|

市場調查報告書

商品編碼

1940766

美國零擔貨運 (LTL) 市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)United States Less Than-Truck-Load (LTL) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

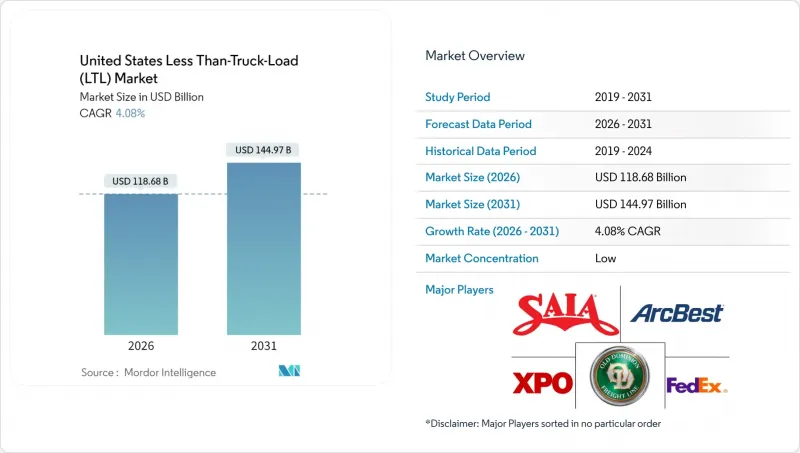

美國零擔貨運 (LTL) 市場預計到 2026 年將達到 1,186.8 億美元,高於 2025 年的 1,140.3 億美元。

預計到 2031 年將達到 1,449.7 億美元,2026 年至 2031 年的複合年成長率為 4.08%。

電子商務履約、國內製造業的回歸以及全通路零售策略正在重塑運輸業格局,而主要都市貨運站的運力限制已將洛杉磯和新澤西等市場的平均倉庫租金推高至每平方英尺8美元以上。由於司機短缺導致人事費用上升、能源價格波動以及Yellow Corp.於2023年退出市場後產業整合加速,加劇了競爭環境,促使區域性承運商收購破產重組後的貨運站。儘管根據《基礎設施投資與就業法案》(IIJA)核准的投資將用於建造卡車專用車道和港口改造,從而提高網路通行效率,但東海岸和墨西哥灣沿岸沿岸的勞工動盪導致貨運路線週期性變更,使得短期服務可靠性存在不確定性。這些因素共同增強了美國零擔貨運(LTL)市場的韌性,因為托運人優先考慮運輸方式的柔軟性、詳細的運輸資訊以及技術驅動的定價模式。

美國零擔貨運 (LTL) 市場趨勢與洞察

電子商務履約的成長

預計到2024年,美國零售電商銷售額將超過1兆美元,零售商正擴大將庫存設在人口中心附近,以便實現一到兩天的配送。這種地理多元化推動了中等重量貨物的運輸頻率增加,這些貨物無法納入小型包裹網路,從而擴大了美國零擔貨運市場的潛在基本客群。像PITT OHIO這樣的托運人正在利用人工智慧最佳化路線,降低25%的人事費用,並縮短服務時間。家具、家電和辦公設備的住宅配送受益於專業的零擔貨運最後一公里服務,這推動了對升降尾板設施和高階服務能力的持續投資。隨著墨西哥產品進入北美大都會圈地區的配送範圍,與近岸外包相關的跨境電商將進一步提升貨運量。從2025年到2030年,隨著零售商尋求以具有競爭力的價格實現穩定的兩天送達服務,美國零擔貨運市場仍將是全通路策略的重要組成部分。

製造業回流主導的國內製造業復甦

超過9,100億美元的聯邦工業激勵措施正在推動汽車、航太、醫療設備和電子產品生產回流美國,並將生產活動集中在35號州際公路及類似走廊沿線。墨西哥預計在2024年成為美國最大的貿易夥伴,這將推動跨境卡車運輸量的成長,而精通海關文件和邊境運輸的零擔貨運公司將從中受益。 Averitt公司擴建位於聖安東尼奧的設施(佔地85,000平方英尺,擁有80個交叉裝卸貨位)正是利用資產佈局來抓住這一成長機會的絕佳例證。附近工廠穩定的零件供應提高了物流密度,為擁有戰略性樞紐的承運商提供了更優的網路經濟效益和定價優勢。因此,美國小包裹運輸市場在區域化供應鏈中扮演越來越重要的角色,這些供應鏈能夠抵禦跨太平洋運輸中斷的影響。

司機短缺和勞動力老化

藥物和酒精檢測資訊交換中心的實施可能會導致多達17.7萬名司機失業,而目前約有三分之一的駕駛人即將退休,這可能會進一步減少可用勞動力。為了應對這一局面,貨運公司正在提高工資(例如,Averitt公司計劃在2025年將其危險品運輸司機的薪水從每英里0.60美元提高到0.64美元),並將20%的利潤分配給員工退休帳戶以提高員工留任率。然而,薪資上漲推高了營運比率,迫使貨運公司重新思考公路規劃、提高裝載率,並透過實施車道維持系統等駕駛輔助技術來延長駕駛人的職業生涯。儘管貨運供需環境良好,但持續的招募挑戰仍限制著美國小型包裹運輸市場的成長。

細分市場分析

到2025年,批發和零售業將占美國零擔貨運市場的34.56%,預計2026年至2031年將以5.13%的複合年成長率成長,成長速度超過其他所有行業,因為零售商正加速將商品囤積在更靠近消費地的地方。製造業仍是第二大貢獻者,這得益於零件透過內陸樞紐向北近岸外包。建築業、農業和能源產業雖然存在季節性波動,但它們共同提高了次市場的線路密度,否則這些市場將面臨運力失衡的問題。

由於零售業履約需要透過微型倉配和暗店模式快速補貨,中等重量的貨物擴大採用零擔運輸(LTL),而非整車運輸或小包裹運輸。人工智慧增強的需求預測降低了大型連鎖店的庫存持有成本,但也導致運輸頻率增加,最終擴大了美國零擔運輸市場。製造業貨物,特別是汽車零件和機械,平衡了南北運輸路線,減少了空駛里程,並支持了網路經濟效益。因此,美國零擔運輸業保持了穩定的收入結構,並透過垂直多元化降低了該行業的周期性波動。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 按經濟活動分類的GDP分配

- 按經濟活動分類的GDP成長

- 經濟表現及概覽

- 電子商務產業的趨勢

- 製造業趨勢

- 運輸和倉儲業的GDP

- 物流績效

- 道路長度

- 出口趨勢

- 進口趨勢

- 燃油價格趨勢

- 卡車運輸營運成本

- 卡車運輸車隊規模(按類型)

- 主要卡車供應商

- 公路貨運量趨勢

- 公路貨運價格趨勢

- 透過交通方式分享

- 通貨膨脹

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 電子商務履約的成長

- 製造業回流主導的國內製造業復甦

- 全通路零售網路最佳化

- 將都市區零售地產改造為交叉轉運微型樞紐

- 透過 API 支援將運輸方式從小包裹轉換為零擔運輸(適用於中小托運人)

- 《基礎建設投資與就業法案》(IIJA) 卡車專用道投資提升零擔貨運可靠性

- 市場限制

- 促進要素短缺和勞動力老化

- 柴油價格波動

- 主要都會區面臨嚴重的碼頭運能限制

- 倉庫工會化的連鎖反應

- 市場創新

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 終端用戶產業

- 農業、漁業、林業

- 建設業

- 製造業

- 石油天然氣、採礦和採石

- 批發和零售

- 其他

- 目的地

- 國內的

- 國際的

第6章 競爭情勢

- 市場集中度

- 關鍵策略舉措

- 市佔率分析

- 公司簡介

- A. Duie Pyle, Inc.

- ArcBest

- Averitt Express, Inc.

- CH Robinson

- Day & Ross

- Daylight Transport, LLC

- Dayton Freight Lines, Inc.

- DHL Group

- Estes Express Lines

- Fastfrate Inc.

- FedEx

- Knight-Swift Transportation Holdings Inc.

- Landstar System Inc.

- Oak Harbor Freight Lines, Inc.

- Old Dominion Freight Line

- Pitt Ohio Transportation Group

- R+L Carriers, Inc.

- Roadrunner Freight

- Saia Inc.

- Schneider National, Inc.

- Southeastern Freight Lines

- TFI International Inc.

- United Parcel Service of America, Inc.(UPS)

- Ward Transport and Logistics Corporation

- Werner Enterprises Inc.

- XPO, Inc.

第7章 市場機會與未來展望

The United States Less than-Truck-Load market size in 2026 is estimated at USD 118.68 billion, growing from 2025 value of USD 114.03 billion with 2031 projections showing USD 144.97 billion, growing at 4.08% CAGR over 2026-2031.

E-commerce fulfillment, reshoring of domestic manufacturing, and omnichannel retail strategies are re-shaping shipment profiles, while capacity constraints in tier-1 metropolitan terminals have elevated average warehouse lease rates above USD 8 per square foot in markets such as Los Angeles and New Jersey. Rising labor costs linked to driver shortages, energy price volatility, and heightened consolidation following Yellow Corporation's 2023 exit are intensifying competitive dynamics and encouraging regional carriers to acquire terminals released by the bankruptcy estate. Investments authorized under the Infrastructure Investment and Jobs Act (IIJA) are earmarked for truck-only lanes and port upgrades that will enhance network fluidity, yet near-term service reliability remains sensitive to East and Gulf Coast labor disruptions that periodically reroute freight flows. Collectively, these factors reinforce the resilience of the United States Less than-Truck-Load market as shippers favor mode flexibility, granular visibility, and technology-enabled pricing models.

United States Less Than-Truck-Load (LTL) Market Trends and Insights

E-commerce Fulfillment Growth

United States retail e-commerce sales surpassed USD 1 trillion in 2024, prompting retailers to position inventory within one- to two-day ground zones around dense population centers. This geographic dispersion increases the frequency of medium-weight shipments unsuitable for parcel networks, thereby enlarging the addressable base of the United States Less than-Truck-Load market. Carriers such as PITT OHIO apply artificial-intelligence-driven route optimization to reduce labor costs by 25% and sharpen service windows. Residential deliveries of furniture, appliances, and office equipment yield higher margins when carried through specialized LTL final-mile services, encouraging ongoing investment in lift-gate equipment and white-glove capabilities. Cross-border e-commerce related to nearshoring further lifts volumes as Mexican-origin goods flow north into metropolitan delivery zones. As retailers seek consistent two-day performance at competitive rates, the United States Less than-Truck-Load market will remain integral to omnichannel fulfillment strategies across 2025-2030.

Reshoring-Led Domestic Manufacturing Rebound

Federal industrial incentives exceeding USD 910 billion stimulate the onshoring of automotive, aerospace, medical device, and electronics production, concentrating activity along the Interstate 35 corridor and similar arteries. Mexico ascended to the United States' top trading partner position in 2024, raising cross-border truck traffic that benefits LTL carriers adept at customs documentation and border drayage. Averitt's 85,000 ft2 San Antonio expansion featuring 80 cross-dock doors typifies asset deployment aimed at capturing this surge. Predictable component flows from nearshore plants allow density gains, translating into superior network economics and pricing leverage for carriers with strategically located terminals. The United States Less than-Truck-Load market consequently deepens its role in regionalized supply chains designed for resilience against trans-Pacific disruptions.

Driver Shortage and Aging Workforce

Drug and Alcohol Clearinghouse enforcement could remove up to 177,000 drivers, reducing the effective labor pool even as nearly one-third of current operators are near retirement age. Carriers counter by hiking pay-Averitt lifted hazmat driver rates from USD 0.60 to USD 0.64 per mile in 2025-and by channeling 20% of profits into employee retirement accounts to boost retention. Yet wage escalation inflates operating ratios, compelling carriers to refine linehaul planning, increase load factors, and introduce driver-assisting technology such as lane-keeping systems to lengthen career longevity. Persistent recruitment hurdles continue to weigh on the United States Less than-Truck-Load market growth trajectory despite healthy freight fundamentals.

Other drivers and restraints analyzed in the detailed report include:

- Omnichannel Retail Network Optimization

- Urban Retail Real-Estate Repurposed into Cross-Dock Micro-Hubs

- Acute Terminal-Capacity Constraints in Tier-1 Metros

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wholesale and Retail Trade accounted for 34.56% of the United States less than-truck-load market size in 2025 and is advancing at a 5.13% CAGR between 2026-2031, outpacing every other vertical as retailers recalibrate inventory closer to consumption points. Manufacturing remains the second-largest contributor, buoyed by nearshoring that channels components northbound through inland hubs. Construction, Agriculture, and Energy add variability across seasons, yet together strengthen lane density in secondary markets where capacity would otherwise be imbalanced.

Retail fulfillment's requirement for rapid restocking of micro-fulfillment and dark-store formats means medium-weight loads ride LTL more often than truckload or parcel. AI-enhanced demand sensing has trimmed inventory carrying costs for large chains, yet it raises shipment frequency, a factor that ultimately expands the United States Less than-Truck-Load market. Manufacturing traffic, especially auto parts and machinery, keeps south-to-north routes balanced, reducing empty miles and undergirding network economics. The United States Less than-Truck-Load industry thus maintains a stable revenue mix, mitigating sector cyclicality through vertical diversification.

The United States Less Than-Truck-Load (LTL) Market Report is Segmented by End User Industry (Agriculture, Fishing, and Forestry, Construction, Manufacturing, Oil and Gas, Mining and Quarrying, Wholesale and Retail Trade, and Others), and Destination (Domestic and International). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- A. Duie Pyle, Inc.

- ArcBest

- Averitt Express, Inc.

- C.H. Robinson

- Day & Ross

- Daylight Transport, LLC

- Dayton Freight Lines, Inc.

- DHL Group

- Estes Express Lines

- Fastfrate Inc.

- FedEx

- Knight-Swift Transportation Holdings Inc.

- Landstar System Inc.

- Oak Harbor Freight Lines, Inc.

- Old Dominion Freight Line

- Pitt Ohio Transportation Group

- R+L Carriers, Inc.

- Roadrunner Freight

- Saia Inc.

- Schneider National, Inc.

- Southeastern Freight Lines

- TFI International Inc.

- United Parcel Service of America, Inc. (UPS)

- Ward Transport and Logistics Corporation

- Werner Enterprises Inc.

- XPO, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 GDP Distribution by Economic Activity

- 4.3 GDP Growth by Economic Activity

- 4.4 Economic Performance and Profile

- 4.4.1 Trends in E-Commerce Industry

- 4.4.2 Trends in Manufacturing Industry

- 4.5 Transport and Storage Sector GDP

- 4.6 Logistics Performance

- 4.7 Length of Roads

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Pricing Trends

- 4.11 Trucking Operational Costs

- 4.12 Trucking Fleet Size by Type

- 4.13 Major Truck Suppliers

- 4.14 Road Freight Tonnage Trends

- 4.15 Road Freight Pricing Trends

- 4.16 Modal Share

- 4.17 Inflation

- 4.18 Regulatory Framework

- 4.19 Value Chain and Distribution Channel Analysis

- 4.20 Market Drivers

- 4.20.1 E-Commerce Fulfilment Growth

- 4.20.2 Reshoring-Led Domestic Manufacturing Rebound

- 4.20.3 Omnichannel Retail Network Optimisation

- 4.20.4 Urban Retail Real-Estate Repurposed into Cross-Dock Micro-Hubs

- 4.20.5 API-Enabled Parcel-To-LTL Mode Shift For SMB Shippers

- 4.20.6 Truck-Only Lane Investments Under the IIJA Boosting LTL Transit Reliability

- 4.21 Market Restraints

- 4.21.1 Driver Shortage and Ageing Workforce

- 4.21.2 Diesel-Price Volatility

- 4.21.3 Acute Terminal-Capacity Constraints in Tier-1 Metros

- 4.21.4 Warehouse Labour Unionisation Ripple-Effects

- 4.22 Technology Innovations in the Market

- 4.23 Porter's Five Forces Analysis

- 4.23.1 Threat of New Entrants

- 4.23.2 Bargaining Power of Buyers

- 4.23.3 Bargaining Power of Suppliers

- 4.23.4 Threat of Substitutes

- 4.23.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Destination

- 5.2.1 Domestic

- 5.2.2 International

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 A. Duie Pyle, Inc.

- 6.4.2 ArcBest

- 6.4.3 Averitt Express, Inc.

- 6.4.4 C.H. Robinson

- 6.4.5 Day & Ross

- 6.4.6 Daylight Transport, LLC

- 6.4.7 Dayton Freight Lines, Inc.

- 6.4.8 DHL Group

- 6.4.9 Estes Express Lines

- 6.4.10 Fastfrate Inc.

- 6.4.11 FedEx

- 6.4.12 Knight-Swift Transportation Holdings Inc.

- 6.4.13 Landstar System Inc.

- 6.4.14 Oak Harbor Freight Lines, Inc.

- 6.4.15 Old Dominion Freight Line

- 6.4.16 Pitt Ohio Transportation Group

- 6.4.17 R+L Carriers, Inc.

- 6.4.18 Roadrunner Freight

- 6.4.19 Saia Inc.

- 6.4.20 Schneider National, Inc.

- 6.4.21 Southeastern Freight Lines

- 6.4.22 TFI International Inc.

- 6.4.23 United Parcel Service of America, Inc. (UPS)

- 6.4.24 Ward Transport and Logistics Corporation

- 6.4.25 Werner Enterprises Inc.

- 6.4.26 XPO, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment