|

市場調查報告書

商品編碼

1940749

越南潤滑油:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Vietnam Lubricants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

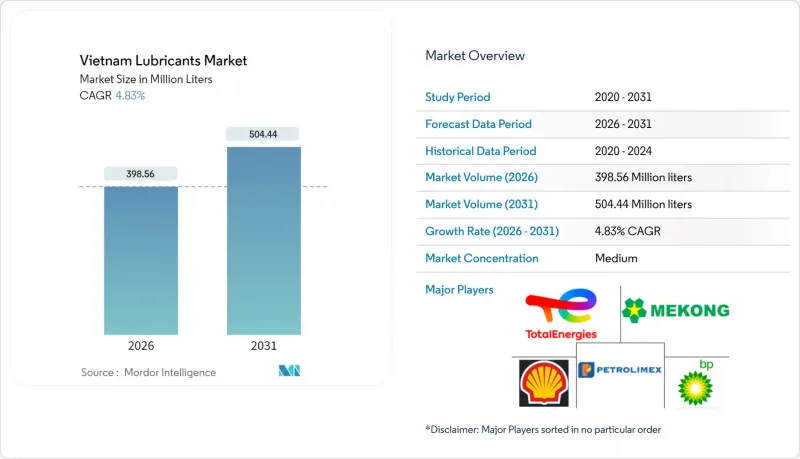

預計到 2026 年,越南潤滑油市場規模將達到 3.9856 億公升。

這意味著從 2025 年的 3.802 億公升成長到 2031 年的 5.0444 億公升。預計從 2026 年到 2031 年,將繼續以 4.83% 的複合年成長率成長。

在電氣化趨勢的推動下,越南潤滑油市場預計將持續成長。摩托車仍是主要的交通工具,而新的製造業投資也持續推動工業活動。不斷成長的車輛保有量支撐著市場成長勢頭,對高性能產品的需求日益成長,穩定的外國直接投資也帶動了工業園區機械設備的需求。市場參與企業正專注於高階換油週期產品、廣泛的分銷網路以及本地化配方,以抵禦基油價格波動的影響。同時,即將實施的環境稅和生產者延伸責任制(EPR)法規正促使生產商轉向合成和生物基產品線,雖然價格更高,但生命週期排放更低。儘管電動車(EV)正在逐步蠶食傳統機油的需求,但這些相互交織的趨勢仍為越南潤滑油市場創造了強勁的短期前景。

越南潤滑油市場趨勢及分析

汽車保有量增加和摩托車的優越性

越南的產業政策目標是到2030年使乘用車和摩托車的年銷量達到約100萬至110萬輛。摩托車目前仍佔車輛總量的絕大部分,仍以內燃機為主,需要頻繁更換機油。儘管電動機車在2024年新註冊摩托車中佔多數,但都市區的續航里程問題仍支撐著對礦物油和半合成油的持續需求。摩托車的定期保養週期,加上可支配收入的不斷成長,繼續為機油和變速箱油的銷售量成長奠定了基礎。

加速製造業工業化進程和吸引外商直接投資(FDI)

2024年上半年,製造業外商直接投資將達到152億美元,其中加工和電子工廠的投資金額將佔總投資額的三分之二以上。這筆資金將用於購買機械設備,而這些設備需要油壓油、齒輪油和金屬加工油來延長使用壽命並減少停機時間。海防、北寧和同奈的工業園區需要符合全球供應鏈審核標準的OEM認證潤滑油。由此產生的合成潤滑油和生物基潤滑油的需求,將在整個預測期內推動高級產品市場滲透率的提升。

基礎油進口價格波動

越南基礎油需求很大程度上依賴進口,使得當地調配商極易受到全球原油價格波動的影響。 2024年第二類基礎油現貨價格的大幅上漲擠壓了利潤空間,導致大多數黏度等級的零售價格上漲。庫存信貸有限的獨立調配商難以將成本轉嫁給消費者,並面臨被大規模促銷的國際品牌搶佔市場佔有率的風險。因此,一些經銷商減少了本地庫存,導致部分省會城市間歇性缺貨,直到供應協議恢復正常。

細分市場分析

截至2025年,汽車引擎機油市佔率佔比達37.90%,凸顯了越南交通運輸領域以摩托車為主導的現狀。在越南,二行程和四衝程機油滿足了龐大的二輪車市場需求,該市場註冊車輛數量高達7,700萬輛。工業機油是成長最快的產品類型,預計到2031年將以5.22%的複合年成長率成長,這主要得益於新建燃氣發電和可再生能源發電計劃的推動。原始設備製造商(OEM)對低灰配方的需求,使得延長維護週期成為推動市場成長的主要因素。變速箱油預計將受益於乘用車自動變速箱普及率的提高,而齒輪油的需求預計將與輕型商用車和物流車輛的擴張密切相關。

由於三星和富士康的供應商加大了對精密加工的投資,金屬加工液的需求不斷成長,而Master Fluid Solutions的本地分銷網路也為這一趨勢提供了支持。越南電力發展計畫的目標是到2030年實現29%的可再生能源佔比,因此渦輪機油和變壓器油的需求穩定成長,這為利潤豐厚的特種油品創造了機會。整體而言,為了滿足現代設備高負載和高溫的運作條件,產品結構正向高性能合成油轉變。

越南潤滑油市場報告按產品類型(汽車引擎油、工業引擎油、變速箱油、齒輪油、煞車油、液壓油、潤滑脂等)、終端用戶產業(汽車、船舶、航太、重型機械、工業)和基料類型(礦物油基、合成油、半合成油、生物基)進行細分。市場預測以公升為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 汽車保有量增加和摩托車的優越性

- 工業化進程加速和外國直接投資推動製造業成長。

- 過渡到合成和高性能潤滑油

- 外資汽車零件工廠的成長

- 跨境電商物流車輛的擴張

- 市場限制

- 基礎油進口價格波動

- 電動摩托車的迅速普及

- 加強處理規定

- 價值鏈分析

- 法律規範

- 終端用戶趨勢

- 汽車產業

- 製造業

- 發電業

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 依產品類型

- 汽車引擎油

- 工業機油

- 變速箱油

- 齒輪油

- 煞車油

- 油壓

- 潤滑脂

- 加工油(包括橡膠加工油和白油)

- 金屬加工油

- 渦輪機油

- 變壓器油

- 其他產品類型

- 按最終用戶行業分類

- 車

- 搭乘用車

- 商用車輛

- 摩托車

- 船

- 航太

- 重型機械

- 建造

- 礦業

- 農業

- 工業的

- 發電

- 冶金/金屬加工

- 紡織業

- 石油和天然氣

- 其他終端用戶產業

- 車

- 依基礎油類型

- 礦物油性潤滑劑

- 合成潤滑油

- 半合成潤滑油

- 生物性潤滑劑

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- AP SAIGON PETRO

- BP plc

- Chevron Corporation

- ENEOS Vietnam Company Limited.

- Exxon Mobil Corporation

- Fuchs Petrolub SE

- Idemitsu Kosan Co. Ltd

- Lubrizol

- Mekong Petrochemical JSC

- Motul

- Nikko Lubricant Vietnam.

- Petrolimex(PLX)

- PETRONAS Lubricants International

- PVOIL

- Shell plc

- SK Enmove Ltd

- T&T Viet Nam Lubricants Co.,LTD.

- TotalEnergies

第7章 市場機會與未來展望

第8章:執行長面臨的關鍵策略挑戰

Vietnam Lubricants Market size in 2026 is estimated at 398.56 million liters, growing from 2025 value of 380.20 million liters with 2031 projections showing 504.44 million liters, growing at 4.83% CAGR over 2026-2031.

This growth persists even as electrification advances, because two-wheelers continue to dominate mobility, and new manufacturing investments keep industrial activity rising. An expanding vehicle parc sustains momentum, a shift toward higher-performance formulations, and steady foreign direct investment that lifts machinery demand across industrial zones. Market participants emphasize premium drain-interval products, broad distribution, and localized blending to protect margins against base-oil cost fluctuations. At the same time, looming environmental taxes and Extended Producer Responsibility (EPR) rules are steering producers toward synthetic and bio-based lines that command higher price points yet trim lifecycle emissions. These intersecting trends frame a resilient near-term outlook for the Vietnam lubricants market even as electric vehicles (EVs) gradually erode conventional engine oil volumes.

Vietnam Lubricants Market Trends and Insights

Rising Vehicle Parc and Two-Wheeler Dominance

Vietnam's industrial policy aims to achieve annual passenger-car and two-wheeler sales of approximately 1.0-1.1 million units by 2030. Two-wheelers still account for the majority of the vehicle fleet, preserving a large base of internal-combustion engines that require frequent oil changes. Although electric motorcycles accounted for a significant portion of new two-wheeler registrations in 2024, range anxiety outside urban cores continues to underpin sustained demand for mineral oil and semi-synthetic products. Regular maintenance cycles associated with motorcycles, combined with rising disposable incomes, continue to anchor volume growth for engine oils and transmission fluids.

Accelerating Industrialization and FDI Manufacturing Growth

Manufacturing FDI reached USD 15.2 billion in the first six months of 2024, with processing and electronics plants accounting for more than two-thirds of the inflows. These capital injections translate into machinery installations that demand hydraulic, gear, and metalworking fluids engineered for longer drain intervals and lower downtime. Industrial parks in Hai Phong, Bac Ninh, and Dong Nai require OEM-approved lubricants that comply with global supply-chain audit standards. The resulting pull for synthetic and bio-based lubricants helps lift overall premium-product penetration through the forecast window.

Base-Oil Import Price Volatility

Vietnam imports the majority of its base-oil requirement, exposing local blenders to global crude swings. A spike in Group II base-oil spot prices in 2024 compressed margins and led to retail price hikes across most viscosity grades. Independent blenders with limited inventory credit struggled to pass on costs, risking volume losses to heavily promoted international brands. As a result, some distributors trimmed rural stock levels, causing sporadic shortages in tier-3 cities until supply contracts normalized.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Synthetic and Higher-Performance Lubricants

- Growth of Foreign-Invested Auto-Component Plants

- Rapid Rise of Electric Motorcycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, automotive engine oil commands a 37.90% share of the market, underscoring Vietnam's transportation landscape, which is heavily skewed towards motorcycles. Here, both 2-stroke and 4-stroke engine oils cater to a staggering 77 million registered two-wheelers. Industrial engine oil is the fastest-growing product category, expanding at a 5.22% CAGR through 2031, driven by new gas-fired and renewable power projects. The demand is driven by OEM requirements for low-ash formulations that enable longer maintenance intervals. Transmission fluids are expected to benefit from increased automatic-transmission penetration in passenger cars, while gear oil demand is expected to align with the expansion of light-commercial and logistics fleets.

Metalworking fluids escalate in tandem with precision-machining investments by Samsung and Foxconn suppliers, and Master Fluid Solutions' localized distribution underscores this trend. Turbine and transformer oils are experiencing steady growth as Vietnam's Power Development Plan targets a 29% renewable capacity by 2030, creating specialty-fluid opportunities that offer attractive margins. Overall, the product mix is tilting toward higher-performance synthetics that accommodate high-load, high-temperature operating conditions in modern equipment.

The Vietnam Lubricants Market Report is Segmented by Product Type (Automotive Engine Oil, Industrial Engine Oil, Transmission Fluids, Gear Oil, Brake Fluids, Hydraulic Fluids, Greases, and More), End-User Industry (Automotive, Marine, Aerospace, Heavy Equipment, and Industrial), and Base Stock Type (Mineral Oil-Based, Synthetic, Semi-Synthetic, and Bio-Based). The Market Forecasts are Provided in Terms of Volume (Litres).

List of Companies Covered in this Report:

- AP SAIGON PETRO

- BP p.l.c.

- Chevron Corporation

- ENEOS Vietnam Company Limited.

- Exxon Mobil Corporation

- Fuchs Petrolub SE

- Idemitsu Kosan Co. Ltd

- Lubrizol

- Mekong Petrochemical JSC

- Motul

- Nikko Lubricant Vietnam.

- Petrolimex (PLX)

- PETRONAS Lubricants International

- PVOIL

- Shell plc

- SK Enmove Ltd

- T&T Viet Nam Lubricants Co.,LTD.

- TotalEnergies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising vehicle parc and two-wheeler dominance

- 4.2.2 Accelerating industrialisation and FDI manufacturing growth

- 4.2.3 Shift toward synthetic/higher-performance lubricants

- 4.2.4 Growth of foreign-invested auto-component plants

- 4.2.5 Expansion of cross-border e-commerce logistics fleets

- 4.3 Market Restraints

- 4.3.1 Base-oil import price volatility

- 4.3.2 Rapid rise of electric motorcycles

- 4.3.3 Stricter used-oil disposal rules

- 4.4 Value Chain Analysis

- 4.5 Regulatory Framework

- 4.6 End-User Trends

- 4.6.1 Automotive Industry

- 4.6.2 Manufacturing Industry

- 4.6.3 Power Generation Industry

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Automotive Engine Oil

- 5.1.2 Industrial Engine Oil

- 5.1.3 Transmission Fluids

- 5.1.4 Gear Oil

- 5.1.5 Brake Fluids

- 5.1.6 Hydraulic Fluids

- 5.1.7 Greases

- 5.1.8 Process Oil (Including Rubber Process Oil and White Oil)

- 5.1.9 Metalworking Fluids

- 5.1.10 Turbine Oil

- 5.1.11 Transformer Oil

- 5.1.12 Other Product Types

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.1.1 Passenger Vehicles

- 5.2.1.2 Commercial Vehicles

- 5.2.1.3 Two-Wheelers

- 5.2.2 Marine

- 5.2.3 Aerospace

- 5.2.4 Heavy Equipment

- 5.2.4.1 Construction

- 5.2.4.2 Mining

- 5.2.4.3 Agriculture

- 5.2.5 Industrial

- 5.2.5.1 Power Generation

- 5.2.5.2 Metallurgy and Metalworking

- 5.2.5.3 Textiles

- 5.2.5.4 Oil and Gas

- 5.2.5.5 Other End-Use Industries

- 5.2.1 Automotive

- 5.3 By Base Stock Type

- 5.3.1 Mineral Oil-Based Lubricants

- 5.3.2 Synthetic Lubricants

- 5.3.3 Semi-Synthetic Lubricants

- 5.3.4 Bio-Based Lubricants

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 AP SAIGON PETRO

- 6.4.2 BP p.l.c.

- 6.4.3 Chevron Corporation

- 6.4.4 ENEOS Vietnam Company Limited.

- 6.4.5 Exxon Mobil Corporation

- 6.4.6 Fuchs Petrolub SE

- 6.4.7 Idemitsu Kosan Co. Ltd

- 6.4.8 Lubrizol

- 6.4.9 Mekong Petrochemical JSC

- 6.4.10 Motul

- 6.4.11 Nikko Lubricant Vietnam.

- 6.4.12 Petrolimex (PLX)

- 6.4.13 PETRONAS Lubricants International

- 6.4.14 PVOIL

- 6.4.15 Shell plc

- 6.4.16 SK Enmove Ltd

- 6.4.17 T&T Viet Nam Lubricants Co.,LTD.

- 6.4.18 TotalEnergies

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

8 Key Strategic Questions for CEOs

2026年全球潤滑油市場報告

2026年全球潤滑油市場報告 潤滑油市場:按產品類型、基礎油、黏度等級、最終用戶和分銷管道分類的全球市場預測,2026-2032年大豆油基潤滑劑市場:2026-2032年全球市場預測(依產品類型、包裝、應用、終端用戶產業及通路分類)紡織潤滑劑市場:依產品類型、劑型、應用及最終用途分類-2026年至2032年全球預測金屬切削潤滑劑市場:依產品類型、金屬類型、應用、終端用戶產業和通路分類-2026-2032年全球預測

潤滑油市場:按產品類型、基礎油、黏度等級、最終用戶和分銷管道分類的全球市場預測,2026-2032年大豆油基潤滑劑市場:2026-2032年全球市場預測(依產品類型、包裝、應用、終端用戶產業及通路分類)紡織潤滑劑市場:依產品類型、劑型、應用及最終用途分類-2026年至2032年全球預測金屬切削潤滑劑市場:依產品類型、金屬類型、應用、終端用戶產業和通路分類-2026-2032年全球預測 潤滑油過濾器市場規模、佔有率和成長分析:按過濾器類型、應用、材質、最終用戶和地區分類 - 2026-2033 年產業預測

潤滑油過濾器市場規模、佔有率和成長分析:按過濾器類型、應用、材質、最終用戶和地區分類 - 2026-2033 年產業預測 2026-2034年全球紗線潤滑劑市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球紗線潤滑劑市場規模、佔有率、趨勢和成長分析報告 玻璃潤滑劑市場規模、佔有率和成長分析:按潤滑劑基礎類型、配方類型、應用方法、包裝類型、最終用戶產業和地區分類-2026-2033年產業預測自行車潤滑脂市場按產品類型、通路、濃稠度等級和應用分類-全球預測,2026-2032年

玻璃潤滑劑市場規模、佔有率和成長分析:按潤滑劑基礎類型、配方類型、應用方法、包裝類型、最終用戶產業和地區分類-2026-2033年產業預測自行車潤滑脂市場按產品類型、通路、濃稠度等級和應用分類-全球預測,2026-2032年 Isododecane潤滑劑市場規模、佔有率和成長分析:按產品類型、應用、最終用戶和地區分類-2026-2033年產業預測

Isododecane潤滑劑市場規模、佔有率和成長分析:按產品類型、應用、最終用戶和地區分類-2026-2033年產業預測