|

市場調查報告書

商品編碼

1940879

鉭電容器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Tantalum Capacitors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

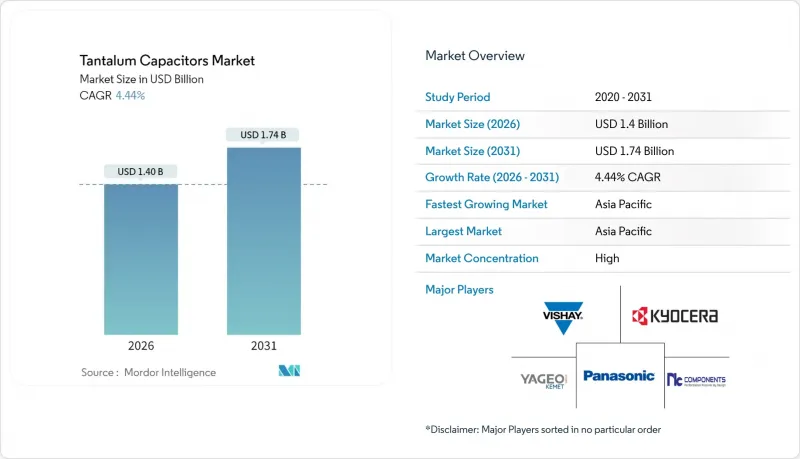

鉭電容器市場預計將從 2025 年的 13.4 億美元成長到 2026 年的 14 億美元,預計到 2031 年將達到 17.4 億美元,2026 年至 2031 年的複合年成長率為 4.44%。

儘管成本壓力持續存在,但對高電容密度、溫度穩定性和長期可靠性的強勁需求,使鉭電容器市場在關鍵電子設備領域保持了其穩固地位。消費性電子設備的微型化、汽車電氣化的加速、5G基礎設施的擴展以及多層陶瓷電容器(MLCC)供應鏈的中斷,共同推動了鉭電容器市場的穩定成長。同時,關鍵礦產的貿易限制和原物料價格的上漲限制了複合年成長率的預測,並迫使買家尋求多元化的籌資策略。

全球鉭電容器市場趨勢及洞察

電子機器の小型化

隨著基板的縮小,每平方公分的散熱量急劇增加,這使得鉭電容的熱穩定性對於智慧型手機、穿戴式裝置和植入式醫療設備中嵌入的電源管理積體電路至關重要。現代旗艦智慧型手機包含超過1000個電容器,其中鉭電容承擔著關鍵的電源線調節功能,這要求其具有高體積效率和高回流焊接電阻。 OEM藍圖對折疊式和超薄外形尺寸的需求推動了對更小封裝尺寸且不犧牲電容容量的需求,從而保持了鉭電容市場的成長動能。

車用電子設備的普及應用日益廣泛

汽車電氣化正在推動電容器在眾多應用領域的需求,包括驅動逆變器、車載充電器、高級駕駛輔助系統 (ADAS) 和資訊娛樂模組。聚合物鉭電容器的動作溫度範圍為 -40°C 至 +150°C,並具有低等效串聯電阻 (ESR)。在 48V 和新興的 800V 架構中,它們的性能優於陶瓷電容器。 TDK 預測,由於汽車訂單激增導致車輛單價上漲,被動元件市場將在 2025 會計年度實現成長。這些趨勢確保鉭電容器市場與電氣化的長期發展趨勢保持高度一致。

鉭礦價格和供應波動

剛果民主共和國的衝突導致生產中斷,以及小規模礦工被指控有強迫勞動現象,使得原料供應緊張,價格上漲波及電容器物料清單(BOM)成本。 2024年9月,美國對中國鉭進口徵收25%的關稅後,美國鉭消費量大幅下降。這迫使原始設備製造商(OEM)實現採購多元化並重新設計產品,從而限制了鉭電容器在成本敏感型市場的滲透率。

細分市場分析

到2025年,固體聚合物鉭電容器將佔總收入的38.62%,因為原始設備製造商(OEM)優先考慮降低等效串聯電阻(ESR)和提高故障安全性能。鉭電容器市場受益於聚合物的安全故障模式,這種模式消除了與二氧化錳(MnO2)陰極相關的析氧風險。鈮氧化物電容器雖然目前仍屬於小眾市場,但隨著設計人員逐漸規避原料風險,預計到2031年將以5.94%的複合年成長率成長。固體MnO2元件仍將是成本敏感型消費性電子設備的大量選擇,而濕式電解結構將在大容量儲能領域保持其地位。

封裝創新與材料轉型相輔相成。聚合物組件滿足了5G功率放大器和電動車車載充電器對漣波電流的需求,從而鞏固了鉭電容市場。隨著醫療植入和穿戴式感測器追求更小的封裝尺寸,能夠承受超過1000次熱循環的聚合物技術的穩定性將成為關鍵因素。

預計到2025年,表面黏著技術封裝將佔總收入的77.45%,複合年成長率(CAGR)為5.03%,這反映了多層PCB自動化組裝和密度提升的趨勢。由於貼片精度提高,禁區範圍縮小,與表面黏著技術封裝相關的鉭電容市場規模正在擴大。通孔封裝在航太、國防和重工業電路基板領域仍然十分重要,因為在這些領域,機械強度和現場可維護性比封裝形式更為重要。

基板電容器的發展藍圖進一步強化了表面黏著技術的優勢,該技術能夠壓縮Z軸高度並降低功率迴路電感。三星馬達已更新其元件庫,以簡化射頻功率模組的模擬工作流程,從而進一步推動設計採用表面黏著技術鉭電容器。

區域分析

預計到 2025 年,亞太地區將佔全球收入的 44.10%,到 2031 年將以 5.63% 的複合年成長率成長。中國大力發展消費性電子產品,並輔以先進封裝補貼,推動了對被動元件的需求;同時,韓國和台灣正在建立記憶體代工廠基地,這些工廠需要高頻去耦元件。

在北美,由於對中國鉭進口徵收25%的關稅以及美國國防部將於2027年生效的採購法規,供應鏈重組正在進行中。美國本土電容器製造商正迅速認證來自澳洲和巴西的符合道德規範的鉭礦石,以使軍事項目免受衝突地區的影響。這些政策變化在重塑區域需求的同時,也催生了可追溯的美國製造鉭部件的利基需求。

歐洲正優先考慮永續性發展,並推廣採購無衝突認證的鉭。德國一級汽車供應商正與波蘭和捷克的電容器工廠合作,以滿足縮短物流週期和準時生產的需求,從而保護鉭電容器市場免受海運延誤的影響。

世界其他地區正在崛起,成為替代性的原料供應基地。澳洲擁有大規模的硬岩鉭礦礦床,目前正在擴大精煉產能,以符合西方環境、社會和治理(ESG)標準。盧安達正在發展精礦精煉基礎設施,以提高當地的附加價值。巴西米納斯吉拉斯州的計劃將增加礦石供應,並有助於分散全球供應風險。

其他福利:

- Excel格式的市場預測(ME)表

- アナリストサポート(3ヶ月間)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 電子設備小型化

- 車用電子設備的普及應用日益廣泛

- 5G智慧型手機產量激增

- MLCC供應的不確定性使鉭具有優勢。

- 植入式醫療設備的可靠性要求

- 航太和國防關鍵任務電子設備的擴展需要高度可靠的電容器。

- 市場限制

- 鉭礦價格和供應波動

- セラミックコンデンサおよびアルミコンデンサとの競合

- タンタル原料の輸出規制

- 新興的氧化鈮和石墨烯電容器

- バリュー/サプライチェーン分析

- 監管環境

- 技術展望

- 投資,資金籌措環境

- 波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 宏觀經濟影響評估

第5章 市場規模與成長預測

- 依產品類型

- 固體二氧化錳鉭電容器

- 固體聚合物鉭電容器

- 濕式電解鉭電容器

- 氧化鈮電容器

- 按安裝類型

- 表面黏著技術(SMD)

- 通孔(附引腳)

- 按容量範圍

- 最大100μF

- 100 至 1,000 μF

- 1,000μF以上

- 透過使用

- 家用電子電器

- 汽車電子

- 工業設備

- 醫療設備

- 防衛,航太

- 通訊基礎設施

- 其他用途

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東

- 以色列

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東地區

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度分析

- 策略趨勢與發展

- Vendor Positioning Analysis

- 公司簡介

- KEMET Corporation(Yageo)

- KYOCERA AVX Components Corporation

- Panasonic Corporation

- Vishay Intertechnology Inc.

- Hongda Capacitors Co. Ltd.

- Samsung Electro-Mechanics

- NIC Components Corp.

- Exxelia Group

- Abracon LLC

- TE Connectivity Ltd.

- Rohm Semiconductor

- Suntan Capacitors

- NEC Corporation

- UF Capacitors Factory Co., LTD

第7章 市場機會與未來展望

The tantalum capacitors market is expected to grow from USD 1.34 billion in 2025 to USD 1.4 billion in 2026 and is forecast to reach USD 1.74 billion by 2031 at 4.44% CAGR over 2026-2031.

Strong demand for high-capacitance density, temperature stability, and long-term reliability keeps the tantalum capacitors market firmly rooted in mission-critical electronics, even as cost pressures persist. Miniaturization of consumer devices, accelerated electrification of vehicles, expanding 5G infrastructure, and supply-chain disturbances in multilayer ceramic capacitors (MLCCs) collectively underpin steady expansion. At the same time, trade restrictions on critical minerals and raw-material price spikes temper the CAGR outlook and force buyers to diversify sourcing strategies.

Global Tantalum Capacitors Market Trends and Insights

Miniaturization of Electronic Devices

As circuit boards shrink, heat dissipation per square centimeter rises steeply, making tantalum's thermal stability indispensable for power-management ICs embedded within smartphones, wearables, and implantable medical devices. A modern flagship smartphone integrates more than 1,000 capacitors, and tantalum versions secure critical power-rail conditioning roles where volumetric efficiency and elevated reflow-temperature tolerance intersect . OEM roadmaps that target foldable, ultra-slim form factors reinforce demand for smaller case sizes without sacrificing capacitance, sustaining momentum in the tantalum capacitors market.

Rising In-Vehicle Electronics Adoption

Automotive electrification multiplies capacitor demand across traction inverters, on-board chargers, advanced driver assistance systems, and infotainment modules. Polymer tantalum capacitors remain qualified at -40 °C to +150 °C and exhibit low equivalent series resistance (ESR), outperforming ceramics in 48 V and emerging 800 V architectures. TDK projected growth in passive components for fiscal 2025 by citing surging automotive orders that elevate value per vehicle . These trends keep the tantalum capacitors market well aligned with the long-term electrification curve.

Tantalum Ore Price and Supply Volatility

Conflict-related production interruptions in the Democratic Republic of Congo and forced-labor allegations among artisanal miners tighten raw-material supply lines, transmitting price spikes through to capacitor BOMs . U.S. consumption fell sharply after a 25% tariff on Chinese tantalum imports took effect in September 2024, compelling OEMs to dual-source or re-engineer designs . These disruptions limit cost-sensitive penetration of the tantalum capacitors market.

Other drivers and restraints analyzed in the detailed report include:

- Surge in 5G Smartphone Production

- MLCC Supply Instability Favoring Tantalum

- Competition from Ceramic and Aluminum Capacitors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solid polymer tantalum capacitors captured 38.62% revenue in 2025 as OEMs prioritized ESR reduction and fail-safe performance . The tantalum capacitors market benefits from polymers' benign failure mode, eliminating the oxygen generation risk that accompanies MnO2 cathodes. Niobium oxide capacitors, though still niche, chart a 5.94% CAGR through 2031 as designers hedge raw-material risk. Solid MnO2 devices remain the volume option for cost-sensitive consumer gear, while wet-electrolytic constructions hold ground in bulk-storage niches.

Packaging innovation complements material shifts. Polymer parts support ripple-current demands in 5G power amplifiers and EV onboard chargers, reinforcing the tantalum capacitors market. As medical implants and wearable sensors push for smaller case sizes, polymer technology's stability across 1,000+ thermal cycles becomes decisive .

Surface-mount packages commanded 77.45% revenue in 2025 and are forecast to grow 5.03% CAGR, reflecting automated assembly and multilayer PCB density targets. The tantalum capacitors market size linked to surface-mount formats gains from pick-and-place accuracy improvements that shrink keep-out zones. Through-hole variants stay relevant in aerospace, defense, and heavy industrial boards where mechanical robustness and field maintainability trump form factor.

Surface-mount leadership is reinforced by PCB-embedded capacitor roadmaps that compress z-axis height and shorten power-loop inductance. Samsung Electro-Mechanics updated its part libraries to streamline simulation workflows for RF power modules, further tilting design wins toward surface-mount tantalums.

The Tantalum Capacitors Market Report is Segmented by Product Type (Solid MnO2, Solid Polymer, Wet Electrolytic, Niobium Oxide), Mounting Type (Surface-Mount, Through-Hole), Capacitance Range (Up To 100 MF, Others), Application (Consumer Electronics, Automotive Electronics, Industrial Equipment, Medical Devices, Telecommunications Infrastructure, and ), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific accounted for 44.10% of global revenue in 2025 and is poised to expand at a 5.63% CAGR through 2031. China's consumer-electronics production push, backed by subsidies for advanced packaging, reinforces passive-component pull, while Korea and Taiwan anchor memory fabs that consume high-frequency decoupling parts.

North America retools supply chains after a 25% tariff on Chinese tantalum imports and impending 2027 DoD sourcing restrictions. Domestic capacitor manufacturers expedite the qualification of ethically sourced ore from Australia and Brazil to insulate military programs from conflict-area risks . These policy shifts reshape regional volumes but also create niche demand for traceable, U.S.-made tantalum components.

Europe focuses on sustainability credentials and drives procurement toward certified conflict-free tantalum. German automotive Tier 1 suppliers collaborate with Polish and Czech capacitor plants to shorten logistics loops and meet just-in-time mandates, protecting the tantalum capacitors market against lengthy maritime delays.

Rest-of-World regions rise as alternative feedstock hubs. Australia, possessing large hard-rock tantalite reserves, adds refining capacity aligned with Western ESG standards, while Rwanda develops concentrate-upgrading infrastructure to capture more value locally. Brazil's Minas Gerais projects unlock incremental ore tonnage that diversifies global supply risk.

- KEMET Corporation (Yageo)

- KYOCERA AVX Components Corporation

- Panasonic Corporation

- Vishay Intertechnology Inc.

- Hongda Capacitors Co. Ltd.

- Samsung Electro-Mechanics

- NIC Components Corp.

- Exxelia Group

- Abracon LLC

- TE Connectivity Ltd.

- Rohm Semiconductor

- Suntan Capacitors

- NEC Corporation

- UF Capacitors Factory Co., LTD

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Miniaturization of electronic devices

- 4.2.2 Rising in-vehicle electronics adoption

- 4.2.3 Surge in 5G smartphone production

- 4.2.4 MLCC supply instability favoring tantalum

- 4.2.5 Reliability demand in implantable medical devices

- 4.2.6 Expansion of mission-critical aerospace and defense electronics requiring high-reliability capacitors

- 4.3 Market Restraints

- 4.3.1 Tantalum ore price and supply volatility

- 4.3.2 Competition from ceramic and aluminum capacitors

- 4.3.3 Export controls on tantalum raw materials

- 4.3.4 Emerging niobium-oxide and graphene capacitors

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Investment and Funding Landscape

- 4.8 Porters Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

- 4.9 Macroeconomic Impact Assessment

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Solid MnO2 Tantalum Capacitors

- 5.1.2 Solid Polymer Tantalum Capacitors

- 5.1.3 Wet Electrolytic Tantalum Capacitors

- 5.1.4 Niobium Oxide Capacitors

- 5.2 By Mounting Type

- 5.2.1 Surface-Mount (SMD)

- 5.2.2 Through-Hole (Leaded)

- 5.3 By Capacitance Range

- 5.3.1 Up to 100 uF

- 5.3.2 100 to 1,000 uF

- 5.3.3 Above 1,000 uF

- 5.4 By Application

- 5.4.1 Consumer Electronics

- 5.4.2 Automotive Electronics

- 5.4.3 Industrial Equipment

- 5.4.4 Medical Devices

- 5.4.5 Defense and Aerospace

- 5.4.6 Telecommunications Infrastructure

- 5.4.7 Other Applications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 France

- 5.5.2.3 United Kingdom

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 South Korea

- 5.5.3.4 India

- 5.5.3.5 Rest of Asia Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 Israel

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Analysis

- 6.2 Strategic Moves and Developments

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 KEMET Corporation (Yageo)

- 6.4.2 KYOCERA AVX Components Corporation

- 6.4.3 Panasonic Corporation

- 6.4.4 Vishay Intertechnology Inc.

- 6.4.5 Hongda Capacitors Co. Ltd.

- 6.4.6 Samsung Electro-Mechanics

- 6.4.7 NIC Components Corp.

- 6.4.8 Exxelia Group

- 6.4.9 Abracon LLC

- 6.4.10 TE Connectivity Ltd.

- 6.4.11 Rohm Semiconductor

- 6.4.12 Suntan Capacitors

- 6.4.13 NEC Corporation

- 6.4.14 UF Capacitors Factory Co., LTD

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

鉭電容器市場-2026-2032年全球市場預測

鉭電容器市場-2026-2032年全球市場預測 五氧化二鉭市場機會、成長要素、產業趨勢分析及2026-2035年預測。

五氧化二鉭市場機會、成長要素、產業趨勢分析及2026-2035年預測。 全球五氧化二鉭市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球五氧化二鉭市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2032 年鉭電容器市場預測:按類型、安裝類型、電容範圍、電壓範圍、應用和地區進行的全球分析2030 年鉭電容器市場預測:按類型、電容、額定電壓、安裝類型、等級、應用、最終用戶和地區進行的全球分析

2032 年鉭電容器市場預測:按類型、安裝類型、電容範圍、電壓範圍、應用和地區進行的全球分析2030 年鉭電容器市場預測:按類型、電容、額定電壓、安裝類型、等級、應用、最終用戶和地區進行的全球分析 鉭質電容的全球市場:產業分析,規模,佔有率,成長,趨勢,預測(2024年~2031年)

鉭質電容的全球市場:產業分析,規模,佔有率,成長,趨勢,預測(2024年~2031年) 五氧化二鉭市場,按產品類型、按產品提供類型、按應用、按國家和地區 - 2024-2032年產業分析、市場規模、市場佔有率和預測

五氧化二鉭市場,按產品類型、按產品提供類型、按應用、按國家和地區 - 2024-2032年產業分析、市場規模、市場佔有率和預測