|

市場調查報告書

商品編碼

1940802

美國POS終端:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)United States (US) Point Of Sale (POS) Terminals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

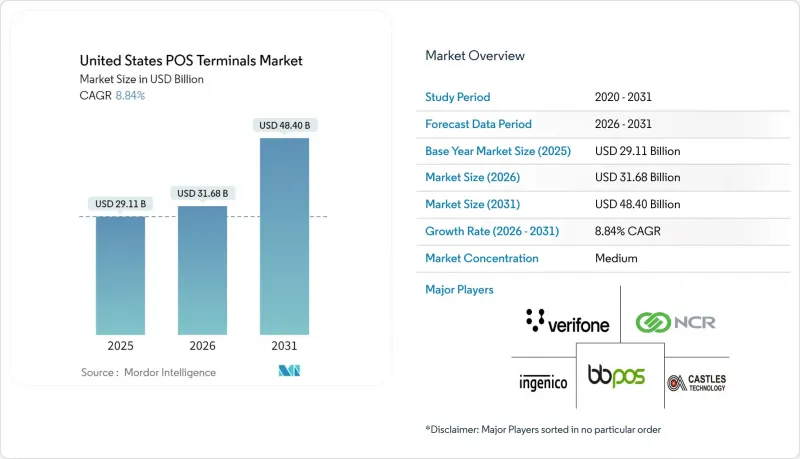

美國POS終端市場預計將從2025年的291.1億美元成長到2026年的316.8億美元,到2031年達到484億美元,2026年至2031年的複合年成長率為8.84%。

這一成長主要得益於EMV和NFC升級的加速、非接觸式支付的日益普及以及小規模企業向雲端行動POS解決方案的遷移。監管因素,包括PCI DSS 4.0的強制要求,正在推動硬體更新換代,而包括FedNow在內的即時支付基礎設施正在重塑人們對支付的預期。隨著處理器費用的壓縮降低了獨立硬體的利潤率,供應商整合的壓力也越來越大。零售商也更傾向於支援半整合架構和嵌入式金融應用的安卓智慧設備,這些設備能夠在不超出PCI監管範圍的情況下實現統一的商業分析。

美國銷售點終端市場趨勢與洞察

EMV 和 NFC 終端的快速更新週期

EMVCo 的數據顯示,到 2024 年,美國非接觸式交易將成長 87%,其中輕觸支付將佔所有刷卡交易的 34%。非 EMV 硬體的責任轉移增加了詐欺風險,促使商家升級到支援 NFC 的終端。非接觸式支付比晶片插入快 53%,從而減少了等待時間和購物車棄購率。競爭壓力迫使那些行動較慢的商家在 2027 年合約到期前升級終端。

小型企業正在轉向基於雲端的行動POS解決方案

根據美國聯邦會的一項調查,67%的美國小型企業優先考慮在其支付系統中整合庫存管理和分析功能。與傳統的租賃方式相比,基於平板電腦的行動POS系統可降低初始硬體成本,並減少23%的每月處理費用。 Stripe和Square提供的嵌入式金融服務進一步降低了採用門檻,幫助快閃店零售商在任何有網路連線的地方接受付款。

針對POS終端機的網路攻擊日益複雜化

FS-ISAC 的追蹤研究表明,到 2024 年,針對 POS 系統的惡意軟體變種將增加 34%,其中包括利用 NFC 通道和 Android 系統的漏洞。這迫使零售商將終端檢測和加密通訊納入累計,使 POS 系統的整體成本增加 15% 至 25%。由於擔心系統複雜性增加,小規模企業擴大推遲升級,或在風險較高的環境中重新採用現金支付。

細分市場分析

非接觸式支付解決方案是美國POS終端市場成長最快的細分領域,複合年成長率高達10.37%。然而,到2025年,接觸式讀卡機仍將佔據美國POS終端市場68.15%的佔有率。萬事達卡的研究顯示,非接觸式支付已佔全球面對面交易的73%,在美國的使用率更是年增87%。聯準會的數據顯示,由於處理速度更快、更衛生,消費者對非接觸式支付的偏好將從2023年的23%上升到2024年的41%。

商家正利用現有基礎設施逐步引入NFC技術,同時繼續支援晶片密碼支付,以應對高額交易和老年人。雙介面終端順應了不斷變化的支付習慣,Apple Pay和Google Pay已覆蓋67%的35歲以下智慧型手機用戶。能夠無縫提供接觸式和非接觸式支付的供應商預計在2031年之前引領美國POS終端市場的成長。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 宏觀經濟因素的影響

- 市場促進因素

- EMV 和 NFC 終端的快速更新週期

- 中小企業正在轉向基於雲端的行動支付解決方案

- 零售商需要整合式商務分析

- PCI-DSS 4.0 合規性推動硬體更新換代

- 銷售點即時支付和電子錢包接受度激增

- 嵌入式金融獨立軟體開發商提供捆綁式終端和軟體即服務 (SaaS) 服務。

- 市場限制

- 針對POS終端機的網路攻擊正變得越來越複雜。

- 小規模導致小型零售商推遲資本投資。

- 處理器和閘道器費用的壓縮給硬體利潤率帶來了壓力。

- 遍遠地區的網路連線不足限制了無線POS機的效能

- 產業價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 買方的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 競爭對手之間的競爭

- 替代品的威脅

- 對影響市場的宏觀經濟因素進行評估

第5章 市場規模與成長預測

- 透過付款方式

- 聯繫類型

- 非接觸式

- 按POS類型

- 固定式POS系統

- 行動/可攜式POS系統

- 按最終用戶行業分類

- 零售

- 飯店業

- 衛生保健

- 運輸/物流

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Verifone Systems Inc.

- Ingenico Inc.

- PAX Technology Limited

- Toshiba Global Commerce Solutions, Inc.

- NCR Corporation

- Diebold Nixdorf Incorporated

- Castles Technology Co., Ltd.

- BBPOS Limited

- Newland Payment Technology Co., Ltd.

- UIC Payworld Inc.

- Equinox Payments, LLC

- Clover Network, LLC

- Square Inc.(Block Inc.)

- Toast, Inc.

- Lightspeed Commerce Inc.

- Posiflex Technology, Inc.

- Epson America, Inc.

- Elo Touch Solutions, Inc.

- HP Inc.(Retail Solutions)

- Zebra Technologies Corporation

第7章 市場機會與未來展望

The United States Point Of Sale Terminals market is expected to grow from USD 29.11 billion in 2025 to USD 31.68 billion in 2026 and is forecast to reach USD 48.4 billion by 2031 at 8.84% CAGR over 2026-2031.

This growth is driven by accelerated EMV and NFC upgrades, rising contactless adoption, and the migration of small merchants to cloud-based mobile POS solutions. Regulatory triggers, including PCI DSS 4.0 mandates, are prompting hardware refresh cycles, while FedNow and other real-time rails are reshaping settlement expectations. Processor fee compression is intensifying vendor consolidation pressures as margins on standalone hardware narrow. Merchants also favor Android smart terminals that support semi-integrated architectures and embedded finance applications, enabling unified commerce analytics without breaching PCI scope.

United States (US) Point Of Sale (POS) Terminals Market Trends and Insights

Rapid EMV and NFC Terminal Upgrade Cycle

EMVCo recorded an 87% rise in U.S. contactless transactions during 2024, with tap-to-pay now accounting for 34% of all card-present activity. Liability shifts on non-EMV hardware elevate fraud risk, pushing merchants toward NFC-ready replacements. Contactless processing is 53% faster than chip insert, cutting wait times and limiting basket abandonment. Competitive pressure now compels even late-adopting small businesses to refresh terminals ahead of 2027 contract renewals.

SME Shift to Cloud-Based mPOS Solutions

Federal Reserve polling shows 67% of U.S. small firms prioritize integrated inventory and analytics within payment systems. Tablet-based mPOS reduces upfront hardware costs and lowers monthly processing fees by 23% versus legacy leases. Embedded finance bundles from Stripe and Square further compress adoption friction, helping pop-up retailers accept payments wherever connectivity exists.

Intensifying Cyber-Attack Sophistication on POS End-Points

FS-ISAC tracked a 34% rise in POS-targeted malware variants during 2024, including exploits on NFC channels and Android vulnerabilities. Merchants now budget for endpoint detection and encrypted communications that raise overall POS system costs 15-25%. Smaller operators, deterred by added complexity, postpone upgrades or revert to cash-only in high-risk settings.

Other drivers and restraints analyzed in the detailed report include:

- Retailer Demand for Unified Commerce Analytics

- PCI-DSS 4.0 Compliance Driving Hardware Refresh

- Inflation-Driven Cap-Ex Deferrals by Small Merchants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Contactless solutions constitute the fastest-moving slice of the US POS terminals market at a 10.37% CAGR, although contact-based readers still held a 68.15% US POS terminals market share in 2025. Mastercard found tap-to-pay already represents 73% of face-to-face transactions globally, and U.S. usage climbed 87% year over year. Federal Reserve data shows consumer preference for contactless rose to 41% in 2024 from 23% in 2023, sustained by quicker throughput and hygiene benefits.

Merchants continue to support chip-and-PIN for large-ticket sales and older consumer cohorts, leveraging the installed base while gradually layering in NFC. Dual-interface devices accommodate evolving wallet habits as Apple Pay and Google Pay reach 67% penetration among under-35 smartphone owners. Vendors able to furnish seamless contact and contactless acceptance stand to capture the incremental US POS terminals market size expansion through 2031.

The United States Point of Sale Terminals Market Report is Segmented by Mode of Payment Acceptance (Contact-Based and Contactless), POS Type (Fixed Point-Of-Sale Systems, Mobile/Portable Point-Of-Sale Systems), End-User Industry (Retail, Hospitality, Healthcare, Transportation and Logistics, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Verifone Systems Inc.

- Ingenico Inc.

- PAX Technology Limited

- Toshiba Global Commerce Solutions, Inc.

- NCR Corporation

- Diebold Nixdorf Incorporated

- Castles Technology Co., Ltd.

- BBPOS Limited

- Newland Payment Technology Co., Ltd.

- UIC Payworld Inc.

- Equinox Payments, LLC

- Clover Network, LLC

- Square Inc. (Block Inc.)

- Toast, Inc.

- Lightspeed Commerce Inc.

- Posiflex Technology, Inc.

- Epson America, Inc.

- Elo Touch Solutions, Inc.

- HP Inc. (Retail Solutions)

- Zebra Technologies Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors

- 4.3 Market Drivers

- 4.3.1 Rapid EMV and NFC Terminal Upgrade Cycle

- 4.3.2 SME Shift to Cloud-Based mPOS Solutions

- 4.3.3 Retailer Demand for Unified Commerce Analytics

- 4.3.4 PCI-DSS 4.0 Compliance Driving Hardware Refresh

- 4.3.5 Surge in Real-Time Payment and Wallet Acceptance at POS

- 4.3.6 Embedded-Finance ISVs Bundling Terminals with SaaS

- 4.4 Market Restraints

- 4.4.1 Intensifying Cyber-attack Sophistication on POS End-points

- 4.4.2 Inflation-Driven Cap-Ex Deferrals by Small Merchants

- 4.4.3 Processor and Gateway Fee Compression Squeezing Hardware Margins

- 4.4.4 Rural Connectivity Gaps Limiting Wireless POS Performance

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Intensity of Competitive Rivalry

- 4.8.5 Threat of Substitutes

- 4.9 Assessment of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Mode of Payment Acceptance

- 5.1.1 Contact-based

- 5.1.2 Contactless

- 5.2 By POS Type

- 5.2.1 Fixed Point-of-Sale Systems

- 5.2.2 Mobile / Portable Point-of-Sale Systems

- 5.3 By End-User Industry

- 5.3.1 Retail

- 5.3.2 Hospitality

- 5.3.3 Healthcare

- 5.3.4 Transportation and Logistics

- 5.3.5 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Verifone Systems Inc.

- 6.4.2 Ingenico Inc.

- 6.4.3 PAX Technology Limited

- 6.4.4 Toshiba Global Commerce Solutions, Inc.

- 6.4.5 NCR Corporation

- 6.4.6 Diebold Nixdorf Incorporated

- 6.4.7 Castles Technology Co., Ltd.

- 6.4.8 BBPOS Limited

- 6.4.9 Newland Payment Technology Co., Ltd.

- 6.4.10 UIC Payworld Inc.

- 6.4.11 Equinox Payments, LLC

- 6.4.12 Clover Network, LLC

- 6.4.13 Square Inc. (Block Inc.)

- 6.4.14 Toast, Inc.

- 6.4.15 Lightspeed Commerce Inc.

- 6.4.16 Posiflex Technology, Inc.

- 6.4.17 Epson America, Inc.

- 6.4.18 Elo Touch Solutions, Inc.

- 6.4.19 HP Inc. (Retail Solutions)

- 6.4.20 Zebra Technologies Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

2026年全球POS系統需求市場報告2026年全球銷售點(POS)市場報告

2026年全球POS系統需求市場報告2026年全球銷售點(POS)市場報告 餐廳POS系統市場依部署方式、最終用戶、組件、營運和支付方式分類,全球預測(2026-2032年)

餐廳POS系統市場依部署方式、最終用戶、組件、營運和支付方式分類,全球預測(2026-2032年) 銷售點 (POS) 市場分析及至 2035 年預測:按類型、產品類型、服務、技術、組件、應用、設備、部署類型、最終用戶和功能分類餐飲POS終端市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能及安裝類型分類

銷售點 (POS) 市場分析及至 2035 年預測:按類型、產品類型、服務、技術、組件、應用、設備、部署類型、最終用戶和功能分類餐飲POS終端市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能及安裝類型分類 2026-2034年全球餐飲POS終端市場規模、佔有率、趨勢及成長分析報告

2026-2034年全球餐飲POS終端市場規模、佔有率、趨勢及成長分析報告 日本POS終端市場規模、佔有率、趨勢和預測:按組件、終端類型、企業規模、行業和地區分類,2026-2034年

日本POS終端市場規模、佔有率、趨勢和預測:按組件、終端類型、企業規模、行業和地區分類,2026-2034年 餐廳POS解決方案市場 - 全球產業規模、佔有率、趨勢、機會和預測,按部署方式、應用、最終用途、地區和競爭格局分類,2021-2031年預測

餐廳POS解決方案市場 - 全球產業規模、佔有率、趨勢、機會和預測,按部署方式、應用、最終用途、地區和競爭格局分類,2021-2031年預測 攜帶式銷售點(POS)終端市場規模、佔有率和成長分析(按組件、產品類型、作業系統、應用和地區分類)-2026-2033年產業預測

攜帶式銷售點(POS)終端市場規模、佔有率和成長分析(按組件、產品類型、作業系統、應用和地區分類)-2026-2033年產業預測 Android POS市場規模、佔有率和成長分析(按類型、應用和地區分類)-產業預測(2026-2033年)

Android POS市場規模、佔有率和成長分析(按類型、應用和地區分類)-產業預測(2026-2033年)