|

市場調查報告書

商品編碼

1940708

東南亞POS終端:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Southeast Asia POS Terminal - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

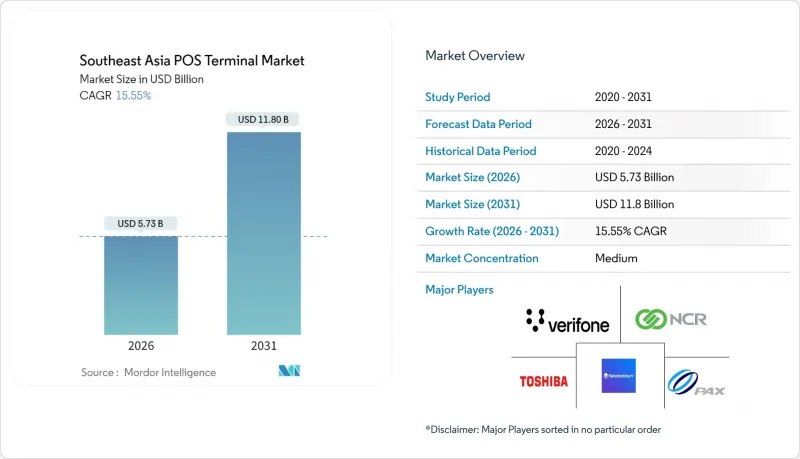

2025年東南亞POS終端市值為49.6億美元,預計2031年將達到118億美元,高於2026年的57.3億美元。

預測期(2026-2031 年)的複合年成長率預計為 15.55%。

東南亞POS終端市場持續快速成長,主要受消費者加速轉向行動錢包、QR碼應用日益普及以及政府強制推行數位支付等因素的推動。商家正將資金投入軟體定義終端或混合終端,這些終端整合了QR碼、NFC和銀行卡功能,旨在簡化櫃檯設備並滿足未來的支付需求。競爭焦點正從硬體規格轉向軟體生態系統,供應商將庫存管理、客戶關係管理(CRM)和貸款工具整合到雲端控制面板中,從而獲得競爭優勢。東協區域支付互聯互通計畫下的跨境支付舉措可望加快身分驗證速度,這將是推動東南亞POS終端市場在2030年前持續成長的關鍵因素。

東南亞POS終端市場趨勢與洞察

數位支付在東南亞迅速發展

2024年,在印尼、泰國和菲律賓,行動錢包交易量超過了傳統銀行卡網路。這項轉變正在加速東南亞POS終端市場多模式終端的更換。光是印尼的QRIS(QR碼支付系統)就記錄了超過160億筆交易,迫使商家從單一功能的讀卡機遷移到整合QR/NFC功能的終端。終端製造商目前正在設計具有全通路API的終端,以實現商店和配送通路的統一支付處理。為此,支付處理商正在預先安裝增值應用程式,例如會員計劃、庫存管理和先買後付(BNPL)服務,以確保設備在五年使用壽命內持續可用。這導致硬體更換需求持續兩位數成長,尤其是在那些從紙質收銀機升級的小規模商家中。

政府主導的無現金政策和電子支付法規

馬來西亞的e-Tunai Rakyat、泰國的PromptPay以及印尼的中小企業補貼計劃,每季都在推動數千台補貼終端進入東南亞POS終端市場。合規條款要求終端具備經認證的NFC和EMV功能,這促使能夠透過本地安全審核的中階安卓機型訂單增加。由於補貼通常涵蓋初始硬體成本,供應商正迅速轉向基於SaaS的授權模式,即使在津貼結束後也能持續產生收入。遍遠地區的推廣計畫正在推動區域城市的需求成長,使經銷商能夠比自然成長的商家拓展速度更快地將業務擴展到大都會區以外的地區。

網路安全和資料隱私漏洞

印尼央行報告稱,2024年POS終端相關的詐騙企圖激增45%,凸顯了即時威脅的重要性。如果不加以控制,這些威脅可能會阻礙新終端的部署。利用過時韌體的惡意韌體可以在單一終端機被攻破後迅速傳播,因此監管機構強制要求進行空中補丁更新。缺乏IT負責人的小規模零售商依賴供應商來保全行動。更新延遲會導致規避風險的商家推遲採購。因此,供應商必須提供資安管理服務,以維持東南亞POS終端市場的成長動能。

細分市場分析

預計到2025年,非接觸式支付將佔東南亞POS終端市場收入佔有率的56.97%,並在2031年之前以17.05%的複合年成長率成長。這項優勢促使「輕觸支付」成為新型終端產品的標配功能。目前,供應商正致力於最佳化天線位置和螢幕提示設計,以實現兩秒以內的支付交易,商家認為這項功能能夠顯著提升交易效率。對於小額交易的小規模商家而言,QR碼方案仍然至關重要,它可以確保消費者不會因錢包選擇而放棄支付。

終端機製造商正在入門級機型中取消機械卡槽以降低組件成本,同時推廣用於螢幕輸入密碼交易的SoftPOS系統。這一趨勢表明,到2020年代中期,東南亞非接觸式POS終端市場將不再局限於淘汰專用卡式硬體。此外,這一趨勢也促使通訊業者將密碼容量LTE資料方案與mPOS訂閱捆綁銷售,以應對韌體持續更新和分析數據傳輸而帶來的流量激增。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 數位支付在東南亞迅速發展

- 政府政策旨在促進無現金交易和電子支付法規

- 行動銷售點(mPOS)在中小企業和微型零售商的應用日益普及

- 將先買後付功能整合到POS硬體中

- 旅遊業主導的全通路零售業在新冠疫情後的復甦

- 過渡到基於安卓的開放作業系統設備和應用商店

- 市場限制

- 網路安全和資料隱私漏洞

- 現代POS終端總體擁有成本高

- 東南亞國家認證法規碎片化

- 主要城市以外地區設備服務網路薄弱

- 產業價值鏈分析

- 監管環境

- 技術展望

- 宏觀經濟因素的影響

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 對影響市場的宏觀經濟因素進行評估

第5章 市場規模與成長預測

- 透過付款方式

- 聯繫類型

- 非接觸式支付

- 按POS類型

- 固定式POS系統

- 行動/可攜式POS系統

- 按最終用戶行業分類

- 零售

- 飯店業

- 衛生保健

- 運輸/物流

- 其他終端用戶產業

- 按國家/地區

- 新加坡

- 馬來西亞

- 泰國

- 印尼

- 菲律賓

- 越南

- 東南亞及其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Worldline SA(Ingenico)

- Verifone Systems LLC

- PAX Technology Ltd.

- NCR Corporation

- Toshiba TEC Corporation

- Newland Payment Technology Co., Ltd.

- HP Inc.

- Samsung Electronics Co., Ltd.

- Fujian Newland Computer Co., Ltd.(Urovo)

- SUNMI Technology Co., Ltd.

- SZZT Electronics Co., Ltd.

- Diebold Nixdorf, Incorporated

- NEC Corporation

- Fujitsu Limited

- BBPOS International Limited

- Centerm Information Co., Ltd.

- New POS Technology Ltd.

- Castles Technology Co., Ltd.

- SUNAR Technology Co., Ltd.

- Squareup International Ltd.

第7章 市場機會與未來展望

The Southeast Asia POS Terminal Market was valued at USD 4.96 billion in 2025 and estimated to grow from USD 5.73 billion in 2026 to reach USD 11.8 billion by 2031, at a CAGR of 15.55% during the forecast period (2026-2031).

Strong consumer migration to mobile wallets, rising ubiquity of QR codes, and government mandates that compel digital payment acceptance are keeping the Southeast Asia POS Terminal market on a steep growth trajectory. Merchants are shifting capital toward software-defined or hybrid devices that consolidate QR, NFC, and card functions, trimming counter clutter while future-proofing acceptance needs. Competitive focus has moved from hardware specifications to software ecosystems, favoring vendors that bundle inventory, CRM, and financing tools into cloud dashboards. Cross-border payment initiatives under the ASEAN Regional Payment Connectivity program promise faster certification cycles, a factor set to unlock incremental demand for the Southeast Asia POS Terminal market through 2030.

Southeast Asia POS Terminal Market Trends and Insights

Rapid Expansion of Digital Payments Across Southeast Asia

Mobile wallets processed more transactions than traditional card networks in Indonesia, Thailand, and the Philippines during 2024, a shift that has amplified replacement cycles for multi-modal devices across the Southeast Asia POS Terminal market. QRIS in Indonesia alone logged more than 16 billion transactions, forcing merchants to ditch single-function card readers in favor of integrated QR/NFC units. Device makers now design terminals with omnichannel APIs, enabling unified reconciliation across storefront and delivery channels. Payment processors, in turn, preload value-added apps loyalty, inventory, BNPL to keep devices sticky over a five-year lifespan. The net effect is sustained double-digit hardware refresh demand, particularly from micro-merchants upgrading from paper or cash registers.

Government Cash-less Initiatives and E-payment Regulations

Malaysia's e-Tunai Rakyat, Thailand's PromptPay, and Indonesia's SME subsidy schemes collectively inject thousands of subsidized terminals into the Southeast Asia POS Terminal market every quarter. Compliance clauses require certified NFC and EMV functionality, accelerating orders for mid-range Android models able to pass local security audits. Because subsidies often cover up-front hardware costs, vendors increasingly pivot to SaaS-based licensing that drives recurring revenue even after grants expire. Rural onboarding programs extend demand into second-tier cities, helping distributors expand beyond capital regions much faster than organic merchant acquisition would allow.

Cyber-security and Data-privacy Vulnerabilities

Bank Indonesia recorded a 45% jump in POS-linked fraud attempts during 2024, highlighting real-time threats that could stall new deployments if unaddressed. Malware that exploits outdated firmware spreads quickly once a single device is breached, prompting regulators to mandate over-the-air patch cycles. Smaller retailers, lacking IT staff, depend on vendors for security orchestration; when updates lag, risk-averse merchants defer purchases. Consequently, suppliers must bundle managed security services to keep the Southeast Asia POS Terminal market growth momentum intact.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption of mPOS Among SMEs and Micro-merchants

- Integration of BNPL Capabilities into POS Hardware

- High Total Cost of Ownership for Modern POS Devices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Contactless payments controlled 56.97% revenue share within the Southeast Asia POS Terminal market in 2025, and the segment is forecast to widen at a 17.05% CAGR through 2031. That dominance positions tap-to-pay as the baseline capability for every new device SKU. Vendors now engineer antenna placement and screen prompts to accelerate sub-two-second checkouts, an attribute that merchants equate with higher throughput. QR fallback remains essential for low-value micro-merchant use cases, ensuring no consumer gets blocked by wallet preference.

Terminal makers are stripping mechanical card slots from entry-level units, dropping component costs while promoting SoftPOS for PIN-on-glass transactions. This evolution underlines how the Southeast Asia POS Terminal market size tied to contactless solutions will eclipse card-only hardware retirements by mid-decade. The push also drives telcos to bundle higher LTE data caps with mPOS subscriptions, reflecting traffic spikes from always-connected firmware updates and analytics pings.

The Southeast Asia POS Terminal Market Report is Segmented by Mode of Payment Acceptance (Contact-Based and Contactless), POS Type (Fixed Point-Of-Sale System and Mobile/Portable Point-Of-Sale Systems), End-User Industry (Retail, Hospitality, Healthcare, Transportation and Logistics, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Worldline SA (Ingenico)

- Verifone Systems LLC

- PAX Technology Ltd.

- NCR Corporation

- Toshiba TEC Corporation

- Newland Payment Technology Co., Ltd.

- HP Inc.

- Samsung Electronics Co., Ltd.

- Fujian Newland Computer Co., Ltd. (Urovo)

- SUNMI Technology Co., Ltd.

- SZZT Electronics Co., Ltd.

- Diebold Nixdorf, Incorporated

- NEC Corporation

- Fujitsu Limited

- BBPOS International Limited

- Centerm Information Co., Ltd.

- New POS Technology Ltd.

- Castles Technology Co., Ltd.

- SUNAR Technology Co., Ltd.

- Squareup International Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid expansion of digital payments across Southeast Asia

- 4.2.2 Government cash-less initiatives and e-payment regulations

- 4.2.3 Rising adoption of mPOS among SMEs and micro-merchants

- 4.2.4 Integration of BNPL capabilities into POS hardware

- 4.2.5 Tourism-driven omnichannel retail recovery post-COVID

- 4.2.6 Migration to Android-based open-OS terminals and app stores

- 4.3 Market Restraints

- 4.3.1 Cyber-security and data-privacy vulnerabilities

- 4.3.2 High total cost of ownership for modern POS devices

- 4.3.3 Fragmented certification rules across SEA nations

- 4.3.4 Weak device-servicing networks beyond tier-1 cities

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Assessment of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Mode of Payment Acceptance

- 5.1.1 Contact-based

- 5.1.2 Contactless

- 5.2 By POS Type

- 5.2.1 Fixed Point-of-Sale Systems

- 5.2.2 Mobile / Portable Point-of-Sale Systems

- 5.3 By End-User Industry

- 5.3.1 Retail

- 5.3.2 Hospitality

- 5.3.3 Healthcare

- 5.3.4 Transportation and Logistics

- 5.3.5 Other End-User Industries

- 5.4 By Country

- 5.4.1 Singapore

- 5.4.2 Malaysia

- 5.4.3 Thailand

- 5.4.4 Indonesia

- 5.4.5 Philippines

- 5.4.6 Vietnam

- 5.4.7 Rest of Southeast Asia

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Worldline SA (Ingenico)

- 6.4.2 Verifone Systems LLC

- 6.4.3 PAX Technology Ltd.

- 6.4.4 NCR Corporation

- 6.4.5 Toshiba TEC Corporation

- 6.4.6 Newland Payment Technology Co., Ltd.

- 6.4.7 HP Inc.

- 6.4.8 Samsung Electronics Co., Ltd.

- 6.4.9 Fujian Newland Computer Co., Ltd. (Urovo)

- 6.4.10 SUNMI Technology Co., Ltd.

- 6.4.11 SZZT Electronics Co., Ltd.

- 6.4.12 Diebold Nixdorf, Incorporated

- 6.4.13 NEC Corporation

- 6.4.14 Fujitsu Limited

- 6.4.15 BBPOS International Limited

- 6.4.16 Centerm Information Co., Ltd.

- 6.4.17 New POS Technology Ltd.

- 6.4.18 Castles Technology Co., Ltd.

- 6.4.19 SUNAR Technology Co., Ltd.

- 6.4.20 Squareup International Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

近距離場通訊 (NFC) POS 終端和支付市場:按組件、產品類型、支付方式、部署模式、組織規模和產業分類-2026-2032 年全球市場預測

近距離場通訊 (NFC) POS 終端和支付市場:按組件、產品類型、支付方式、部署模式、組織規模和產業分類-2026-2032 年全球市場預測 2026年全球銷售點終端市場報告人工智慧終端市場:按組件、組織規模、部署模式、技術、應用和產業分類-2026-2032年全球預測2026年全球零售POS終端市場報告2026年全球餐飲POS終端市場報告POS終端市場按組件、部署方式、外形規格、最終用戶和銷售管道,全球預測,2026-2032年

2026年全球銷售點終端市場報告人工智慧終端市場:按組件、組織規模、部署模式、技術、應用和產業分類-2026-2032年全球預測2026年全球零售POS終端市場報告2026年全球餐飲POS終端市場報告POS終端市場按組件、部署方式、外形規格、最終用戶和銷售管道,全球預測,2026-2032年 POS終端市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶及功能分類銷售點終端市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、部署、最終用戶、功能及安裝模式分類

POS終端市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶及功能分類銷售點終端市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、部署、最終用戶、功能及安裝模式分類 全球POS終端市場規模、佔有率、趨勢及成長分析報告(2026-2034年)非接觸式POS終端全球市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球POS終端市場規模、佔有率、趨勢及成長分析報告(2026-2034年)非接觸式POS終端全球市場規模、佔有率、趨勢和成長分析報告(2026-2034年)