|

市場調查報告書

商品編碼

1940909

美國屋頂材料市場:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)United States Roofing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

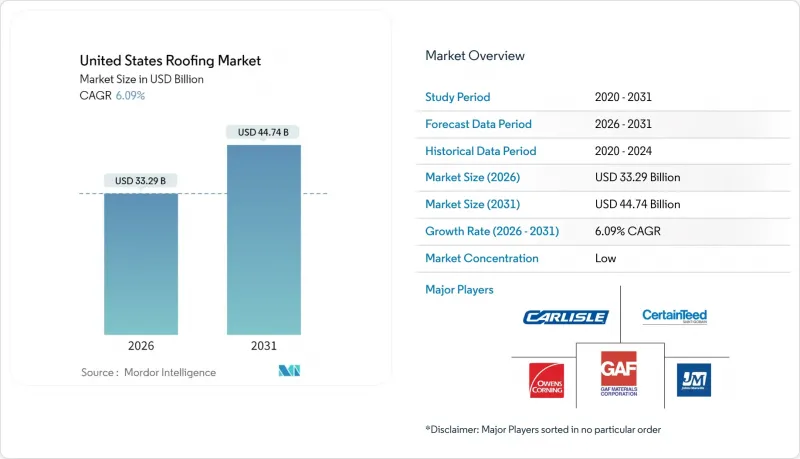

據估計,到 2026 年,美國屋頂市場價值將達到 332.9 億美元,高於 2025 年的 313.8 億美元。

預計到 2031 年,該市場規模將達到 447.4 億美元,2026 年至 2031 年的複合年成長率為 6.09%。

美國老舊住宅存量、頻繁發生的極端天氣事件以及聯邦政府的節能獎勵,共同支撐著這一行業的穩定擴張。屋頂更換佔年度安裝總量的五分之四以上,確保了即使新建築項目放緩,該行業也能擁有可預測的需求基礎。對於商業計劃,平屋頂和低坡度屋頂系統佔據主導地位,因為膜材技術能夠滿足現代建築規範的能源性能要求。同時,由於業主對耐用且適用於太陽能的屋頂表面的需求,金屬和TPO產品的市場佔有率正在超過其他材料。分銷整合推動了家得寶和QXO等公司達成的數十億美元交易,並將人工智慧工具引入供應鏈,為大型平台鋪平了道路,使其能夠為承包商提供更快捷的交貨和客製化的產品服務。

美國屋頂市場趨勢與分析

住宅存量維修週期將推動持續的需求。

每年超過80%的屋頂工程需求源自於屋頂更換,而美國住宅的平均房齡已接近40年。強風的侵襲加速了瀝青瓦的劣化,現場研究表明,瀝青瓦的使用壽命通常只有10年。美國東北部和中西部地區住宅了大量戰後建造的房屋,這些住宅目前正處於維修階段,這使得承包商無論經濟狀況如何波動都能獲得穩定的訂單。抵押房屋抵押貸款利率的下降進一步推動了這一趨勢,使業主能夠將部分房產價值用於維修預算。無人機輔助的房屋狀況評估可以縮短檢查時間並產生客觀的資料集,從而加快保險理賠速度,並進一步最佳化計劃流程。

與氣候相關的風暴災害修復將重塑市場動態

2024年,美國與屋頂相關的保險理賠金額超過300億美元。對流風暴造成的財產損失高達570億美元,幾乎是去年的兩倍。德克薩斯州、科羅拉多以及鄰近的龍捲風走廊各州發生的此類事件比例不斷上升,非危險性風災和冰雹災害的索賠比例從2022年的17%上升到2024年的25%。這種反覆發生的災害將縮短屋頂更換週期,導致本已緊張的勞動市場需求激增。目前,保險公司正在降低15至20年以上屋頂的承保範圍,並為4級抗衝擊等級的屋頂系統提供保費折扣,引導客戶選擇高成本的金屬和複合材料產品。

技術純熟勞工短缺限制了成長潛力

到2025年,建設產業需要新增50.1萬名工人,然而五分之一的屋頂工人已經超過55歲。艱苦的工作條件導致屋頂工人的離職率高於其他行業。儘管美國國家屋頂承包商協會(NRCA)擴大了TRAC課程,克萊姆森大學也斥資100萬美元建立了屋頂產業中心,但學徒畢業生仍無法滿足市場需求。勞動力短缺推高了建築成本,導致計劃延期,並限制了承包商向風暴災區擴張的速度。私募股權支持的平台正在積極招聘,但小規模承包商在工資和福利方面無法與之競爭,導致人才缺口進一步擴大。

細分市場分析

預計到2025年,住宅應用將占美國屋頂市場收入的59.12%,並在2031年之前以7.18%的複合年成長率成長,這主要得益於老舊住宅和風暴造成的屋頂更換需求。可預測的更換週期為安裝商提供了穩定的收入基礎,而第25C條稅額扣抵鼓勵業主升級到節能型屋頂材料和金屬板,從而有助於提升房產價值。保險公司也正在鼓勵使用抗衝擊系統,這進一步縮短了更換週期。

受企業淨零排放目標和電子商務擴張的推動,倉庫建設熱潮帶動商業需求持續成長。低坡度防水捲材及其太陽能適用表面正吸引尋求降低營運成本的設施管理人員的關注,而聯邦基礎設施資金也正投入學校、交通樞紐和公共設施建設。儘管住宅市場仍然是美國屋頂市場的支柱,但大型全國性承包商正擴大調整其業務組合,增加各類商業計劃,以對沖單戶住宅需求的區域性波動風險。

到2025年,維修將占美國屋頂市場的81.65%,反映出建築存量趨於成熟以及風暴災害保險賠償頻繁。無人機影像、人工智慧輔助的狀況評估以及簡化的保險入口網站正在縮短理賠週期,加快風暴過後屋頂的拆除速度,促使承包商將人力和資源集中投入到專門負責屋頂翻新的快速響應團隊中。

雖然新增安裝量目前佔比不高,但隨著陽光地帶住宅量增加以及資料中心建設在區域性城市蓬勃發展,預計其年複合成長率將達到7.52%。現代建築規範強制要求使用反光和耐火材料,這推高了單位成本。建築商與經銷商之間的合作使得現場材料儲存成為可能,最大限度地減少了盜竊和天氣造成的延誤,即使在人手不足的情況下,也促進了相關技術的應用。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 住宅存量維修週期(佔需求的 80% 以上)

- 氣候變遷導致的風暴災害修復和保險費用

- 聯邦和州政府的節能獎勵(IRA稅額扣抵,第 24 章)

- 大型零售商進軍專業經銷領域(家得寶與SRS的合作)

- 人工智慧驅動的航空數據定價和保險理賠處理(Verisk、EagleView)

- 市場限制

- 由於技術純熟勞工短缺,建築成本不斷上漲

- 瀝青和聚合物原料價格波動;

- 假冒仿冒品材料的普遍存在

- 保險收緊:提高免賠額,並將劣化屋頂排除在承保範圍之外

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模及成長預測(價值,單位:十億美元)

- 按行業

- 住宅

- 商業的

- 辦公室和零售設施

- 工業與物流

- 其他

- 基礎設施

- 按安裝類型

- 新安裝

- 更換/維修(屋頂更換)

- 按屋頂類型

- 斜屋頂

- 平屋頂/低坡度屋頂

- 依材料類型

- 改性瀝青

- EPDM橡膠

- 熱塑性聚烯

- PVC膜

- 金屬

- 瓦

- 其他

- 按地區

- 東北

- 中西部

- 東南

- 西

- 西南

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- GAF Materials Corporation

- Owens Corning

- CertainTeed(Saint-Gobain)

- Carlisle Companies Inc.

- Johns Manville(Berkshire Hathaway)

- IKO Industries

- TAMKO Building Products

- Atlas Roofing Corporation

- Beacon Building Products

- ABC Supply Co.

- Holcim Elevate(Firestone Building Products)

- Duro-Last Inc.

- Malarkey Roofing Products

- CentiMark Corporation

- Tecta America

- Flynn Group

- Baker Roofing Company

- IronHead Roofing

- Sika Sarnafil

- MFM Building Products

第7章 市場機會與未來展望

United States Roofing Market market size in 2026 is estimated at USD 33.29 billion, growing from 2025 value of USD 31.38 billion with 2031 projections showing USD 44.74 billion, growing at 6.09% CAGR over 2026-2031.

Renewals triggered by the nation's aging housing stock, the growing frequency of severe weather events, and federal energy-efficiency incentives underpin this steady expansion. Re-roofing activities account for more than four-fifths of annual installation volume, giving the industry a predictable demand foundation even when new construction moderates. Flat and low-slope systems dominate commercial projects because their membrane technologies satisfy modern building-code requirements for energy performance, while metal and TPO products outpace other materials as owners seek durability and solar-ready surfaces. Distribution consolidation, led by Home Depot's and QXO's multibillion-dollar deals, ushers artificial-intelligence tools into supply chains and positions large platforms to offer contractors faster deliveries and tailored assortments.

United States Roofing Market Trends and Insights

Housing-Stock Re-Roofing Cycle Drives Sustained Demand

More than four-fifths of annual roofing demand comes from re-roofing, and the median U.S. home age is nearing 40 years. Elevated wind exposure accelerates asphalt-shingle degradation, with field studies showing failures as early as 10 years into service life. Concentrated cohorts of post-war homes in the Northeast and Midwest are now simultaneously entering their renewal windows, giving contractors consistent volume regardless of macroeconomic swings. The cycle intensifies when mortgage rates dip, allowing owners to convert equity into upgrade budgets. Drone-based condition assessments shorten inspection times and create objective datasets that speed insurance claims, further smoothing project pipelines.

Climate-Driven Storm Repairs Reshape Market Dynamics

U.S. roof-related claims exceeded USD 30 billion in 2024 as convective storms produced USD 57 billion in property damage, almost double the prior year. Texas, Colorado, and adjacent Tornado Alley states account for a rising share of events, with non-catastrophic wind and hail claims climbing from 17% in 2022 to 25% in 2024. This recurring hazard compresses replacement cycles and pushes demand spikes into already tight labor markets. Insurers now depreciate coverage for roofs older than 15-20 years and offer premium credits for Class 4 impact-rated systems, nudging customers toward higher-cost metal and synthetic products.

Skilled-Labor Shortages Constrain Growth Potential

The construction sector needs 501,000 more workers in 2025, yet 1 in 5 roofers is already over 55 years old. Harsh job-site conditions drive higher turnover than in other trades, and apprenticeship completions lag demand despite NRCA's expanded TRAC curriculum and Clemson's USD 1 million Roofing Industry Center commitment. Labor shortfalls inflate installation costs, extend project backlogs, and limit the pace at which contractors can scale into storm-damaged regions. Private equity-backed platforms recruit aggressively, but smaller shops struggle to match wage offers and benefit packages, widening capacity gaps.

Other drivers and restraints analyzed in the detailed report include:

- Federal Energy Efficiency Incentives Accelerate Premium Adoption

- Retail Distribution Consolidation Transforms Market Access

- Material Price Volatility Pressures Margin Stability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Residential applications generated 59.12% of 2025 revenue for the United States roofing market and are on track for a 7.18% CAGR through 2031 as aging homes collide with storm-driven replacements. Predictable renewal cycles give installers steady baselines, while Section 25C credits persuade owners to upgrade to energy-efficient shingles or metal panels that boost property values. Insurers incentivize impact-rated systems, compressing replacement timelines even further.

Commercial demand gains momentum from corporate net-zero commitments and an e-commerce-fueled warehouse boom. Low-slope membranes with solar-ready surfaces attract facility managers seeking lower operating costs, and federal infrastructure funding channels work to schools, transit centers, and public offices. Although residential still anchors the United States roofing market, large national contractors increasingly balance their portfolios with diversified commercial projects to hedge regional single-family swings.

Replacement undertakings represented 81.65% of the United States roofing market size in 2025, reflecting a mature building inventory and frequent storm damage settlements. Drone imagery, AI-assisted condition scoring, and streamlined insurance portals shorten claim cycles, driving faster roof tear-offs once weather events hit. Contractors, therefore, allocate personnel and inventory toward ready-response teams that specialize in reroof projects.

New installations account for a smaller share yet are forecast to grow 7.52% CAGR as migration pushes housing starts in the Sun Belt and data-center builds sweep secondary metros. Modern codes mandate reflective or fire-rated coverings, often elevating unit costs. Partnerships between builders and distributors enable job-site staging that minimizes theft and weather delays, reinforcing adoption even when labor remains tight.

The United States Roofing Market Report is Segmented by Sector (Residential, Commercial, Infrastructure), by Installation Type (New Installation, Replacement/Renovation), by Roofing Type (Slope Roof, Flat/Low-Slope Roof), by Material Type (Modified Bitumen, EPDM Rubber, TPO, PVC Membrane, and More), and by Geography (Northeast, Midwest, Southeast, West, Southwest). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- GAF Materials Corporation

- Owens Corning

- CertainTeed (Saint-Gobain)

- Carlisle Companies Inc.

- Johns Manville (Berkshire Hathaway)

- IKO Industries

- TAMKO Building Products

- Atlas Roofing Corporation

- Beacon Building Products

- ABC Supply Co.

- Holcim Elevate (Firestone Building Products)

- Duro-Last Inc.

- Malarkey Roofing Products

- CentiMark Corporation

- Tecta America

- Flynn Group

- Baker Roofing Company

- IronHead Roofing

- Sika Sarnafil

- MFM Building Products

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Housing-stock re-roofing cycle (>=80 % of demand)

- 4.2.2 Climate-driven storm repairs & insurance spend

- 4.2.3 Federal/State energy-efficiency incentives (IRA tax credits, Title 24)

- 4.2.4 Retail giant entry into specialty distribution (Home Depot-SRS deal)

- 4.2.5 AI-enabled aerial data pricing/claims (Verisk, EagleView)

- 4.3 Market Restraints

- 4.3.1 Skilled-labor shortages elevating installation costs

- 4.3.2 Volatility in asphalt & polymer feedstock prices

- 4.3.3 Proliferation of counterfeit/sub-spec materials

- 4.3.4 Insurance tightening: higher deductibles & roof-age exclusions

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Sector

- 5.1.1 Residential

- 5.1.2 Commercial

- 5.1.2.1 Offices and Retail

- 5.1.2.2 Industrial and Logistics

- 5.1.2.3 Others

- 5.1.3 Infrastructure

- 5.2 By Installation Type

- 5.2.1 New Installation

- 5.2.2 Replacement / Renovation (Re-Roofing)

- 5.3 By Roofing Type

- 5.3.1 Slope Roof

- 5.3.2 Flat / Low-Slope Roof

- 5.4 By Material Type

- 5.4.1 Modified Bitumen

- 5.4.2 EPDM Rubber

- 5.4.3 Thermoplastic Polyolefin

- 5.4.4 PVC Membrane

- 5.4.5 Metals

- 5.4.6 Tiles

- 5.4.7 Others

- 5.5 By Geography

- 5.5.1 Northeast

- 5.5.2 Midwest

- 5.5.3 Southeast

- 5.5.4 West

- 5.5.5 Southwest

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 GAF Materials Corporation

- 6.4.2 Owens Corning

- 6.4.3 CertainTeed (Saint-Gobain)

- 6.4.4 Carlisle Companies Inc.

- 6.4.5 Johns Manville (Berkshire Hathaway)

- 6.4.6 IKO Industries

- 6.4.7 TAMKO Building Products

- 6.4.8 Atlas Roofing Corporation

- 6.4.9 Beacon Building Products

- 6.4.10 ABC Supply Co.

- 6.4.11 Holcim Elevate (Firestone Building Products)

- 6.4.12 Duro-Last Inc.

- 6.4.13 Malarkey Roofing Products

- 6.4.14 CentiMark Corporation

- 6.4.15 Tecta America

- 6.4.16 Flynn Group

- 6.4.17 Baker Roofing Company

- 6.4.18 IronHead Roofing

- 6.4.19 Sika Sarnafil

- 6.4.20 MFM Building Products

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

2026年全球低坡度住宅屋頂市場報告2026年全球屋頂材料市場報告

2026年全球低坡度住宅屋頂市場報告2026年全球屋頂材料市場報告 黏土瓦市場:依產品類型、應用、銷售管道和地區分類

黏土瓦市場:依產品類型、應用、銷售管道和地區分類 綠色和藍色屋頂市場:按屋頂類型、組件、系統設計、安裝類型、屋頂結構、應用和用例分類——2026-2032年全球預測非住宅建築屋面紗織物市場:按產品、材料、安裝類型、應用、最終用途和分銷管道分類-2026-2032年全球預測屋頂通風產品市場:依產品類型、安裝類型、材質類型、最終用戶、通路分類,全球預測(2026-2032)

綠色和藍色屋頂市場:按屋頂類型、組件、系統設計、安裝類型、屋頂結構、應用和用例分類——2026-2032年全球預測非住宅建築屋面紗織物市場:按產品、材料、安裝類型、應用、最終用途和分銷管道分類-2026-2032年全球預測屋頂通風產品市場:依產品類型、安裝類型、材質類型、最終用戶、通路分類,全球預測(2026-2032) 全球屋頂材料市場規模、佔有率、趨勢及成長分析報告(2026-2034)2026年全球複合塑膠屋頂瓦市場報告

全球屋頂材料市場規模、佔有率、趨勢及成長分析報告(2026-2034)2026年全球複合塑膠屋頂瓦市場報告 屋頂材料市場-全球產業規模、佔有率、趨勢、機會、預測:依產品類型、應用、地區、競爭格局分類,2021-2031年屋頂系統市場 - 全球產業規模、佔有率、趨勢、機會及預測(依材料、產品、建築類型、最終用戶產業、地區及競爭格局分類,2021-2031年)

屋頂材料市場-全球產業規模、佔有率、趨勢、機會、預測:依產品類型、應用、地區、競爭格局分類,2021-2031年屋頂系統市場 - 全球產業規模、佔有率、趨勢、機會及預測(依材料、產品、建築類型、最終用戶產業、地區及競爭格局分類,2021-2031年)