|

市場調查報告書

商品編碼

1940803

西班牙網路安全:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Spain Cybersecurity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

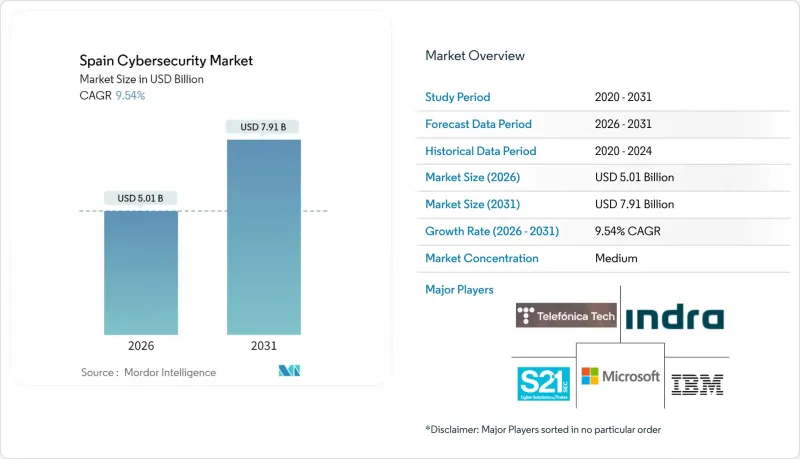

西班牙網路安全市場預計將從 2025 年的 45.7 億美元成長到 2026 年的 50.1 億美元,到 2031 年達到 79.1 億美元,2026 年至 2031 年的複合年成長率為 9.54%。

西班牙致力於將自身打造成為歐洲大陸網路安全中心,加上勒索軟體活動激增以及歐盟層面的嚴格監管,正推動企業持續增加對雲端防護、託管偵測和抗量子加密解決方案的投資。諸如12億歐元的國家網路安全戰略、「數位西班牙2026藍圖」以及CorA雲端遷移計畫等公共部門項目,正在擴大國內供應商市場。 5G的快速部署、旅遊業主導的無現金零售以及日益成長的工業數位化,進一步擴大了攻擊面,迫使企業優先考慮將安全編配和事件回應外包。儘管微企業面臨人才短缺和預算限制等挑戰,但西班牙充滿活力的Start-Ups生態系統和有針對性的公共補貼仍在持續吸引外國資本和技術合作夥伴進入西班牙網路安全市場。

西班牙網路安全市場趨勢與洞察

西班牙斥資12億歐元推出國家網路安全戰略,加速安全支出。

政府承諾在2025年將國內生產毛額的2%用於安全和國防,其中31.16%將用於加強通訊和網路安全能力。這將產生12億歐元,用於量子安全密碼試點計畫、大規模安全營運中心(SOC)升級以及旨在將西班牙提升至全球網路創新前五名的人才培養計畫。西班牙各銀行已將其技術支出加倍,推動了西班牙網路安全市場網路安全和身分管理(IAM)合約的激增。

在「數位西班牙2026」計畫下,中小企業的快速數位化擴大了攻擊面。

「數位西班牙2026」計畫旨在提升50萬名員工的技能,並提供津貼以支付安全實施成本。然而,目前70%的網路攻擊針對中小企業,暴露出基礎防禦措施的脆弱性。 「數位工具包」(Kit Digital)的補貼計畫為擁有10至49名員工的企業提供企業級防火牆和託管偵測與回應(MDR)資金籌措,鼓勵供應商專注於輕量級、自動化解決方案,從而為西班牙網路安全市場創造新的收入來源。

認證網路安全人才短缺

西班牙國家網路安全與資訊安全委員會 (INCIBE) 預計,到 2025 年,西班牙將需要 99,600 名網路安全專業人員,高於上年度的83,000 名缺口。後量子密碼學和基於人工智慧的威脅狩獵技能尤其稀缺,迫使企業將監控任務外包給運作24/7 全天候安全營運中心 (SOC) 的本地託管安全服務提供者 (MSSP)。儘管 INCIBE 和「數位西班牙」計畫提供免費課程,但人才供應仍然不足,阻礙了西班牙網路安全市場內部採用相關技術的步伐。

細分市場分析

到2025年,解決方案將佔總收入的69.12%,並將繼續成為西班牙網路安全市場的基石,因為各組織都在加強下一代防火牆(NGFW)、外部偵測與回應(EDR)和身分與存取管理(IAM)等核心防禦措施。遵守NIS2指令正在推動企業應用安全支出,而各自治機構則優先考慮符合ENS標準的雲端控制。託管服務是成長最快的細分市場,它提供遠端安全營運中心(SOC)功能,以應對技能短缺問題,並將平均檢測時間縮短48%。 Telefónica Tech目前每天為其西班牙客戶分析超過4000個雲端警報,這表明本土供應商如何將本地專業知識轉化為在西班牙網路安全市場的競爭優勢。

對專業服務的需求仍然強勁,尤其是ENS審核和NIS2合規準備。一家能源營運商聘請Indra顧問公司重新設計其OT系統分段,此前該公司預計2024年網路攻擊將增加43%。同時,Start-Ups正在實現用戶註冊和策略配置的自動化,從而簡化中小企業的部署流程。高階託管服務和自助式SaaS是兩大發展趨勢,即使業務收益加速成長,它們仍主導解決方案的發展,並增強了西班牙網路安全市場的整體規模前景。

預計到2025年,雲端採用將佔總營收的62.18%,複合年成長率(CAGR)為13.12%。 CorA指令、多重雲端戰略和主權託管要求正迫使政府機構和銀行將身分視為新的安全邊界。 ENS「Alto」認證已成為供應商資格的最低標準,提高了進入門檻,並促使企業將支出集中於符合標準的供應商。雖然國防機構和關鍵公共產業仍將繼續依賴本地部署控制,但混合配置正成為大型企業發展藍圖的主流,推動西班牙網路安全市場對跨SaaS、IaaS和傳統資產的統一策略引擎的需求。

對於中小企業而言,雲端安全可以降低資本支出,並提供對威脅情報來源的即時存取。加那利群島的緊急服務部門透過加密主權雲端中的所有工作負載來保護公民數據,這顯示了公共機構如何在安全性和延遲要求之間取得平衡。這種廣泛的應用也印證了為什麼到2031年,雲端將在西班牙網路安全市場中佔據更大的佔有率。

西班牙網路安全市場報告按產品類型(解決方案、服務)、部署模式(本地部署、雲端部署)、最終用戶垂直產業(銀行、金融服務和保險、醫療保健、IT 和電信、工業和國防、製造業、零售和電子商務、能源和公共產業、其他)以及最終用戶公司規模(中小企業、大型企業)對產業進行細分。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 西班牙斥資12億歐元製定國家網路安全戰略,加速安全支出。

- 在「數位西班牙2026」計畫下,中小企業的快速數位化擴大了攻擊面。

- 公共管理雲端採用計畫 (CorA 計畫) 推動了對雲端原生安全的需求

- 5G部署加速推動邊緣威脅增加,網路安全投資也隨之成長。

- 旅遊業主導的無現金零售熱潮推動了打擊支付詐騙的行動。

- 針對西班牙關鍵基礎設施的國家級威脅活動活性化

- 市場限制

- 認證網路安全人才短缺

- 微型、小型和中型企業的預算限制

- 本地採購流程的碎片化

- 對進口安全技術的依賴

- 關鍵法規結構評估

- 價值鏈分析

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 主要用例和案例研究

- 宏觀經濟因素對市場的影響

- 投資分析

第5章 市場區隔

- 報價

- 解決方案

- 應用程式安全

- 雲端安全

- 資料安全

- 身分和存取管理

- 基礎設施保護

- 綜合風險管理

- 網路安全設備

- 端點安全

- 其他服務

- 服務

- 專業服務

- 託管服務

- 解決方案

- 透過部署模式

- 本地部署

- 雲

- 按最終用戶行業分類

- BFSI

- 衛生保健

- 資訊科技/通訊

- 工業與國防

- 製造業

- 零售與電子商務

- 能源與公共產業

- 製造業

- 其他

- 按最終用戶公司規模分類

- 小型企業

- 主要企業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Telefonica Tech(Cybersecurity & Cloud Tech SLU)

- Indra Sistemas SA

- Grupo S21Sec(Thales)

- Microsoft Corp.

- IBM Corporation

- Cisco Systems Inc.

- Palo Alto Networks Inc.

- Check Point Software Technologies Ltd.

- Fortinet Inc.

- Accenture plc

- Atos SE

- Capgemini SE

- Orange Cyberdefense(Orange Espana)

- Secureworks Inc.

- ESET Espana

- Sophos Ltd.

- Trend Micro Inc.

- CrowdStrike Holdings Inc.

- Alias Robotics SL

- Titanium Industrial Security SL

- Evolium Technologies SLU(Redtrust)

- Outpost24 Group(Blueliv)

- Acuntia SAU(Axians)

- GMV Innovating Solutions

- Everis(NTT DATA Spain)

- KPMG Spain

第7章 市場機會與未來展望

The Spain cybersecurity market is expected to grow from USD 4.57 billion in 2025 to USD 5.01 billion in 2026 and is forecast to reach USD 7.91 billion by 2031 at 9.54% CAGR over 2026-2031.

Spain's decision to position itself as a continental cybersecurity hub, combined with surging ransomware activity and strict EU-level mandates, is fuelling sustained spending on cloud-based protection, managed detection, and quantum-safe encryption solutions. Public-sector programs such as the EUR 1.2 billion National Cybersecurity Strategy, the Digital Spain 2026 roadmap, and the CorA cloud migration plan are enlarging the domestic addressable base for vendors. Rapid 5G rollout, tourism-led cashless retail, and growing industrial digitisation further widen the attack surface, prompting enterprises to prioritise security orchestration and incident-response outsourcing. Although the talent shortage and budget limits at micro-SMEs act as headwinds, Spain's vibrant start-up ecosystem and targeted public subsidies continue to draw foreign capital and technology partnerships into the Spain cybersecurity market.

Spain Cybersecurity Market Trends and Insights

Spain's EUR 1.2 billion National Cybersecurity Strategy accelerating security spend

Government pledges to channel 2% of GDP into security and defence in 2025 include a dedicated 31.16% slice for telecom and cyber capabilities. The resulting flow of EUR 1.2 billion is being directed toward quantum-safe cryptography pilots, large-scale SOC upgrades, and workforce programmes that aim to elevate Spain into the global top five for cyber innovation. Spanish banks have already doubled technology outlays, prompting a parallel surge in network-security and IAM contracts within the Spain cybersecurity market .

Rapid digitalisation of SMEs under Digital Spain 2026 expanding attack surface

Digital Spain 2026 targets the upskilling of 500,000 workers and dispenses grants that offset security adoption costs, yet 70% of current attacks hit SMEs, exposing gaps in basic controls. Kit Digital subsidies now finance enterprise-grade firewalls and MDR subscriptions for firms with 10-49 staff, stimulating vendor focus on lightweight, automated offerings that anchor new revenue in the Spain cybersecurity market.

Scarcity of certified cybersecurity talent

INCIBE estimates that Spain needed 99,600 specialists in 2025, up from 83,000 vacancies the previous year. Post-quantum cryptography and AI-enabled threat hunting skills are especially rare, prompting enterprises to outsource monitoring to local MSSPs that run 24/7 SOCs. Although INCIBE and Digital Spain programmes deliver free courses, the pipeline remains insufficient, curbing in-house deployment pace across the Spain cybersecurity market.

Other drivers and restraints analyzed in the detailed report include:

- CorA plan cloud adoption boosting native cloud-security demand

- 5G rollout intensifying edge threats and network-security investment

- Budget constraints among micro-SMEs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions accounted for 69.12% of 2025 revenue and continue to anchor the Spain cybersecurity market as organisations bolster core defences such as NGFWs, EDR and IAM. Compliance with the NIS2 Directive spurs enterprise spending on application security, while autonomous-community agencies prioritise ENS-aligned cloud controls. Managed services, the fastest-growing subsegment, respond to skills shortages by supplying remote SOC functions that compress mean time to detect by 48%. Telefonica Tech now analyses more than 4,000 cloud alerts daily for Spanish customers, illustrating how domestic providers convert local expertise into competitive differentiation within the Spain cybersecurity market.

Demand for professional services endures, centred on ENS audits and NIS2 readiness. Energy utilities relied on Indra consultants to redesign OT segmentation after a 43% attack spike in 2024. Meanwhile, startups automate onboarding and policy configuration to streamline SME adoption. The dual trajectory of high-end managed services and self-service SaaS keeps solutions in the lead even as service revenues accelerate, reinforcing the overall Spain cybersecurity market size outlook.

Cloud deployments captured 62.18% revenue in 2025 and are forecast to advance at a 13.12% CAGR. CorA mandates, multicloud strategies, and sovereign hosting requirements push agencies and banks to treat identity as the new perimeter. ENS "Alto" certification has become a baseline vendor qualification, raising barriers to entry and concentrating spend among compliant suppliers. On-premise controls persist in defence and critical utilities, but hybrid topologies dominate large-enterprise roadmaps, requiring unified policy engines that span SaaS, IaaS, and legacy assets inside the Spain cybersecurity market.

For SMEs, cloud security removes capital expense and provides instant access to threat intelligence feeds. Canary Islands emergency services secured citizen data by encrypting all workloads in a sovereign cloud, showing how public agencies can balance protection and latency requirements. This broad adoption underlines why cloud's share of the Spain cybersecurity market size will widen further by 2031.

The Cybersecurity Market in Spain Report Segments the Industry Into by Offering (Solutions, and Services), Deployment Mode (On-Premise, and Cloud), End-User Vertical (BFSI, Healthcare, IT and Telecom, Industrial and Defense, Manufacturing, Retail and E-Commerce, Energy and Utilities, Manufacturing, and Others), and End-User Enterprise Size (Small and Medium Enterprises (SMEs), and Large Enterprises).

List of Companies Covered in this Report:

- Telefonica Tech (Cybersecurity & Cloud Tech SLU)

- Indra Sistemas SA

- Grupo S21Sec (Thales)

- Microsoft Corp.

- IBM Corporation

- Cisco Systems Inc.

- Palo Alto Networks Inc.

- Check Point Software Technologies Ltd.

- Fortinet Inc.

- Accenture plc

- Atos SE

- Capgemini SE

- Orange Cyberdefense (Orange Espana)

- Secureworks Inc.

- ESET Espana

- Sophos Ltd.

- Trend Micro Inc.

- CrowdStrike Holdings Inc.

- Alias Robotics SL

- Titanium Industrial Security SL

- Evolium Technologies SLU (Redtrust)

- Outpost24 Group (Blueliv)

- Acuntia SAU (Axians)

- GMV Innovating Solutions

- Everis (NTT DATA Spain)

- KPMG Spain

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Spain's EUR 1.2 B National Cybersecurity Strategy Accelerating Security Spend

- 4.2.2 Rapid Digitalisation of SMEs under "Digital Spain 2026" Expanding Attack Surface

- 4.2.3 Cloud Adoption by Public Administration (CorA Plan) Boosting Native Cloud-Security Demand

- 4.2.4 5G Roll-out Intensifying Edge Threats and Network-Security Investment

- 4.2.5 Tourism-Led Cashless Retail Boom Driving Payment-Fraud Mitigation

- 4.2.6 Heightened Nation-State Threat Activity Targeting Spanish Critical Infrastructure

- 4.3 Market Restraints

- 4.3.1 Scarcity of Certified Cybersecurity Talent

- 4.3.2 Budget Constraints among Micro-SMEs

- 4.3.3 Fragmented Regional Procurement Processes

- 4.3.4 Dependence on Imported Security Technologies

- 4.4 Evaluation of Critical Regulatory Framework

- 4.5 Value Chain Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Key Use Cases and Case Studies

- 4.9 Impact on Macroeconomic Factors of the Market

- 4.10 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Offering

- 5.1.1 Solutions

- 5.1.1.1 Application Security

- 5.1.1.2 Cloud Security

- 5.1.1.3 Data Security

- 5.1.1.4 Identity and Access Management

- 5.1.1.5 Infrastructure Protection

- 5.1.1.6 Integrated Risk Management

- 5.1.1.7 Network Security Equipment

- 5.1.1.8 Endpoint Security

- 5.1.1.9 Other Services

- 5.1.2 Services

- 5.1.2.1 Professional Services

- 5.1.2.2 Managed Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By End-User Vertical

- 5.3.1 BFSI

- 5.3.2 Healthcare

- 5.3.3 IT and Telecom

- 5.3.4 Industrial and Defense

- 5.3.5 Manufacturing

- 5.3.6 Retail and E-commerce

- 5.3.7 Energy and Utilities

- 5.3.8 Manufacturing

- 5.3.9 Others

- 5.4 By End-User Enterprise Size

- 5.4.1 Small and Medium Enterprises (SMEs)

- 5.4.2 Large Enterprises

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Telefonica Tech (Cybersecurity & Cloud Tech SLU)

- 6.4.2 Indra Sistemas SA

- 6.4.3 Grupo S21Sec (Thales)

- 6.4.4 Microsoft Corp.

- 6.4.5 IBM Corporation

- 6.4.6 Cisco Systems Inc.

- 6.4.7 Palo Alto Networks Inc.

- 6.4.8 Check Point Software Technologies Ltd.

- 6.4.9 Fortinet Inc.

- 6.4.10 Accenture plc

- 6.4.11 Atos SE

- 6.4.12 Capgemini SE

- 6.4.13 Orange Cyberdefense (Orange Espana)

- 6.4.14 Secureworks Inc.

- 6.4.15 ESET Espana

- 6.4.16 Sophos Ltd.

- 6.4.17 Trend Micro Inc.

- 6.4.18 CrowdStrike Holdings Inc.

- 6.4.19 Alias Robotics SL

- 6.4.20 Titanium Industrial Security SL

- 6.4.21 Evolium Technologies SLU (Redtrust)

- 6.4.22 Outpost24 Group (Blueliv)

- 6.4.23 Acuntia SAU (Axians)

- 6.4.24 GMV Innovating Solutions

- 6.4.25 Everis (NTT DATA Spain)

- 6.4.26 KPMG Spain

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

全球網路安全市場:機會與戰略展望(至2035年)

全球網路安全市場:機會與戰略展望(至2035年) IT與通訊網路安全市場-全球產業規模、佔有率、趨勢、機會與預測:按部署模式、安全解決方案、最終用戶產業、地區和競爭格局分類,2021-2031年

IT與通訊網路安全市場-全球產業規模、佔有率、趨勢、機會與預測:按部署模式、安全解決方案、最終用戶產業、地區和競爭格局分類,2021-2031年 網路安全代理型人工智慧:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

網路安全代理型人工智慧:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) IT與通訊網路安全市場:依解決方案、部署類型、企業規模、最終用戶、國家及地區分類-產業分析、市場規模、市場佔有率及2026年至2033年預測

IT與通訊網路安全市場:依解決方案、部署類型、企業規模、最終用戶、國家及地區分類-產業分析、市場規模、市場佔有率及2026年至2033年預測 通訊網路安全市場預測至2034年-按組件、部署模式、安全類型、解決方案類型、應用、最終用戶和地區分類的全球分析

通訊網路安全市場預測至2034年-按組件、部署模式、安全類型、解決方案類型、應用、最終用戶和地區分類的全球分析 網路安全市場規模、佔有率和成長分析:按組件、部署模式、安全類型、組織規模、最終用戶產業和地區分類-2026-2033年產業預測

網路安全市場規模、佔有率和成長分析:按組件、部署模式、安全類型、組織規模、最終用戶產業和地區分類-2026-2033年產業預測 2026-2030年全球公共部門網路安全市場

2026-2030年全球公共部門網路安全市場 全球網路安全代理型人工智慧市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球網路安全代理型人工智慧市場規模、佔有率、趨勢和成長分析報告(2026-2034) 後量子安全市場分析及至2035年預測:產品、服務、技術、組件、應用、部署狀態及最終用戶人工智慧驅動的網路安全解決方案市場預測至2034年:按交付方式、技術類型、安全類型、部署方式、組織規模、最終用戶和地區分類的全球分析

後量子安全市場分析及至2035年預測:產品、服務、技術、組件、應用、部署狀態及最終用戶人工智慧驅動的網路安全解決方案市場預測至2034年:按交付方式、技術類型、安全類型、部署方式、組織規模、最終用戶和地區分類的全球分析