|

市場調查報告書

商品編碼

1940784

交流電機(AC馬達):市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031年)Alternating Current (AC) Motor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

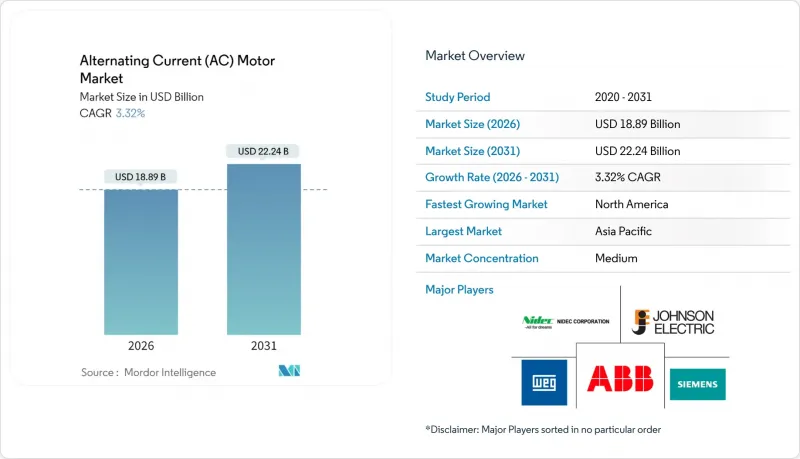

預計到 2026 年,AC馬達馬達市場價值將達到 188.9 億美元,從 2025 年的 182.9 億美元成長到 2031 年的 222.4 億美元。

預計2026年至2031年年複合成長率(CAGR)為3.32%。

這一成長軌跡更受到IE3和IE4法規驅動的能源效率提升驅動型設備更新換代週期的影響,而非新增產能。在離散製造、可再生能源和暖通空調(HVAC)領域,高效節能設計的應用日益普及,亞洲的自動化項目和北美地區的回流生產也支撐了基準需求。為因應原物料價格波動和半導體短缺,供應商的策略圍繞著銅繞組、電工鋼和電力電子領域的垂直整合。雖然石油和天然氣等成熟的終端用戶領域仍然是收入的主要來源,但成長速度更快的領域正轉向水處理、資料中心和風力發電機輔助設備,這些領域全生命週期的節能效益足以支撐其溢價。

全球交流電機市場趨勢與洞察

強制性節能法規推動了高階引擎的普及

IE3 已成為全球最低標準,而 IE4 在歐洲和美國的普及速度正在加快,這有效地將老舊、效率較低的型號從採購清單中剔除。為了滿足更嚴格的損耗限制,製造商正在升級工廠,配備自動化疊片壓機生產線和精密磁鐵組裝。這種轉變給缺乏資金投資新模具的小型區域性公司帶來了壓力,同時也加劇了市場集中度,使其集中在成熟的全球企業手中。採購團隊現在會在 75% 和 50% 的負載點評估馬達的滿載效率,這增強了永磁同步馬達設計的價值提案。符合公用事業公司高額電機補貼條件的終端用戶可以將投資回收期縮短至兩年以內,這進一步推動了監管改革的進程。

工業自動化推動了對中功率馬達的需求

汽車、電子和物流企業正在擴大協作機器人規模,這需要功率在 1-100kW 之間的精密馬達。配備編碼器的伺服同步馬達能夠提供機器人焊接、取放和自動導引運輸車(AGV) 所需的亞毫米級精度。整合式驅動器和馬達安裝感測器的扭矩向量控制技術可最大限度地減少停機時間。中國、日本和韓國針對智慧工廠的區域性獎勵正在加速升級計劃,而北美工廠也將類似的架構納入其回流計畫。能夠提供驅動器、控制器和分析軟體捆綁銷售的供應商正在獲得更高的利潤率。

原物料價格波動對製造業經濟帶來壓力。

銅繞組佔電機材料成本的四分之一之多,因此,倫敦金屬交易所銅價在2024年之前18%的波動幅度給原始設備製造商(OEM)的季度利潤率帶來了壓力。由於中國出口政策的不確定性,釹鏑永磁體的價格也大幅上漲。製造商們採取了替代策略,包括最佳化槽填充、採用鋁製轉子籠和高鐵氧體磁鐵材料。大型製造商則透過簽訂多年期供應合約和建立自身的磁體回收計畫來規避風險。

細分市場分析

由於其結構穩固且初始成本低,預計即使到2025年,感應電動機仍將維持69.12%的AC馬達馬達市場佔有率。然而,隨著永久磁鐵磁通密度的提高和控制設備的下降,同步馬達的替代需求預計將以5.53%的複合年成長率成長。因此,同步馬達型AC馬達馬達的市場規模預計將比現有感應電動機的替代需求成長更快。

高效率對於高能耗工廠來說極具吸引力,而內建的位置回饋功能則有助於機器人和輸送機的定位控制。原始設備製造商(OEM)正在將同步馬達與磁場定向驅動裝置捆綁銷售,以簡化試運行。雖然單相感應馬達在住宅空調仍然佔據主導地位,但多相同步馬達正在汽車噴漆車間和SMT生產線上逐步普及。預計未來十年,這兩種技術在交流馬達市場佔有率上的差距將逐漸縮小。

預計到2025年,低壓(低於1千伏特)馬達將佔通用製造業和暖通空調(HVAC)領域總收入的60.88%。然而,由於風力發電廠和海水淡化廠對兆瓦級輔助設備的需求,高壓(高於11千伏特)馬達將呈現最高的複合年成長率(CAGR),達到5.14%。因此,高壓交流電機市場規模預計將以高於中壓馬達市場的速度成長。

為了應對高壓下的局部放電,原始設備製造商 (OEM) 正在將緊湊型定子槽設計為標準;環氧樹脂雲母絕緣系統則可延長馬達在潮濕的海上機艙環境中的使用壽命。電網規範的實施也推動了具有卓越功率因數性能的同步馬達的應用。巴西和越南的工程總承包商 (EPC) 擴大採用高壓電機,以最大限度地減少長距離電纜傳輸過程中的電流和電纜損耗,從而擴大了此類交流電機的市場佔有率。

區域分析

到2025年,亞太地區將佔全球收入的44.10%。在中國,高科技製造業的復甦推動了精密馬達的進口;而印度可再生能源的普及應用則帶動了風能和太陽能等大型設施對驅動裝置的需求。越南和泰國等東南亞國家正逐步實現伺服生產線的在地化,從而縮短進口前置作業時間。在韓國和日本,政府對高效率馬達成本高達20%的補貼正在加速升級改造。

南美洲是成長最快的地區,預計到2031年年均複合成長率將達到4.02%。在巴西,國家開發銀行的資金正用於工業現代化,帶動了石化產業叢集對IE3+馬達的訂單成長。阿根廷的RenovAr競標系統刺激了風電場投資,並提振了對500kW以上同步馬達的需求。匯率波動正在縮小資本投資窗口,但墨西哥和巴西設有組裝廠的原始設備製造商(OEM)正在對沖外匯風險並鎖定大額訂單。

北美和歐洲仍然是以替換為主導的市場。美國《CHIPS法案》和《IRA法案》下的回流生產激勵措施鼓勵新建工廠,這些工廠需要中型伺服陣列。加拿大偏遠地區的礦場偏好堅固耐用、高功率、配備防冰軸承的馬達。歐盟生態設計指令正在推動現有工廠升級至IE4標準。斯堪地那維亞國家正在為區域供熱泵制定IE5標準,而德國汽車產業則擴大整合智慧馬達和驅動組件,同時保持較高的價格。在這兩個地區,平均售價的上漲抵消了銷售成長放緩的影響,穩定了老牌交流馬達的市佔率。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 強制性能效法規(IE3/IE4)

- 工業自動化和機器人技術的快速普及

- 擴大可再生能源資產(風能、太陽能)

- 商業地產中暖通空調/冷凍設備的擴建

- 軸向磁通AC馬達在電動車領域的興起

- 人工智慧驅動的預測性維護生態系統

- 市場限制

- 銅和稀土元素價格波動

- 高效率馬達的初始成本高

- 電力電子(IGBT)供應鏈中的瓶頸

- 遵守廢舊產品回收及收集義務

- 產業生態系分析

- 監管現狀和標準

- 技術展望(邊緣運算和人工智慧分析)

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 依馬達類型

- AC馬達

- 單相

- 多相

- 同步AC馬達

- 直流勵磁轉子

- 永久磁鐵

- 滯後現象

- 磁阻

- AC馬達

- 按電壓等級

- 低電壓(1千伏特或以下)

- 中壓(1-11kV)

- 高壓(超過11千伏特)

- 按額定輸出

- 小於1千瓦

- 1~100kW

- 100~500 kW

- 超過500千瓦

- 按效率等級

- IE1(標準)

- IE2(高效率)

- IE3(高級版)

- IE4(超級高級版)

- IE5(超高級版)

- 按最終用戶行業分類

- 石油和天然氣

- 化學品/石油化工

- 發電

- 用水和污水

- 金屬和採礦

- 食品/飲料

- 個人作品

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東地區

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 中東

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 供應商排名分析

- 公司簡介

- ABB Ltd.

- Siemens AG

- WEG Equipamentos Eletricos SA

- Nidec Corporation

- Johnson Electric Holdings Limited

- Yaskawa Electric Corporation

- Regal Rexnord Corporation

- Rockwell Automation, Inc.

- Franklin Electric Co., Inc.

- Bosch Rexroth AG

- Kirloskar Electric Company Ltd.

- SEVA-tec GmbH

- Toshiba Corporation

- Mitsubishi Electric Corporation

- TECO Electric & Machinery Co., Ltd.

- Leroy-Somer Holding(Nidec)

- ATB Austria Antriebstechnik AG

- Getriebebau NORD GmbH & Co. KG

- Oriental Motor Co., Ltd.

- Brook Crompton UK Ltd.

第7章 市場機會與未來展望

The alternating current motor market size in 2026 is estimated at USD 18.89 billion, growing from 2025 value of USD 18.29 billion with 2031 projections showing USD 22.24 billion, growing at 3.32% CAGR over 2026-2031.

This growth trajectory is shaped less by green-field capacity additions and more by efficiency-driven replacement cycles mandated by IE3 and IE4 regulations. Premium-efficiency design adoption is expanding across discrete manufacturing, renewable-energy, and HVAC segments, while automation programs in Asia and reshoring efforts in North America sustain baseline demand. Vendor strategies revolve around vertical integration in copper winding, electrical steel, and power electronics to buffer raw-material volatility and semiconductor shortages. Mature end-user sectors such as oil and gas continue to anchor revenues, yet faster growth is migrating toward water treatment, data centers, and wind-turbine auxiliaries, where lifetime energy savings justify premium pricing.

Global Alternating Current (AC) Motor Market Trends and Insights

Mandatory Energy-Efficiency Regulations Drive Premium Motor Adoption

IE3 has become the global compliance floor, and IE4 adoption is accelerating across Europe and the United States, effectively eliminating low-efficiency legacy models from procurement lists. Manufacturers are therefore retooling plants with automated lamination stamping and precision magnet-assembly lines to meet stricter loss limits. The shift burdens smaller regional firms that lack capital for new tooling, consolidating share with global incumbents. Procurement teams now evaluate motors on full-load efficiency at 75% and 50% duty points, which strengthens the value proposition of synchronous permanent-magnet designs. End-users capturing utility rebates for premium motors shorten payback periods to under two years, further reinforcing the regulatory push.

Industrial Automation Accelerates Mid-Range Motor Demand

Automotive, electronics, and logistics facilities are scaling collaborative robot fleets that rely on precision-controlled 1-100 kW motors. Servo-grade synchronous machines equipped with encoders deliver the sub-millimeter accuracy required in robotic welding, pick-and-place, and automated guided vehicles. Integrated drives and on-motor sensors enable torque-vector control, minimizing downtime. Regional incentives for smart factories in China, Japan, and Korea are pulling forward upgrade projects, while North American plants adopt similar architectures under reshoring schemes. Suppliers able to bundle drives, controllers, and analytics software capture premium margins.

Raw-Material Price Volatility Pressures Manufacturing Economics

Copper winding accounts for up to one-quarter of motor material cost, so London Metal Exchange price swings of 18% in 2024 drove quarterly margin compression among OEMs. Permanent-magnet grades of neodymium and dysprosium likewise spiked amid Chinese export policy uncertainty. Manufacturers adopted substitution tactics such as optimized slot fills, aluminum rotor cages, and ferrite-rich magnet compositions. Larger players hedge with multiyear supply contracts and proprietary magnet recycling programs.

Other drivers and restraints analyzed in the detailed report include:

- Renewable-Energy Infrastructure Expands High-Power Motor Applications

- Commercial HVAC Modernization

- Premium Motor Cost Barriers in Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Induction motors retained 69.12% share of the alternating current motor market in 2025 due to their rugged construction and low initial cost. Yet synchronous alternatives are projected at a 5.53% CAGR as permanent-magnet flux densities climb and controller prices fall. The alternating current motor market size for synchronous variants is therefore set to outpace replacements in the installed induction base.

Their premium efficiency appeals to energy-intensive plants, while built-in position feedback supports robotics and conveyor indexing. OEMs bundle synchronous machines with field-oriented drives that simplify commissioning. Although single-phase induction units remain dominant in residential air conditioners, multi-phase synchronous motors now permeate automotive paint shops and SMT lines. The alternating current motor market share gap between the two technologies is expected to narrow over the decade.

Low-voltage (<1 kV) machines delivered 60.88% revenue in 2025 across general manufacturing and HVAC. High-voltage (>11 kV) models, however, show the strongest 5.14% CAGR as wind farms and desalination plants demand multi-megawatt auxiliaries. The alternating current motor market size in high-voltage will therefore rise faster than the mid-voltage segment.

OEMs standardize compact stator slot designs to manage partial-discharge at high voltages, while epoxy-mica insulation systems extend lifetimes in damp offshore nacelles. Grid-code compliance further drives synchronous options with leading power-factor capability. EPC contractors in Brazil and Vietnam increasingly specify high-voltage motors to minimize current and cable losses across long cable runs, enlarging the alternating current motor market share for this class.

The Alternating Current (AC) Motor Market Report is Segmented by Motor Type (Induction AC Motors, and Synchronous AC Motors), Voltage Class (Low, Medium, and High Voltage), Power Rating (less Than 1 KW, 1-100 KW, 100-500 KW, and More), Efficiency Class (IE1-IE5), End-User Industry (Oil and Gas, Chemicals, Power Generation, Water Treatment, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 44.10% of global revenue in 2025. China's high-tech manufacturing rebound spurred precision-motor imports, whereas India's renewable-energy rollout necessitated utility-scale drives for wind and solar assets. Southeast Asian countries such as Vietnam and Thailand are now localizing servo production lines, shrinking import lead times. Government subsidies covering up to 20% of premium-efficiency motor cost accelerate replacements in Korea and Japan.

South America is the fastest-growing region at 4.02% CAGR through 2031. Brazil channels National Development Bank funding toward industrial modernization, lifting orders for IE3-plus motors in petrochemical clusters. Argentina's RenovAr auctions foster wind-farm investment, triggering demand for >500 kW synchronous units. Currency volatility narrows capex windows, but OEMs with Mexican or Brazilian assembly plants hedge exchange-rate risks and secure volume contracts.

North America and Europe remain replacement-driven markets. U.S. reshoring incentives under the CHIPS and IRA acts stimulate greenfield factories requiring mid-range servo arrays. Canada's remote mining operations favor rugged high-power motors with ice-rated bearings. Europe's Ecodesign mandates drive IE4 upgrades across legacy plants. Scandinavian countries specify IE5 for district-heating pumps, while Germany's automotive sector integrates smart-motor plus drive packages, sustaining premium price points. Both regions compensate for slower unit growth with higher average selling prices, stabilizing alternating current motor market share among established brands.

- ABB Ltd.

- Siemens AG

- WEG Equipamentos Eletricos S.A.

- Nidec Corporation

- Johnson Electric Holdings Limited

- Yaskawa Electric Corporation

- Regal Rexnord Corporation

- Rockwell Automation, Inc.

- Franklin Electric Co., Inc.

- Bosch Rexroth AG

- Kirloskar Electric Company Ltd.

- SEVA-tec GmbH

- Toshiba Corporation

- Mitsubishi Electric Corporation

- TECO Electric & Machinery Co., Ltd.

- Leroy-Somer Holding (Nidec)

- ATB Austria Antriebstechnik AG

- Getriebebau NORD GmbH & Co. KG

- Oriental Motor Co., Ltd.

- Brook Crompton UK Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory energy-efficiency regulations (IE3/IE4)

- 4.2.2 Rapid industrial automation and robotics uptake

- 4.2.3 Expansion of renewable-energy assets (wind, solar)

- 4.2.4 HVAC/R build-out in commercial real estate

- 4.2.5 Rise of axial-flux PM AC motors in e-mobility

- 4.2.6 AI-enabled predictive-maintenance ecosystems

- 4.3 Market Restraints

- 4.3.1 Volatile copper and rare-earth metal prices

- 4.3.2 High upfront cost of premium-efficiency motors

- 4.3.3 Power-electronics (IGBT) supply-chain bottlenecks

- 4.3.4 End-of-life recycling and take-back compliance

- 4.4 Industry Ecosystem Analysis

- 4.5 Regulatory Landscape and Standards

- 4.6 Technological Outlook (Edge and AI analytics)

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Motor Type

- 5.1.1 Induction AC Motors

- 5.1.1.1 Single-phase

- 5.1.1.2 Poly-phase

- 5.1.2 Synchronous AC Motors

- 5.1.2.1 DC-excited Rotor

- 5.1.2.2 Permanent-Magnet

- 5.1.2.3 Hysteresis

- 5.1.2.4 Reluctance

- 5.1.1 Induction AC Motors

- 5.2 By Voltage Class

- 5.2.1 Low Voltage (<=1 kV)

- 5.2.2 Medium Voltage (>1-11 kV)

- 5.2.3 High Voltage (>11 kV)

- 5.3 By Power Rating

- 5.3.1 Less than 1 kW

- 5.3.2 1-100 kW

- 5.3.3 100-500 kW

- 5.3.4 Greater than 500 kW

- 5.4 By Efficiency Class

- 5.4.1 IE1 (Standard)

- 5.4.2 IE2 (High)

- 5.4.3 IE3 (Premium)

- 5.4.4 IE4 (Super-Premium)

- 5.4.5 IE5 (Ultra-Premium)

- 5.5 By End-user Industry

- 5.5.1 Oil and Gas

- 5.5.2 Chemicals and Petrochemicals

- 5.5.3 Power Generation

- 5.5.4 Water and Wastewater

- 5.5.5 Metals and Mining

- 5.5.6 Food and Beverage

- 5.5.7 Discrete Manufacturing

- 5.5.8 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 Saudi Arabia

- 5.6.4.1.2 United Arab Emirates

- 5.6.4.1.3 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Egypt

- 5.6.4.2.3 Rest of Africa

- 5.6.4.1 Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Vendor Ranking Analysis

- 6.5 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.5.1 ABB Ltd.

- 6.5.2 Siemens AG

- 6.5.3 WEG Equipamentos Eletricos S.A.

- 6.5.4 Nidec Corporation

- 6.5.5 Johnson Electric Holdings Limited

- 6.5.6 Yaskawa Electric Corporation

- 6.5.7 Regal Rexnord Corporation

- 6.5.8 Rockwell Automation, Inc.

- 6.5.9 Franklin Electric Co., Inc.

- 6.5.10 Bosch Rexroth AG

- 6.5.11 Kirloskar Electric Company Ltd.

- 6.5.12 SEVA-tec GmbH

- 6.5.13 Toshiba Corporation

- 6.5.14 Mitsubishi Electric Corporation

- 6.5.15 TECO Electric & Machinery Co., Ltd.

- 6.5.16 Leroy-Somer Holding (Nidec)

- 6.5.17 ATB Austria Antriebstechnik AG

- 6.5.18 Getriebebau NORD GmbH & Co. KG

- 6.5.19 Oriental Motor Co., Ltd.

- 6.5.20 Brook Crompton UK Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

全球開關式磁阻電動機市場規模、佔有率、趨勢及成長分析報告(2026-2034)

全球開關式磁阻電動機市場規模、佔有率、趨勢及成長分析報告(2026-2034) 同步磁阻馬達(SynRM)-全球市場佔有率和排名、總收入和需求預測(2026-2032)

同步磁阻馬達(SynRM)-全球市場佔有率和排名、總收入和需求預測(2026-2032) 2026年全球中高功率馬達市場報告2026年全球交流電機市場報告2026年全球高速馬達市場報告

2026年全球中高功率馬達市場報告2026年全球交流電機市場報告2026年全球高速馬達市場報告 汽車軸向馬達市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、動力類型、需求類別、地區和競爭格局分類,2021-2031年)

汽車軸向馬達市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、動力類型、需求類別、地區和競爭格局分類,2021-2031年) 開關式磁阻電動機市場按類型、功率、相數、額定電壓、控制方式、應用和最終用戶產業分類,全球預測,2026-2032年全球高速馬達市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析、未來預測(2026-2034)

開關式磁阻電動機市場按類型、功率、相數、額定電壓、控制方式、應用和最終用戶產業分類,全球預測,2026-2032年全球高速馬達市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析、未來預測(2026-2034) 日本低壓馬達市場規模、佔有率、趨勢及預測(按效率、應用、終端用戶產業及地區分類),2026-2034年

日本低壓馬達市場規模、佔有率、趨勢及預測(按效率、應用、終端用戶產業及地區分類),2026-2034年 交流馬達市場規模、佔有率及成長分析(按類型、電壓、應用和地區分類)-2026-2033年產業預測

交流馬達市場規模、佔有率及成長分析(按類型、電壓、應用和地區分類)-2026-2033年產業預測