢、機會和預測:按配方類型、產品類型、成分、類型、應用、地區和競爭格局分類,2021-2031年 Ethiprole市場:產品類型、劑型、作物類型、應用方法、用途、最終用途-2026-2032年全球市場預測Famoxadone市場:全球市場按產品形式、劑量、分銷管道、應用和最終用戶分類的預測——2026-2032年農藥市場:2026年至2032年全球市場預測(按類型、來源、配方、施用方法、作物類型和銷售管道)

Ethiprole市場:產品類型、劑型、作物類型、應用方法、用途、最終用途-2026-2032年全球市場預測Famoxadone市場:全球市場按產品形式、劑量、分銷管道、應用和最終用戶分類的預測——2026-2032年農藥市場:2026年至2032年全球市場預測(按類型、來源、配方、施用方法、作物類型和銷售管道) 2026-2030年全球農業殺蟲劑市場

2026-2030年全球農業殺蟲劑市場 新菸鹼類殺蟲劑全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

新菸鹼類殺蟲劑全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球有機磷農藥市場報告2026年全球特種農藥市場報告2026年全球農業化學助劑市場報告

2026年全球有機磷農藥市場報告2026年全球特種農藥市場報告2026年全球農業化學助劑市場報告