|

市場調查報告書

商品編碼

1940726

東南亞廣告市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Southeast Asia Advertising - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

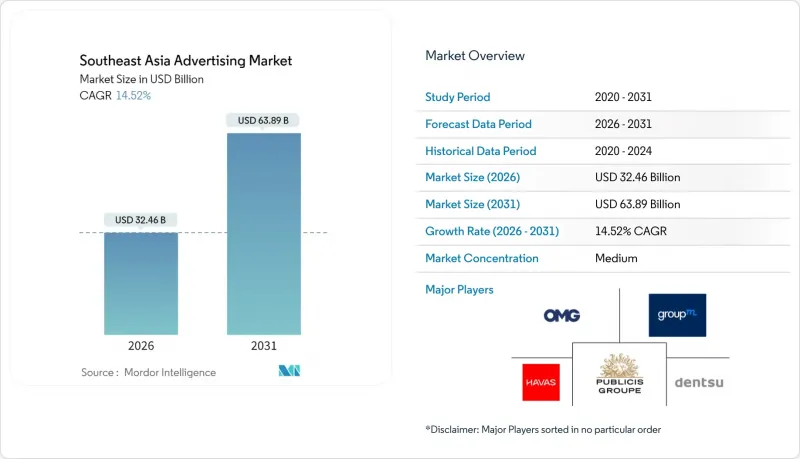

2025年東南亞廣告市場價值283.4億美元,預計到2031年將達到638.9億美元,高於2026年的324.6億美元。

預測期(2026-2031 年)的複合年成長率預計為 14.52%。

行動優先的數位化快速普及、人工智慧驅動的宣傳活動最佳化以及政府對中小企業部署線上廣告的補貼,共同支撐了營收成長。儘管廣告支出仍集中在傳統管道,但向自動化和數據密集型廣告形式的轉變已十分明顯,尤其是在智慧型手機月均行動數據使用量預計將從2023年的13GB成長到2030年的59GB的情況下。超級應用生態系統、不斷擴展的零售媒體網路以及數位戶外廣告(DOOH)指標的改進,正在拓寬通路組合,並提升全部區域品牌的廣告支出回報率(ROAS)。

東南亞廣告市場趨勢與洞察

行動寬頻普及率不斷提高

行動連線正在重塑東南亞廣告市場的覆蓋範圍。 GSMA預測,到2030年,每月資料使用量將成長四倍以上,為此前受頻寬限制的高位元率影片和身臨其境型內容格式創造了空間。在印度尼西亞,固定寬頻普及率不足20%,行動網路已成為預設的數位入口,加速了廣告主採用基於位置的定向投放和以影片為主導的創新。網速的提升也豐富了程式化平台可用的數據,將即時互動指標轉變為廣告資源購買和最佳化的主要機制。

程式化數位戶外廣告加速普及

數位廣告看板如今配備了動態廣告,可根據即時天氣和交通資訊進行調整。 Moving Walls 與 GroupM 於 2024 年 7 月達成的一項協議,使馬來西亞的廣告主能夠獲得檢驗戶外廣告 (DOOH) 資源,從而緩解了傳統廣告可見性方面的擔憂。在新加坡和曼谷等人口稠密的城市,演算法排期可以根據一天中的時間、繁忙的路線以及從行動裝置捕捉到的市場行為來輪換創新。戶外廣告開放測量組織 (Open Measurement in Out-of-Home Group) 等標準組織正在發布開放原始碼的廣告曝光率框架,從而滿足廣告主對線上管道課責的需求。

出版商庫存高度分散

馬來西亞擁有超過300家廣告看板所有者,迫使買家零散地拼湊宣傳活動。 CtrlShift的AMP市場目前整合了七大出版商的廣告資源,但規模仍然有限。印尼和菲律賓的小規模數位出版商缺乏通用的廣告科技堆疊和定價透明度,進一步加劇了這個問題。這種分散化推高了交易成本,阻礙了新進者,並減緩了東南亞廣告市場程式化支出的成長速度。

細分市場分析

截至2025年,傳統通路在東南亞廣告市場仍佔據60.12%的佔有率,這主要得益於電視在農村和老年人的持續存在。然而,這一領域的成長較為溫和,與數位媒體15.05%的複合年成長率形成鮮明對比,預示著智慧型手機和價格實惠的資料方案正在推動消費者行為發生不可逆轉的轉變。這種快速成長得益於程序化購買的高效性和精準定位,這是電視和紙媒無法比擬的。在泰國,數位廣告支出將在2024年首次超過電視廣告(45%對35%),這標誌著消費者正大幅轉向線上影片和社群媒體。

數位廣告的興起進一步受到跨境電商宣傳活動的推動,這些活動需要即時在地化,而只有演算法管道才能提供這種能力。同時,在人口密集的大都會圈,電影院和傳統戶外廣告形式仍然具有重要意義,因為這些地區的高階受眾重視沉浸式、品牌安全的廣告環境。然而,由於在成效指標、歸因分析和受眾數據方面存在不足,廣告預算正大幅流向數位廣告,從而形成一種反饋循環,並將在預測期內重塑東南亞廣告市場的支出結構。

預計到2025年,電視仍將佔據29.35%的市場佔有率,繼續保持其作為最盈利單一媒體的地位,這不僅體現了傳統媒體的影響力,也展現了其大規模覆蓋的效率。然而,數位戶外廣告(DOOH)的成長勢頭最為強勁,年複合成長率高達15.72%,這主要得益於螢幕成本的下降、5G網路連接的普及以及標準化的廣告曝光率衡量系統。廣告主看重DOOH能夠根據一天中的不同時段更新創新,並根據天氣或交通堵塞等特定地點的刺激因素觸發廣告投放。

傳統紙媒和廣播在某些細分市場仍然具有吸引力,例如針對老年族群的報紙插頁廣告或擁擠路段的通勤時段廣播廣告。然而,隨著衡量標準差異的擴大,它們的市佔率正在萎縮。影院廣告可以利用大片上映期間的優質廣告位,但影院容量限制了其成長。數位廣告,包括搜尋、社群媒體廣告、展示廣告和OTT影片,持續蠶食著傳統廣播廣告的預算,更完善的歸因模型和人工智慧增強的創新測試使品牌能夠最佳化其在東南亞廣告市場的即時表現。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 行動寬頻普及率不斷提高

- 加速採用程式化數位戶外廣告

- 政府主導的中小企業的數位化優先支持措施

- 人工智慧驅動的動態創新最佳化

- 超應用程式廣告生態系統(Grab、Gojek)

- 跨境電子商務的快速成長

- 市場限制

- 出版商庫存高度分散

- 不透明的經銷商回扣行為

- 更嚴格的個人資料保護條例(PDPA 的變體)

- 數位戶外廣告指標有限

- 產業價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 買方的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 宏觀經濟因素如何影響市場

第5章 市場規模與成長預測

- 按頻道類型

- 傳統媒體

- 數位媒體

- 透過廣告媒介

- 電視機

- 數位廣告

- 印刷

- 收音機

- 電影院

- 戶外廣告(OOH)

- 數位戶外廣告(DOOH)

- 按交易類型

- 程式化

- 非程式化

- 按最終用戶行業分類

- 消費品(FMCG)

- 零售與電子商務

- 車

- BFSI

- 通訊/IT

- 醫療保健和製藥

- 旅遊

- 其他終端用戶產業

- 按國家/地區

- 新加坡

- 馬來西亞

- 印尼

- 泰國

- 越南

- 菲律賓

- 其他國家(柬埔寨、寮國、緬甸、汶萊、東帝汶)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Dentsu International Asia Pte. Ltd.

- GroupM Asia Pacific Holdings Ltd.

- Omnicom Media Group Asia Pacific Pte. Ltd.

- Publicis Groupe SA

- Havas Media Asia Pacific Pte. Ltd.

- IPG Mediabrands Singapore Pte. Ltd.

- JCDecaux Singapore Pte. Ltd.

- Clear Channel Singapore Pte. Ltd.

- XCO Media Pte. Ltd.

- Mediacorp OOH Media Pte. Ltd.

- Moove Media Pte. Ltd.

- SPH Media Limited(SPHMBO)

- Moving Walls Sdn. Bhd.

- Spectrum Outdoor Sdn. Bhd.

- TAC Media Sdn. Bhd.

- VGI Global Media Public Co. Ltd.

- Sea Digital Media Pte. Ltd.

- AdColony(Digital Turbine Singapore Pte. Ltd.)

- GrabAds Holdings Pte. Ltd.

- Gojek Ads(PT Dompet Anak Bangsa)

- Kantar Media Singapore Pte. Ltd.

- Innity Corporation Berhad

第7章 市場機會與未來展望

The South East Asia Advertising market was valued at USD 28.34 billion in 2025 and estimated to grow from USD 32.46 billion in 2026 to reach USD 63.89 billion by 2031, at a CAGR of 14.52% during the forecast period (2026-2031).

Revenue growth rides on rapid mobile-first digital adoption, AI-enabled campaign optimization, and government grants that help small businesses advertise online. While traditional channels still concentrate spending, the shift toward automated, data-rich formats is unmistakable, especially as monthly mobile data usage per smartphone is set to climb from 13 GB in 2023 to 59 GB by 2030. Super-app ecosystems, expanding retail media networks, and stronger measurement standards for Digital Out-of-Home (DOOH) are widening the channel mix and enhancing return on ad spend for brands across the region.

Southeast Asia Advertising Market Trends and Insights

Rising Mobile Broadband Penetration

Mobile connectivity is redefining ad reach across the Southeast Asia Advertising market. GSMA projects that monthly data usage will surge more than fourfold by 2030, opening space for high-bit-rate video and immersive formats that were previously bandwidth-constrained. With Indonesia's fixed broadband penetration below 20%, mobile is the default digital gateway, prompting advertisers to adopt location-based targeting and video-first creative. Faster speeds also enrich the data available to programmatic platforms, turning real-time engagement metrics into the primary mechanism for buying and optimizing inventory.

Accelerated Uptake of Programmatic DOOH

Digital billboards now stream dynamic ads shaped by live weather or traffic feeds. A July 2024 deal between Moving Walls and GroupM gave Malaysian buyers verified DOOH inventory, mitigating historical viewability doubts. In dense Singapore and Bangkok, algorithmic scheduling lets brands rotate creative by daypart, congested routes, or in-market behaviors pulled from mobile devices. Standard-setting bodies such as the Open Measurement in Out-of-Home Group released open-source impression frameworks, bringing the accountability that advertisers expect from online channels.

High Fragmentation of Publisher Inventory

Malaysia counts more than 300 billboard owners, forcing buyers to stitch together campaigns piecemeal. CtrlShift's AMP marketplace now aggregates inventory from seven major publishers, but scale remains limited. Smaller digital publishers across Indonesia and the Philippines compound the problem, lacking common ad-tech stacks or transparency in pricing. Fragmentation raises transaction costs, deters new entrants, and slows the growth trajectory of programmatic spend within the Southeast Asia Advertising market.

Other drivers and restraints analyzed in the detailed report include:

- Government-Led Digital-First SME Incentives

- AI-Driven Dynamic Creative Optimization

- Opaque Agency Rebate Practices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Traditional channels retained a 60.12% share of the South East Asia Advertising market in 2025, buoyed by entrenched TV viewership among rural and older audiences. Yet the segment's modest growth contrasts with digital media's 15.05% CAGR, signaling an irreversible consumption pivot fueled by smartphones and cheaper data plans. Rapid gains stem from programmatic buying efficiencies and granular targeting that television or print cannot match. Thailand marked a pivotal moment in 2024 when digital ad spend surpassed TV, taking 45% versus 35%, underlining consumer migration to online video and social feeds.

Digital's advance is accelerated further by cross-border e-commerce campaigns demanding real-time localization, a capability only algorithmic channels can deliver. Meanwhile, cinema and classic outdoor formats remain relevant in dense metros, where premium audiences value immersive, brand-safe settings. Still, the differential in performance metrics, attribution, and audience data tilts budgets heavily toward digital, reinforcing a feedback loop that reshapes the spending mix of the Southeast Asia Advertising market over the forecast period.

Television's 29.35% stake in 2025 still positions it as the most lucrative single medium, reflecting both legacy habit and mass-reach efficiency. However, Digital Out-of-Home exhibits the highest trajectory at 15.72% CAGR, aided by falling screen costs, 5G connectivity, and standardized impression counting frameworks. Advertisers appreciate DOOH's ability to refresh creative by daypart or trigger ads based on localized stimuli such as weather or traffic congestion.

Traditional print and radio keep niche appeal, newspaper inserts among older readers, and commuter-time radio ads on high-congestion routes, but their share contracts as measurement gaps widen. Cinema capitalizes on blockbuster releases for premium placements, yet venue capacity caps growth. Digital advertising covering search, social, display, and OTT video continues to siphon dollars from broadcast budgets, riding on better attribution models and AI-enhanced creative testing that optimize in-flight performance for brands across the Southeast Asia Advertising market.

The South East Asia Advertising Market Report is Segmented by Channel Type (Traditional Media and Digital Media), Advertising Medium (Television, Digital Advertising, Print, and More), Transaction Type (Programmatic and Non-Programmatic), End-User Industry (FMCG, Retail and E-Commerce, Automotive, BFSI, Telecom and IT, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Dentsu International Asia Pte. Ltd.

- GroupM Asia Pacific Holdings Ltd.

- Omnicom Media Group Asia Pacific Pte. Ltd.

- Publicis Groupe SA

- Havas Media Asia Pacific Pte. Ltd.

- IPG Mediabrands Singapore Pte. Ltd.

- JCDecaux Singapore Pte. Ltd.

- Clear Channel Singapore Pte. Ltd.

- XCO Media Pte. Ltd.

- Mediacorp OOH Media Pte. Ltd.

- Moove Media Pte. Ltd.

- SPH Media Limited (SPHMBO)

- Moving Walls Sdn. Bhd.

- Spectrum Outdoor Sdn. Bhd.

- TAC Media Sdn. Bhd.

- VGI Global Media Public Co. Ltd.

- Sea Digital Media Pte. Ltd.

- AdColony (Digital Turbine Singapore Pte. Ltd.)

- GrabAds Holdings Pte. Ltd.

- Gojek Ads (PT Dompet Anak Bangsa)

- Kantar Media Singapore Pte. Ltd.

- Innity Corporation Berhad

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising mobile broadband penetration

- 4.2.2 Accelerated uptake of programmatic DOOH

- 4.2.3 Government-led digital-first SME incentives

- 4.2.4 AI-driven dynamic creative optimisation

- 4.2.5 Super-app advertising ecosystems (Grab, Gojek)

- 4.2.6 Cross-border e-commerce boom

- 4.3 Market Restraints

- 4.3.1 High fragmentation of publisher inventory

- 4.3.2 Opaque agency rebate practices

- 4.3.3 Stringent personal-data regulations (PDPA variants)

- 4.3.4 Limited measurement standards for DOOH

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Channel Type

- 5.1.1 Traditional Media

- 5.1.2 Digital Media

- 5.2 By Advertising Medium

- 5.2.1 Television

- 5.2.2 Digital Advertising

- 5.2.3 Print

- 5.2.4 Radio

- 5.2.5 Cinema

- 5.2.6 Out-of-Home (OOH)

- 5.2.7 Digital OOH (DOOH)

- 5.3 By Transaction Type

- 5.3.1 Programmatic

- 5.3.2 Non-Programmatic

- 5.4 By End-User Industry

- 5.4.1 Fast-Moving Consumer Goods (FMCG)

- 5.4.2 Retail and E-commerce

- 5.4.3 Automotive

- 5.4.4 BFSI

- 5.4.5 Telecom and IT

- 5.4.6 Healthcare and Pharma

- 5.4.7 Travel and Tourism

- 5.4.8 Other End-User Industries

- 5.5 By Country

- 5.5.1 Singapore

- 5.5.2 Malaysia

- 5.5.3 Indonesia

- 5.5.4 Thailand

- 5.5.5 Vietnam

- 5.5.6 Philippines

- 5.5.7 Other Countries (Cambodia, Laos, Myanmar, Brunei, Timor-Leste)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Dentsu International Asia Pte. Ltd.

- 6.4.2 GroupM Asia Pacific Holdings Ltd.

- 6.4.3 Omnicom Media Group Asia Pacific Pte. Ltd.

- 6.4.4 Publicis Groupe SA

- 6.4.5 Havas Media Asia Pacific Pte. Ltd.

- 6.4.6 IPG Mediabrands Singapore Pte. Ltd.

- 6.4.7 JCDecaux Singapore Pte. Ltd.

- 6.4.8 Clear Channel Singapore Pte. Ltd.

- 6.4.9 XCO Media Pte. Ltd.

- 6.4.10 Mediacorp OOH Media Pte. Ltd.

- 6.4.11 Moove Media Pte. Ltd.

- 6.4.12 SPH Media Limited (SPHMBO)

- 6.4.13 Moving Walls Sdn. Bhd.

- 6.4.14 Spectrum Outdoor Sdn. Bhd.

- 6.4.15 TAC Media Sdn. Bhd.

- 6.4.16 VGI Global Media Public Co. Ltd.

- 6.4.17 Sea Digital Media Pte. Ltd.

- 6.4.18 AdColony (Digital Turbine Singapore Pte. Ltd.)

- 6.4.19 GrabAds Holdings Pte. Ltd.

- 6.4.20 Gojek Ads (PT Dompet Anak Bangsa)

- 6.4.21 Kantar Media Singapore Pte. Ltd.

- 6.4.22 Innity Corporation Berhad

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment