|

市場調查報告書

商品編碼

1940718

歐洲設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Europe Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

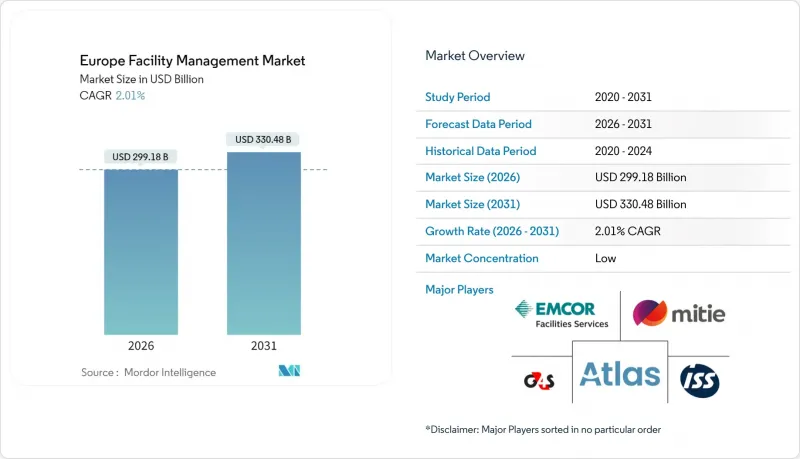

預計到 2026 年,歐洲設施管理市場規模將達到 2,991.8 億美元,高於 2025 年的 2,932.8 億美元。

預計到 2031 年將達到 3,304.8 億美元,2026 年至 2031 年的複合年成長率為 2.01%。

穩定成長反映了維護模式從成本主導轉變為資料驅動型績效服務的轉變、日益嚴格的能源效率法規以及公共部門外包業務的成長。硬性服務仍然是該行業的基礎,因為老化的建築基礎設施需要密集的機械、電氣和管道維護。同時,在以健康、福祉和體驗為導向的職場的推動下,軟性服務正在加速發展。俄烏衝突後能源價格上漲,促使客戶越來越傾向選擇最佳化合約而非工時和材料合約。隨著ESG報告法規和日益複雜的數位技術對專業知識的需求不斷成長,外包業務也在不斷擴張。私募股權投資,例如Techem公司72億美元的收購案,凸顯了對該領域經常性收入的信心。

歐洲設施管理市場趨勢與洞察

老舊建築存量:維修主導的設施管理支出

歐洲四分之三的建築存量超過50年,因此對結合技術維護和能源效率的綜合維修項目有持續的需求。績效合約模式,例如Centrica與聖喬治大學醫院簽訂的15年合約(該合約每年減少二氧化碳排放6000噸,節省110萬美元),證明了以維修為重點的設施服務在財務上的可行性。隨著淨零能耗建築標準的日益嚴格,德國和法國的建築組合在維修中迫切需要整合物聯網感測器、預測性維護和能源效能分析。歐洲投資銀行估計,能源效率領域的年度資金缺口高達1,850億歐元,這使得設施服務供應商成為籌集資金的關鍵中介。

後緊縮時代公共部門外包勢頭強勁

為了達到效率目標和履行環境、社會及治理(ESG)資訊揭露義務,政府機構正在將複雜的服務外包。英國就業與退休金部已授予ISS一份為期七年、每年價值1.75億美元的契約,用於集中管理清潔、餐飲服務和設施維護。北歐和德國的市政當局也紛紛效仿,剪切機議會與VINCI Facilities簽訂了為期十年的框架契約,優先考慮協同能源管理。醫療機構尤其重視協同能源管理,因為全天候運作、感染控制和高能耗空調都需要專門的支援。

經濟壓力(通貨膨脹、成本最佳化)

人事費用、材料和能源成本的上漲正迫使客戶重新談判合約並削減非必要的設施管理支出。世邦魏理仕 (CBRE) 的研究發現,儘管 35% 的企業增加了 2023 年的設施管理預算,但仍有 29% 的企業認為供應鏈中斷是其面臨的最大威脅。由於醫療保健客戶推遲了競標,索迪斯 (Sodexo) 的歐洲業務在 2025 會計年度上半年的內部成長率僅為 2.1%。利潤率壓力在南歐和東歐尤為嚴峻,這些地區對價格的高度敏感導致商品化趨勢加劇。

細分市場分析

到2025年,硬性服務將佔歐洲設施管理市場的61.05%,凸顯了對老舊建築基礎設施的機電裝置(MEP)、暖通空調(HVAC)和消防安全進行維護的必要性。儘管由於持續的維修活動,整個行業的成長速度放緩,但歐洲硬性服務領域的設施管理市場規模仍在不斷擴大。由於客戶希望延長資產使用壽命並遵守能源使用法規,預測性資產管理正變得越來越普遍。

儘管規模較小,但隨著員工體驗策略優先考慮高級清潔、禮賓和保全服務,軟性服務預計將實現 4.61% 的複合年成長率。混合辦公模式的興起推動了對空間預訂、靈活餐飲和非接觸式門禁的需求,並將技術融入傳統的前台營運中。客流量分析等軟性服務數據回饋到能源演算法中,創造了整合機會,使服務提供者能夠更深入地參與客戶的營運規劃。

歐洲設施管理市場按服務類型(硬性服務與軟性服務)、交付模式(內部營運與外包)、最終用戶行業(商業、酒店、公共基礎設施及機構、醫療保健、工業及流程、其他最終用戶行業)和國家/地區進行細分。市場預測以以金額為準。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 歐洲商業地產目前運轉率

- 領先設施管理服務提供者的盈利基準

- 勞動指標-技術純熟勞工和非技術技術純熟勞工參與率

- 按服務類型分類的設施管理市場佔有率(%)

- 按硬體服務分類的設施管理市場佔有率(%)

- 以軟性服務分類的設施管理市場佔有率(%)

- 主要都會區的都市化和人口成長

- 歐洲部門投資優先事項基礎設施發展計劃

- 與勞動和安全標準相關的監管促進因素

- 歐盟綠色交易中能源效率目標對FM需求的影響

- 科技整合:物聯網與人工智慧變革服務交付

- 不斷變化的職場:混合辦公模式重塑設施管理優先事項

- 市場促進因素

- 老舊建築存量:維修主導的設施管理支出

- 財政緊縮後公共部門外包趨勢

- 能源價格波動加速了能源最佳化型設施管理服務的發展

- 強制性ESG報告需要數據驅動的設施管理解決方案。

- 疫情後對健康與安全認證的需求

- 私募股權整合推動了綜合設施管理的普及。

- 市場限制

- 經濟壓力(通貨膨脹、成本最佳化)

- 歐盟內部分散的管理體制阻礙了標準化供應。

- 房地產科技互通性有限會增加整合成本

- 互聯建築系統面臨的網路安全風險

- 價值鏈分析

- PESTEL 分析

- 新參與企業的監管和法律體制

- 宏觀經濟指標對FM需求的影響

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 投資與資金籌措分析

第5章 市場規模與成長預測

- 按服務類型

- 硬服務

- 資產管理

- 機電及暖通空調服務

- 消防系統和安全措施

- 其他硬體維修服務

- 軟服務

- 辦公室支援與安全

- 清潔服務

- 餐飲服務

- 其他軟性調頻服務

- 硬服務

- 以規定形式

- 內部

- 外包

- 單頻調頻

- 綜合設施管理服務

- 綜合設施管理(綜合FM)

- 按最終用戶行業分類

- 商業(IT/通訊、零售/倉儲)

- 餐飲服務業(飯店、餐廳、大型餐廳)

- 公共及公共基礎設施(政府、教育、交通)

- 醫療保健(公立和私立機構)

- 工業和流程工業(製造業、能源業、採礦業)

- 其他終端用戶產業(多用戶住宅、娛樂、運動和休閒)

- 按國家/地區

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 斯洛維尼亞

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Mitie Group PLC

- Emcor Facilities Services WLL

- Atlas FM Ltd.

- G4S Facilities Management UK Ltd.

- ISS Global

- Engie FM Ltd.(Cofely AG)

- Andron Facilities Management

- Apleona GmbH

- Dussmann Group

- Vinci Facilities Ltd.

- Okin Group

- Aramark Corporation

- CBRE Group Inc.

- Assured Europe

- Jones Lang LaSalle Inc.

- Sodexo SA

- Johnson Controls International plc

- Bouygues Energies and Services

第7章 市場機會與未來趨勢

- 評估差距和未滿足的需求

- 技術主導整合設施管理(物聯網、建築管理系統、基於人工智慧的預測性維護)

- 對符合ESG標準的設施管理解決方案的需求

- 服務模式的未來變化(基於績效的合約)

European Facility Management Market size in 2026 is estimated at USD 299.18 billion, growing from 2025 value of USD 293.28 billion with 2031 projections showing USD 330.48 billion, growing at 2.01% CAGR over 2026-2031.

A steady expansion reflects the sector's shift from cost-driven maintenance toward data-enabled performance services, tighter energy-efficiency mandates, and widening public-sector outsourcing. Hard services remain the industry's anchor as ageing building systems require intensive mechanical, electrical, and plumbing care, while soft services accelerate on the back of health, wellness, and experience-oriented workplaces. Rising energy prices since the Russia-Ukraine conflict have pushed clients to favor optimization contracts over time-and-materials tasks. Outsourcing gains scale as ESG reporting rules and digital-technology complexity demand specialized know-how. Private-equity interest, typified by Techem's USD 7.2 billion transaction, underlines confidence in the segment's recurring-revenue profile.

Europe Facility Management Market Trends and Insights

Aging Building Stock: Retrofit-Driven FM Spending

Three-quarters of the European building stock is more than 50 years old, creating sustained demand for comprehensive retrofit programmes that bundle technical maintenance with energy upgrades. Performance-contract models such as Centrica's 15-year deal at St George's University Hospitals, which cuts 6,000 tonnes of carbon and saves USD 1.1 million annually, illustrate the financial viability of retrofit-oriented facility services. German and French portfolios face the greatest urgency as Nearly-Zero-Energy Building standards tighten, pushing facility managers to integrate IoT sensors, predictive maintenance, and energy-performance analytics during refurbishments. The European Investment Bank estimates a EUR 185 billion yearly funding gap for energy efficiency, positioning facility service providers as key intermediaries for capital access.

Public-Sector Outsourcing Momentum Post-Fiscal Austerity

Government departments are transferring multi-service bundles to external providers to meet efficiency targets and ESG disclosure obligations. The UK Department for Work and Pensions awarded ISS a seven-year contract worth USD 175 million per year, consolidating cleaning, catering, and technical maintenance under one roof. Nordic and German municipalities follow suit, evidenced by VINCI Facilities' decade-long framework with Lincolnshire County Council that prioritises collaborative energy management. Health-care estates are prominent adopters as 24/7 operations, infection control, and high-energy HVAC loads demand specialist support.

Economic Pressures (Inflation, Cost Optimisation)

Rising labour, material, and energy inputs prompt clients to renegotiate contracts, curbing discretionary FM spend. CBRE notes that while 35% of organisations raised FM budgets in 2023, 29% still listed supply-chain disruption as the top threat. Sodexo's European business recorded only 2.1% organic growth for the first half of fiscal 2025 as healthcare clients delayed tenders. Margin pressure is acute in Southern and Eastern Europe, where price sensitivity drives commoditisation.

Other drivers and restraints analyzed in the detailed report include:

- Energy Price Volatility Accelerating Energy-Optimisation Services

- ESG Reporting Mandates Requiring Data-Driven Solutions

- Fragmented EU Regulatory Regimes Hindering Standardised Delivery

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hard services hold 61.05% of the European facility management market in 2025, underlining the necessity of MEP, HVAC, and fire-safety upkeep across an ageing building base. Persistent retrofit activity keeps the European facility management market size for hard services expanding despite moderate industry growth. Predictive asset management gains traction as clients look to extend equipment life cycles and comply with energy-use regulations.

Soft services, though smaller, deliver a 4.61% forecast CAGR as employee-experience strategies prioritise advanced cleaning, concierge, and security packages. Hybrid work drives demand for space booking, flexible catering, and touchless access control, threading technology through traditional frontline functions. Integration opportunities arise where soft-service data, such as footfall analytics, feed back into energy algorithms, further embedding providers in client operational planning.

Europe Facility Management Market is Segmented by Service Type (Hard Services and Soft Services), Offering Type (In-House and Outsourced), End-User Industry (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, Industrial and Process, and Other End-User Industries), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Mitie Group PLC

- Emcor Facilities Services WLL

- Atlas FM Ltd.

- G4S Facilities Management UK Ltd.

- ISS Global

- Engie FM Ltd. (Cofely AG)

- Andron Facilities Management

- Apleona GmbH

- Dussmann Group

- Vinci Facilities Ltd.

- Okin Group

- Aramark Corporation

- CBRE Group Inc.

- Assured Europe

- Jones Lang LaSalle Inc.

- Sodexo SA

- Johnson Controls International plc

- Bouygues Energies and Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.1.1 Current Occupancy Rates in Europe Commercial Real Estate

- 4.1.2 Profitability Benchmarks of Major FM Providers

- 4.1.3 Workforce Indicators - Skilled and Unskilled Labor Participation

- 4.1.4 Facility Management Market Share (%) by Service Type

- 4.1.5 Facility Management Market Share (%) by Hard Services

- 4.1.6 Facility Management Market Share (%) by Soft Services

- 4.1.7 Urbanization and Population Growth in Top Metro Areas

- 4.1.8 Sector Investment Priorities in Europe Infrastructure Pipeline

- 4.1.9 Regulatory Drivers Specific to Labour and Safety Standards

- 4.1.10 EU Green Deal Energy-Efficiency Targets Impact on FM Demand

- 4.1.11 Technology Integration: IoT and AI Transforming Service Delivery

- 4.1.12 Changing Workplace Dynamics: Hybrid Work Reshaping FM Priorities

- 4.2 Market Drivers

- 4.2.1 Aging Building Stock: Retrofit-Driven FM Spending

- 4.2.2 Public Sector Outsourcing Momentum Post-Fiscal Austerity

- 4.2.3 Energy Price Volatility Accelerating Energy-Optimization FM Services

- 4.2.4 ESG Reporting Mandates Requiring Data-Driven FM Solutions

- 4.2.5 Post-Pandemic Health and Safety Certification Demand

- 4.2.6 Private Equity Consolidation Driving Integrated FM Adoption

- 4.3 Market Restraint

- 4.3.1 Economic Pressures (Inflation, Cost Optimisation)

- 4.3.2 Fragmented EU Regulatory Regimes Hindering Standardised Delivery

- 4.3.3 Limited PropTech Interoperability Increasing Integration Costs

- 4.3.4 Cybersecurity Risks to Connected Building Systems

- 4.4 Value Chain Analysis

- 4.5 PESTEL Analysis

- 4.6 Regulatory and Legislative Framework for Market Entrants

- 4.7 Impact of Macroeconomic Indicators on FM Demand

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Services

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment and Funding Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Service Type

- 5.1.1 Hard Services

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard FM Services

- 5.1.2 Soft Services

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft FM Services

- 5.1.1 Hard Services

- 5.2 By Offering Type

- 5.2.1 In-house

- 5.2.2 Outsourced

- 5.2.2.1 Single FM

- 5.2.2.2 Bundled FM

- 5.2.2.3 Integrated FM

- 5.3 By End-user Industry

- 5.3.1 Commercial (IT and Telecom, Retail and Warehouses)

- 5.3.2 Hospitality (Hotels, Eateries, Large-scale Restaurants)

- 5.3.3 Institutional and Public Infrastructure (Govt, Education, Transportation)

- 5.3.4 Healthcare (Public and Private Facilities)

- 5.3.5 Industrial and Process (Manufacturing, Energy, Mining)

- 5.3.6 Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure)

- 5.4 By Country

- 5.4.1 United Kingdom

- 5.4.2 Germany

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Slovenia

- 5.4.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Mitie Group PLC

- 6.4.2 Emcor Facilities Services WLL

- 6.4.3 Atlas FM Ltd.

- 6.4.4 G4S Facilities Management UK Ltd.

- 6.4.5 ISS Global

- 6.4.6 Engie FM Ltd. (Cofely AG)

- 6.4.7 Andron Facilities Management

- 6.4.8 Apleona GmbH

- 6.4.9 Dussmann Group

- 6.4.10 Vinci Facilities Ltd.

- 6.4.11 Okin Group

- 6.4.12 Aramark Corporation

- 6.4.13 CBRE Group Inc.

- 6.4.14 Assured Europe

- 6.4.15 Jones Lang LaSalle Inc.

- 6.4.16 Sodexo SA

- 6.4.17 Johnson Controls International plc

- 6.4.18 Bouygues Energies and Services

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Technology-led Integrated FM (IoT, BMS, AI-based Predictive Maintenance)

- 7.3 ESG-compliant FM Solutions Demand

- 7.4 Future Service-Model Shifts (Outcome-based Contracts)

全球設施管理服務市場:機會與策略展望(至2035年)

全球設施管理服務市場:機會與策略展望(至2035年) 日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)