|

市場調查報告書

商品編碼

1940759

NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)NOR Flash - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

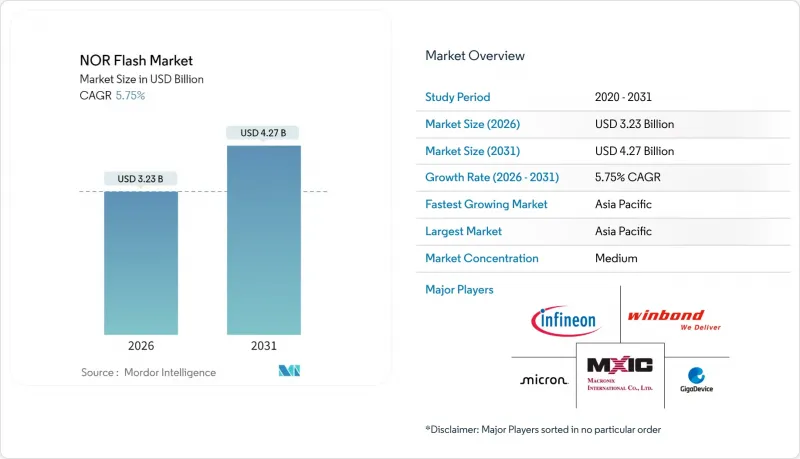

預計 NOR 快閃記憶體市場在 2025 年的價值為 30.5 億美元,從 2026 年的 32.3 億美元成長到 2031 年的 42.7 億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 5.75%。

成長勢頭反映了高級駕駛輔助系統 (ADAS) 內容的不斷增加、物聯網邊緣節點應用的日益廣泛以及工業自動化領域投資的重新成長。串行架構因其引腳數少、尺寸緊湊和能源效率高等優勢而佔據主導地位,使其非常適合空間受限的產品。介面升級,特別是四路和八路 SPI,正在提高讀取頻寬,從而實現更快的啟動速度和更豐富的程式碼執行。製造商也在積極回應,推出低電壓元件、車規級功能安全認證以及早期 3D NOR 晶片試點項目,這些產品在不犧牲可靠性的前提下提高了密度。

全球NOR快閃記憶體市場趨勢與洞察

韌體密集型ADAS和網域控制器推動了對汽車級NOR的需求

汽車平台正從分散式電控系統 ( ECU) 轉型為採用集中式即時韌體的域/區域架構。 NOR 快閃記憶體具有確定性的讀取延遲和即時執行能力,這些特性有助於實現功能安全目標。英飛凌獲得 ASIL-D 認證的 SEMPER 系列產品展示了整合錯誤檢查和雙庫冗餘如何增強程式碼儲存的可靠性。 Level 2+ 和 Level 3 功能的普及推動了對 512Mb 至 2Gb 系列 NOR 快閃記憶體產品的需求,預計到 2030 年,汽車 NOR 快閃記憶體的出貨量將以 7.13% 的複合年成長率成長。

全球製造地採用四路/八路 SPI 實現物聯網邊緣設備的快速啟動

儘管四路 SPI 已佔據物聯網程式碼儲存插槽的一半以上,但八路/xSPI 正在崛起,因為它能將持續讀取頻寬提升至 400 MB/s,並將下載時間縮短一半。 Synopsys 報告稱,與平行記憶體相比,xSPI 減少了引腳數量開銷,簡化了 PCB 佈線並降低了物料成本。 GigaDevice 的 GD25LX 系列可將韌體載入時間縮短 80%,從而實現邊緣即時分析。這種吞吐量優勢使得工業環境中能夠實現更高級的感測器融合和空中升級 (OTA) 功能。

容量超過 256Mb 的 NAND 快閃記憶體價格溢價是高密度快閃記憶體產品普及的一大障礙。

當程式碼大小超過 256Mb 時,串列NAND和 eMMC 由於每位元成本低 2-5 倍,正逐漸取代 NOR 快閃記憶體。廠商也紛紛推出混合設計方案,例如千兆裝置上的 QSPI NAND,以兼具 NAND 快閃記憶體的經濟性,提供與 NOR 快閃記憶體相近的隨機讀取效能。然而,高密度消費性電子設備在選擇 NOR 快閃記憶體之前,仍會繼續評估系統總成本。

細分市場分析

到2025年,串行產品將佔據88.67%的市場佔有率,這反映了其4-6引腳介面、小型封裝和易於組裝等優勢。並行NOR門在真正需要隨機位元組存取的領域仍然很重要,例如抬頭顯示器和故障安全叢集,但隨著微控制器和FPGA廠商轉向串行程式碼存儲,其市場佔有率正在萎縮。

元件供應商將串列 NOR 快閃記憶體與預先檢驗的驅動程式堆疊捆綁在一起,從而縮短了 OEM 廠商的產品上市時間。新興的 3D NOR 快閃記憶體原型首先以串列封裝形式出現,為該架構帶來了更高的密度和成本優勢。因此,在未來十年,NOR 快閃記憶體市場將繼續支援串列裝置的藍圖。

到 2025 年,四路 SPI 將佔總收入的 40.72%,成為主流微控制器的主要驅動力。隨著裝置容量達到峰值,該細分市場的複合年成長率將放緩,而八路/xSPI 將以 7.15% 的速度成長,滿足需要即時啟動 Linux 和 AUTOSAR 鏡像的工作負載需求。八路 SPI 也符合 JEDEC xSPI通訊協定,使 NOR Flash 能夠擴大其在汽車一級供應商和工業系統整合商中的市場佔有率,這些供應商和整合商更重視引腳相容性而非儲存密度。

預計到 2031 年,支援八進位/xSPI 的 NOR Flash 市場規模將顯著成長。向下相容的軟體介面簡化了遷移過程,使設計人員能夠在不更改基板設計的情況下逐步提升頻寬。供應商正透過將介面演進與安全性和功能安全選項結合,瞄準高階插槽市場。

由於適用於高級資訊娛樂主機和可程式邏輯控制器,容量超過 256Mb 的設備將在 2025 年佔據 19.94% 的市場佔有率,而容量低於 64Mb(高於 32Mb)的零件將以 8.12% 的速度成長,因為它們為韌體物聯網節點提供了容量和成本的良好平衡。

高密度晶片藍圖利用堆疊晶粒和新興的3D佈局來緩解平面縮放的限制。然而,32-64Mb插槽的銷售成長最為強勁,因為邊緣設備的代碼擴展與嚴格的組件成本限制之間存在衝突。供應商提供跨密度等級的引腳相容升級方案,最大限度地減少OEM廠商的重新設計負擔。

NOR Flash市場按類型(串行、平行)、介面(例如,SPI單/雙介面)、容量(例如,低於2Mb)、電壓(例如,3V級)、終端用戶應用(例如,家用電子電器)、製程節點(例如,90nm及以上)、封裝類型(例如,WLCSP/CSP)和地區(例如,北美)進行細分。市場預測以價值(美元)和數量(單位)為單位。

區域分析

預計到2025年,亞太地區將佔NOR快閃記憶體市場收入的約60.55%,並預計到2031年將顯著成長。中國為提高半導體自給自足能力所做的努力,促使大量資金流入55奈米和40奈米製程的量產生產線,並將區域採購轉向國內供應商。台灣地區繼續佔據全球晶圓供應的大部分佔有率,儘管面臨地緣政治風險,仍為外部客戶提供支援。日本和韓國透過其歷史悠久的晶圓廠做出貢獻,鎧俠(Kioxia)位於北上的新二期晶圓廠預計將於2025年底開始分階段增加產能。

北美是一個高階市場,專注於汽車、工業和航太設計。政府在《晶片法案》(CHIPS Act)的支持下,正推動本地晶圓產能提升和先進封裝計劃的發展,從而實現供應多元化,擺脫對海外代工廠的依賴。美光科技正在拓展其面向汽車應用的NOR記憶體產品組合,而理想汽車的跨域控制器則是中國電動車採用美國製造記憶體的一個例證。

歐洲維持著與NOR功能安全特性相符的嚴格可靠性和可追溯性標準。總部位於德國的英飛凌正在為一級汽車製造商和工業4.0原始設備製造商建造本土供應鏈。歐盟政策制定者正在投資建立一個具有韌性的半導體生態系統,這有望增強NOR供應商的需求前景,同時降低該地區對亞洲晶圓代工廠的依賴。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 韌體密集型ADAS和網域控制器推動了對汽車級NOR的需求

- 快速啟動型物聯網邊緣設備的四路/八路SPI採用趨勢(依全球製造地分類)

- 衛星群級低地球軌道衛星需要抗輻射的NOR快閃記憶體元件

- 中國正努力利用55nm和40nm製程技術提升NOR記憶體的自給自足能力。

- 工業4.0工廠強制要求安全啟動和OTA更新

- 低功耗 1.8V 串列 NOR 記憶體(適用於穿戴式/照護現場醫療設備)

- 市場限制

- 容量超過 256Mb 的 NAND 快閃記憶體成本溢價限制了高密度消費產品的普及。

- 45nm製程規模擴展的限制/開機OEM藍圖轉向MRAM/ReRAM替代方案

- 台灣晶圓代工廠集中度高,有供應鏈中斷的風險。

- 中國產能擴張將降低平均售價,進而影響供應商的利潤率。

- 價值/供應鏈分析

- 宏觀趨勢影響分析

- 監理與技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 定價分析

- 投資分析

第5章 市場規模與成長預測

- 按類型

- 串行 NOR 快閃記憶體

- 並行 NOR 快閃記憶體

- 透過介面

- SPI 單/雙

- 四路 SPI

- 八進位和xSPI

- 按密度

- NOR 低於 2 Mbit

- NOR 最高可達 4 Mbit(超過 2 Mbit)

- <8 Mbit (>4 Mbit) NOR

- <16 Mbit (>8 Mbit) NOR

- 32Mbit 或更低(超過 16Mbit)NOR

- 64Mbit 或更低(超過 32Mbit)NOR

- 128Mbit 或更低(超過 64MB)NOR

- 256Mbit 或更低(超過 128MB)NOR

- 超過 256 兆比特

- 透過電壓

- 3V級

- 1.8V 類

- 寬電壓(1.65V 至 3.6V)

- 其他 - 1.2V 級(以及低於 1.8V 的類似級)(2.5V、5V 等)

- 透過最終用戶應用程式

- 家用電子電器

- 溝通

- 車

- 產業

- 其他用途

- 依製程技術節點

- 90奈米及更早

- 65nm

- 55奈米(包括58奈米)

- 45nm

- 28奈米或更小

- 按包裝類型

- WLCSP/CSP

- QFN/SOIC

- BGA/FBGA

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 台灣

- 印度

- 東南亞

- 亞太其他地區

- 世界其他地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Winbond Electronics Corporation

- Macronix International Co. Ltd.

- GigaDevice Semiconductor Inc.

- Infineon Technologies AG

- Micron Technology Inc.

- Integrated Silicon Solution Inc.

- Microchip Technology Inc.

- Renesas Electronics Corporation

- Elite Semiconductor Microelectronics Technology Inc.

- Wuhan XMC

- Puya Semiconductor(Shanghai)Co. Ltd.

- Samsung Semiconductor

- Alliance Memory

- Zbit Semiconductor

- YMTC-Xi'an Longsys

- Fudan Microelectronics Group Co. Ltd.

- AMIC Technology Corporation

- BOYA Microelectronics Co. Ltd.

- XTX Technology(Shenzhen)Limited

- Shenzhen Longsys Electronics Co. Ltd.

第7章 市場機會與未來展望

The NOR flash market was valued at USD 3.05 billion in 2025 and estimated to grow from USD 3.23 billion in 2026 to reach USD 4.27 billion by 2031, at a CAGR of 5.75% during the forecast period (2026-2031).

Growth momentum reflects rising content in advanced driver-assistance systems (ADAS), wider use in IoT edge nodes, and renewed investment in industrial automation. Serial architectures dominate because their low pin count, compact footprint, and energy efficiency align with space-constrained products. Interface upgrades-especially Quad and Octal SPI-are lifting read bandwidths, enabling faster boot and richer code execution. Manufacturers are also responding with lower-voltage parts, automotive-grade functional-safety certifications, and early 3D NOR pilots that raise density without sacrificing reliability.

Global NOR Flash Market Trends and Insights

Firmware-intensive ADAS and Domain Controllers Accelerating Automotive-grade NOR Demand

Automotive platforms are migrating from distributed electronic control units to domain and zone architectures that centralize real-time firmware. NOR Flash delivers deterministic read latency and instant-on execution, attributes that underpin functional safety targets. Infineon's SEMPER family, now ASIL-D certified, demonstrates how integrated error-checking and dual-bank redundancy strengthen code-storage resilience. As Level 2+ and Level 3 features proliferate, demand for 512 Mb-2 Gb serial parts is rising, propelling automotive NOR volumes at 7.13% CAGR through 2030.

Quad/Octal SPI Adoption for Fast-Boot IoT Edge Devices across Global Manufacturing Hubs

Quad SPI already powers more than half of IoT code-storage sockets, yet Octal/xSPI is emerging because it pushes sustained read bandwidths to 400 MB/s while halving download times. Synopsys reports that xSPI cuts pin-count overhead versus parallel memory, easing PCB routing and lowering BOM cost. GigaDevice's GD25LX series shows an 80% reduction in firmware load time, enabling real-time analytics at the edge. This throughput benefit is unlocking richer sensor-fusion and over-the-air update features in industrial settings.

Cost Premium over NAND Above 256 Mb Limiting High-Density Consumer Adoption

When code size grows beyond 256 Mb, Serial NAND or eMMC often displace NOR because they offer two to five times lower cost per bit. Vendors are countering with hybrid designs, such as GigaDevice's QSPI NAND-that deliver NOR-like random read at NAND economics. Nevertheless, high-density consumer devices will continue to evaluate total system cost before selecting NOR.

Other drivers and restraints analyzed in the detailed report include:

- Constellation-Scale LEO Satellites Requiring Radiation-Hardened NOR Flash Devices

- China's 55 nm and 40 nm Indigenous Process Push for NOR Self-Sufficiency

- Scaling Ceilings Beyond 45 nm Steering OEM Roadmaps Toward MRAM/ReRAM Substitutes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Serial products supplied 88.67% of the 2025 market share, reflecting their four-to-six-pin interface, smaller packages, and lower assembly complexity. Parallel NOR remains relevant where true random byte access is mandatory, such as heads-up displays and fail-safe clusters, but its footprint is narrowing as microcontroller and FPGA suppliers migrate to serial code storage.

Component vendors bundle Serial NOR with pre-verified driver stacks, accelerating time-to-market for OEMs. Emerging 3D NOR prototypes will debut first in serial footprints, giving the architecture another density and cost tailwind. In this context, the NOR Flash market continues to favor Serial device roadmaps through the decade.

Quad SPI delivered 40.72% revenue in 2025, underpinning mainstream microcontrollers. The segment's CAGR eases as installed bases peak, while Octal/xSPI climbs at 7.15% on workloads that need instant-on Linux or AUTOSAR images. Octal also aligns with JEDEC xSPI protocol, enabling NOR Flash market share gains among automotive Tier 1s and industrial SIs that value pin compatibility across densities.

The NOR Flash market size for Octal/xSPI parts is projected to jump significantly by 2031. Backward-compatible software hooks ease migration; hence, designers can phase-upgrade bandwidth without board redesign. Suppliers are merging interface advancements with security and functional-safety options to target premium sockets.

Devices with greater than 256 Mb captured 19.94% market share in 2025 due to their suitability for sophisticated infotainment head units and programmable logic controllers. Meanwhile, 64-Mb-and-less (greater than 32 Mb) parts grow fastest at 8.12% because they balance capacity and cost for firmware-rich IoT nodes.

Higher-density roadmaps leverage stacked-die or emerging 3D layouts to mitigate planar scaling ceilings. However, volume growth will remain strongest in 32-64 Mb sockets where code expansion in edge devices collides with tight bill-of-materials constraints. Vendors provide pin-compatible upgrade paths across density steps, minimizing redesign effort for OEMs.

NOR Flash Market is Segmented by Type (Serial, Parallel), Interface (SPI Single/Dual, and More), Density (2 Mb and Less, and More), Voltage (3V Class, and More), End-User Application (Consumer Electronics, and More), Process Technology Node (90 Nm and Older, and More), Packaging Type (WLCSP/CSP, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia Pacific controlled about 60.55% of the NOR Flash market revenue in 2025 and is projected to expand significantly by 2031. China's semiconductor self-sufficiency drive has drawn considerable capital toward 55 nm and 40 nm serial lines, shifting regional procurement toward domestic vendors. Taiwan continues to supply a significant portion of global wafers, anchoring external customers despite geopolitical risk. Japan and South Korea contribute through long-established fabs; Kioxia's new Kitakami Fab 2 will add incremental capacity starting late 2025.

North America represents a premium segment specialized in automotive, industrial, and aerospace designs. Government incentives under the CHIPS Act are catalyzing local wafer starts and advanced-packaging projects, diversifying supply away from overseas foundries. Micron is broadening its automotive NOR portfolio, with Li Auto's cross-domain controller an illustration of U.S. memory inside Chinese EVs.

Europe maintains strict reliability and traceability standards that align with NOR's functional-safety traits. Infineon's headquarters in Germany anchors a domestic supply chain serving Tier 1 automotive and Industry 4.0 OEMs. EU policymakers are channeling funds toward a resilient semiconductor ecosystem, which could ease the region's dependence on Asian foundries while strengthening demand visibility for NOR suppliers.

- Winbond Electronics Corporation

- Macronix International Co. Ltd.

- GigaDevice Semiconductor Inc.

- Infineon Technologies AG

- Micron Technology Inc.

- Integrated Silicon Solution Inc.

- Microchip Technology Inc.

- Renesas Electronics Corporation

- Elite Semiconductor Microelectronics Technology Inc.

- Wuhan XMC

- Puya Semiconductor (Shanghai) Co. Ltd.

- Samsung Semiconductor

- Alliance Memory

- Zbit Semiconductor

- YMTC - Xi'an Longsys

- Fudan Microelectronics Group Co. Ltd.

- AMIC Technology Corporation

- BOYA Microelectronics Co. Ltd.

- XTX Technology (Shenzhen) Limited

- Shenzhen Longsys Electronics Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Firmware-intensive ADAS and Domain Controllers Accelerating Automotive-grade NOR Demand

- 4.2.2 Quad/Octal SPI Adoption for Fast-Boot IoT Edge Devices across Global Manufacturing Hubs

- 4.2.3 Constellation-Scale LEO Satellites Requiring Radiation-Hardened NOR Flash Devices

- 4.2.4 China's 55 nm and 40 nm Indigenous Process Push for NOR Self-Sufficiency

- 4.2.5 Secure Boot and OTA Update Mandates in Industry 4.0 Factories

- 4.2.6 Low-Power 1.8 V Serial NOR for Wearable/Point-of-Care Healthcare Electronics

- 4.3 Market Restraints

- 4.3.1 Cost Premium over NAND Above 256 Mb Limiting High-Density Consumer Adoption

- 4.3.2 Scaling Ceilings Beyond 45 nm Steering OEM Roadmaps Toward MRAM/ReRAM Substitutes

- 4.3.3 Foundry Concentration in Taiwan Exposing Supply-Chain Disruption Risk

- 4.3.4 ASP Compression from Expanding Chinese Capacity Impacting Vendor Margins

- 4.4 Value / Supply-Chain Analysis

- 4.5 Macro Trend Impact Analysis

- 4.6 Regulatory and Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, VOLUME)

- 5.1 By Type (Value, Volume)

- 5.1.1 Serial NOR Flash

- 5.1.2 Parallel NOR Flash

- 5.2 By Interface (Value)

- 5.2.1 SPI Single / Dual

- 5.2.2 Quad SPI

- 5.2.3 Octal and xSPI

- 5.3 By Density (Value)

- 5.3.1 2 Megabit And Less NOR

- 5.3.2 4 Megabit And Less-NOR (greater than 2mb) NOR

- 5.3.3 8 Megabit And Less (greater than 4mb) NOR

- 5.3.4 16 Megabit And Less (greater than 8mb) NOR

- 5.3.5 32 Megabit And Less (greater than 16mb) NOR

- 5.3.6 64 Megabit And Less (greater than 32mb) NOR

- 5.3.7 128 Megabit and Less (greater than 64MB) NOR

- 5.3.8 256 Megabit and Less (greater than 128MB) NOR

- 5.3.9 Greater than 256 Megabit

- 5.4 By Voltage (Value)

- 5.4.1 3 V Class

- 5.4.2 1.8 V Class

- 5.4.3 Wide-Voltage (1.65 V - 3.6 V)

- 5.4.4 Others - 1.2V Class (and similar sub-1.8V) (2.5V, 5V, etc.)

- 5.5 By End-user Application (Value, Volume)

- 5.5.1 Consumer Electronics

- 5.5.2 Communication

- 5.5.3 Automotive

- 5.5.4 Industrial

- 5.5.5 Other Applications

- 5.6 By Process Technology Node (Value)

- 5.6.1 90 nm and Older

- 5.6.2 65 nm

- 5.6.3 55 nm (including 58 nm)

- 5.6.4 45 nm

- 5.6.5 28 nm and Below

- 5.7 By Packaging Type (Value)

- 5.7.1 WLCSP / CSP

- 5.7.2 QFN / SOIC

- 5.7.3 BGA / FBGA

- 5.7.4 Others

- 5.8 By Geography (Value, Volume)

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Mexico

- 5.8.2 Europe

- 5.8.2.1 Germany

- 5.8.2.2 France

- 5.8.2.3 United Kingdom

- 5.8.2.4 Italy

- 5.8.2.5 Rest of Europe

- 5.8.3 Asia-Pacific

- 5.8.3.1 China

- 5.8.3.2 Japan

- 5.8.3.3 South Korea

- 5.8.3.4 Taiwan

- 5.8.3.5 India

- 5.8.3.6 South East Asia

- 5.8.3.7 Rest of Asia-Pacific

- 5.8.4 Rest of the World

- 5.8.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Winbond Electronics Corporation

- 6.4.2 Macronix International Co. Ltd.

- 6.4.3 GigaDevice Semiconductor Inc.

- 6.4.4 Infineon Technologies AG

- 6.4.5 Micron Technology Inc.

- 6.4.6 Integrated Silicon Solution Inc.

- 6.4.7 Microchip Technology Inc.

- 6.4.8 Renesas Electronics Corporation

- 6.4.9 Elite Semiconductor Microelectronics Technology Inc.

- 6.4.10 Wuhan XMC

- 6.4.11 Puya Semiconductor (Shanghai) Co. Ltd.

- 6.4.12 Samsung Semiconductor

- 6.4.13 Alliance Memory

- 6.4.14 Zbit Semiconductor

- 6.4.15 YMTC - Xi'an Longsys

- 6.4.16 Fudan Microelectronics Group Co. Ltd.

- 6.4.17 AMIC Technology Corporation

- 6.4.18 BOYA Microelectronics Co. Ltd.

- 6.4.19 XTX Technology (Shenzhen) Limited

- 6.4.20 Shenzhen Longsys Electronics Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet Need Analysis

2026年全球金屬氧化物半導體(MOS)微處理器市場報告2026年全球金屬氧化物半導體(MOS)標準單元和現場可程式邏輯市場報告

2026年全球金屬氧化物半導體(MOS)微處理器市場報告2026年全球金屬氧化物半導體(MOS)標準單元和現場可程式邏輯市場報告 人工智慧記憶體市場預測至2034年—按記憶體類型、組件、部署模式、技術、應用和地區分類的全球分析2026年全球快閃記憶體市場報告2026年全球金屬氧化物半導體(MOS)記憶體市場報告2026年全球存取記憶體和顯示器市場報告

人工智慧記憶體市場預測至2034年—按記憶體類型、組件、部署模式、技術、應用和地區分類的全球分析2026年全球快閃記憶體市場報告2026年全球金屬氧化物半導體(MOS)記憶體市場報告2026年全球存取記憶體和顯示器市場報告 快閃記憶體控制器市場按NAND類型、介面類型、外形規格、應用和最終用戶分類,全球預測(2026-2032年)

快閃記憶體控制器市場按NAND類型、介面類型、外形規格、應用和最終用戶分類,全球預測(2026-2032年) NOR快閃記憶體市場分析及預測(至2035年):依類型、產品類型、技術、應用、設備、最終用戶、組件、製程、部署類型及功能分類加密隨身碟市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、形狀、材質及最終用戶分類2026年NOR快閃記憶體全球市場報告

NOR快閃記憶體市場分析及預測(至2035年):依類型、產品類型、技術、應用、設備、最終用戶、組件、製程、部署類型及功能分類加密隨身碟市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、形狀、材質及最終用戶分類2026年NOR快閃記憶體全球市場報告