|

市場調查報告書

商品編碼

1940856

亞太地區混凝土外加劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Asia-Pacific Concrete Admixtures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

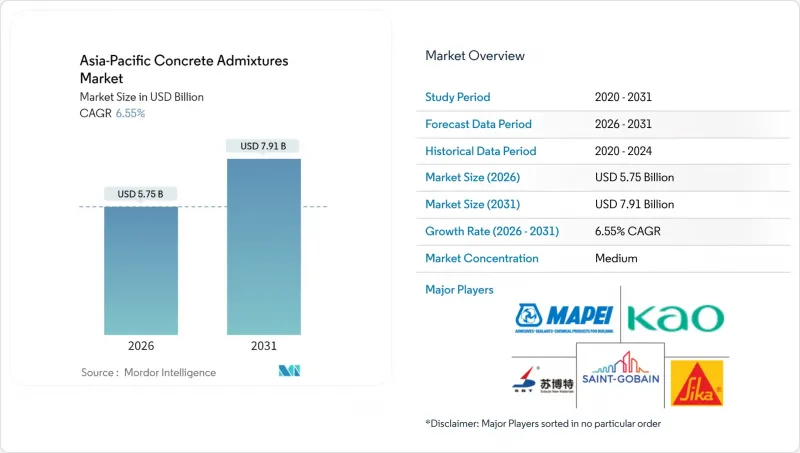

亞太地區混凝土外加劑市場預計將從 2025 年的 54 億美元成長到 2026 年的 57.5 億美元,預計到 2031 年將達到 79.1 億美元,2026 年至 2031 年的複合年成長率為 6.55%。

政府在交通、能源和城市改造領域的持續投入,預拌混凝土和預製系統的快速普及,以及地震帶和沿海地區耐久性標準的提高,目前都在支撐市場需求。承包商正在指定能夠減少用水量、加快強度發展並能承受高水泥基材料(SCM)用量的混凝土配比,從而幫助客戶縮短計劃週期並降低碳排放強度。儘管全球供應商透過收購進行整合的趨勢仍在繼續,但區域專業供應商正利用位置優勢,使競爭保持適度。供應側風險,例如波動較大的聚羧酸醚(PCE)原料成本和承包商通路分散,限制了近期的成長。然而,亞太地區的混凝土外加劑市場將繼續受益於資料中心、電池超級工廠和大型住宅專案的快速應用。

亞太地區混凝土外加劑市場趨勢及洞察

政府主導的大型企劃計劃

在中國、印度和印度尼西亞,價值數十億美元的交通走廊、機場和產業叢集正在採用摻加外加劑的混凝土,以滿足緊迫的工期和50年的使用壽命目標。混凝土生產商正在引入聚羧酸醚類高效減水劑和收縮控制添加劑,以實現混凝土快速強度發展和無裂縫的大量澆築。馬來西亞作為區域數位基礎設施中心的地位正在加速超大規模建設,這需要低滲透性和優異施工性能的高性能混凝土混合料。這些公私合作的大型企劃專案推動了亞太地區混凝土外加劑市場的強勁成長,性能導向規範也擴大被納入採購框架中。

快速採用預拌混凝土及預製混凝土攪拌站

新型預拌混凝土和預製構件工廠中標準化配料和自動化稱重平台的出現,推動了對穩定、客製化外加劑解決方案的需求。越南和泰國的混凝土外加劑應用正處於臨界點,集中式攪拌站的品質和產能均已超越現場攪拌方式,從而持續推高了對減水劑和速凝劑的需求。新加坡先進的預製構件產業生態系統進一步展現了富含外加劑的自密實混凝土在成本和速度方面的優勢,並鞏固了這一模式,其他東南亞市場也渴望效仿。

聚羧酸醚原料價格波動

丙烯酸衍生物是高效減水劑的合成原料,其價格隨原油供應趨勢波動,擠壓生產商的利潤空間,並使固定價格合約的執行變得更加複雜。東南亞地區對國內石化產能的限制對中國的出口政策產生了日益顯著的影響,導致亞太地區混凝土外加劑市場安全庫存增加,並出現週期性附加費。

細分市場分析

到2025年,減水劑將佔亞太地區混凝土外加劑市場36.95%的佔有率,這反映了其在包括大型住宅、路面鋪設和結構框架等廣泛應用領域的多功能性。承包商欣賞其在不改變水灰比的情況下可實現5-10兆帕的穩定強度提升,從而減少水泥用量並降低接合材料成本。

預計到2031年,超塑化劑將以7.02%的複合年成長率快速成長,成為市場上成長最快的產品。資料中心地下室和超級工廠的地面需要低滲透性混合料,且坍落度需保持在150毫米以上並維持兩小時以上。馬貝(MAPEI)、西卡(Sika)和聖戈班(Saint-Gobain)等公司推出了獨特的聚羧酸系產品,兼具早期強度高和收縮率低的優點,進一步擴大了其競爭優勢。

在中國北方和日本,凍融循環對路面完整性構成重大威脅,因此加氣劑仍然至關重要。在混凝土大批量澆築和水下澆築中,減縮劑和黏度調節劑的需求分別增加。儘管這些配方應用範圍較小,但它們透過解決氣候和應用方面的特定挑戰,為亞太地區的混凝土外加劑市場增添了價值。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 政府主導的大型計劃計劃

- 快速採用預拌混凝土及預製混凝土攪拌站

- 向低碳轉型/向富含SCM(水泥基外加劑)的混凝土混合料轉型

- 更嚴格的抗震和沿海建築標準耐久性要求

- 資料中心與電池超級工廠建設熱潮

- 市場限制

- 聚羧酸醚(PCE)原料價格波動

- 分散的承包商通路會延誤外加劑規格的製定

- 依賴進口的供應鏈容易受到地緣政治風險的影響。

- 價值鏈分析

- 監管環境

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 終端用戶產業趨勢

第5章 市場規模與成長預測

- 按混合物類型

- 加速器

- 加氣劑

- 高效減水劑(超塑化劑)

- 減水劑

- 緩速器

- 收縮抑制劑

- 黏度調節劑

- 其他(腐蝕抑制劑、防水劑等)

- 應用領域

- 商業的

- 工業和公共設施

- 基礎設施

- 住宅

- 按地區

- 澳洲

- 中國

- 印度

- 印尼

- 日本

- 馬來西亞

- 韓國

- 泰國

- 越南

- 亞太其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Cementaid International

- CICO Technologies

- Guangdong Redwall New Materials Co.,Ltd

- Jiangsu Subote New Materials Co., Ltd.

- Kao Corporation

- MAPEI SpA

- Master Builders Solutions Holdings GmbH

- MC-Bauchemie

- PT Penta-Chemicals Indonesia

- Pidilite Industries Ltd.

- RPM International

- Saint-Gobain

- Sika AG

- Xypex Chemical Corporation

第7章 市場機會與未來展望

第8章:執行長面臨的關鍵策略問題

The Asia-Pacific Concrete Admixtures Market is expected to grow from USD 5.40 billion in 2025 to USD 5.75 billion in 2026 and is forecast to reach USD 7.91 billion by 2031 at 6.55% CAGR over 2026-2031.

Sustained government spending on transport, energy, and urban renewal, fast-rising adoption of ready-mix and precast systems, and tightened durability norms in seismic and coastal zones together anchor current demand. Contractors specify engineered mixes that lower water demand, accelerate strength gain, and accommodate high supplementary cementitious material (SCM) loads, helping owners cut project cycle times and carbon intensity. Competitive intensity remains moderate as global suppliers consolidate through acquisitions, while local specialists capitalize on proximity advantages. Supply-side risks, linked to polycarboxylate ether (PCE) feedstock cost swings and fragmented contractor channels, temper near-term growth. However, the Asia-Pacific concrete admixtures market continues to benefit from the rapid uptake in data-center, battery-gigafactory, and large-scale housing programs.

Asia-Pacific Concrete Admixtures Market Trends and Insights

Government Megaproject Pipeline

Multi-billion-dollar transport corridors, airports, and industrial clusters across China, India, and Indonesia rely on admixture-enhanced concrete to meet tight schedules and 50-year service-life targets. Concrete producers deploy polycarboxylate-ether superplasticizers and shrinkage-reducing additives to achieve rapid strength gain and crack-free mass pours. Malaysia's designation as a regional digital-infrastructure hub accelerates hyperscale build-outs that mandate high-performance mixes with low permeability and superior workability. This convergence of public and private megaprojects keeps the Asia-Pacific concrete admixtures market on a robust growth trajectory, with procurement frameworks increasingly embedding performance-based specifications.

Rapid Penetration of Ready-Mix and Precast Concrete Plants

Standardized batching and automated dosing platforms at new ready-mix and precast facilities heighten demand for consistent, tailor-made admixture solutions. Vietnam and Thailand are now reaching adoption inflection points, where centralized plants outperform site-mixed alternatives in terms of quality and throughput, drawing in continuous volumes of water reducers and accelerators. Singapore's advanced precast ecosystem further showcases the cost and speed dividends of admixture-rich self-compacting concrete, reinforcing a template other Southeast Asian markets seek to replicate.

Volatility in Polycarboxylate Ether Feedstock Prices

Prices for acrylic-acid derivatives that underpin superplasticizer synthesis fluctuate with crude-oil supply dynamics, compressing producer margins and complicating fixed-price contracting. Limited domestic petrochemical capacity across Southeast Asia amplifies exposure to Chinese export policies, prompting higher safety stocks and periodic surcharges in the Asia-Pacific concrete admixtures market.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Low-Carbon/SCM-Rich Concrete Blends

- Stricter Durability Specs in Seismic and Coastal Building Codes

- Fragmented Contractor Channel Slows Admixture Specification

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Water reducers captured 36.95% of the Asia-Pacific concrete admixtures market in 2025, reflecting universal applicability across mass housing, pavements, and structural frames. Contractors value their predictable 5-10 MPa strength uplift at unchanged water-to-cement ratios, enabling leaner cement content and savings on overall binder cost.

Superplasticizers are projected to post the swiftest 7.02% CAGR to 2031, as data-center basements and giga-factory floors require low-permeability mixes with 150-mm slump retention over two hours. MAPEI, Sika, and Saint-Gobain introduce proprietary polycarboxylate grades that combine high early strength with reduced shrinkage, further extending their competitive lead.

Air-entraining agents remain vital in northern China and Japan, where freeze-thaw cycles pose a significant threat to pavement integrity. Shrinkage-reducing and viscosity-modifying additives gain traction in large-volume pours and underwater placements, respectively. Although niche, these formulations lengthen the value ladder within the Asia-Pacific concrete admixtures market by solving climate- and application-specific challenges.

The Asia-Pacific Concrete Admixtures Market Report is Segmented by Admixture Type (Accelerators, Air-Entraining, High-Range Water Reducers, Water Reducers, Retarders, Shrinkage-Reducing, Viscosity-Modifying, and Others), End-Use Sector (Commercial, Industrial and Institutional, Infrastructure, and Residential), and Geography (Australia, China, India, Indonesia, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Cementaid International

- CICO Technologies

- Guangdong Redwall New Materials Co.,Ltd

- Jiangsu Subote New Materials Co., Ltd.

- Kao Corporation

- MAPEI S.p.A.

- Master Builders Solutions Holdings GmbH

- MC-Bauchemie

- P.T. Penta-Chemicals Indonesia

- Pidilite Industries Ltd.

- RPM International

- Saint-Gobain

- Sika AG

- Xypex Chemical Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government megaproject pipeline

- 4.2.2 Rapid penetration of ready-mix and precast concrete plants

- 4.2.3 Shift toward low-carbon/SCM-rich concrete blends

- 4.2.4 Stricter durability specs in seismic and coastal building codes

- 4.2.5 Data-center and battery-gigafactory construction boom

- 4.3 Market Restraints

- 4.3.1 Volatility in polycarboxylate ether (PCE) feedstock prices

- 4.3.2 Fragmented contractor channel slows admixture specification

- 4.3.3 Import-based supply chains vulnerable to geopolitical risk

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 End-use Sector Trends

5 Market Size and Growth Forecasts (Value)

- 5.1 By Admixture Type

- 5.1.1 Accelerators

- 5.1.2 Air-Entraining

- 5.1.3 High-Range Water Reducers (Superplasticizers)

- 5.1.4 Water Reducers

- 5.1.5 Retarders

- 5.1.6 Shrinkage-Reducing

- 5.1.7 Viscosity-Modifying

- 5.1.8 Others (Corrosion-inhibiting, Waterproofing, etc.)

- 5.2 By End-Use Sector

- 5.2.1 Commercial

- 5.2.2 Industrial and Institutional

- 5.2.3 Infrastructure

- 5.2.4 Residential

- 5.3 By Geography

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Malaysia

- 5.3.7 South Korea

- 5.3.8 Thailand

- 5.3.9 Vietnam

- 5.3.10 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Cementaid International

- 6.4.2 CICO Technologies

- 6.4.3 Guangdong Redwall New Materials Co.,Ltd

- 6.4.4 Jiangsu Subote New Materials Co., Ltd.

- 6.4.5 Kao Corporation

- 6.4.6 MAPEI S.p.A.

- 6.4.7 Master Builders Solutions Holdings GmbH

- 6.4.8 MC-Bauchemie

- 6.4.9 P.T. Penta-Chemicals Indonesia

- 6.4.10 Pidilite Industries Ltd.

- 6.4.11 RPM International

- 6.4.12 Saint-Gobain

- 6.4.13 Sika AG

- 6.4.14 Xypex Chemical Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

8 Key Strategic Questions for CEOS

全球混凝土外加劑市場(至2031年):按類型(高性能減水劑、標準減水劑、速凝劑、緩凝劑、引氣劑)、應用(住宅、商業、基礎設施)和地區分類

全球混凝土外加劑市場(至2031年):按類型(高性能減水劑、標準減水劑、速凝劑、緩凝劑、引氣劑)、應用(住宅、商業、基礎設施)和地區分類 全球混凝土外加劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球混凝土外加劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 混凝土外加劑市場:按類型、原料、形態、應用和最終用戶分類-2026-2032年全球市場預測

混凝土外加劑市場:按類型、原料、形態、應用和最終用戶分類-2026-2032年全球市場預測 混凝土外加劑市場報告:按產品、最終用戶和地區分類(2026-2034 年)

混凝土外加劑市場報告:按產品、最終用戶和地區分類(2026-2034 年) 2026年全球混凝土外加劑市場報告2026年全球減縮劑市場報告

2026年全球混凝土外加劑市場報告2026年全球減縮劑市場報告 混凝土外加劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)全球混凝土外加劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球多羧酸減水劑市場報告

混凝土外加劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)全球混凝土外加劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球多羧酸減水劑市場報告 混凝土外加劑市場規模、佔有率和趨勢分析報告:按類型、地區和細分市場預測(2026-2033 年)

混凝土外加劑市場規模、佔有率和趨勢分析報告:按類型、地區和細分市場預測(2026-2033 年)